Financial Reporting Bulletins (Revised As of 2022) : While Those Deleted Were Marked As Such

Financial Reporting Bulletins (Revised As of 2022) : While Those Deleted Were Marked As Such

You might also like

- NCWC Final ReportDocument26 pagesNCWC Final ReportAnitah MasoniNo ratings yet

- Companies (General Provisions and Forms) Regulations 2018Document99 pagesCompanies (General Provisions and Forms) Regulations 2018YousafNo ratings yet

- Revised SRC Rule 68 SummaryDocument85 pagesRevised SRC Rule 68 SummaryBernadette Cervantes100% (3)

- Bpi - Sec Cert TemplateDocument2 pagesBpi - Sec Cert Templatemiron68100% (2)

- Financial Reporting Bulletins (Revised As of 2022) : While Those Deleted Were Marked As SuchDocument16 pagesFinancial Reporting Bulletins (Revised As of 2022) : While Those Deleted Were Marked As SuchMark Anthony B. BacayoNo ratings yet

- Compilation of Material Findings On 2019 Afs Reviewed by The CommissionDocument10 pagesCompilation of Material Findings On 2019 Afs Reviewed by The CommissionAllyssa Camille ArcangelNo ratings yet

- Cap 622D Consolidated Version For The Whole Chapter (01-02-2019) (English)Document10 pagesCap 622D Consolidated Version For The Whole Chapter (01-02-2019) (English)Jessica YimNo ratings yet

- 74931bos60524 m1 AnnexureDocument38 pages74931bos60524 m1 AnnexureBala Guru Prasad TadikamallaNo ratings yet

- CARODocument9 pagesCAROSai Lakshmi PNo ratings yet

- Financial Reporting BulletinsDocument3 pagesFinancial Reporting BulletinsEmil A. MolinaNo ratings yet

- Apollo Tyres Annual Report FY2023-260-274Document15 pagesApollo Tyres Annual Report FY2023-260-274Carrots TopNo ratings yet

- Rules, 2018 To Amend The Companies (Audit and Auditors) Rules, 2014Document46 pagesRules, 2018 To Amend The Companies (Audit and Auditors) Rules, 2014Sunil DesaiNo ratings yet

- Rules, 2018 To Amend The Companies (Audit and Auditors) Rules, 2014Document59 pagesRules, 2018 To Amend The Companies (Audit and Auditors) Rules, 2014RAJANEESH V RNo ratings yet

- ICSIsuggestion 2009Document117 pagesICSIsuggestion 2009Iqbaljit Singh AujlaNo ratings yet

- Rev SCH III - Sent PDFDocument18 pagesRev SCH III - Sent PDFAjay DesaleNo ratings yet

- CSR MB 2023Document46 pagesCSR MB 2023Marie BanuNo ratings yet

- Caro 2020Document11 pagesCaro 2020Gaurav Chauhan CANo ratings yet

- Scheme of ArrangementDocument33 pagesScheme of ArrangementVedant MaskeNo ratings yet

- Amendments in Business Law, Ethics and Communication: (For May 2018 Exams (Old Syllabubs) As Per RTP)Document3 pagesAmendments in Business Law, Ethics and Communication: (For May 2018 Exams (Old Syllabubs) As Per RTP)Neha jainNo ratings yet

- Securities and Exchange Board of IndiaDocument8 pagesSecurities and Exchange Board of IndiaDebashis DeyNo ratings yet

- Notification Dated 20.09.2022Document4 pagesNotification Dated 20.09.2022mazars advisoryNo ratings yet

- Advanced AccountingDocument33 pagesAdvanced AccountingvijaykumartaxNo ratings yet

- RTP 2Document44 pagesRTP 2Harsh KumarNo ratings yet

- Companies Act, 2013 PDFDocument25 pagesCompanies Act, 2013 PDFshivam vermaNo ratings yet

- 57996bos47277gp1 PDFDocument126 pages57996bos47277gp1 PDFAnand PandeyNo ratings yet

- Intermediate Accounting RTP May 20Document44 pagesIntermediate Accounting RTP May 20Durgadevi BaskaranNo ratings yet

