Download as pdf or txt

You might also like

- Solution Manual For Corporate Finance A Focused Approach 6th EditionDocument37 pagesSolution Manual For Corporate Finance A Focused Approach 6th Editionjanetgriffintizze100% (17)

- SOP MerchandiseDocument6 pagesSOP MerchandiseAnonymous eSjcWuULRNo ratings yet

- Ill Wind in FriezfordDocument36 pagesIll Wind in FriezfordNick KNo ratings yet

- Biong Making Sense of The PastDocument9 pagesBiong Making Sense of The PastCarlo Biong100% (5)

- Chapter 5Document14 pagesChapter 5Donna John MazulaNo ratings yet

- P6MYS AnsDocument12 pagesP6MYS AnsLi HYu ClfEiNo ratings yet

- Corrigendum To MFD - WB Version Dec 2019 - Chapter 8 - Effective From 31mar2020Document14 pagesCorrigendum To MFD - WB Version Dec 2019 - Chapter 8 - Effective From 31mar2020Manish MahatoNo ratings yet

- Capital GainsDocument6 pagesCapital GainsMuskanDodejaNo ratings yet

- ALZONA - OE Financing DecisionsDocument3 pagesALZONA - OE Financing DecisionsJames Ryan AlzonaNo ratings yet

- Module I - Income Tax and GSTDocument4 pagesModule I - Income Tax and GSTMuhammed Yaseen MNo ratings yet

- Direct Taxes Code 2010Document14 pagesDirect Taxes Code 2010musti_shahNo ratings yet

- Lodha Budget Briefing 2018Document44 pagesLodha Budget Briefing 2018s k shettyNo ratings yet

- Tax Watch Bulletin Tax Amendment Bills 2023Document22 pagesTax Watch Bulletin Tax Amendment Bills 2023BonnieNo ratings yet

- Final ReitDocument5 pagesFinal Reitchris_yvonneNo ratings yet

- Taxation in Mutual FundsDocument16 pagesTaxation in Mutual Fundsvineetb553No ratings yet

- DTC ProvisionsDocument3 pagesDTC ProvisionsrajdeeppawarNo ratings yet

- Direct Tax Code: Kunal Vora Bhavik BhanderiDocument11 pagesDirect Tax Code: Kunal Vora Bhavik BhanderiBhavik BhanderiNo ratings yet

- Taxation 12Document13 pagesTaxation 12surajspammsNo ratings yet

- 7th Term - Legal Frameworks of ConstructionDocument79 pages7th Term - Legal Frameworks of ConstructionShreedharNo ratings yet

- Income Based Valuation - l3Document14 pagesIncome Based Valuation - l3Kristene Romarate DaelNo ratings yet

- Stockspot Tax Guide 2023Document4 pagesStockspot Tax Guide 2023striker1976No ratings yet

- Deloitte Budget Update - 2019Document24 pagesDeloitte Budget Update - 2019Carol PereiraNo ratings yet

- Unit 2 B-CDocument20 pagesUnit 2 B-CAnish KartikNo ratings yet

- Study GuideDocument22 pagesStudy Guidedave_88opNo ratings yet

- Tax Guide: C M Y KDocument10 pagesTax Guide: C M Y Kjoefrancis5052693No ratings yet

- Singapore Tax System#published Article# - 1556967521Document17 pagesSingapore Tax System#published Article# - 1556967521Vaibhav ChoudhryNo ratings yet

- One Advice For Investors Earning Dividend Income - Unlearn, Then Relearn!Document6 pagesOne Advice For Investors Earning Dividend Income - Unlearn, Then Relearn!Ramasayi Gummadi100% (1)

- Taxation Management AssignmentDocument11 pagesTaxation Management AssignmentniraliNo ratings yet

- Capital GainDocument9 pagesCapital Gainbarakkat72No ratings yet

- Capital GainDocument4 pagesCapital GainqwertyNo ratings yet

- KPMG Budget HighlightsDocument24 pagesKPMG Budget Highlightsapi-3732007No ratings yet

