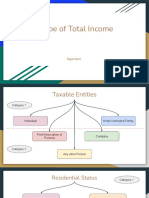

Residential Status of An Asset: There Are Two Sets of Conditions

Residential Status of An Asset: There Are Two Sets of Conditions

You might also like

- Solutions PepallDocument48 pagesSolutions PepallJoseph Guen67% (6)

- Burfisher Introduction To CGE Models 2016Document441 pagesBurfisher Introduction To CGE Models 2016paul argamosaNo ratings yet

- Anton Kriel Detailed ReviewDocument4 pagesAnton Kriel Detailed ReviewMus'ab Abdullahi Bulale100% (2)

- DTP 2nd ModuleDocument6 pagesDTP 2nd ModuleVeena GowdaNo ratings yet

- Direct Taxation: Residential Status of Individual, Company, HUF, AOP, BOIDocument11 pagesDirect Taxation: Residential Status of Individual, Company, HUF, AOP, BOIsameer prasadNo ratings yet

- Residential StatusDocument45 pagesResidential StatusSureshramana MayyaNo ratings yet

- Resdential Status Questionsby Garun Kumar GDCM SrikakulamDocument9 pagesResdential Status Questionsby Garun Kumar GDCM Srikakulamgeddadaarun100% (1)

- Income TaxDocument14 pagesIncome Taxankit srivastavaNo ratings yet

- Residential Status and Incidence of Tax On Income Under Income Tax ActDocument6 pagesResidential Status and Incidence of Tax On Income Under Income Tax ActhaseefaNo ratings yet

- Income Tax Planning-1Document32 pagesIncome Tax Planning-1Ashutosh ShuklaNo ratings yet

- Residential StatusDocument40 pagesResidential StatusSankalp ShuklaNo ratings yet

- Income Tax and Law UNIT-1 Part2Document26 pagesIncome Tax and Law UNIT-1 Part2rashmianand712No ratings yet

- Caa0eresidential StatusDocument13 pagesCaa0eresidential StatusShashwat MishraNo ratings yet

- Residential Status and Tax IncedenceDocument46 pagesResidential Status and Tax IncedenceAmit YadavNo ratings yet

- MB FM 03 TAX PLANNING AND FINANCIAL REPORTING New-1Document70 pagesMB FM 03 TAX PLANNING AND FINANCIAL REPORTING New-1Khushboo SinghNo ratings yet

- It - Lesson 3Document14 pagesIt - Lesson 3Sugandha AgarwalNo ratings yet

- Residential Status Under Income-Tax Act, 1961Document6 pagesResidential Status Under Income-Tax Act, 1961Bharat Tailor100% (1)

- Residential Status and Tax IncidenceDocument46 pagesResidential Status and Tax IncidenceÄbhíñävJäíñNo ratings yet

- CTP - Residential Status & Scope of IncomeDocument7 pagesCTP - Residential Status & Scope of IncomeankushdeshmukhNo ratings yet

- Residential Status (Individual) : 1. Basic Condition 2. Additional Condition (Subsequent Condition)Document5 pagesResidential Status (Individual) : 1. Basic Condition 2. Additional Condition (Subsequent Condition)Ali NadafNo ratings yet

- Scope of Total Income U/S. 5: Presented To:-Prof. SeemaDocument17 pagesScope of Total Income U/S. 5: Presented To:-Prof. SeemaRaksha ShettyNo ratings yet

- R S T I: Esidence and Cope of Otal NcomeDocument5 pagesR S T I: Esidence and Cope of Otal NcomeMnk BhkNo ratings yet

- Taxation 13Document14 pagesTaxation 13Ayush RainaNo ratings yet

- Residence and Scope of Total Income PDFDocument7 pagesResidence and Scope of Total Income PDFsidharthNo ratings yet

- Scope of Total IncomeDocument17 pagesScope of Total IncomeAvishiNo ratings yet

- Section 5 Which Defines The "Scope of Income" Section 6 Which Defines The "The Residential Status" of The PersonDocument8 pagesSection 5 Which Defines The "Scope of Income" Section 6 Which Defines The "The Residential Status" of The PersondipxxxNo ratings yet

- Residential Status of A Person Determines Whether The Person's Income Is Chargeable To Tax in India or NotDocument22 pagesResidential Status of A Person Determines Whether The Person's Income Is Chargeable To Tax in India or Notkshitizjain07No ratings yet