- Law - May 2020Document18 pagesLaw - May 2020Princy ManglaNo ratings yet

- Law p4Document90 pagesLaw p4Shyam virsinghNo ratings yet

- Sl. No. Particular Provision Form Due Date (Companies Act) Relaxed Due Date (COVID-19) 1Document3 pagesSl. No. Particular Provision Form Due Date (Companies Act) Relaxed Due Date (COVID-19) 1Munish SharmaNo ratings yet

- Departmental Interpretation and Practice Notes No. 7 (Revised)Document33 pagesDepartmental Interpretation and Practice Notes No. 7 (Revised)Difanny KooNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument39 pages© The Institute of Chartered Accountants of IndiaGowriNo ratings yet

- SRC Rule 68 As AmendedDocument51 pagesSRC Rule 68 As AmendedGilYah MoralesNo ratings yet

- CARO 2020 Book NotesDocument11 pagesCARO 2020 Book NotesCreanativeNo ratings yet

- CA Journal - Article On Schedule IIIDocument6 pagesCA Journal - Article On Schedule IIISIDDHARTH MANDELIANo ratings yet

- GEO - Definitive Information Statement 2021Document264 pagesGEO - Definitive Information Statement 2021Aaron HuangNo ratings yet

- Compilation of Material Findings On 2013 AFS of Financing CompaniesDocument5 pagesCompilation of Material Findings On 2013 AFS of Financing CompaniesJuan FrivaldoNo ratings yet

- VAT Administrative Exceptions Guide - EN - 12 03 2020Document14 pagesVAT Administrative Exceptions Guide - EN - 12 03 2020aliNo ratings yet

- Appendix 1 - Letter of EngagementDocument6 pagesAppendix 1 - Letter of Engagementl.lawliet.ryuzaki.frNo ratings yet

- Ind As 108Document10 pagesInd As 108CA Seshan KrishNo ratings yet

- 001Document16 pages001sathya_41095No ratings yet

- LAPD IntR in 2012 09 Arc 11 IN9 Issue 4 Archived On 14 October 2009Document17 pagesLAPD IntR in 2012 09 Arc 11 IN9 Issue 4 Archived On 14 October 2009sibiyazukiswa27No ratings yet

- FR Power Full Book @mission - CA - Final PDFDocument422 pagesFR Power Full Book @mission - CA - Final PDFlaksh sangtaniNo ratings yet

- Master Circular On Preparation of Financial Statements General Insurance BusinessDocument38 pagesMaster Circular On Preparation of Financial Statements General Insurance BusinesslavkmNo ratings yet

- Corporate & Other LawsDocument22 pagesCorporate & Other Laws1234rutikarrrNo ratings yet

- 263081-2019-Revised Securities Regulation Code SRC Rule20210728-11-K6tsx3Document61 pages263081-2019-Revised Securities Regulation Code SRC Rule20210728-11-K6tsx3Regina RozarioNo ratings yet

- Caro, 2020Document11 pagesCaro, 2020IntrovertNo ratings yet

- Unit 2 Corporate Tax Planning and ManagementDocument21 pagesUnit 2 Corporate Tax Planning and Managementsankiworld3No ratings yet

- BCF 405 Financial Reporting - Module 2 PDFDocument45 pagesBCF 405 Financial Reporting - Module 2 PDFNaresh KumarNo ratings yet

- Appendix 8 - Companies Ordinance (Cap. 622) Disclosure ChecklistDocument46 pagesAppendix 8 - Companies Ordinance (Cap. 622) Disclosure Checklistl.lawliet.ryuzaki.frNo ratings yet

- Q3Document24 pagesQ3Mohamed HamedNo ratings yet

- Ca Intermediate Referencer For Quick Revision (ICAI)Document23 pagesCa Intermediate Referencer For Quick Revision (ICAI)Jeet VekariyaNo ratings yet

- The Statement of Financial Position of C F LTD For TheDocument1 pageThe Statement of Financial Position of C F LTD For TheBube KachevskaNo ratings yet

