Download as docx, pdf, or txt

You might also like

- A Study of Impact of GST On Hospitality & Travel and Tourism Industry - BHAKTI NISHAR TDAF026CDocument66 pagesA Study of Impact of GST On Hospitality & Travel and Tourism Industry - BHAKTI NISHAR TDAF026Csanu duttaNo ratings yet

- Impact of Goods and Service Tax On Consumers, GSTDocument70 pagesImpact of Goods and Service Tax On Consumers, GSTKkk JjjNo ratings yet

- Goods and Service Tax - Mba ProjectDocument10 pagesGoods and Service Tax - Mba Projectsangeetha jNo ratings yet

- Of The Master of Business AdministrationDocument48 pagesOf The Master of Business AdministrationArun ksNo ratings yet

- GSTDocument46 pagesGSTAninda SahaNo ratings yet

- New GSTDocument30 pagesNew GSTSonia MohapatraNo ratings yet

- Project On GSTDocument38 pagesProject On GSTGourav Pareek100% (1)

- Simplified Goods & Services Tax (GST) For Hotels & RestaurantsDocument14 pagesSimplified Goods & Services Tax (GST) For Hotels & Restaurantsvishaljain_caNo ratings yet

- GST Report About RestaurantsDocument13 pagesGST Report About RestaurantsVarun RimmalapudiNo ratings yet

- Impact of GST On Various SectorsDocument2 pagesImpact of GST On Various SectorsSwathi ReddyNo ratings yet

- Impact of GSTDocument70 pagesImpact of GSTRaman TiwariNo ratings yet

- GSTDocument15 pagesGSTNausheen MerchantNo ratings yet

- Implimantation of GSTDocument43 pagesImplimantation of GSTManoj BeheraNo ratings yet

- Indian GSTDocument55 pagesIndian GSTShivam KharuleNo ratings yet

- Summer Training Report On: "GST Prime Cleaning Services"Document97 pagesSummer Training Report On: "GST Prime Cleaning Services"Master PrintersNo ratings yet

- GST (Vishal Joshi)Document93 pagesGST (Vishal Joshi)Ravin Arvin0% (1)

- GST ProjectDocument53 pagesGST Projectafaque khan0% (1)

- Priyanka ChorageDocument72 pagesPriyanka ChorageTasmay EnterprisesNo ratings yet

- Black Book On GSTDocument70 pagesBlack Book On GSTMrRishabh97No ratings yet

- GST in India - Objectives, Concerns and ChallengesDocument44 pagesGST in India - Objectives, Concerns and Challengesakhilca87% (15)

- GSTDocument20 pagesGSTSanjaygowda55k100% (2)

- GST - Textile IndustryDocument16 pagesGST - Textile IndustrykaranNo ratings yet

- Impacts of GST On Indian EconomyDocument14 pagesImpacts of GST On Indian EconomyR.Deepak KannaNo ratings yet

- Project Report GSTDocument57 pagesProject Report GSTVidhi RamchandaniNo ratings yet

- Project Report On GST Implications in IndiaDocument1 pageProject Report On GST Implications in IndiaRajesh Dasari100% (1)

- GST ImpactDocument40 pagesGST ImpactKhushi Lalit BokadiaNo ratings yet

- CHAPTER - 2 Literature ReviewDocument12 pagesCHAPTER - 2 Literature ReviewSarva ShivaNo ratings yet

- Project GSTDocument128 pagesProject GSTthilakNo ratings yet

- Implementation of Goods and Services Tax (GST) in IndiaDocument18 pagesImplementation of Goods and Services Tax (GST) in IndiaAkanksha BhattNo ratings yet

- SUMMER TRAINING REPORT - CameyDocument99 pagesSUMMER TRAINING REPORT - CameycameyNo ratings yet

- Final ReportDocument24 pagesFinal ReportPrachikarambelkarNo ratings yet

- Ankit - GST - Project 33333333333333Document30 pagesAnkit - GST - Project 33333333333333ankit SharmaNo ratings yet