- Residential Status: Vaibhav BanjanDocument14 pagesResidential Status: Vaibhav Banjandeepika gawasNo ratings yet

- Income Tax Law & Practice Residential StatusDocument11 pagesIncome Tax Law & Practice Residential StatusManleen KaurNo ratings yet

- Residentail StatusDocument11 pagesResidentail StatusRashmi JayaprakashNo ratings yet

- Residential Status: Presented ByDocument17 pagesResidential Status: Presented ByRohit SinghNo ratings yet

- ITax 2 - Residential Status UpdatedDocument18 pagesITax 2 - Residential Status UpdatedSudha AgarwalNo ratings yet

- Business TaxationDocument7 pagesBusiness Taxationdoimishti86No ratings yet

- Residential Status: Vaibhav BanjanDocument14 pagesResidential Status: Vaibhav BanjanAnmolNo ratings yet

- Residential Status DC 2023-24Document11 pagesResidential Status DC 2023-24avinashhpv7785No ratings yet

- Short Notes of Residential StatusDocument3 pagesShort Notes of Residential StatusutsavNo ratings yet

- Presentation On Residential Status & Its Incidence On Tax LiabilityDocument13 pagesPresentation On Residential Status & Its Incidence On Tax LiabilitypriyaniNo ratings yet

- Law of Taxation Rules For Determining Residential Status: ProblemsDocument13 pagesLaw of Taxation Rules For Determining Residential Status: ProblemsgeethammaniNo ratings yet

- 3rd Sem Taxation Ppt-3.Pdf328Document34 pages3rd Sem Taxation Ppt-3.Pdf328Harpreet SinghNo ratings yet

- Residential StatusDocument17 pagesResidential Statussaif aliNo ratings yet

- Day4 Residential Status and Incidence of Tax (9 Oct)Document12 pagesDay4 Residential Status and Incidence of Tax (9 Oct)1986anuNo ratings yet

- Taxation: A Person or Company Is Chargeable To Tax Not On What His Pocket Saves But On What Goes IntoDocument22 pagesTaxation: A Person or Company Is Chargeable To Tax Not On What His Pocket Saves But On What Goes IntoJitendra Kumar100% (1)

- Residential Status and Taxation For Individuals - Taxguru - inDocument2 pagesResidential Status and Taxation For Individuals - Taxguru - inSubhamNo ratings yet

- Income Tax Summary BookDocument40 pagesIncome Tax Summary BookMaithili SUBRAMANIANNo ratings yet

- Residential Status ppt1Document17 pagesResidential Status ppt1Prasanna ReddyNo ratings yet

- Residential Status ppt1Document17 pagesResidential Status ppt1Reddy ReddyNo ratings yet

- Semester V Direct Tax Residence & Scope of Total Income A/087/Divya KamaliyaDocument14 pagesSemester V Direct Tax Residence & Scope of Total Income A/087/Divya KamaliyaHarsh KamaliyaNo ratings yet

- Residential Status & Exempted IncomesDocument8 pagesResidential Status & Exempted IncomesMr UniqueNo ratings yet

- TaxassignmentDocument7 pagesTaxassignmentMuditNo ratings yet

- RESIDENCE RELATED - 3rd SemDocument33 pagesRESIDENCE RELATED - 3rd Semyokip59536No ratings yet

- Residential Status PDFDocument14 pagesResidential Status PDFPaiNo ratings yet

- Direct Tax Summary NotesDocument88 pagesDirect Tax Summary NotesAlisha LukeNo ratings yet

- Residential Status and Incidence of Tax - Study MaterialDocument6 pagesResidential Status and Incidence of Tax - Study MaterialEmeline SoroNo ratings yet

- Residential Status and Tax Incidence: Dr. Niti SaxenaDocument11 pagesResidential Status and Tax Incidence: Dr. Niti SaxenaYusufNo ratings yet

- e Book PDF PDFDocument91 pagese Book PDF PDFGiri SukumarNo ratings yet

- TaxassignmentDocument7 pagesTaxassignmentMuditNo ratings yet

- Chapter-2 Residential StatusDocument5 pagesChapter-2 Residential StatusBrinda RNo ratings yet

- Relationship Between Residential Status and Incidence of TaxDocument5 pagesRelationship Between Residential Status and Incidence of Taxsuyash dugarNo ratings yet