- The Income Tax ActDocument15 pagesThe Income Tax ActfbuameNo ratings yet

- Fas116-Acctg For Contributions Received and MadeDocument42 pagesFas116-Acctg For Contributions Received and MadeALEIHNo ratings yet

- Essay On Passive IncomeDocument10 pagesEssay On Passive IncomeJithesh ViswanadhNo ratings yet

- Alert: The Finance (Miscellaneous Provisons) BillDocument11 pagesAlert: The Finance (Miscellaneous Provisons) BillJohn SmithNo ratings yet

- Axis Factsheet April 2020Document57 pagesAxis Factsheet April 2020GNo ratings yet

- Taxation Law 1 - Notes Co: Less: DeductionsDocument24 pagesTaxation Law 1 - Notes Co: Less: DeductionsClint Lou Matthew EstapiaNo ratings yet

- Tax Planning For Salaried IndividualsDocument20 pagesTax Planning For Salaried IndividualsRAJNo ratings yet

- DT NotesDocument41 pagesDT NotesHariprasad bhatNo ratings yet

- Tax On Mutual FundsDocument7 pagesTax On Mutual FundsPramod KumarNo ratings yet

- Deloitte Tax Alert - Corporate Tax Rates Slashed and Fiscal Relief AnnouncedDocument4 pagesDeloitte Tax Alert - Corporate Tax Rates Slashed and Fiscal Relief AnnouncedSunil GidwaniNo ratings yet

- Tax Treatment of Dividend ReceivedDocument10 pagesTax Treatment of Dividend ReceivedmukeshNo ratings yet

- Financial Act 2Document1 pageFinancial Act 2Kashif AliNo ratings yet

- NISM Series 5A Chapter 8Document12 pagesNISM Series 5A Chapter 8sachinaman.2016No ratings yet

- IHCDocument52 pagesIHCMin Li67% (3)

- Tax Reckoner: Snapshot of Tax Rates Specific To Mutual FundsDocument3 pagesTax Reckoner: Snapshot of Tax Rates Specific To Mutual FundsSUBHASH SHARMANo ratings yet

- Income Taxation 1: Holding PeriodDocument4 pagesIncome Taxation 1: Holding PeriodKarl John Jay ValderamaNo ratings yet

- Indian Accounting Standard 12: © The Institute of Chartered Accountants of IndiaDocument22 pagesIndian Accounting Standard 12: © The Institute of Chartered Accountants of IndiaRITZ BROWNNo ratings yet

- Taxation in Mutual FundsDocument18 pagesTaxation in Mutual Fundsvineetb553No ratings yet

- Inctax Lecture Notes Froup 2 and 6Document27 pagesInctax Lecture Notes Froup 2 and 6KrizahMarieCaballeroNo ratings yet

- Taxation Interest Income and Its Effect On SavingsDocument25 pagesTaxation Interest Income and Its Effect On SavingsTimothy AngeloNo ratings yet

- Income Tax Guide UgandaDocument13 pagesIncome Tax Guide UgandaMoses LubangakeneNo ratings yet

- Closed End Fund CompanyDocument33 pagesClosed End Fund CompanyIvy LiewNo ratings yet

- Assignment of Income DoctrineDocument20 pagesAssignment of Income DoctrinewxwgmumpdNo ratings yet

- Financial Planning & Tax Management - Section - 115-O of The Indian Income Tax Act, 1961Document8 pagesFinancial Planning & Tax Management - Section - 115-O of The Indian Income Tax Act, 1961Gaurav KumarNo ratings yet

- Paper Presentation On Direct Tax Code BILL 2009: CA. Vijay R KalaniDocument19 pagesPaper Presentation On Direct Tax Code BILL 2009: CA. Vijay R Kalanihardrocks69No ratings yet

- Tax Planning Guide: 1800 3000 6070 Buyonline@iciciprulifeDocument14 pagesTax Planning Guide: 1800 3000 6070 Buyonline@iciciprulifeRohitNo ratings yet