- Project ReportDocument24 pagesProject ReportanilNo ratings yet

- Synopsis On GSTDocument9 pagesSynopsis On GSTsamiullah100% (1)

- A STUDY OF PERCEPTION OF TAXPAYERS TOWARDS NewDocument41 pagesA STUDY OF PERCEPTION OF TAXPAYERS TOWARDS NewsiddhantNo ratings yet

- Sample Sip Report ADocument46 pagesSample Sip Report AJagrati KanojiyaNo ratings yet

- Registration Under GST Law Section 22,23&24 of The CGST Act, 2017 CA.P. Ashwin KumaarDocument38 pagesRegistration Under GST Law Section 22,23&24 of The CGST Act, 2017 CA.P. Ashwin Kumaarshiva ramanNo ratings yet

- Goods & Services Tax (GST) - (One Nation One Tax)Document40 pagesGoods & Services Tax (GST) - (One Nation One Tax)sumukh0% (1)

- Project Report On GST-2018Document32 pagesProject Report On GST-2018Piyush Chauhan50% (6)

- Impact of Implementation of GST Among RetailersDocument60 pagesImpact of Implementation of GST Among RetailersYuvan Venkat100% (1)

- A Study On Prospects and Challenges in Implementation of Goods and Services Tax (GST) in IndiaDocument4 pagesA Study On Prospects and Challenges in Implementation of Goods and Services Tax (GST) in IndiamadanNo ratings yet

- Dhruv ProjectDocument61 pagesDhruv ProjectFahim FaisalNo ratings yet

- IATA Financial Assessment Portal FAQDocument10 pagesIATA Financial Assessment Portal FAQutawxNo ratings yet

- GST - Final ProjectDocument52 pagesGST - Final ProjectAbinas behura BC-20-137No ratings yet

- Impact of GST On Business and Start-Ups - Doc REPORT WRITING 10Document60 pagesImpact of GST On Business and Start-Ups - Doc REPORT WRITING 10Shruti UpadhyayNo ratings yet

- GST Project For McomDocument41 pagesGST Project For McomRockNo ratings yet

- GSTDocument19 pagesGSTRiyaz haja MohideenNo ratings yet

- Vision Collage of Management Kanpur Submitted To, Miss Keerti Tiwari Submitted By, M/S. Anam FatimaDocument24 pagesVision Collage of Management Kanpur Submitted To, Miss Keerti Tiwari Submitted By, M/S. Anam FatimaAnam FatimaNo ratings yet

- Indirect Tax GST BookDocument106 pagesIndirect Tax GST BookDancer Vijay VishwakarmaNo ratings yet

- Aud 1 To Aud 12Document12 pagesAud 1 To Aud 12kishor kumarNo ratings yet

- Alexander Martis - Impact of Goods and Service Tax (GST) On The Consumers in MumbaiDocument80 pagesAlexander Martis - Impact of Goods and Service Tax (GST) On The Consumers in MumbaiAlexander Martis100% (2)

- Summer Project Report: "A Comparative Study of GST Return "Document60 pagesSummer Project Report: "A Comparative Study of GST Return "Aditya DaswaniNo ratings yet

- Report On IMPACT OF GST ON REAL ESTATE INDUSTRYDocument31 pagesReport On IMPACT OF GST ON REAL ESTATE INDUSTRYsamNo ratings yet

- Good and Service Tax"Document37 pagesGood and Service Tax"yash sahareNo ratings yet

- College GST Project - RahulDocument56 pagesCollege GST Project - RahulTarun KumarNo ratings yet

- Komal Tathod (Finance)Document54 pagesKomal Tathod (Finance)yashpal PatilNo ratings yet

- Impact of GST On Automobile IndustryDocument3 pagesImpact of GST On Automobile Industrypvaibhav08No ratings yet

- Annual Report (2021-2022)Document80 pagesAnnual Report (2021-2022)GoMarkhaArjNo ratings yet

- GST Implications Black BookDocument53 pagesGST Implications Black Booksarveshpadwal985No ratings yet

- Title PGW With NoDocument6 pagesTitle PGW With No19 - Miten KariyaNo ratings yet