- Form No. 3ae: Audit Report Under Section 35D (4) /35E (6) of The Income-Tax Act, 1961Document2 pagesForm No. 3ae: Audit Report Under Section 35D (4) /35E (6) of The Income-Tax Act, 1961Anonymous 2evaoXKKdNo ratings yet

- Economic Laws Module 1Document405 pagesEconomic Laws Module 1Mohammed AslamNo ratings yet

- Companies Auditors Report Order2020Document5 pagesCompanies Auditors Report Order2020SP CONTRACTORNo ratings yet

- Overview Rev ScheduleIII PravinsethiaDocument26 pagesOverview Rev ScheduleIII PravinsethiaRakhi SahaniNo ratings yet

- U NT N: Module 21 Professional ResponsibilitiesDocument2 pagesU NT N: Module 21 Professional ResponsibilitiesZeyad El-sayedNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument22 pages© The Institute of Chartered Accountants of IndiaHemant AherNo ratings yet

- Consolidated BTL 02 03Document36 pagesConsolidated BTL 02 03santoshsadanNo ratings yet

- Circulars/Notifications: Legal UpdateDocument8 pagesCirculars/Notifications: Legal UpdateAnupam BaliNo ratings yet

- Guidance Note On CARO 2020 LatestDocument8 pagesGuidance Note On CARO 2020 Latestsanjaypunjabi78No ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- TW9 Ud Ghse V9 HCM 9 ZC 19 UZW1 WB GF0 ZS5 W ZGYDocument1 pageTW9 Ud Ghse V9 HCM 9 ZC 19 UZW1 WB GF0 ZS5 W ZGYmiron68No ratings yet

- CTO Citizens Charter 2020Document58 pagesCTO Citizens Charter 2020miron68No ratings yet

- 2023ExposureDraft - Fines and Penalties Late and Non Filing Draft ExposureDocument12 pages2023ExposureDraft - Fines and Penalties Late and Non Filing Draft Exposuremiron68No ratings yet

- TRANSFER - ISO - CAO Transaction Application Forms - Revised - v02 - 02262018Document1 pageTRANSFER - ISO - CAO Transaction Application Forms - Revised - v02 - 02262018miron68No ratings yet

- 2022notice CRMDDocument1 page2022notice CRMDmiron68No ratings yet

- 2022notice - NOTICE TO THE PUBLIC Sec 162 RCC 2Document2 pages2022notice - NOTICE TO THE PUBLIC Sec 162 RCC 2miron68No ratings yet

- DOF Package 2 UPSEAA Presentation by Usec Karl Kendrick Chua Oct 21 2019Document61 pagesDOF Package 2 UPSEAA Presentation by Usec Karl Kendrick Chua Oct 21 2019miron68No ratings yet

- RMC No 61 2016Document6 pagesRMC No 61 2016miron68No ratings yet

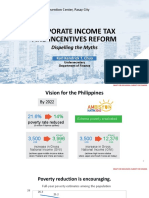

- Corporate Income Tax and Incentives Reform: Dispelling The MythsDocument47 pagesCorporate Income Tax and Incentives Reform: Dispelling The Mythsmiron68No ratings yet

- Conceptual Design Development Agreement: June 2010Document12 pagesConceptual Design Development Agreement: June 2010miron68No ratings yet

- 20141105-Contract-and-NTP-Printing of 2013 Annual ReportDocument11 pages20141105-Contract-and-NTP-Printing of 2013 Annual Reportmiron68No ratings yet

- Special Power of AttorneyDocument2 pagesSpecial Power of Attorneymiron68No ratings yet

- Field Experience B: Principal Interview 1Document7 pagesField Experience B: Principal Interview 1Raymond BartonNo ratings yet

- Universal: Make NoDocument8 pagesUniversal: Make NoChinmaya BeheraNo ratings yet

- 03 Practice Exercise 1Document1 page03 Practice Exercise 1Missy YamaroNo ratings yet

