Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5823)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Commerce SS1 Third Term Lesson PlanDocument14 pagesCommerce SS1 Third Term Lesson PlanIvan ObaroNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- La Liga Filipina Discourse Analysis WorkshopDocument3 pagesLa Liga Filipina Discourse Analysis Workshopdasha limNo ratings yet

- Chap008 A SOLDocument13 pagesChap008 A SOLKaif Mohammad HussainNo ratings yet

- Types of ProbabilityDocument17 pagesTypes of Probabilitydasha limNo ratings yet

- Prelim ExamDocument5 pagesPrelim Examdasha limNo ratings yet

- (2 Points) : True FalseDocument11 pages(2 Points) : True Falsedasha limNo ratings yet

- ADV ACCTG Theories1946Document4 pagesADV ACCTG Theories1946dasha limNo ratings yet

- AuditingDocument106 pagesAuditingdasha limNo ratings yet

- December 2014: FOB Term Date Shipped Date Received Invoice Number AmountDocument8 pagesDecember 2014: FOB Term Date Shipped Date Received Invoice Number Amountdasha limNo ratings yet

- This Study Resource Was Shared Via: Discourse Analysis WorkshopDocument2 pagesThis Study Resource Was Shared Via: Discourse Analysis Workshopdasha limNo ratings yet

- Partnership 42Document1 pagePartnership 42dasha limNo ratings yet

- E20 Derivatives PDFDocument4 pagesE20 Derivatives PDFdasha limNo ratings yet

- This Study Resource Was: Pas 41 - AgricultureDocument3 pagesThis Study Resource Was: Pas 41 - Agriculturedasha limNo ratings yet

- NonesDocument15 pagesNonesMary Rose Nones100% (3)

- Pset1 2014Document4 pagesPset1 2014Gualtiero AzzaliniNo ratings yet

- TFLTW IZzp 0 Wqja 6 HDocument5 pagesTFLTW IZzp 0 Wqja 6 HveersainikNo ratings yet

- Arogya Lekha: From ED (HI) 'S Desk.Document7 pagesArogya Lekha: From ED (HI) 'S Desk.Prasannakumar PatilNo ratings yet

- Finmar FormulaDocument2 pagesFinmar FormulaCPAs AccountNo ratings yet

- 2014 Procedures in Approving Apeco Project ProposalDocument1 page2014 Procedures in Approving Apeco Project ProposalDiana Lyn Bello CastilloNo ratings yet

- Proactiveinvestors UK - LWP Technologies Chairman Siegfried Konig in Proactive QA SessionsDocument3 pagesProactiveinvestors UK - LWP Technologies Chairman Siegfried Konig in Proactive QA Sessionsa.hasan670No ratings yet

- SEC. 121. Tax On Banks and Non-Bank Financial Intermediaries.Document3 pagesSEC. 121. Tax On Banks and Non-Bank Financial Intermediaries.Edel MartinezNo ratings yet

- Appollo Ispat Complex LTDDocument155 pagesAppollo Ispat Complex LTDNoor BDNo ratings yet

- Indian Foreign Exchange MarketDocument18 pagesIndian Foreign Exchange MarketAbhimanyu GoyalNo ratings yet

- BTC OptionsDocument15 pagesBTC OptionsJoana CostaNo ratings yet

- Vdocuments - MX - Fria Flow Chart Final 1 PDFDocument44 pagesVdocuments - MX - Fria Flow Chart Final 1 PDFM Grazielle EgeniasNo ratings yet

- Back Office SerivceDocument172 pagesBack Office SerivceAbhijith Pai100% (2)

- Official Presentation Group 1 (Autosaved)Document19 pagesOfficial Presentation Group 1 (Autosaved)Đặng Ngọc ÁnhNo ratings yet

- Stern Corporation Balance SheetDocument4 pagesStern Corporation Balance SheetYessy KawiNo ratings yet

- Spotlight On Spending #16: Sparta World Shooting and Recreation ComplexDocument2 pagesSpotlight On Spending #16: Sparta World Shooting and Recreation ComplexIllinois PolicyNo ratings yet

- Portfolio ManagmentDocument30 pagesPortfolio ManagmentMitali AmagdavNo ratings yet

- ENGIMAN (Outline)Document15 pagesENGIMAN (Outline)Michelle PalconNo ratings yet

- Inflation Learner NotesDocument7 pagesInflation Learner Noteskatolicious638No ratings yet

- Project Report Sonam GuptaDocument89 pagesProject Report Sonam Guptarafeeq505No ratings yet

- Finance Project Rubric 2023Document7 pagesFinance Project Rubric 2023Xansos0% (1)

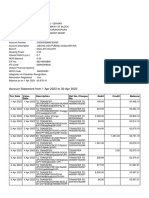

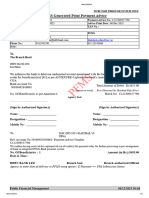

- PFMS Generated Print Payment Advice: To, The Branch HeadDocument2 pagesPFMS Generated Print Payment Advice: To, The Branch HeadAnurag gargNo ratings yet

- Kelompok 7 Anggota: 1.aditiya Bayu Setiaji 2. Nurica Rizky KhasanahDocument2 pagesKelompok 7 Anggota: 1.aditiya Bayu Setiaji 2. Nurica Rizky KhasanahPenatik KisahNo ratings yet

- Jan Martinelli A College Student Has Been Seeking Ways To PDFDocument1 pageJan Martinelli A College Student Has Been Seeking Ways To PDFTaimur TechnologistNo ratings yet

- Jyothirmayi PaperDocument2 pagesJyothirmayi PapermnnappajiNo ratings yet

- Acquisition and Restructuring StrategiesDocument14 pagesAcquisition and Restructuring Strategiesvipulp_10No ratings yet

- Bank Account Updation FormDocument2 pagesBank Account Updation Forms.sabapathyNo ratings yet

- Deposit Slip CertificateDocument1 pageDeposit Slip CertificateMalou AblazaNo ratings yet

- Compromise Proposal For Rs. For Settlement of Loan Account No of M/s. / Shri / Smt.Document2 pagesCompromise Proposal For Rs. For Settlement of Loan Account No of M/s. / Shri / Smt.Arvind VarmaNo ratings yet