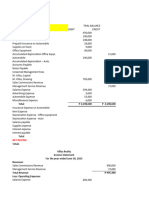

Profit After Tax: Revenue 25% Contribution Margin (% Change From Last y - 2%

Profit After Tax: Revenue 25% Contribution Margin (% Change From Last y - 2%

You might also like

- FULL Download Ebook PDF Introduction To Finance Markets Investments and Financial Management 15th Edition PDF EbookDocument41 pagesFULL Download Ebook PDF Introduction To Finance Markets Investments and Financial Management 15th Edition PDF Ebookdavid.conrad655100% (39)

- Far110 Group Assignment 2Document7 pagesFar110 Group Assignment 21ANurul AnisNo ratings yet

- Noreen5e Appendix07C TB AnswerKeyDocument214 pagesNoreen5e Appendix07C TB AnswerKeyLeighNo ratings yet

- Case 2 Marking SchemeDocument22 pagesCase 2 Marking SchemeHello100% (1)

- Allied Food Products: A Case StudyDocument18 pagesAllied Food Products: A Case StudyMikey MadRatNo ratings yet

- Mini Project CAIA (Financial Statement)Document2 pagesMini Project CAIA (Financial Statement)norizzatisyamrilNo ratings yet

- Sales Type Lease - LessorDocument19 pagesSales Type Lease - LessorRogelynCodillaNo ratings yet

- Itemized: Gross Income From OperationsDocument9 pagesItemized: Gross Income From OperationsLyka RoguelNo ratings yet

- Particulars Taka Taka TakaDocument2 pagesParticulars Taka Taka TakaTushar Mahmud SizanNo ratings yet

- Activity 3Document1 pageActivity 3John Michael Gaoiran GajotanNo ratings yet

- M.rifli P5.3 Akuntansi PengantarDocument5 pagesM.rifli P5.3 Akuntansi PengantarRafli AgustianNo ratings yet

- Solution Problem On Project EvaluationDocument5 pagesSolution Problem On Project EvaluationHasanNo ratings yet

- 1Document20 pages1Denver AcenasNo ratings yet

- Reviewer Quiz 4Document21 pagesReviewer Quiz 4Jessica Mikah Lim AgbayaniNo ratings yet

- FIN702: Corporate Financial Management 1 Tutorial 2: Financial Statement AnalysisDocument3 pagesFIN702: Corporate Financial Management 1 Tutorial 2: Financial Statement AnalysisBetcy RaetoraNo ratings yet

- ACCT 1107 - Assignment #4Document3 pagesACCT 1107 - Assignment #4hkarim8641No ratings yet

- Illustrative Problem - Sales Type Lease With Residual ValueDocument2 pagesIllustrative Problem - Sales Type Lease With Residual ValueQueen ValleNo ratings yet

- FinalDocument2 pagesFinalAyla BalmesNo ratings yet

- Trial Balance CompletedDocument1 pageTrial Balance CompletedapachemonoNo ratings yet

- DagohoyDocument6 pagesDagohoylinkin soyNo ratings yet

- Example For Chapter 2 (FABM2)Document10 pagesExample For Chapter 2 (FABM2)Althea BañaciaNo ratings yet

- Description Income Expenses Assets LiabilitiesDocument12 pagesDescription Income Expenses Assets LiabilitiesNipuna Perera100% (1)

- August Q1Document3 pagesAugust Q1tengku rilNo ratings yet

- Kertas Kerja Neraca LajurDocument11 pagesKertas Kerja Neraca LajurSri Winarsih RamadanaNo ratings yet

- Case Study Invetment DecisionDocument8 pagesCase Study Invetment DecisionKelsy NguyenNo ratings yet

- 3 Exam Part IDocument6 pages3 Exam Part IRJ DAVE DURUHANo ratings yet

- Assignment-5-Single-Entry-Method-students-DAVID FinalDocument11 pagesAssignment-5-Single-Entry-Method-students-DAVID FinalJOY MARIE RONATONo ratings yet

- Exercise Lecture 2 Cash FlowDocument2 pagesExercise Lecture 2 Cash Flowdebbie intanNo ratings yet

- Is Fishing Non Motorized BangkaDocument4 pagesIs Fishing Non Motorized BangkaAnonymous EvbW4o1U7No ratings yet

