Download as xlsx, pdf, or txt

You might also like

- Final Grading Exam - Key AnswersDocument35 pagesFinal Grading Exam - Key AnswersJEFFERSON CUTE97% (32)

- GETHICS - MIDTERM EXAMINATION - 1ST SEMESTER - 2022-2023 1st PartDocument5 pagesGETHICS - MIDTERM EXAMINATION - 1ST SEMESTER - 2022-2023 1st PartMariette Alex AgbanlogNo ratings yet

- Case 3Document13 pagesCase 3Prezi Toli100% (1)

- Audit of Long Term Liabilities 2Document5 pagesAudit of Long Term Liabilities 2Cesar EsguerraNo ratings yet

- Machete Company Requirement: Prepare Journal Entries Debit CreditDocument1 pageMachete Company Requirement: Prepare Journal Entries Debit CreditAnonnNo ratings yet

- Chapter 24 Answer KeyDocument3 pagesChapter 24 Answer KeyShane TabunggaoNo ratings yet

- Investments in Debt SecuritiesDocument34 pagesInvestments in Debt SecuritiesNobu NobuNo ratings yet

- Assignment On LiabilitiesDocument7 pagesAssignment On LiabilitiesVixen Aaron EnriquezNo ratings yet

- Acctg Lab 4Document3 pagesAcctg Lab 4AngieNo ratings yet

- Lecture Note BBF311 - 014718Document9 pagesLecture Note BBF311 - 014718saidsulaiman2095No ratings yet

- Lecture Note On Investment - 013451Document9 pagesLecture Note On Investment - 013451saidsulaiman2095No ratings yet

- Gonzalez, John Williever A. - Bonds Payable-Between Interest Dates and SerialDocument4 pagesGonzalez, John Williever A. - Bonds Payable-Between Interest Dates and SerialJohn Williever GonzalezNo ratings yet

- Chapter 20 - Effective Interest Method (Amortized Cost, FVOCI, FVPL)Document66 pagesChapter 20 - Effective Interest Method (Amortized Cost, FVOCI, FVPL)Never Letting GoNo ratings yet

- 9TH Bonds Payable Part IIDocument8 pages9TH Bonds Payable Part IIAnthony DyNo ratings yet

- Renton Effective Am21Document5 pagesRenton Effective Am21Kris Hazel RentonNo ratings yet

- Exercise 14Document11 pagesExercise 14dwitaNo ratings yet

- BOND Part 1Document8 pagesBOND Part 1James Ryan AlzonaNo ratings yet

- Ia2 Final Exam A Test Bank - CompressDocument32 pagesIa2 Final Exam A Test Bank - CompressFiona MiralpesNo ratings yet

- Intermediate AccountingDocument10 pagesIntermediate AccountingJean AmisiNo ratings yet

- Note Payable Irrevocably Designated As at Fair Value Through Profit or LossDocument4 pagesNote Payable Irrevocably Designated As at Fair Value Through Profit or Lossnot funny didn't laughNo ratings yet

- Chapter 16Document6 pagesChapter 16YasirNo ratings yet

- IA 1 - Chapter 6 Notes Receivable Problems Part 2Document11 pagesIA 1 - Chapter 6 Notes Receivable Problems Part 2John CentinoNo ratings yet

- Investment in Associate ExercisesDocument7 pagesInvestment in Associate ExercisesJo KeNo ratings yet

- Bonds Payable-Between Interest Dates and SerialDocument4 pagesBonds Payable-Between Interest Dates and SerialJohn Williever GonzalezNo ratings yet

- Problem 6-1: Interest Expense Present ValueDocument3 pagesProblem 6-1: Interest Expense Present ValueAngieNo ratings yet

- Lobrigas Unit3 Topic1 AssessmentDocument9 pagesLobrigas Unit3 Topic1 AssessmentClaudine LobrigasNo ratings yet

- Chapter 14 - Homework AnswerDocument10 pagesChapter 14 - Homework AnswerSaja AlbarjesNo ratings yet

- BANGI, Joshua Celton - Assign2.Document7 pagesBANGI, Joshua Celton - Assign2.Joshua BangiNo ratings yet

- 07 Loan Receivable MCPDocument4 pages07 Loan Receivable MCPkyle mandaresioNo ratings yet

- Notes Payable: Problem 1: True or FalseDocument16 pagesNotes Payable: Problem 1: True or FalseKim HanbinNo ratings yet

- Chapter 8Document6 pagesChapter 8swaroopcharmiNo ratings yet

- AP-LIABS-3 (With Answers)Document4 pagesAP-LIABS-3 (With Answers)Kendrew SujideNo ratings yet

- Audprob Bonds Problem With SolutionsDocument4 pagesAudprob Bonds Problem With Solutionsreviewrecord.rr2No ratings yet

- Chapter 08-Borrowing Costs-Tutorial AnswersDocument4 pagesChapter 08-Borrowing Costs-Tutorial AnswersMayomi JayasooriyaNo ratings yet