- VI Semester B.B.A.3 Degree Examination, May - 2019 Services Management (RCU Fresh 2017-18)Document2 pagesVI Semester B.B.A.3 Degree Examination, May - 2019 Services Management (RCU Fresh 2017-18)PariNo ratings yet

- Vi Semester B.B.A. 3 Degree Examination, May/June 2018 International Business Management (Regular)Document2 pagesVi Semester B.B.A. 3 Degree Examination, May/June 2018 International Business Management (Regular)PariNo ratings yet

- Synopsis-Rutuja PatilDocument6 pagesSynopsis-Rutuja PatilPariNo ratings yet

- Bharat Forge LTD., Pune. Variance Analysis Executive SummaryDocument95 pagesBharat Forge LTD., Pune. Variance Analysis Executive SummaryPariNo ratings yet

- Chapter - I: Belgaum Institute of Management Studies, MBA, Belgaum. 1Document74 pagesChapter - I: Belgaum Institute of Management Studies, MBA, Belgaum. 1PariNo ratings yet

- Presentation On Summer in Plant Project: BY, Satish.V.Patil MBA07006041Document23 pagesPresentation On Summer in Plant Project: BY, Satish.V.Patil MBA07006041PariNo ratings yet

- UTI BankDocument81 pagesUTI BankPariNo ratings yet

- Title No: Demat: Is It 100% Safe For An InvestorDocument3 pagesTitle No: Demat: Is It 100% Safe For An InvestorPariNo ratings yet

- Satish EndDocument74 pagesSatish EndPariNo ratings yet

- Title No: Demat: Is It 100% Safe For An InvestorDocument3 pagesTitle No: Demat: Is It 100% Safe For An InvestorPariNo ratings yet

- Executive SummaryDocument65 pagesExecutive SummaryPariNo ratings yet

- Kuvempu University: Master of Business AdministrationDocument5 pagesKuvempu University: Master of Business AdministrationPariNo ratings yet

- Acknowledgement: Doodhaganga-Krishna Sahakari Sakkare Karkhane Niyamit, ChikkodiDocument89 pagesAcknowledgement: Doodhaganga-Krishna Sahakari Sakkare Karkhane Niyamit, ChikkodiPariNo ratings yet

- Kuvempu UniversityDocument5 pagesKuvempu UniversityPariNo ratings yet

- A) Executive Summary: Bazaar Mysore Road Bangalore' Helps To Know The Effectiveness of Promotional StrategyDocument43 pagesA) Executive Summary: Bazaar Mysore Road Bangalore' Helps To Know The Effectiveness of Promotional StrategyPariNo ratings yet

- Unit 1 Introduction (POM)Document17 pagesUnit 1 Introduction (POM)PariNo ratings yet

- K.L. E'S College of Brachelor of Computer Application (B.K College Campus) CHIKODI-591201Document6 pagesK.L. E'S College of Brachelor of Computer Application (B.K College Campus) CHIKODI-591201PariNo ratings yet

- Executive Summary: Belgaum Institute of Management Studies (BIMS) MBADocument57 pagesExecutive Summary: Belgaum Institute of Management Studies (BIMS) MBAPariNo ratings yet

- International Economics 15th Edition Robert Carbaugh Test BankDocument26 pagesInternational Economics 15th Edition Robert Carbaugh Test BankCassandraHarrisyanb100% (65)

- For CHAPTER 2Document8 pagesFor CHAPTER 2NIKKI FE MORALNo ratings yet

- CE For Fire VictimDocument1 pageCE For Fire VictimJaz AchNo ratings yet

- Third Rail Sectioning Diagram of Dream City Depot - 230817 - 185014Document2 pagesThird Rail Sectioning Diagram of Dream City Depot - 230817 - 185014rishabhNo ratings yet

- Mankiw Macroeconomics 6e Ch02 Test AnsDocument7 pagesMankiw Macroeconomics 6e Ch02 Test AnsNgọc AnhNo ratings yet

- Assignment Cover Sheet: Pham Thanh Duy E1900299Document19 pagesAssignment Cover Sheet: Pham Thanh Duy E1900299Thanh DuyNo ratings yet