- BLT FINAL Assignment (Feb - June 2020) FINALDocument16 pagesBLT FINAL Assignment (Feb - June 2020) FINALSalman SajidNo ratings yet

- Assessment 1 - Assignment 1Document5 pagesAssessment 1 - Assignment 1Ten NineNo ratings yet

- Ffa ADocument5 pagesFfa Aaccounts officerNo ratings yet

- Advanced Accounting 2CDocument5 pagesAdvanced Accounting 2CHarusiNo ratings yet

- Financial Accounting hw1Document5 pagesFinancial Accounting hw1Jermaine M. SantoyoNo ratings yet

- Laporan Laba Rugi PT PUTRA BANUA - ISMI FATMASYARIDocument1 pageLaporan Laba Rugi PT PUTRA BANUA - ISMI FATMASYARIIsmi FatmasyariNo ratings yet

- Book 1Document6 pagesBook 1chrstncstlljNo ratings yet

- Financial Analysis DashboardDocument11 pagesFinancial Analysis DashboardZidan ZaifNo ratings yet

- Non-Current Asset: Balance Sheet 31-Dec-20Document4 pagesNon-Current Asset: Balance Sheet 31-Dec-20Shehzadi Mahum (F-Name :Sohail Ahmed)No ratings yet

- Ice NineDocument4 pagesIce NinePolene GomezNo ratings yet

- BADVAC1XDocument8 pagesBADVAC1Xfaye pantiNo ratings yet

- Latihan P7-4Document6 pagesLatihan P7-4ryuNo ratings yet

- Compe SolutionDocument10 pagesCompe SolutionRianell Andrea AsumbradoNo ratings yet

- Pricilla AssignmentDocument3 pagesPricilla AssignmentjasonnumahnalkelNo ratings yet

- Invincble Manufacturing Balance SheetDocument4 pagesInvincble Manufacturing Balance SheetArjun Pratap SinghNo ratings yet

- Project Information Project 1Document8 pagesProject Information Project 1biniamNo ratings yet

- Module 2 - Financial StatementsDocument6 pagesModule 2 - Financial Statementskemifawole13No ratings yet

- Madaraka Ltd. Statement of Comprehensive Income For The Year Ended 31 March 2020 KES'000' KES'000'Document17 pagesMadaraka Ltd. Statement of Comprehensive Income For The Year Ended 31 March 2020 KES'000' KES'000'Maryjoy KilonzoNo ratings yet

- Accounts List Summary PDFDocument2 pagesAccounts List Summary PDFOkie FernandaNo ratings yet

- Paragon SPL & SFP With AnswerDocument3 pagesParagon SPL & SFP With Answerramyaa baluNo ratings yet

- AACA2 AssignmentsDocument20 pagesAACA2 AssignmentsadieNo ratings yet

- Kertas Kerja UAS IchaDocument30 pagesKertas Kerja UAS Ichaaida anumNo ratings yet

- PYQ June 2018Document4 pagesPYQ June 2018Nur Amira NadiaNo ratings yet

- Mount Carmel School of Maria Aurora, Inc. Maria Aurora, 3202 AuroraDocument5 pagesMount Carmel School of Maria Aurora, Inc. Maria Aurora, 3202 AuroraZoe Vera S. AcainNo ratings yet

- 2022 12 01 Answer Key Additional M6 M7Document15 pages2022 12 01 Answer Key Additional M6 M7Niger RomeNo ratings yet

- Irene LaguioDocument18 pagesIrene LaguioAlvinNoay100% (2)

- 5.ast - Installment & FranchisingDocument12 pages5.ast - Installment & FranchisingElaineJrV-IgotNo ratings yet

- Uas Metode KuantitifDocument12 pagesUas Metode Kuantitifariyanto wibowoNo ratings yet

- AliyaDocument6 pagesAliyaaserbeyene29No ratings yet

- WorkDocument4 pagesWorkhassan KyendoNo ratings yet

- Dream World CompanyDocument9 pagesDream World CompanyJC NicaveraNo ratings yet

- 8447809Document11 pages8447809blackghostNo ratings yet

- BT Tổng Hợp Topic 7 8 2Document12 pagesBT Tổng Hợp Topic 7 8 2Man Tran Y NhiNo ratings yet

- China Tea CompanyDocument4 pagesChina Tea CompanyLeika Gay Soriano OlarteNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- The Rise of Uber and Regulating The Disruptive Innovator: The Political Quarterly May 2017Document9 pagesThe Rise of Uber and Regulating The Disruptive Innovator: The Political Quarterly May 2017Henry TranNo ratings yet

