Download as pdf or txt

You might also like

- Normas NES M1019Document12 pagesNormas NES M1019Margarita Torres FloresNo ratings yet

- Least Mastered Competencies (Grade 6)Document14 pagesLeast Mastered Competencies (Grade 6)Renge Taña91% (33)

- The Essentials of Psychodynamic PsychotherapyDocument6 pagesThe Essentials of Psychodynamic PsychotherapyMarthaRamirez100% (3)

- Statement of Transactions: Sundaram Finance LimitedDocument1 pageStatement of Transactions: Sundaram Finance LimitedBhavin SagarNo ratings yet

- Bengal & Assam CompanyDocument64 pagesBengal & Assam Companyvishal_patil_3No ratings yet

- Mohit Agro Gujarat AmbujaDocument20 pagesMohit Agro Gujarat AmbujaMuskan KhatriNo ratings yet

- Fairness OpinionDocument8 pagesFairness OpinionMyush SharmaNo ratings yet

- Sunrise Efficient Marketing LimitedDocument83 pagesSunrise Efficient Marketing Limitedanady135344No ratings yet

- Valuation Report Final SSPL PDFDocument8 pagesValuation Report Final SSPL PDFbts foreverNo ratings yet

- Annual Reports 16 17 BrilaDocument246 pagesAnnual Reports 16 17 BrilaMAYUGAMNo ratings yet

- Floor 25, Phiroze Jeejeebhoy Towers, Dalal Street: February 07, 2024Document6 pagesFloor 25, Phiroze Jeejeebhoy Towers, Dalal Street: February 07, 2024contact.rohitkapseNo ratings yet

- 31032022Document115 pages31032022Mohammad ZaidNo ratings yet

- ACAPL - Valuation Report - May, 2023Document16 pagesACAPL - Valuation Report - May, 2023Shashi Bhushan PrinceNo ratings yet

- Ar 2017 2018Document77 pagesAr 2017 2018shark123No ratings yet

- Type Text HereDocument9 pagesType Text HerevineminaiNo ratings yet

- MUGHAL 2017 Mughal Iron & Steel Industries Limited - Text.markedDocument86 pagesMUGHAL 2017 Mughal Iron & Steel Industries Limited - Text.markedKanwal YaseenNo ratings yet

- Ar14 15Document142 pagesAr14 15Divey AhujaNo ratings yet

- Gul Ahmed Annual Report 2007Document73 pagesGul Ahmed Annual Report 2007AISHASABAHATNo ratings yet

- Kesar Terminals & Infrastructure LTDDocument118 pagesKesar Terminals & Infrastructure LTDSanjeev AggarwalNo ratings yet

- Akash M&ADocument6 pagesAkash M&Aakshali raneNo ratings yet

- Jayaswal Neco PDFDocument117 pagesJayaswal Neco PDFSUKHSAGAR1969No ratings yet

- SaregamaDocument147 pagesSaregamaHarish BahraNo ratings yet

- Man KasiaDocument81 pagesMan KasiaSUKHSAGAR1969No ratings yet

- Reg 30 Outcomeof BMResults Q1 FY2020Document12 pagesReg 30 Outcomeof BMResults Q1 FY2020Dipanshu NagarNo ratings yet

- HDFC Sales Pvt. Ltd.Document16 pagesHDFC Sales Pvt. Ltd.Shankar AjNo ratings yet

- Vision Comptech LTD 2007Document10 pagesVision Comptech LTD 2007Debkumar958No ratings yet

- Balrampur Chini Q4FY20Document21 pagesBalrampur Chini Q4FY20premNo ratings yet

- 15 637994517915958750 AnnualReportDocument210 pages15 637994517915958750 AnnualReportAkanksha SinghNo ratings yet

- Arshiya: National Stock Exchange of India Limited BSE LimitedDocument28 pagesArshiya: National Stock Exchange of India Limited BSE Limitednaresh kayadNo ratings yet