- Labor Migration TheoriesDocument9 pagesLabor Migration TheoriesR BNo ratings yet

- Tutorial On Capital Budgeting: Year Cash Flow (Rs. in Million)Document3 pagesTutorial On Capital Budgeting: Year Cash Flow (Rs. in Million)afzalkhanNo ratings yet

- Logistics and Competitive StrategyDocument14 pagesLogistics and Competitive StrategyPankaj DograNo ratings yet

- Topic 10 (Trade)Document35 pagesTopic 10 (Trade)shelleyallynNo ratings yet

- Chapter 1: Introduction To Accounting (FAR By: Millan)Document91 pagesChapter 1: Introduction To Accounting (FAR By: Millan)Lovely LimNo ratings yet

- Aca 2024 PlannerDocument1 pageAca 2024 Planneryfarhana2002No ratings yet

- ComesaDocument45 pagesComesa123sexNo ratings yet

- Assignment 2 Pma1113 Set LDocument10 pagesAssignment 2 Pma1113 Set LIvy NalyaNo ratings yet

- Practice Tax Problem With Answers-1Document2 pagesPractice Tax Problem With Answers-1Ana SofiaNo ratings yet

- Macrobloques Chuquicamata Subterránea PDFDocument13 pagesMacrobloques Chuquicamata Subterránea PDFJOSE ARAYANo ratings yet

- ACCT 3039 Breakeven 0 Quality Costing 2Document6 pagesACCT 3039 Breakeven 0 Quality Costing 2Kymani MccarthyNo ratings yet

- CPRS Export Documentary Requirements 2020 - New PDFDocument2 pagesCPRS Export Documentary Requirements 2020 - New PDFCzarina Danielle EsequeNo ratings yet

- Ravi Shankar PrasadDocument3 pagesRavi Shankar PrasadAadarsh KumarNo ratings yet

- Mengupas Persoalan Standar Akuntansi Keuangan - Goodwil Di Berbagai Negara: Suatu Pendekatan Studi LiteraturDocument17 pagesMengupas Persoalan Standar Akuntansi Keuangan - Goodwil Di Berbagai Negara: Suatu Pendekatan Studi LiteraturNina HernawatiNo ratings yet

- Delhi Public School Bangalore - East Social Science (Economics) Globalisation (Notes)Document6 pagesDelhi Public School Bangalore - East Social Science (Economics) Globalisation (Notes)Abhigyan KesriNo ratings yet

- Goubert - Historical Demography and The Reinterpretation of Early Modern French History - A Research Review PDFDocument13 pagesGoubert - Historical Demography and The Reinterpretation of Early Modern French History - A Research Review PDFDécio GuzmánNo ratings yet

- Individual Assignment 1 (Đư C T PH C H I)Document9 pagesIndividual Assignment 1 (Đư C T PH C H I)Hoàng AnhNo ratings yet

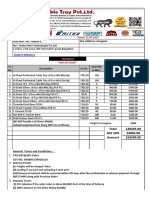

- Stratos Infra Technologies PVT - Ltd.-Quo-347-25.07.2023Document1 pageStratos Infra Technologies PVT - Ltd.-Quo-347-25.07.2023Divyansh GuptaNo ratings yet

- A Study On Performance Appraisal of Idbi Bank in IndiaDocument43 pagesA Study On Performance Appraisal of Idbi Bank in Indiasj computersNo ratings yet

- BSP Circulars 2020-2000Document64 pagesBSP Circulars 2020-2000Miguel BenitezNo ratings yet

- Money LessonDocument3 pagesMoney LessonSoledadCorderoOrdóñezNo ratings yet

- Unit 3 Fiscal PolicyDocument47 pagesUnit 3 Fiscal PolicyThu Trang HàNo ratings yet

- Current Affairs: Energy Crisis in PakistanDocument10 pagesCurrent Affairs: Energy Crisis in PakistanArsalan Khan GhauriNo ratings yet

- The GraphDocument2 pagesThe GraphStanislav KovalenkoNo ratings yet