- XLSCDocument8 pagesXLSCpanjumuttaaiNo ratings yet

- Gloria Jeans CoffeesDocument21 pagesGloria Jeans CoffeessrynqranNo ratings yet

- Aeon7200 Service Manual-V00.01-A4Document37 pagesAeon7200 Service Manual-V00.01-A4annaya kitaNo ratings yet

- Dynea Group Annual Report 2010Document47 pagesDynea Group Annual Report 2010Vistasp MajorNo ratings yet

- If We're All So Busy, Why Isn't Anything Getting Done?: People & Organizational Performance PracticeDocument6 pagesIf We're All So Busy, Why Isn't Anything Getting Done?: People & Organizational Performance PracticeRahul PambharNo ratings yet

- CRN 7542 IRR Fair Election ActDocument16 pagesCRN 7542 IRR Fair Election Actjuju_batugalNo ratings yet

- Engleski - Strucni Centralni TerminiDocument56 pagesEngleski - Strucni Centralni TerminivjakovljevicNo ratings yet

- Ebbs & Flows: EM Maiden Funds Outflow in 15 WeeksDocument9 pagesEbbs & Flows: EM Maiden Funds Outflow in 15 WeeksNgọcThủy100% (1)

- Icr18650j V8 80044Document1 pageIcr18650j V8 80044rrebollarNo ratings yet

- Working DrawingDocument21 pagesWorking DrawingBelachew Dosegnaw100% (1)

- Session 8 & 9 - Sales and Operations Planning Faculty - Dr. CP Garg, IIM RohtakDocument31 pagesSession 8 & 9 - Sales and Operations Planning Faculty - Dr. CP Garg, IIM RohtakSiddharthNo ratings yet

- Diagnostic Manual: Scorpio VLX-non RefreshDocument24 pagesDiagnostic Manual: Scorpio VLX-non RefreshMarcelo MendozaNo ratings yet

- (Scaled Agile Framework) : Devops Team, Amid BorhaniDocument28 pages(Scaled Agile Framework) : Devops Team, Amid BorhaniAmid BorhaniNo ratings yet

- Guidelines On Mainstreaming DRR and CCA in The Comprehensive Development PlanDocument35 pagesGuidelines On Mainstreaming DRR and CCA in The Comprehensive Development PlanRey Jan Sly100% (6)

- Path SensitizationDocument4 pagesPath SensitizationTarun SinghNo ratings yet

- Assessment & Development Centre Workshop: Psyasia International'SDocument5 pagesAssessment & Development Centre Workshop: Psyasia International'SAditya BagaswaraNo ratings yet

- Yima Clothing Wholesale Market - An Exploration of Zhanxi Clothing Market Area - Business in GuangzhDocument5 pagesYima Clothing Wholesale Market - An Exploration of Zhanxi Clothing Market Area - Business in GuangzhjacksparrowNo ratings yet

- Micro Surfacing BrochureDocument5 pagesMicro Surfacing Brochureadilumer2No ratings yet

- Gas Sweetening Processes: (1) 73000 Nm3/H (2) 139000 Nm3/H Peak (3) 1.57 Mnm3/D PeakDocument1 pageGas Sweetening Processes: (1) 73000 Nm3/H (2) 139000 Nm3/H Peak (3) 1.57 Mnm3/D PeakAjaykumarNo ratings yet

- Commercial Kitchen VentilationDocument46 pagesCommercial Kitchen Ventilationjeremie whiteNo ratings yet

- DRT450 Reach Stacker SpecDocument4 pagesDRT450 Reach Stacker SpecNuñez Jesus100% (4)

- Deductions From Income From Other SourcesDocument7 pagesDeductions From Income From Other SourcesPADMANABHAN POTTINo ratings yet

- A Presentation On PEDocument28 pagesA Presentation On PEanishNo ratings yet

- Lovely Professional University Assingment of Human Resource ManagementDocument7 pagesLovely Professional University Assingment of Human Resource ManagementRajesh GuptaNo ratings yet

- Government e Marketplace (GeM) - 10.01.2024Document9 pagesGovernment e Marketplace (GeM) - 10.01.2024SSPOS DHULENo ratings yet