- Residential StatusDocument3 pagesResidential StatusMd DanishNo ratings yet

- Residential StatusDocument20 pagesResidential StatusroopamNo ratings yet

- Residential Status of An AssesseeDocument5 pagesResidential Status of An AssesseeKishore KNo ratings yet

- Personal Tax Planning 201718Document79 pagesPersonal Tax Planning 201718Deepak JainNo ratings yet

- Deed of Conditional SaleDocument2 pagesDeed of Conditional SaleVincent VincentNo ratings yet

- Hubungan Antara Kredibilitas Petugas Pelayanan Informasi Puskesmas Dengan Sikap Pengunjung Terhadap Puskesmas NagregDocument23 pagesHubungan Antara Kredibilitas Petugas Pelayanan Informasi Puskesmas Dengan Sikap Pengunjung Terhadap Puskesmas NagregJokowi 3 PeriodeNo ratings yet

- NZ Denim Daily Statement - 2024.Document8 pagesNZ Denim Daily Statement - 2024.Fazley RabbiNo ratings yet

- Science Sampling TestsDocument36 pagesScience Sampling TestsZane sohNo ratings yet

- Evelyn Hone College of Applied Arts and Commerce School of Business Studies Human Resource SectionDocument4 pagesEvelyn Hone College of Applied Arts and Commerce School of Business Studies Human Resource SectionMichelo HabulemboNo ratings yet

- GPH-BUET Test ReportDocument24 pagesGPH-BUET Test ReportAtikur RahmanNo ratings yet

- Itb 5Document25 pagesItb 5Byul make me gay Yoongi make me straightNo ratings yet

- Ex SuppDocument63 pagesEx SuppaqwzsxNo ratings yet

- University of Santo TomasDocument1 pageUniversity of Santo TomasDennis Michael DyNo ratings yet

- Damodaram Sanjivayya National Law University, Ap, India: SubjectDocument16 pagesDamodaram Sanjivayya National Law University, Ap, India: SubjectPradeep reddy JonnalaNo ratings yet

- Short Answer Key: Problem Set 1Document3 pagesShort Answer Key: Problem Set 1Sagheer Hussain DaharNo ratings yet

- Standard Pert-Cpm For BuildingDocument90 pagesStandard Pert-Cpm For BuildingJoji Ann UayanNo ratings yet

- Cheque Requisition Form SampleDocument1 pageCheque Requisition Form SamplehenaediNo ratings yet

- 2023 LoGFA TECHNOTESDocument13 pages2023 LoGFA TECHNOTESHedjarah MulokNo ratings yet

- BUSINESS DEVELOPMENT at LAKME LEVER PRIVATE LIMITEDDocument18 pagesBUSINESS DEVELOPMENT at LAKME LEVER PRIVATE LIMITEDjagdish kaleNo ratings yet

- Raport Kroll II OcrDocument154 pagesRaport Kroll II OcrSergiu BadanNo ratings yet

- Steward BankDocument20 pagesSteward BankSarah ManiwaNo ratings yet

- Abm Las Applied Week 2Document9 pagesAbm Las Applied Week 2Andrea Grace Bayot AdanaNo ratings yet

- Stats 242: Algorithmic Trading and Quantitative Strategies Summer 2011Document9 pagesStats 242: Algorithmic Trading and Quantitative Strategies Summer 2011Veeken ChaglassianNo ratings yet

- H07RN-F, Enhanced Version: Product InformationDocument5 pagesH07RN-F, Enhanced Version: Product InformationDarwin YupaNo ratings yet

- 5.2 Production MethodsDocument3 pages5.2 Production MethodsGonzalo PastorNo ratings yet

- FDNACCT Business Case - 3T1819 PDFDocument2 pagesFDNACCT Business Case - 3T1819 PDFRoy BonitezNo ratings yet

- Tool & Die - IntroductionDocument20 pagesTool & Die - IntroductionAivan Adams SaberonNo ratings yet

- Job Order Quiz 05 PDFDocument3 pagesJob Order Quiz 05 PDFZamantha Tiangco0% (1)

- Semester Syllabus First and Second, Higher Education, Madhya Pradesh, IndiaDocument1 pageSemester Syllabus First and Second, Higher Education, Madhya Pradesh, IndiaGarima GarimaNo ratings yet

- Trading Strategies Involving Options: Fundamentals of Futures and Options Markets, 6Document15 pagesTrading Strategies Involving Options: Fundamentals of Futures and Options Markets, 6rockman911No ratings yet