- Lecture-Borrowing Costs and Exchange of Nonmonetary AssetDocument6 pagesLecture-Borrowing Costs and Exchange of Nonmonetary AssetorillosachristoperjohnNo ratings yet

- PracticeSet BondsPayableDocument5 pagesPracticeSet BondsPayablearabelle contrerasNo ratings yet

- Cyntia Amelia Siregar-4b-Lat-9-Pt. Palas Star PlantationDocument8 pagesCyntia Amelia Siregar-4b-Lat-9-Pt. Palas Star PlantationAmel GpNo ratings yet

- Chapter 20 CompilationDocument41 pagesChapter 20 CompilationMaria Licuanan0% (1)

- Quiz 2 BPDocument4 pagesQuiz 2 BPspur iousNo ratings yet

- Aol AccDocument19 pagesAol AccANGELYCA LAURANo ratings yet

- Lobrigas Unit3 Topic2 AssessmentDocument6 pagesLobrigas Unit3 Topic2 AssessmentClaudine LobrigasNo ratings yet

- Cherryl Febryan Christyanto - 202030225Document6 pagesCherryl Febryan Christyanto - 202030225Cherryl Febryan ChristyantoNo ratings yet

- Quiz 4 With SolutionDocument5 pagesQuiz 4 With SolutionKarl Lincoln TemporosaNo ratings yet

- (Chapter 2) Sol Man of Intermediate Accounting 2 by Zeus MillanDocument17 pages(Chapter 2) Sol Man of Intermediate Accounting 2 by Zeus MillanJonathan Villazon RosalesNo ratings yet

- Problem 5-3 Requirement 1 2020Document7 pagesProblem 5-3 Requirement 1 2020Adyagila Ecarg NelehNo ratings yet

- Liabilities Part 2Document43 pagesLiabilities Part 2Luisa Janelle BoquirenNo ratings yet

- Quiz 2 BP With Answers PDFDocument4 pagesQuiz 2 BP With Answers PDFspur iousNo ratings yet

- Bonds Problem With Solutions 2Document4 pagesBonds Problem With Solutions 2reviewrecord.rr2No ratings yet

- Audprob Bonds Problem With Solutions 2Document4 pagesAudprob Bonds Problem With Solutions 2reviewrecord.rr2No ratings yet

- Answer Key - Problem Sets - Adjusting EntriesDocument2 pagesAnswer Key - Problem Sets - Adjusting EntriesAlexa AbaryNo ratings yet

- Bonds Payable Issued at A PremiumDocument6 pagesBonds Payable Issued at A PremiumCris Ann Marie ESPAnOLANo ratings yet

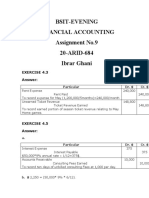

- Bsit-Evening Financial Accounting Assignment No.9 20-ARID-684 Ibrar GhaniDocument3 pagesBsit-Evening Financial Accounting Assignment No.9 20-ARID-684 Ibrar Ghaniibrar ghani100% (1)

- (Ust-Jpia) Quiz 1 Intermediate Accounting 2 Solution ManualDocument6 pages(Ust-Jpia) Quiz 1 Intermediate Accounting 2 Solution ManualRENZ ALFRED ASTRERONo ratings yet

- Acc 201 CH 10Document16 pagesAcc 201 CH 10Trickster TwelveNo ratings yet

- GUINTO - Activity 1 - Loans and Impairment ReceivableDocument4 pagesGUINTO - Activity 1 - Loans and Impairment ReceivableGUINTO, DAN FRANCIS B.No ratings yet

- Problem 3Document11 pagesProblem 3Charmaine Kaye OndoyNo ratings yet

- SS CT 1 FAR270 Sem MAC2022 StudentDocument4 pagesSS CT 1 FAR270 Sem MAC2022 Studentsharifah nurshahira sakinaNo ratings yet

- Fra 3Document7 pagesFra 3Subhajyoti MukhopadhyayNo ratings yet

- Using Economic Indicators to Improve Investment AnalysisFrom EverandUsing Economic Indicators to Improve Investment AnalysisRating: 3.5 out of 5 stars3.5/5 (1)

- Deed of Absolute Sale: Know All Men by These PresentsDocument3 pagesDeed of Absolute Sale: Know All Men by These PresentsMariette Alex AgbanlogNo ratings yet

- Individual (Scott Rae's 7-Step Model) : Agbanlog, Mariette Alex, G. 1721-Ethics SamcisDocument1 pageIndividual (Scott Rae's 7-Step Model) : Agbanlog, Mariette Alex, G. 1721-Ethics SamcisMariette Alex AgbanlogNo ratings yet

- Submitted By:: Abarientos, Ashly Kate Agbanlog, Mariette Alex Gatchallan, Jeremiel Rodas, Norym JhairhaDocument5 pagesSubmitted By:: Abarientos, Ashly Kate Agbanlog, Mariette Alex Gatchallan, Jeremiel Rodas, Norym JhairhaMariette Alex AgbanlogNo ratings yet

- SAMCIS 1318 GRIZAL - AssignmentDocument2 pagesSAMCIS 1318 GRIZAL - AssignmentMariette Alex AgbanlogNo ratings yet