- Bodor Nest Tube ManualDocument22 pagesBodor Nest Tube ManualNam NguyenNo ratings yet

Download as pdf or txt

You might also like

- NCWC Final ReportDocument26 pagesNCWC Final ReportAnitah MasoniNo ratings yet

- Companies (General Provisions and Forms) Regulations 2018Document99 pagesCompanies (General Provisions and Forms) Regulations 2018YousafNo ratings yet

- Revised SRC Rule 68 SummaryDocument85 pagesRevised SRC Rule 68 SummaryBernadette Cervantes100% (3)

- Bpi - Sec Cert TemplateDocument2 pagesBpi - Sec Cert Templatemiron68100% (2)

- Financial Reporting Bulletins (Revised As of 2022) : While Those Deleted Were Marked As SuchDocument16 pagesFinancial Reporting Bulletins (Revised As of 2022) : While Those Deleted Were Marked As SuchMark Anthony B. BacayoNo ratings yet

- Compilation of Material Findings On 2019 Afs Reviewed by The CommissionDocument10 pagesCompilation of Material Findings On 2019 Afs Reviewed by The CommissionAllyssa Camille ArcangelNo ratings yet

- Cap 622D Consolidated Version For The Whole Chapter (01-02-2019) (English)Document10 pagesCap 622D Consolidated Version For The Whole Chapter (01-02-2019) (English)Jessica YimNo ratings yet

- 74931bos60524 m1 AnnexureDocument38 pages74931bos60524 m1 AnnexureBala Guru Prasad TadikamallaNo ratings yet

- CARODocument9 pagesCAROSai Lakshmi PNo ratings yet

- Financial Reporting BulletinsDocument3 pagesFinancial Reporting BulletinsEmil A. MolinaNo ratings yet

- Apollo Tyres Annual Report FY2023-260-274Document15 pagesApollo Tyres Annual Report FY2023-260-274Carrots TopNo ratings yet

- Rules, 2018 To Amend The Companies (Audit and Auditors) Rules, 2014Document46 pagesRules, 2018 To Amend The Companies (Audit and Auditors) Rules, 2014Sunil DesaiNo ratings yet

- Rules, 2018 To Amend The Companies (Audit and Auditors) Rules, 2014Document59 pagesRules, 2018 To Amend The Companies (Audit and Auditors) Rules, 2014RAJANEESH V RNo ratings yet

- ICSIsuggestion 2009Document117 pagesICSIsuggestion 2009Iqbaljit Singh AujlaNo ratings yet

- Rev SCH III - Sent PDFDocument18 pagesRev SCH III - Sent PDFAjay DesaleNo ratings yet

- CSR MB 2023Document46 pagesCSR MB 2023Marie BanuNo ratings yet

- Caro 2020Document11 pagesCaro 2020Gaurav Chauhan CANo ratings yet

- Scheme of ArrangementDocument33 pagesScheme of ArrangementVedant MaskeNo ratings yet

- Amendments in Business Law, Ethics and Communication: (For May 2018 Exams (Old Syllabubs) As Per RTP)Document3 pagesAmendments in Business Law, Ethics and Communication: (For May 2018 Exams (Old Syllabubs) As Per RTP)Neha jainNo ratings yet

- Securities and Exchange Board of IndiaDocument8 pagesSecurities and Exchange Board of IndiaDebashis DeyNo ratings yet

- Notification Dated 20.09.2022Document4 pagesNotification Dated 20.09.2022mazars advisoryNo ratings yet

- Advanced AccountingDocument33 pagesAdvanced AccountingvijaykumartaxNo ratings yet

- RTP 2Document44 pagesRTP 2Harsh KumarNo ratings yet

- Companies Act, 2013 PDFDocument25 pagesCompanies Act, 2013 PDFshivam vermaNo ratings yet

- 57996bos47277gp1 PDFDocument126 pages57996bos47277gp1 PDFAnand PandeyNo ratings yet

- Intermediate Accounting RTP May 20Document44 pagesIntermediate Accounting RTP May 20Durgadevi BaskaranNo ratings yet