- Matrix RDO MarinduqueDocument195 pagesMatrix RDO MarinduqueKimber Lee0% (1)

Download as docx, pdf, or txt

You might also like

- Solutions PepallDocument48 pagesSolutions PepallJoseph Guen67% (6)

- Burfisher Introduction To CGE Models 2016Document441 pagesBurfisher Introduction To CGE Models 2016paul argamosaNo ratings yet

- Anton Kriel Detailed ReviewDocument4 pagesAnton Kriel Detailed ReviewMus'ab Abdullahi Bulale100% (2)

- DTP 2nd ModuleDocument6 pagesDTP 2nd ModuleVeena GowdaNo ratings yet

- Direct Taxation: Residential Status of Individual, Company, HUF, AOP, BOIDocument11 pagesDirect Taxation: Residential Status of Individual, Company, HUF, AOP, BOIsameer prasadNo ratings yet

- Residential StatusDocument45 pagesResidential StatusSureshramana MayyaNo ratings yet

- Resdential Status Questionsby Garun Kumar GDCM SrikakulamDocument9 pagesResdential Status Questionsby Garun Kumar GDCM Srikakulamgeddadaarun100% (1)

- Income TaxDocument14 pagesIncome Taxankit srivastavaNo ratings yet

- Residential Status and Incidence of Tax On Income Under Income Tax ActDocument6 pagesResidential Status and Incidence of Tax On Income Under Income Tax ActhaseefaNo ratings yet

- Income Tax Planning-1Document32 pagesIncome Tax Planning-1Ashutosh ShuklaNo ratings yet

- Residential StatusDocument40 pagesResidential StatusSankalp ShuklaNo ratings yet

- Income Tax and Law UNIT-1 Part2Document26 pagesIncome Tax and Law UNIT-1 Part2rashmianand712No ratings yet

- Caa0eresidential StatusDocument13 pagesCaa0eresidential StatusShashwat MishraNo ratings yet

- Residential Status and Tax IncedenceDocument46 pagesResidential Status and Tax IncedenceAmit YadavNo ratings yet

- MB FM 03 TAX PLANNING AND FINANCIAL REPORTING New-1Document70 pagesMB FM 03 TAX PLANNING AND FINANCIAL REPORTING New-1Khushboo SinghNo ratings yet

- It - Lesson 3Document14 pagesIt - Lesson 3Sugandha AgarwalNo ratings yet

- Residential Status Under Income-Tax Act, 1961Document6 pagesResidential Status Under Income-Tax Act, 1961Bharat Tailor100% (1)

- Residential Status and Tax IncidenceDocument46 pagesResidential Status and Tax IncidenceÄbhíñävJäíñNo ratings yet

- CTP - Residential Status & Scope of IncomeDocument7 pagesCTP - Residential Status & Scope of IncomeankushdeshmukhNo ratings yet

- Residential Status (Individual) : 1. Basic Condition 2. Additional Condition (Subsequent Condition)Document5 pagesResidential Status (Individual) : 1. Basic Condition 2. Additional Condition (Subsequent Condition)Ali NadafNo ratings yet

- Scope of Total Income U/S. 5: Presented To:-Prof. SeemaDocument17 pagesScope of Total Income U/S. 5: Presented To:-Prof. SeemaRaksha ShettyNo ratings yet

- R S T I: Esidence and Cope of Otal NcomeDocument5 pagesR S T I: Esidence and Cope of Otal NcomeMnk BhkNo ratings yet

- Taxation 13Document14 pagesTaxation 13Ayush RainaNo ratings yet

- Residence and Scope of Total Income PDFDocument7 pagesResidence and Scope of Total Income PDFsidharthNo ratings yet

- Scope of Total IncomeDocument17 pagesScope of Total IncomeAvishiNo ratings yet

- Section 5 Which Defines The "Scope of Income" Section 6 Which Defines The "The Residential Status" of The PersonDocument8 pagesSection 5 Which Defines The "Scope of Income" Section 6 Which Defines The "The Residential Status" of The PersondipxxxNo ratings yet

- Residential Status of A Person Determines Whether The Person's Income Is Chargeable To Tax in India or NotDocument22 pagesResidential Status of A Person Determines Whether The Person's Income Is Chargeable To Tax in India or Notkshitizjain07No ratings yet

- Residential Status: Vaibhav BanjanDocument14 pagesResidential Status: Vaibhav Banjandeepika gawasNo ratings yet