- HFCL Infotel Ltd.Document159 pagesHFCL Infotel Ltd.deepgogna0% (1)

- MPL FR An 2018 19Document82 pagesMPL FR An 2018 19Jähäñ ShërNo ratings yet

- Asian Paints Q2FY24 ResultsDocument15 pagesAsian Paints Q2FY24 ResultskawatgharerNo ratings yet

- 100 200 Full Agm Egm 20230227Document15 pages100 200 Full Agm Egm 20230227Contra Value BetsNo ratings yet

- Circular To ShareholdersDocument16 pagesCircular To Shareholdersharithh.rahsiaNo ratings yet

- BMRCL English Annual Report - 2021-22Document180 pagesBMRCL English Annual Report - 2021-22Hemant SinhmarNo ratings yet

- Jaimni Astrology A Case Study of A Systems Analyst Chara DashaDocument138 pagesJaimni Astrology A Case Study of A Systems Analyst Chara DashaPoonam AggarwalNo ratings yet

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Document11 pagesStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- 0 637655289821812500 AnnualReportDocument200 pages0 637655289821812500 AnnualReportShray GargNo ratings yet

- Shakti Wears Private Limited 112, Navjeevan Complex, Station Road, JaipurDocument5 pagesShakti Wears Private Limited 112, Navjeevan Complex, Station Road, JaipurArnish SharmaNo ratings yet

- Solara Active AbridgedDocument12 pagesSolara Active AbridgedhaadritiNo ratings yet

- Annual Report - FY 2018-19Document17 pagesAnnual Report - FY 2018-19malepati prudhvirajNo ratings yet

- Ba 2019Document117 pagesBa 2019Code NameNo ratings yet

- BIS List of 946 Items 5Document82 pagesBIS List of 946 Items 5AvijitSinharoyNo ratings yet

- LKP Finance Limited: 26 ANNUAL REPORT 2009-2010Document43 pagesLKP Finance Limited: 26 ANNUAL REPORT 2009-2010vikas_ojha54706No ratings yet

- UntitledDocument14 pagesUntitledContra Value BetsNo ratings yet

- 2012 SCC Online Guj 5453: (2013) 176 Comp Cas 217: (2013) 112 Cla 234Document12 pages2012 SCC Online Guj 5453: (2013) 176 Comp Cas 217: (2013) 112 Cla 234devanshi jainNo ratings yet

- Kallam Spinning Mills LTDDocument42 pagesKallam Spinning Mills LTDSIVAKUMARNo ratings yet

- 2000 5000 Full Company Update 20230309Document40 pages2000 5000 Full Company Update 20230309Contra Value BetsNo ratings yet

- Annual Report For The Financial Year 2013-2014: Magma Advisory Services LimitedDocument24 pagesAnnual Report For The Financial Year 2013-2014: Magma Advisory Services Limitedvishal sharmaNo ratings yet

- Dunlop India Limited 2012 PDFDocument10 pagesDunlop India Limited 2012 PDFdidwaniasNo ratings yet

- Ultra TechDocument208 pagesUltra TechOp FfNo ratings yet

- B L Kashyap Annual ReportDocument106 pagesB L Kashyap Annual ReportPrashant KumarNo ratings yet

- Annual Report 2017 Sree Rayalseema Hi PDFDocument115 pagesAnnual Report 2017 Sree Rayalseema Hi PDFSukhsagar AggarwalNo ratings yet

- 137595Document106 pages137595haya.noor11200No ratings yet

- Engro Notice Scheme of Emloyee Stock Options PDFDocument3 pagesEngro Notice Scheme of Emloyee Stock Options PDFFahad MansooriNo ratings yet

- Annual PDFDocument264 pagesAnnual PDFShubham AhujaNo ratings yet

- Valuation ReportDocument11 pagesValuation ReportVani PattnaikNo ratings yet

- Annual Report 2023Document86 pagesAnnual Report 2023waleedsheikh356No ratings yet