- Law - May 2020Document18 pagesLaw - May 2020Princy ManglaNo ratings yet

- Law p4Document90 pagesLaw p4Shyam virsinghNo ratings yet

- Sl. No. Particular Provision Form Due Date (Companies Act) Relaxed Due Date (COVID-19) 1Document3 pagesSl. No. Particular Provision Form Due Date (Companies Act) Relaxed Due Date (COVID-19) 1Munish SharmaNo ratings yet

- Departmental Interpretation and Practice Notes No. 7 (Revised)Document33 pagesDepartmental Interpretation and Practice Notes No. 7 (Revised)Difanny KooNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument39 pages© The Institute of Chartered Accountants of IndiaGowriNo ratings yet

- SRC Rule 68 As AmendedDocument51 pagesSRC Rule 68 As AmendedGilYah MoralesNo ratings yet

- CARO 2020 Book NotesDocument11 pagesCARO 2020 Book NotesCreanativeNo ratings yet

- CA Journal - Article On Schedule IIIDocument6 pagesCA Journal - Article On Schedule IIISIDDHARTH MANDELIANo ratings yet

- GEO - Definitive Information Statement 2021Document264 pagesGEO - Definitive Information Statement 2021Aaron HuangNo ratings yet

- Compilation of Material Findings On 2013 AFS of Financing CompaniesDocument5 pagesCompilation of Material Findings On 2013 AFS of Financing CompaniesJuan FrivaldoNo ratings yet

- VAT Administrative Exceptions Guide - EN - 12 03 2020Document14 pagesVAT Administrative Exceptions Guide - EN - 12 03 2020aliNo ratings yet

- Appendix 1 - Letter of EngagementDocument6 pagesAppendix 1 - Letter of Engagementl.lawliet.ryuzaki.frNo ratings yet

- Ind As 108Document10 pagesInd As 108CA Seshan KrishNo ratings yet

- 001Document16 pages001sathya_41095No ratings yet

- LAPD IntR in 2012 09 Arc 11 IN9 Issue 4 Archived On 14 October 2009Document17 pagesLAPD IntR in 2012 09 Arc 11 IN9 Issue 4 Archived On 14 October 2009sibiyazukiswa27No ratings yet

- FR Power Full Book @mission - CA - Final PDFDocument422 pagesFR Power Full Book @mission - CA - Final PDFlaksh sangtaniNo ratings yet

- Master Circular On Preparation of Financial Statements General Insurance BusinessDocument38 pagesMaster Circular On Preparation of Financial Statements General Insurance BusinesslavkmNo ratings yet

- Corporate & Other LawsDocument22 pagesCorporate & Other Laws1234rutikarrrNo ratings yet

- 263081-2019-Revised Securities Regulation Code SRC Rule20210728-11-K6tsx3Document61 pages263081-2019-Revised Securities Regulation Code SRC Rule20210728-11-K6tsx3Regina RozarioNo ratings yet

- Caro, 2020Document11 pagesCaro, 2020IntrovertNo ratings yet

- Unit 2 Corporate Tax Planning and ManagementDocument21 pagesUnit 2 Corporate Tax Planning and Managementsankiworld3No ratings yet

- BCF 405 Financial Reporting - Module 2 PDFDocument45 pagesBCF 405 Financial Reporting - Module 2 PDFNaresh KumarNo ratings yet

- Appendix 8 - Companies Ordinance (Cap. 622) Disclosure ChecklistDocument46 pagesAppendix 8 - Companies Ordinance (Cap. 622) Disclosure Checklistl.lawliet.ryuzaki.frNo ratings yet

- Q3Document24 pagesQ3Mohamed HamedNo ratings yet

- Ca Intermediate Referencer For Quick Revision (ICAI)Document23 pagesCa Intermediate Referencer For Quick Revision (ICAI)Jeet VekariyaNo ratings yet

- The Statement of Financial Position of C F LTD For TheDocument1 pageThe Statement of Financial Position of C F LTD For TheBube KachevskaNo ratings yet