- Income Tax Law & Practice Residential StatusDocument11 pagesIncome Tax Law & Practice Residential StatusManleen KaurNo ratings yet

- Residentail StatusDocument11 pagesResidentail StatusRashmi JayaprakashNo ratings yet

- Residential Status: Presented ByDocument17 pagesResidential Status: Presented ByRohit SinghNo ratings yet

- ITax 2 - Residential Status UpdatedDocument18 pagesITax 2 - Residential Status UpdatedSudha AgarwalNo ratings yet

- Business TaxationDocument7 pagesBusiness Taxationdoimishti86No ratings yet

- Residential Status: Vaibhav BanjanDocument14 pagesResidential Status: Vaibhav BanjanAnmolNo ratings yet

- Residential Status DC 2023-24Document11 pagesResidential Status DC 2023-24avinashhpv7785No ratings yet

- Short Notes of Residential StatusDocument3 pagesShort Notes of Residential StatusutsavNo ratings yet

- Presentation On Residential Status & Its Incidence On Tax LiabilityDocument13 pagesPresentation On Residential Status & Its Incidence On Tax LiabilitypriyaniNo ratings yet

- Law of Taxation Rules For Determining Residential Status: ProblemsDocument13 pagesLaw of Taxation Rules For Determining Residential Status: ProblemsgeethammaniNo ratings yet

- 3rd Sem Taxation Ppt-3.Pdf328Document34 pages3rd Sem Taxation Ppt-3.Pdf328Harpreet SinghNo ratings yet

- Residential StatusDocument17 pagesResidential Statussaif aliNo ratings yet

- Day4 Residential Status and Incidence of Tax (9 Oct)Document12 pagesDay4 Residential Status and Incidence of Tax (9 Oct)1986anuNo ratings yet

- Taxation: A Person or Company Is Chargeable To Tax Not On What His Pocket Saves But On What Goes IntoDocument22 pagesTaxation: A Person or Company Is Chargeable To Tax Not On What His Pocket Saves But On What Goes IntoJitendra Kumar100% (1)

- Residential Status and Taxation For Individuals - Taxguru - inDocument2 pagesResidential Status and Taxation For Individuals - Taxguru - inSubhamNo ratings yet

- Income Tax Summary BookDocument40 pagesIncome Tax Summary BookMaithili SUBRAMANIANNo ratings yet

- Residential Status ppt1Document17 pagesResidential Status ppt1Prasanna ReddyNo ratings yet

- Residential Status ppt1Document17 pagesResidential Status ppt1Reddy ReddyNo ratings yet

- Semester V Direct Tax Residence & Scope of Total Income A/087/Divya KamaliyaDocument14 pagesSemester V Direct Tax Residence & Scope of Total Income A/087/Divya KamaliyaHarsh KamaliyaNo ratings yet

- Residential Status & Exempted IncomesDocument8 pagesResidential Status & Exempted IncomesMr UniqueNo ratings yet

- TaxassignmentDocument7 pagesTaxassignmentMuditNo ratings yet

- RESIDENCE RELATED - 3rd SemDocument33 pagesRESIDENCE RELATED - 3rd Semyokip59536No ratings yet

- Residential Status PDFDocument14 pagesResidential Status PDFPaiNo ratings yet

- Direct Tax Summary NotesDocument88 pagesDirect Tax Summary NotesAlisha LukeNo ratings yet

- Residential Status and Incidence of Tax - Study MaterialDocument6 pagesResidential Status and Incidence of Tax - Study MaterialEmeline SoroNo ratings yet

- Residential Status and Tax Incidence: Dr. Niti SaxenaDocument11 pagesResidential Status and Tax Incidence: Dr. Niti SaxenaYusufNo ratings yet

- e Book PDF PDFDocument91 pagese Book PDF PDFGiri SukumarNo ratings yet

- TaxassignmentDocument7 pagesTaxassignmentMuditNo ratings yet

- Chapter-2 Residential StatusDocument5 pagesChapter-2 Residential StatusBrinda RNo ratings yet

- Relationship Between Residential Status and Incidence of TaxDocument5 pagesRelationship Between Residential Status and Incidence of Taxsuyash dugarNo ratings yet

- Residential StatusDocument3 pagesResidential StatusMd DanishNo ratings yet

- Residential StatusDocument20 pagesResidential StatusroopamNo ratings yet

- Residential Status of An AssesseeDocument5 pagesResidential Status of An AssesseeKishore KNo ratings yet