- Cera Annual ReportDocument81 pagesCera Annual ReportSingh HarmanNo ratings yet

- Hero Motocorp LTD.: Regd. Office: The Grand Plaza, Plot No. 2, Nelson Mandela RoadDocument12 pagesHero Motocorp LTD.: Regd. Office: The Grand Plaza, Plot No. 2, Nelson Mandela Roadsakshamjain4711No ratings yet

- Prakash Industries LimitedDocument119 pagesPrakash Industries Limitedvivektiwari9229No ratings yet

- Annual Report 2013 - 14 Esaar India LimitedDocument47 pagesAnnual Report 2013 - 14 Esaar India LimitedRishikesh KashyapNo ratings yet

- MPL FR An 2016 17Document76 pagesMPL FR An 2016 17Jähäñ ShërNo ratings yet

- Bse Sme Ipo IndexDocument4 pagesBse Sme Ipo IndexBhavin SagarNo ratings yet

- August 2021 - Shipping Corporation of India LTD by Corporate ProfessionalsDocument10 pagesAugust 2021 - Shipping Corporation of India LTD by Corporate ProfessionalsBhavin SagarNo ratings yet

- Qtrly - Reportq1 FY 2008 2009Document2 pagesQtrly - Reportq1 FY 2008 2009Bhavin SagarNo ratings yet

- Yap 31 1 19Document345 pagesYap 31 1 19Bhavin SagarNo ratings yet

- Nebbia Mutual NDADocument3 pagesNebbia Mutual NDABhavin SagarNo ratings yet

- Revised Market Making Agreement 31.03Document13 pagesRevised Market Making Agreement 31.03Bhavin SagarNo ratings yet

- Revised Underwriting Agreement 31.03Document14 pagesRevised Underwriting Agreement 31.03Bhavin SagarNo ratings yet

- Capital Reduction - Escorts LTD - GalacticoDocument10 pagesCapital Reduction - Escorts LTD - GalacticoBhavin SagarNo ratings yet

- Revised RV - Draft Valuation Report - Hakuna MatataDocument11 pagesRevised RV - Draft Valuation Report - Hakuna MatataBhavin SagarNo ratings yet

- List of Valuation ReportsDocument18 pagesList of Valuation ReportsBhavin SagarNo ratings yet

- 01 Business Partnership Powerpoint TemplateDocument12 pages01 Business Partnership Powerpoint TemplateBhavin SagarNo ratings yet

- 02 Corporate Orange Powerpoint Presentations 16x9 1Document13 pages02 Corporate Orange Powerpoint Presentations 16x9 1Bhavin SagarNo ratings yet

- MCA FinanicialsDocument50 pagesMCA FinanicialsBhavin SagarNo ratings yet

- 01 Business Partnership Powerpoint TemplateDocument12 pages01 Business Partnership Powerpoint TemplateBhavin SagarNo ratings yet

- EKI Energy Services Limited: Payments MadeDocument2 pagesEKI Energy Services Limited: Payments MadeBhavin SagarNo ratings yet

- Corporate Deck - InternationalDocument16 pagesCorporate Deck - InternationalBhavin SagarNo ratings yet

- Bulk DealsDocument63 pagesBulk DealsBhavin SagarNo ratings yet

- EKI Energy Services Limited: Payments MadeDocument2 pagesEKI Energy Services Limited: Payments MadeBhavin SagarNo ratings yet

- Valuation Assignement - WIPDocument2 pagesValuation Assignement - WIPBhavin SagarNo ratings yet

- Bhavin Valuation Cases For FY21Document17 pagesBhavin Valuation Cases For FY21Bhavin SagarNo ratings yet

- Bhavin - Valuation Cases - May 2021Document3 pagesBhavin - Valuation Cases - May 2021Bhavin SagarNo ratings yet

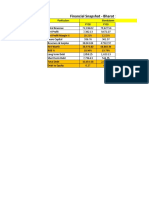

- Bharat Serums & Vaccines LTD - Financial SnapshotDocument2 pagesBharat Serums & Vaccines LTD - Financial SnapshotBhavin SagarNo ratings yet