- Form No. 3ae: Audit Report Under Section 35D (4) /35E (6) of The Income-Tax Act, 1961Document2 pagesForm No. 3ae: Audit Report Under Section 35D (4) /35E (6) of The Income-Tax Act, 1961Anonymous 2evaoXKKdNo ratings yet

- Economic Laws Module 1Document405 pagesEconomic Laws Module 1Mohammed AslamNo ratings yet

- Companies Auditors Report Order2020Document5 pagesCompanies Auditors Report Order2020SP CONTRACTORNo ratings yet

- Overview Rev ScheduleIII PravinsethiaDocument26 pagesOverview Rev ScheduleIII PravinsethiaRakhi SahaniNo ratings yet

- U NT N: Module 21 Professional ResponsibilitiesDocument2 pagesU NT N: Module 21 Professional ResponsibilitiesZeyad El-sayedNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument22 pages© The Institute of Chartered Accountants of IndiaHemant AherNo ratings yet

- Consolidated BTL 02 03Document36 pagesConsolidated BTL 02 03santoshsadanNo ratings yet

- Circulars/Notifications: Legal UpdateDocument8 pagesCirculars/Notifications: Legal UpdateAnupam BaliNo ratings yet

- Guidance Note On CARO 2020 LatestDocument8 pagesGuidance Note On CARO 2020 Latestsanjaypunjabi78No ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- TW9 Ud Ghse V9 HCM 9 ZC 19 UZW1 WB GF0 ZS5 W ZGYDocument1 pageTW9 Ud Ghse V9 HCM 9 ZC 19 UZW1 WB GF0 ZS5 W ZGYmiron68No ratings yet

- CTO Citizens Charter 2020Document58 pagesCTO Citizens Charter 2020miron68No ratings yet

- 2023ExposureDraft - Fines and Penalties Late and Non Filing Draft ExposureDocument12 pages2023ExposureDraft - Fines and Penalties Late and Non Filing Draft Exposuremiron68No ratings yet

- TRANSFER - ISO - CAO Transaction Application Forms - Revised - v02 - 02262018Document1 pageTRANSFER - ISO - CAO Transaction Application Forms - Revised - v02 - 02262018miron68No ratings yet

- 2022notice CRMDDocument1 page2022notice CRMDmiron68No ratings yet

- 2022notice - NOTICE TO THE PUBLIC Sec 162 RCC 2Document2 pages2022notice - NOTICE TO THE PUBLIC Sec 162 RCC 2miron68No ratings yet

- DOF Package 2 UPSEAA Presentation by Usec Karl Kendrick Chua Oct 21 2019Document61 pagesDOF Package 2 UPSEAA Presentation by Usec Karl Kendrick Chua Oct 21 2019miron68No ratings yet

- RMC No 61 2016Document6 pagesRMC No 61 2016miron68No ratings yet

- Corporate Income Tax and Incentives Reform: Dispelling The MythsDocument47 pagesCorporate Income Tax and Incentives Reform: Dispelling The Mythsmiron68No ratings yet

- Conceptual Design Development Agreement: June 2010Document12 pagesConceptual Design Development Agreement: June 2010miron68No ratings yet

- 20141105-Contract-and-NTP-Printing of 2013 Annual ReportDocument11 pages20141105-Contract-and-NTP-Printing of 2013 Annual Reportmiron68No ratings yet

- Special Power of AttorneyDocument2 pagesSpecial Power of Attorneymiron68No ratings yet

- Field Experience B: Principal Interview 1Document7 pagesField Experience B: Principal Interview 1Raymond BartonNo ratings yet

- Universal: Make NoDocument8 pagesUniversal: Make NoChinmaya BeheraNo ratings yet

- 03 Practice Exercise 1Document1 page03 Practice Exercise 1Missy YamaroNo ratings yet

- XLSCDocument8 pagesXLSCpanjumuttaaiNo ratings yet

- Gloria Jeans CoffeesDocument21 pagesGloria Jeans CoffeessrynqranNo ratings yet

- Aeon7200 Service Manual-V00.01-A4Document37 pagesAeon7200 Service Manual-V00.01-A4annaya kitaNo ratings yet