- Personal Tax Planning 201718Document79 pagesPersonal Tax Planning 201718Deepak JainNo ratings yet

- Deed of Conditional SaleDocument2 pagesDeed of Conditional SaleVincent VincentNo ratings yet

- Hubungan Antara Kredibilitas Petugas Pelayanan Informasi Puskesmas Dengan Sikap Pengunjung Terhadap Puskesmas NagregDocument23 pagesHubungan Antara Kredibilitas Petugas Pelayanan Informasi Puskesmas Dengan Sikap Pengunjung Terhadap Puskesmas NagregJokowi 3 PeriodeNo ratings yet

- NZ Denim Daily Statement - 2024.Document8 pagesNZ Denim Daily Statement - 2024.Fazley RabbiNo ratings yet

- Science Sampling TestsDocument36 pagesScience Sampling TestsZane sohNo ratings yet

- Evelyn Hone College of Applied Arts and Commerce School of Business Studies Human Resource SectionDocument4 pagesEvelyn Hone College of Applied Arts and Commerce School of Business Studies Human Resource SectionMichelo HabulemboNo ratings yet

- GPH-BUET Test ReportDocument24 pagesGPH-BUET Test ReportAtikur RahmanNo ratings yet

- Itb 5Document25 pagesItb 5Byul make me gay Yoongi make me straightNo ratings yet

- Ex SuppDocument63 pagesEx SuppaqwzsxNo ratings yet

- University of Santo TomasDocument1 pageUniversity of Santo TomasDennis Michael DyNo ratings yet

- Damodaram Sanjivayya National Law University, Ap, India: SubjectDocument16 pagesDamodaram Sanjivayya National Law University, Ap, India: SubjectPradeep reddy JonnalaNo ratings yet

- Short Answer Key: Problem Set 1Document3 pagesShort Answer Key: Problem Set 1Sagheer Hussain DaharNo ratings yet

- Standard Pert-Cpm For BuildingDocument90 pagesStandard Pert-Cpm For BuildingJoji Ann UayanNo ratings yet

- Cheque Requisition Form SampleDocument1 pageCheque Requisition Form SamplehenaediNo ratings yet

- 2023 LoGFA TECHNOTESDocument13 pages2023 LoGFA TECHNOTESHedjarah MulokNo ratings yet

- BUSINESS DEVELOPMENT at LAKME LEVER PRIVATE LIMITEDDocument18 pagesBUSINESS DEVELOPMENT at LAKME LEVER PRIVATE LIMITEDjagdish kaleNo ratings yet

- Raport Kroll II OcrDocument154 pagesRaport Kroll II OcrSergiu BadanNo ratings yet

- Steward BankDocument20 pagesSteward BankSarah ManiwaNo ratings yet

- Abm Las Applied Week 2Document9 pagesAbm Las Applied Week 2Andrea Grace Bayot AdanaNo ratings yet

- Stats 242: Algorithmic Trading and Quantitative Strategies Summer 2011Document9 pagesStats 242: Algorithmic Trading and Quantitative Strategies Summer 2011Veeken ChaglassianNo ratings yet

- H07RN-F, Enhanced Version: Product InformationDocument5 pagesH07RN-F, Enhanced Version: Product InformationDarwin YupaNo ratings yet

- 5.2 Production MethodsDocument3 pages5.2 Production MethodsGonzalo PastorNo ratings yet

- FDNACCT Business Case - 3T1819 PDFDocument2 pagesFDNACCT Business Case - 3T1819 PDFRoy BonitezNo ratings yet

- Tool & Die - IntroductionDocument20 pagesTool & Die - IntroductionAivan Adams SaberonNo ratings yet

- Job Order Quiz 05 PDFDocument3 pagesJob Order Quiz 05 PDFZamantha Tiangco0% (1)

- Semester Syllabus First and Second, Higher Education, Madhya Pradesh, IndiaDocument1 pageSemester Syllabus First and Second, Higher Education, Madhya Pradesh, IndiaGarima GarimaNo ratings yet

- Trading Strategies Involving Options: Fundamentals of Futures and Options Markets, 6Document15 pagesTrading Strategies Involving Options: Fundamentals of Futures and Options Markets, 6rockman911No ratings yet

- Matrix RDO MarinduqueDocument195 pagesMatrix RDO MarinduqueKimber Lee0% (1)