- Direct Tax CodeDocument10 pagesDirect Tax Codejgaurav80No ratings yet

- Rescue AsdDocument9 pagesRescue AsdsheldonNo ratings yet

- Tax Saving StepsDocument10 pagesTax Saving StepsDheeraj SethNo ratings yet

- Taxation - Allowable Business DeductionsDocument51 pagesTaxation - Allowable Business DeductionsHannah OrosNo ratings yet

- PDS SuperOptionsDocument32 pagesPDS SuperOptionsNick KNo ratings yet

- GHD Superannuation Plan: Product Disclosure StatementDocument32 pagesGHD Superannuation Plan: Product Disclosure StatementNick KNo ratings yet

- Australiansuper: Product Disclosure StatementDocument32 pagesAustraliansuper: Product Disclosure StatementNick KNo ratings yet

- Guide To CC CapDocument16 pagesGuide To CC CapNick KNo ratings yet

- TTR Income: Product Disclosure StatementDocument52 pagesTTR Income: Product Disclosure StatementNick KNo ratings yet

- Australiansuper Select: Product Disclosure StatementDocument16 pagesAustraliansuper Select: Product Disclosure StatementNick KNo ratings yet

- Personal Plan: Product Disclosure StatementDocument28 pagesPersonal Plan: Product Disclosure StatementNick KNo ratings yet

- PDS PublicSectorDocument16 pagesPDS PublicSectorNick KNo ratings yet

- Life Insurance PdsDocument43 pagesLife Insurance PdsNick KNo ratings yet

- Generations Super and Pension Product Disclosure StatementDocument39 pagesGenerations Super and Pension Product Disclosure StatementNick KNo ratings yet

- AU-Vanguard Managed Funds-Reference GuideDocument19 pagesAU-Vanguard Managed Funds-Reference GuideNick KNo ratings yet

- AU-Vanguard Personal Investor Guide Part ADocument28 pagesAU-Vanguard Personal Investor Guide Part ANick KNo ratings yet

- AU-Vanguard Personal Investor Investment MenuDocument12 pagesAU-Vanguard Personal Investor Investment MenuNick KNo ratings yet

- Richmond Bridge Duplication and Traffic Improvements: Community Update - Route Investigation November 2019Document5 pagesRichmond Bridge Duplication and Traffic Improvements: Community Update - Route Investigation November 2019Nick KNo ratings yet

- Info Card 2016-17Document12 pagesInfo Card 2016-17Nick KNo ratings yet

- Generations Personal Super and Pension Additional InformationDocument22 pagesGenerations Personal Super and Pension Additional InformationNick KNo ratings yet

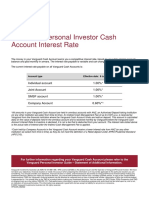

- AU-Vanguard Personal Investor-Cash Account Interest RateDocument1 pageAU-Vanguard Personal Investor-Cash Account Interest RateNick KNo ratings yet

- Common Riverbank Weeds Lower Hawk Nepean BookletDocument68 pagesCommon Riverbank Weeds Lower Hawk Nepean BookletNick KNo ratings yet

- FMA Informative Issue184Document11 pagesFMA Informative Issue184Nick KNo ratings yet

- Woolworths Supermarkets Agreement 2018 Final 02.10.2018Document68 pagesWoolworths Supermarkets Agreement 2018 Final 02.10.2018Nick KNo ratings yet

- Richmond Bridge Duplication and Traffic Improvements: Frequently Asked QuestionsDocument5 pagesRichmond Bridge Duplication and Traffic Improvements: Frequently Asked QuestionsNick KNo ratings yet

- Thermodynamics TestBank Chap 2Document13 pagesThermodynamics TestBank Chap 2Jay Desai100% (3)

- GFW 3600 10Document1 pageGFW 3600 10Ganesan SegarNo ratings yet

- 12 Munsalud Vs NhaDocument2 pages12 Munsalud Vs Nhanikitaspongebob100% (1)