- Dynea Group Annual Report 2010Document47 pagesDynea Group Annual Report 2010Vistasp MajorNo ratings yet

- If We're All So Busy, Why Isn't Anything Getting Done?: People & Organizational Performance PracticeDocument6 pagesIf We're All So Busy, Why Isn't Anything Getting Done?: People & Organizational Performance PracticeRahul PambharNo ratings yet

- CRN 7542 IRR Fair Election ActDocument16 pagesCRN 7542 IRR Fair Election Actjuju_batugalNo ratings yet

- Engleski - Strucni Centralni TerminiDocument56 pagesEngleski - Strucni Centralni TerminivjakovljevicNo ratings yet

- Ebbs & Flows: EM Maiden Funds Outflow in 15 WeeksDocument9 pagesEbbs & Flows: EM Maiden Funds Outflow in 15 WeeksNgọcThủy100% (1)

- Icr18650j V8 80044Document1 pageIcr18650j V8 80044rrebollarNo ratings yet

- Working DrawingDocument21 pagesWorking DrawingBelachew Dosegnaw100% (1)

- Session 8 & 9 - Sales and Operations Planning Faculty - Dr. CP Garg, IIM RohtakDocument31 pagesSession 8 & 9 - Sales and Operations Planning Faculty - Dr. CP Garg, IIM RohtakSiddharthNo ratings yet

- Diagnostic Manual: Scorpio VLX-non RefreshDocument24 pagesDiagnostic Manual: Scorpio VLX-non RefreshMarcelo MendozaNo ratings yet

- (Scaled Agile Framework) : Devops Team, Amid BorhaniDocument28 pages(Scaled Agile Framework) : Devops Team, Amid BorhaniAmid BorhaniNo ratings yet

- Guidelines On Mainstreaming DRR and CCA in The Comprehensive Development PlanDocument35 pagesGuidelines On Mainstreaming DRR and CCA in The Comprehensive Development PlanRey Jan Sly100% (6)

- Path SensitizationDocument4 pagesPath SensitizationTarun SinghNo ratings yet

- Assessment & Development Centre Workshop: Psyasia International'SDocument5 pagesAssessment & Development Centre Workshop: Psyasia International'SAditya BagaswaraNo ratings yet

- Yima Clothing Wholesale Market - An Exploration of Zhanxi Clothing Market Area - Business in GuangzhDocument5 pagesYima Clothing Wholesale Market - An Exploration of Zhanxi Clothing Market Area - Business in GuangzhjacksparrowNo ratings yet

- Micro Surfacing BrochureDocument5 pagesMicro Surfacing Brochureadilumer2No ratings yet

- Gas Sweetening Processes: (1) 73000 Nm3/H (2) 139000 Nm3/H Peak (3) 1.57 Mnm3/D PeakDocument1 pageGas Sweetening Processes: (1) 73000 Nm3/H (2) 139000 Nm3/H Peak (3) 1.57 Mnm3/D PeakAjaykumarNo ratings yet

- Commercial Kitchen VentilationDocument46 pagesCommercial Kitchen Ventilationjeremie whiteNo ratings yet

- DRT450 Reach Stacker SpecDocument4 pagesDRT450 Reach Stacker SpecNuñez Jesus100% (4)

- Deductions From Income From Other SourcesDocument7 pagesDeductions From Income From Other SourcesPADMANABHAN POTTINo ratings yet

- A Presentation On PEDocument28 pagesA Presentation On PEanishNo ratings yet

- Lovely Professional University Assingment of Human Resource ManagementDocument7 pagesLovely Professional University Assingment of Human Resource ManagementRajesh GuptaNo ratings yet

- Government e Marketplace (GeM) - 10.01.2024Document9 pagesGovernment e Marketplace (GeM) - 10.01.2024SSPOS DHULENo ratings yet

- Bodor Nest Tube ManualDocument22 pagesBodor Nest Tube ManualNam NguyenNo ratings yet