- Checklist For Permanent Residence Permit - UDIDocument9 pagesChecklist For Permanent Residence Permit - UDIHenry TranNo ratings yet

- Exploring The Taxi and Uber Demand in New York City: An Empirical Analysis and Spatial ModelingDocument20 pagesExploring The Taxi and Uber Demand in New York City: An Empirical Analysis and Spatial ModelingHenry TranNo ratings yet

- 07 Privacy and SurveillanceDocument57 pages07 Privacy and SurveillanceHenry TranNo ratings yet

- CFA Questions and SolutionsDocument16 pagesCFA Questions and Solutionsvip_thb_2007100% (1)

- Fim Model SolutionDocument7 pagesFim Model Solutionhyp siinNo ratings yet

- Case Study On DHPLDocument7 pagesCase Study On DHPLUtkarsh PandeyNo ratings yet

- Rosewood Case SolutionDocument15 pagesRosewood Case SolutionSecond FloorNo ratings yet

- Some ExercisesDocument3 pagesSome ExercisesMinh Tâm NguyễnNo ratings yet

- ASE20104 Examiner Report - March 2018Document20 pagesASE20104 Examiner Report - March 2018Aung Zaw HtweNo ratings yet

- CHAPTER - 5 Capital Budgeting & Investment DecisionDocument40 pagesCHAPTER - 5 Capital Budgeting & Investment Decisionethnan lNo ratings yet

- CPALE CoverageDocument15 pagesCPALE CoverageMajariya Sahar SabladNo ratings yet

- 54594bos43759 p3 PDFDocument23 pages54594bos43759 p3 PDFWaleed Bin RaoufNo ratings yet

- Week 1 Practice QuizDocument7 pagesWeek 1 Practice QuizDonald112100% (1)

- Finmkt FinalsDocument6 pagesFinmkt FinalsMary Elisha PinedaNo ratings yet

- Project Evaluation Techniques: Discounted Cash Flow and Non-Discounted Cash Flow MethodsDocument32 pagesProject Evaluation Techniques: Discounted Cash Flow and Non-Discounted Cash Flow Methodsfarihafairuz100% (1)

- Kuratko 9 e CH 11Document40 pagesKuratko 9 e CH 11lobna_qassem7176No ratings yet

- K9FuelBar An Energy Treat For Dogs Case AnalysisDocument9 pagesK9FuelBar An Energy Treat For Dogs Case AnalysisRizki EkaNo ratings yet

- Course Code: MCO-07 Course Title: Financial Management Assignment Code: MCO-07/TMA/2020-2021 Coverage: All BlocksDocument9 pagesCourse Code: MCO-07 Course Title: Financial Management Assignment Code: MCO-07/TMA/2020-2021 Coverage: All Blockssubhaa DasNo ratings yet

- Financial Concepts 1Document16 pagesFinancial Concepts 1shaonNo ratings yet

- International Capital BudgetingDocument28 pagesInternational Capital BudgetingMatt ToothacreNo ratings yet

- Empirical Chemicals LTD: Merseyside Project: Case StudyDocument20 pagesEmpirical Chemicals LTD: Merseyside Project: Case Study1b2m3100% (1)

- Project SelectingDocument29 pagesProject SelectingayyazmNo ratings yet

- Document 3Document4 pagesDocument 3Zainab ImranNo ratings yet

- Feasibility Study For Assembly of Bicycle Project Proposal Business Plan in Ethiopia. - Haqiqa Investment Consultant in EthiopiaDocument1 pageFeasibility Study For Assembly of Bicycle Project Proposal Business Plan in Ethiopia. - Haqiqa Investment Consultant in EthiopiaSuleman100% (1)

- Coke Mini-CaseDocument2 pagesCoke Mini-CaseKing CheungNo ratings yet

- Paper Exposed Ore ReserveDocument9 pagesPaper Exposed Ore ReserveMatías Ignacio Loyola GaldamesNo ratings yet

- CHAPTER 4 Financial AspectDocument18 pagesCHAPTER 4 Financial AspectShan ShanNo ratings yet

- Economic Value Added: A Better Technique For Performance MeasurementDocument12 pagesEconomic Value Added: A Better Technique For Performance MeasurementIshita GuptaNo ratings yet

