Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5823)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Revised SSAW Questionnaire Steel PipeDocument8 pagesRevised SSAW Questionnaire Steel PipeMohammad NowfalNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- (Postmillennial Pop (Book 7) ) Stuart Cunningham, David Craig - Social Media Entertainment - The New Intersection of Hollywood and Silicon Valley (Postmillennial Pop) - NYU Press (2019)Document365 pages(Postmillennial Pop (Book 7) ) Stuart Cunningham, David Craig - Social Media Entertainment - The New Intersection of Hollywood and Silicon Valley (Postmillennial Pop) - NYU Press (2019)Inty AS100% (1)

- Sales Process Flow Chart (PDF, 118kb) - New Prodigy Marketing ...Document5 pagesSales Process Flow Chart (PDF, 118kb) - New Prodigy Marketing ...Ian YongNo ratings yet

- PMP PMI Rita FrameworkDocument7 pagesPMP PMI Rita FrameworkUjang BOP EngineerNo ratings yet

- FINM 272 Work Program 2024Document5 pagesFINM 272 Work Program 2024NkatekoNo ratings yet

- Anugya - Bisht Ambuja FinalDocument33 pagesAnugya - Bisht Ambuja FinalmuradNo ratings yet

- Financial Statements: An OverviewDocument41 pagesFinancial Statements: An OverviewGaluh Boga Kuswara100% (1)

- Capital Investment 3rd Year - Potchefstroom-1Document23 pagesCapital Investment 3rd Year - Potchefstroom-1renette1010No ratings yet

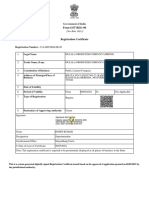

- Form GST REG-06: Government of IndiaDocument3 pagesForm GST REG-06: Government of IndiaAshishNo ratings yet

- Csec Pob January 2015 p2Document15 pagesCsec Pob January 2015 p2Ikera ClarkeNo ratings yet

- BM AshutoshBhandekar MBA06201Document6 pagesBM AshutoshBhandekar MBA06201Ashutosh BhandekarNo ratings yet

- Cap 8 StahelDocument14 pagesCap 8 StahelkitzuragiNo ratings yet

- Cha 4 ProDocument90 pagesCha 4 Proyonas bezaNo ratings yet

- KL Energy Group - Moneylending Pitch DeckDocument17 pagesKL Energy Group - Moneylending Pitch DeckMedic AziziNo ratings yet

- Characteristics of Business MarketDocument2 pagesCharacteristics of Business MarketDenise Katrina PerezNo ratings yet

- Functions of Management-18-27Document10 pagesFunctions of Management-18-27AnggitNo ratings yet

- Marketing Mix 0922 Lesson 13+Document35 pagesMarketing Mix 0922 Lesson 13+Ebenezer Amartey QuarcooNo ratings yet

- Franchise LetterDocument4 pagesFranchise LetterGuar GumNo ratings yet

- What Is Tourism ManagementDocument5 pagesWhat Is Tourism ManagementJonela Adil MustapaNo ratings yet

- The Search For A Sound Business IdeaDocument46 pagesThe Search For A Sound Business IdeaMiguel JaralveNo ratings yet

- QFC Approved Auditors: SL - No# Full Name Address Date of Registration QFCA LicensedDocument1 pageQFC Approved Auditors: SL - No# Full Name Address Date of Registration QFCA LicensedmelvinecgNo ratings yet

- Extracting Full Value From New Product LaunchesDocument37 pagesExtracting Full Value From New Product LaunchesGuido SoldingerNo ratings yet

- SVB State of The Us Wine Industry Report 2024Document63 pagesSVB State of The Us Wine Industry Report 2024nataliafreedom555No ratings yet

- Feaibility Study Under A PandemicDocument2 pagesFeaibility Study Under A PandemicFrutos frititosNo ratings yet

- PRC - CHP 2 Books of Prime EntryDocument21 pagesPRC - CHP 2 Books of Prime EntryKhush Bakht AlihaNo ratings yet

- Profit and Loss PDFDocument7 pagesProfit and Loss PDFDheekshith KumarNo ratings yet

- Linnet Kintu-Phd Thesis RevDocument179 pagesLinnet Kintu-Phd Thesis RevScooby DoNo ratings yet

- Southwest Presentation Group9Document16 pagesSouthwest Presentation Group9Back UpNo ratings yet

- NameDocument1 pageNameORGI GROWNo ratings yet

- The Prelist Along With The Checks Will Be Sent To TheDocument2 pagesThe Prelist Along With The Checks Will Be Sent To TheRaca DesuNo ratings yet