- Senwa Mobile - S615 - Android 3.5inDocument6 pagesSenwa Mobile - S615 - Android 3.5inSERGIO_MANNo ratings yet

- Print - Udyam Registration CertificateDocument2 pagesPrint - Udyam Registration CertificatesahityaasthaNo ratings yet

- Multiple Choice - JOCDocument14 pagesMultiple Choice - JOCMuriel MahanludNo ratings yet

- The 40 Verse Hanuman Chalisa English Translation - From Ajit Vadakayil BlogDocument4 pagesThe 40 Verse Hanuman Chalisa English Translation - From Ajit Vadakayil BlogBharat ShahNo ratings yet

- Manual PDFDocument3 pagesManual PDFDiego FernandezNo ratings yet

- Term Paper (Dev - Econ-2)Document14 pagesTerm Paper (Dev - Econ-2)acharya.arpan08No ratings yet

- Ordinary People Summary ChartDocument2 pagesOrdinary People Summary Chartangela_cristiniNo ratings yet

- RecipesDocument7 pagesRecipesIndira UmareddyNo ratings yet

- For Updates Visit orDocument6 pagesFor Updates Visit orJFJannahNo ratings yet

- Informative Essays TopicsDocument9 pagesInformative Essays Topicsb725c62j100% (2)

- Mindanao Geothermal v. CIRDocument22 pagesMindanao Geothermal v. CIRMarchini Sandro Cañizares KongNo ratings yet

- Ed Batista Self Coaching Class 6 Slideshare 150505182356 Conversion Gate02 PDFDocument34 pagesEd Batista Self Coaching Class 6 Slideshare 150505182356 Conversion Gate02 PDFSyed WilayathNo ratings yet

- Usia Signifikan.Document14 pagesUsia Signifikan.neli fitriaNo ratings yet

- Stones Unit 2bDocument11 pagesStones Unit 2bJamal Al-deenNo ratings yet

- Heirs of John Sycip vs. CA G.R. No. 76487 November 9 1990Document3 pagesHeirs of John Sycip vs. CA G.R. No. 76487 November 9 1990Mariel D. Portillo100% (1)

- New Hardcore 3 Month Workout PlanDocument3 pagesNew Hardcore 3 Month Workout PlanCarmen Gonzalez LopezNo ratings yet

- GAS ModelDocument3 pagesGAS ModelDibyendu ShilNo ratings yet

- 'Deus Caritas Est' - Pope Benedict and 'God Is Love'Document5 pages'Deus Caritas Est' - Pope Benedict and 'God Is Love'Kym JonesNo ratings yet

- Stacey Dunlap ResumeDocument3 pagesStacey Dunlap ResumestaceysdunlapNo ratings yet

- BProfile EnglishDocument3 pagesBProfile EnglishFaraz Ahmed WaseemNo ratings yet

- Common AddictionsDocument13 pagesCommon AddictionsMaría Cecilia CarattoliNo ratings yet

- GIDC Rajju Shroff ROFEL Institute of Management Studies: Subject:-CRVDocument7 pagesGIDC Rajju Shroff ROFEL Institute of Management Studies: Subject:-CRVIranshah MakerNo ratings yet

- Loi Bayanihan PCR ReviewerDocument15 pagesLoi Bayanihan PCR Reviewerailexcj20No ratings yet

- Pengkarya Muda - Aliah BiDocument7 pagesPengkarya Muda - Aliah BiNORHASLIZA BINTI MOHAMAD MoeNo ratings yet

- 11.02.2022-PHC ResultsDocument6 pages11.02.2022-PHC ResultsNILAY TEJANo ratings yet

- GIS Based Analysis On Walkability of Commercial Streets at Continuing Growth Stages - EditedDocument11 pagesGIS Based Analysis On Walkability of Commercial Streets at Continuing Growth Stages - EditedemmanuelNo ratings yet

- CreamsDocument17 pagesCreamsSolomonNo ratings yet