- Capital BudgetingDocument2 pagesCapital BudgetingRonielyn CustodioNo ratings yet

Download as xlsx, pdf, or txt

You might also like

- FULL Download Ebook PDF Introduction To Finance Markets Investments and Financial Management 15th Edition PDF EbookDocument41 pagesFULL Download Ebook PDF Introduction To Finance Markets Investments and Financial Management 15th Edition PDF Ebookdavid.conrad655100% (39)

- Far110 Group Assignment 2Document7 pagesFar110 Group Assignment 21ANurul AnisNo ratings yet

- Noreen5e Appendix07C TB AnswerKeyDocument214 pagesNoreen5e Appendix07C TB AnswerKeyLeighNo ratings yet

- Case 2 Marking SchemeDocument22 pagesCase 2 Marking SchemeHello100% (1)

- Allied Food Products: A Case StudyDocument18 pagesAllied Food Products: A Case StudyMikey MadRatNo ratings yet

- Mini Project CAIA (Financial Statement)Document2 pagesMini Project CAIA (Financial Statement)norizzatisyamrilNo ratings yet

- Sales Type Lease - LessorDocument19 pagesSales Type Lease - LessorRogelynCodillaNo ratings yet

- Itemized: Gross Income From OperationsDocument9 pagesItemized: Gross Income From OperationsLyka RoguelNo ratings yet

- Particulars Taka Taka TakaDocument2 pagesParticulars Taka Taka TakaTushar Mahmud SizanNo ratings yet

- Activity 3Document1 pageActivity 3John Michael Gaoiran GajotanNo ratings yet

- M.rifli P5.3 Akuntansi PengantarDocument5 pagesM.rifli P5.3 Akuntansi PengantarRafli AgustianNo ratings yet

- Solution Problem On Project EvaluationDocument5 pagesSolution Problem On Project EvaluationHasanNo ratings yet

- 1Document20 pages1Denver AcenasNo ratings yet

- Reviewer Quiz 4Document21 pagesReviewer Quiz 4Jessica Mikah Lim AgbayaniNo ratings yet

- FIN702: Corporate Financial Management 1 Tutorial 2: Financial Statement AnalysisDocument3 pagesFIN702: Corporate Financial Management 1 Tutorial 2: Financial Statement AnalysisBetcy RaetoraNo ratings yet

- ACCT 1107 - Assignment #4Document3 pagesACCT 1107 - Assignment #4hkarim8641No ratings yet

- Illustrative Problem - Sales Type Lease With Residual ValueDocument2 pagesIllustrative Problem - Sales Type Lease With Residual ValueQueen ValleNo ratings yet

- FinalDocument2 pagesFinalAyla BalmesNo ratings yet

- Trial Balance CompletedDocument1 pageTrial Balance CompletedapachemonoNo ratings yet

- DagohoyDocument6 pagesDagohoylinkin soyNo ratings yet

- Example For Chapter 2 (FABM2)Document10 pagesExample For Chapter 2 (FABM2)Althea BañaciaNo ratings yet

- Description Income Expenses Assets LiabilitiesDocument12 pagesDescription Income Expenses Assets LiabilitiesNipuna Perera100% (1)

- August Q1Document3 pagesAugust Q1tengku rilNo ratings yet

- Kertas Kerja Neraca LajurDocument11 pagesKertas Kerja Neraca LajurSri Winarsih RamadanaNo ratings yet

- Case Study Invetment DecisionDocument8 pagesCase Study Invetment DecisionKelsy NguyenNo ratings yet

- 3 Exam Part IDocument6 pages3 Exam Part IRJ DAVE DURUHANo ratings yet

- Assignment-5-Single-Entry-Method-students-DAVID FinalDocument11 pagesAssignment-5-Single-Entry-Method-students-DAVID FinalJOY MARIE RONATONo ratings yet

- Exercise Lecture 2 Cash FlowDocument2 pagesExercise Lecture 2 Cash Flowdebbie intanNo ratings yet

- Is Fishing Non Motorized BangkaDocument4 pagesIs Fishing Non Motorized BangkaAnonymous EvbW4o1U7No ratings yet

- BLT FINAL Assignment (Feb - June 2020) FINALDocument16 pagesBLT FINAL Assignment (Feb - June 2020) FINALSalman SajidNo ratings yet