- C Dÿ Efg Ÿ H/Imq Ÿ /wjÿ Hmwÿ Epo V KV O Z: Lllmlnopqr ST Uvst WxÿDocument9 pagesC Dÿ Efg Ÿ H/Imq Ÿ /wjÿ Hmwÿ Epo V KV O Z: Lllmlnopqr ST Uvst WxÿMariette Alex AgbanlogNo ratings yet

- NSTP 1 - M4 - Engage - AsDocument1 pageNSTP 1 - M4 - Engage - AsMariette Alex AgbanlogNo ratings yet

- AE211 Final ExamDocument10 pagesAE211 Final ExamMariette Alex AgbanlogNo ratings yet

- 1719 - Midterm Exams - CFE104: Multiple ChoiceDocument9 pages1719 - Midterm Exams - CFE104: Multiple ChoiceMariette Alex AgbanlogNo ratings yet

- SAMCIS 7867-FIT-OA-PPA-FinalsDocument4 pagesSAMCIS 7867-FIT-OA-PPA-FinalsMariette Alex AgbanlogNo ratings yet

- AGBANLOG - SAMCIS GPPC 1584 - M3 Elaborate PDFDocument1 pageAGBANLOG - SAMCIS GPPC 1584 - M3 Elaborate PDFMariette Alex AgbanlogNo ratings yet

- AGBANLOG - SAMCIS 1530 - POM. Module 6. Unit 2. Activity 14 PDFDocument2 pagesAGBANLOG - SAMCIS 1530 - POM. Module 6. Unit 2. Activity 14 PDFMariette Alex AgbanlogNo ratings yet

- Formative Assessment Chap 3 & 6Document5 pagesFormative Assessment Chap 3 & 6Mariette Alex AgbanlogNo ratings yet

- CMPC 131-Finals Fa1Document6 pagesCMPC 131-Finals Fa1Mariette Alex AgbanlogNo ratings yet

- Cost Midterms Quiz 2 PDFDocument15 pagesCost Midterms Quiz 2 PDFMariette Alex AgbanlogNo ratings yet

- AGBANLOG SAMCIS 7867-FIT-OA-Task 5a Backpacking Plan and Brochure - MakingDocument4 pagesAGBANLOG SAMCIS 7867-FIT-OA-Task 5a Backpacking Plan and Brochure - MakingMariette Alex AgbanlogNo ratings yet

- 7833 Fit - CS Final ExamDocument22 pages7833 Fit - CS Final ExamMariette Alex AgbanlogNo ratings yet

- AGBANLOG, MARIETTE ALEX, GARCIA - SAMCIS 1235 - CMPC 131 - Grade ComputationDocument2 pagesAGBANLOG, MARIETTE ALEX, GARCIA - SAMCIS 1235 - CMPC 131 - Grade ComputationMariette Alex AgbanlogNo ratings yet

- Cost Fa3Document17 pagesCost Fa3Mariette Alex AgbanlogNo ratings yet

- POM ReviewerDocument14 pagesPOM ReviewerMariette Alex AgbanlogNo ratings yet

- Ae 212 Midterm Departmental Exam - Docx-1Document12 pagesAe 212 Midterm Departmental Exam - Docx-1Mariette Alex AgbanlogNo ratings yet

- Pom M3u5 Act 9Document3 pagesPom M3u5 Act 9Mariette Alex AgbanlogNo ratings yet

- Agbanlog - 1316 - BLR 211 - Articles of PartnershipDocument3 pagesAgbanlog - 1316 - BLR 211 - Articles of PartnershipMariette Alex AgbanlogNo ratings yet

- Ae212 Finals Quiz 1Document5 pagesAe212 Finals Quiz 1Mariette Alex AgbanlogNo ratings yet

- SAMCIS 7867 FIT - OA - Task 5b Backpacking Plan and Brochure - MakingDocument1 pageSAMCIS 7867 FIT - OA - Task 5b Backpacking Plan and Brochure - MakingMariette Alex AgbanlogNo ratings yet

- SAMCIS 1668-CFE 103 - Final Exam - 1stsem - AY 22-23Document3 pagesSAMCIS 1668-CFE 103 - Final Exam - 1stsem - AY 22-23Mariette Alex AgbanlogNo ratings yet

- AGBANLOG - SAMCIS GSELF 1729 - Journal Entry #3 - Real Self Vs Ideal SelfDocument1 pageAGBANLOG - SAMCIS GSELF 1729 - Journal Entry #3 - Real Self Vs Ideal SelfMariette Alex Agbanlog100% (2)

- Construction Contract: Lyceum of Subic BayDocument10 pagesConstruction Contract: Lyceum of Subic BayMariette Alex AgbanlogNo ratings yet

- Sa1 Ae 121 - TheoriesDocument6 pagesSa1 Ae 121 - TheoriesMariette Alex AgbanlogNo ratings yet

- Midterm Examination BeeDocument18 pagesMidterm Examination BeeMariette Alex Agbanlog100% (1)