- PIKE MIRacle A529-PQ UserManualDocument23 pagesPIKE MIRacle A529-PQ UserManualKhalid ZghearNo ratings yet

- Brochure - Seminar IBS - Precast Product - FinalDocument2 pagesBrochure - Seminar IBS - Precast Product - FinalShahril ZainulNo ratings yet

- Audley Booking Form - David and Cynthia Bartlett - New Zealand Jan:Feb 2019Document2 pagesAudley Booking Form - David and Cynthia Bartlett - New Zealand Jan:Feb 2019david.bartlett26No ratings yet

- AWOL, SC DecisionsDocument55 pagesAWOL, SC DecisionsMelencio Silverio FaustinoNo ratings yet

- CSS Business Administration MCQsDocument9 pagesCSS Business Administration MCQsMuhammad YouneebNo ratings yet

- CFCDocument2 pagesCFCEli ShiNo ratings yet

- Wa0008Document2 pagesWa0008Jagadamba RealtorNo ratings yet

- Spouses de Guzman V Spouses OchoaDocument1 pageSpouses de Guzman V Spouses Ochoaleia eleazarNo ratings yet

- Dean's Open Letter: Associate Professor Assistant Professor LecturerDocument6 pagesDean's Open Letter: Associate Professor Assistant Professor LecturerMarguerite RiceNo ratings yet

- RSADocument4 pagesRSAmjgirasolNo ratings yet

- 98 Benita Salao Vs Juan SalaoDocument1 page98 Benita Salao Vs Juan SalaoNur OmarNo ratings yet

- Estimate - 2023 37 - 05 - 10 - 23Document2 pagesEstimate - 2023 37 - 05 - 10 - 23Rajendra Singh DhakarNo ratings yet

- 2011 Holiday ListDocument1 page2011 Holiday ListSiva ChandhraNo ratings yet

- Chapter 10 Section 1Document16 pagesChapter 10 Section 1api-206809924No ratings yet

- Ang Mga Kaanib Sa Iglesia NG Dios Kay Kristo Hesus - V - Iglesia NG Dios Kay Cristo JesusDocument2 pagesAng Mga Kaanib Sa Iglesia NG Dios Kay Kristo Hesus - V - Iglesia NG Dios Kay Cristo Jesuserwindm84No ratings yet

- Mobile App Handover List - Rev1Document3 pagesMobile App Handover List - Rev1Sunil Kumar KNo ratings yet

- The Cash Transactions and Cash Balances of Banner Inc ForDocument1 pageThe Cash Transactions and Cash Balances of Banner Inc Foramit raajNo ratings yet

- NYS Human Rights LawDocument41 pagesNYS Human Rights Lawنبيل حناNo ratings yet

- Cover Letter Speaker BoehnerDocument2 pagesCover Letter Speaker Boehnergerald7783No ratings yet

- 102officialcommunicationpdf 2019 12 02 12 24 05 PDFDocument5 pages102officialcommunicationpdf 2019 12 02 12 24 05 PDFpoojaNo ratings yet

- Consolidation Subsequent To The Acquisition Date: Yq Ues Tion in Ale XamDocument30 pagesConsolidation Subsequent To The Acquisition Date: Yq Ues Tion in Ale XamSheda AshrafNo ratings yet

- RecFin AnswerKeySolutionsDocument3 pagesRecFin AnswerKeySolutionsHannah Jane UmbayNo ratings yet

- Change in PV, DV C DP: ENM200 Tutorial Solutions Reservoir Rock Properties 2010Document3 pagesChange in PV, DV C DP: ENM200 Tutorial Solutions Reservoir Rock Properties 2010Ali HijaziNo ratings yet

- Case StudyDocument3 pagesCase StudyMeenakshi AnilNo ratings yet

- Luzon Iron Development Group Corp. v. Bridestone Mining and Development Corp.Document9 pagesLuzon Iron Development Group Corp. v. Bridestone Mining and Development Corp.Princess Samantha SarcedaNo ratings yet