- Assessment 1 - Assignment 1Document5 pagesAssessment 1 - Assignment 1Ten NineNo ratings yet

- Ffa ADocument5 pagesFfa Aaccounts officerNo ratings yet

- Advanced Accounting 2CDocument5 pagesAdvanced Accounting 2CHarusiNo ratings yet

- Financial Accounting hw1Document5 pagesFinancial Accounting hw1Jermaine M. SantoyoNo ratings yet

- Laporan Laba Rugi PT PUTRA BANUA - ISMI FATMASYARIDocument1 pageLaporan Laba Rugi PT PUTRA BANUA - ISMI FATMASYARIIsmi FatmasyariNo ratings yet

- Book 1Document6 pagesBook 1chrstncstlljNo ratings yet

- Financial Analysis DashboardDocument11 pagesFinancial Analysis DashboardZidan ZaifNo ratings yet

- Non-Current Asset: Balance Sheet 31-Dec-20Document4 pagesNon-Current Asset: Balance Sheet 31-Dec-20Shehzadi Mahum (F-Name :Sohail Ahmed)No ratings yet

- Ice NineDocument4 pagesIce NinePolene GomezNo ratings yet

- BADVAC1XDocument8 pagesBADVAC1Xfaye pantiNo ratings yet

- Latihan P7-4Document6 pagesLatihan P7-4ryuNo ratings yet

- Compe SolutionDocument10 pagesCompe SolutionRianell Andrea AsumbradoNo ratings yet

- Pricilla AssignmentDocument3 pagesPricilla AssignmentjasonnumahnalkelNo ratings yet

- Invincble Manufacturing Balance SheetDocument4 pagesInvincble Manufacturing Balance SheetArjun Pratap SinghNo ratings yet

- Project Information Project 1Document8 pagesProject Information Project 1biniamNo ratings yet

- Module 2 - Financial StatementsDocument6 pagesModule 2 - Financial Statementskemifawole13No ratings yet

- Madaraka Ltd. Statement of Comprehensive Income For The Year Ended 31 March 2020 KES'000' KES'000'Document17 pagesMadaraka Ltd. Statement of Comprehensive Income For The Year Ended 31 March 2020 KES'000' KES'000'Maryjoy KilonzoNo ratings yet

- Accounts List Summary PDFDocument2 pagesAccounts List Summary PDFOkie FernandaNo ratings yet

- Paragon SPL & SFP With AnswerDocument3 pagesParagon SPL & SFP With Answerramyaa baluNo ratings yet

- AACA2 AssignmentsDocument20 pagesAACA2 AssignmentsadieNo ratings yet

- Kertas Kerja UAS IchaDocument30 pagesKertas Kerja UAS Ichaaida anumNo ratings yet

- PYQ June 2018Document4 pagesPYQ June 2018Nur Amira NadiaNo ratings yet

- Mount Carmel School of Maria Aurora, Inc. Maria Aurora, 3202 AuroraDocument5 pagesMount Carmel School of Maria Aurora, Inc. Maria Aurora, 3202 AuroraZoe Vera S. AcainNo ratings yet

- 2022 12 01 Answer Key Additional M6 M7Document15 pages2022 12 01 Answer Key Additional M6 M7Niger RomeNo ratings yet

- Irene LaguioDocument18 pagesIrene LaguioAlvinNoay100% (2)

- 5.ast - Installment & FranchisingDocument12 pages5.ast - Installment & FranchisingElaineJrV-IgotNo ratings yet

- Uas Metode KuantitifDocument12 pagesUas Metode Kuantitifariyanto wibowoNo ratings yet

- AliyaDocument6 pagesAliyaaserbeyene29No ratings yet

- WorkDocument4 pagesWorkhassan KyendoNo ratings yet

- Dream World CompanyDocument9 pagesDream World CompanyJC NicaveraNo ratings yet

- 8447809Document11 pages8447809blackghostNo ratings yet

- BT Tổng Hợp Topic 7 8 2Document12 pagesBT Tổng Hợp Topic 7 8 2Man Tran Y NhiNo ratings yet

- China Tea CompanyDocument4 pagesChina Tea CompanyLeika Gay Soriano OlarteNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- The Rise of Uber and Regulating The Disruptive Innovator: The Political Quarterly May 2017Document9 pagesThe Rise of Uber and Regulating The Disruptive Innovator: The Political Quarterly May 2017Henry TranNo ratings yet

- Checklist For Permanent Residence Permit - UDIDocument9 pagesChecklist For Permanent Residence Permit - UDIHenry TranNo ratings yet

- Exploring The Taxi and Uber Demand in New York City: An Empirical Analysis and Spatial ModelingDocument20 pagesExploring The Taxi and Uber Demand in New York City: An Empirical Analysis and Spatial ModelingHenry TranNo ratings yet

- 07 Privacy and SurveillanceDocument57 pages07 Privacy and SurveillanceHenry TranNo ratings yet

- CFA Questions and SolutionsDocument16 pagesCFA Questions and Solutionsvip_thb_2007100% (1)

- Fim Model SolutionDocument7 pagesFim Model Solutionhyp siinNo ratings yet

- Case Study On DHPLDocument7 pagesCase Study On DHPLUtkarsh PandeyNo ratings yet

- Rosewood Case SolutionDocument15 pagesRosewood Case SolutionSecond FloorNo ratings yet

- Some ExercisesDocument3 pagesSome ExercisesMinh Tâm NguyễnNo ratings yet

- ASE20104 Examiner Report - March 2018Document20 pagesASE20104 Examiner Report - March 2018Aung Zaw HtweNo ratings yet

- CHAPTER - 5 Capital Budgeting & Investment DecisionDocument40 pagesCHAPTER - 5 Capital Budgeting & Investment Decisionethnan lNo ratings yet

- CPALE CoverageDocument15 pagesCPALE CoverageMajariya Sahar SabladNo ratings yet

- 54594bos43759 p3 PDFDocument23 pages54594bos43759 p3 PDFWaleed Bin RaoufNo ratings yet

- Week 1 Practice QuizDocument7 pagesWeek 1 Practice QuizDonald112100% (1)

- Finmkt FinalsDocument6 pagesFinmkt FinalsMary Elisha PinedaNo ratings yet

- Project Evaluation Techniques: Discounted Cash Flow and Non-Discounted Cash Flow MethodsDocument32 pagesProject Evaluation Techniques: Discounted Cash Flow and Non-Discounted Cash Flow Methodsfarihafairuz100% (1)

- Kuratko 9 e CH 11Document40 pagesKuratko 9 e CH 11lobna_qassem7176No ratings yet

- K9FuelBar An Energy Treat For Dogs Case AnalysisDocument9 pagesK9FuelBar An Energy Treat For Dogs Case AnalysisRizki EkaNo ratings yet

- Course Code: MCO-07 Course Title: Financial Management Assignment Code: MCO-07/TMA/2020-2021 Coverage: All BlocksDocument9 pagesCourse Code: MCO-07 Course Title: Financial Management Assignment Code: MCO-07/TMA/2020-2021 Coverage: All Blockssubhaa DasNo ratings yet

- Financial Concepts 1Document16 pagesFinancial Concepts 1shaonNo ratings yet

- International Capital BudgetingDocument28 pagesInternational Capital BudgetingMatt ToothacreNo ratings yet

- Empirical Chemicals LTD: Merseyside Project: Case StudyDocument20 pagesEmpirical Chemicals LTD: Merseyside Project: Case Study1b2m3100% (1)

- Project SelectingDocument29 pagesProject SelectingayyazmNo ratings yet

- Document 3Document4 pagesDocument 3Zainab ImranNo ratings yet

- Feasibility Study For Assembly of Bicycle Project Proposal Business Plan in Ethiopia. - Haqiqa Investment Consultant in EthiopiaDocument1 pageFeasibility Study For Assembly of Bicycle Project Proposal Business Plan in Ethiopia. - Haqiqa Investment Consultant in EthiopiaSuleman100% (1)

- Coke Mini-CaseDocument2 pagesCoke Mini-CaseKing CheungNo ratings yet

- Paper Exposed Ore ReserveDocument9 pagesPaper Exposed Ore ReserveMatías Ignacio Loyola GaldamesNo ratings yet

- CHAPTER 4 Financial AspectDocument18 pagesCHAPTER 4 Financial AspectShan ShanNo ratings yet

- Economic Value Added: A Better Technique For Performance MeasurementDocument12 pagesEconomic Value Added: A Better Technique For Performance MeasurementIshita GuptaNo ratings yet

- Capital BudgetingDocument2 pagesCapital BudgetingRonielyn CustodioNo ratings yet