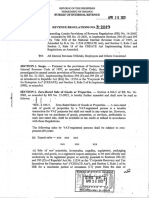

RMC No. 49-2022

RMC No. 49-2022

You might also like

- Rmo 43-90 PDFDocument5 pagesRmo 43-90 PDFRieland Cuevas67% (3)

- Aws A5.02Document30 pagesAws A5.02Meilati Pasca MunaNo ratings yet

- Mental Health LawsuitDocument2 pagesMental Health LawsuitGordon L. HinsonNo ratings yet

- Bureau of Internal RevenueDocument11 pagesBureau of Internal RevenueRomer LesondatoNo ratings yet

- Module 4 - Value Added TaxDocument16 pagesModule 4 - Value Added Taxanon_455551365No ratings yet

- Cfe Brochure 2015 PDFDocument12 pagesCfe Brochure 2015 PDFSittyNo ratings yet

- RMC No. 24-2022Document13 pagesRMC No. 24-2022arnulfojr hicoNo ratings yet

- (VAT) in To: Clarifying (RR) No. The The Tax of (TaxDocument13 pages(VAT) in To: Clarifying (RR) No. The The Tax of (TaxShiela Marie Maraon100% (1)

- Who To File RPTDocument9 pagesWho To File RPTLacie Hohenheim (Doraemon)No ratings yet

- COMMISSIONER OF INTERNAL REVENUE V Cebu Toyo CorpDocument5 pagesCOMMISSIONER OF INTERNAL REVENUE V Cebu Toyo CorpAustin Viel Lagman MedinaNo ratings yet

- Commissioner of Internal Revenue vs. Toshiba Information Equipment (Phils.), Inc., 466 SCRA 211, August 09, 2005Document4 pagesCommissioner of Internal Revenue vs. Toshiba Information Equipment (Phils.), Inc., 466 SCRA 211, August 09, 2005idolbondocNo ratings yet

- Rulings2000 DigestDocument21 pagesRulings2000 DigestArriane MartinezNo ratings yet

- 2 Value Added TaxDocument216 pages2 Value Added TaxnichNo ratings yet

- Value-Added Tax Nature of VatDocument22 pagesValue-Added Tax Nature of VatDiossaNo ratings yet

- CIR vs. ToshibaDocument3 pagesCIR vs. ToshibaKayelyn Lat100% (1)

- Petitioner Respondent Litigation Division (BIR) Avisado Agan Montenegro & AssociatesDocument17 pagesPetitioner Respondent Litigation Division (BIR) Avisado Agan Montenegro & AssociatesRobert Jayson UyNo ratings yet

- Atlas Consolidated Mining V CIR (Case Digest)Document2 pagesAtlas Consolidated Mining V CIR (Case Digest)Jeng Pion100% (2)

- Module 3 Tax Preferences Available For Sole Proprietorship BusinessDocument7 pagesModule 3 Tax Preferences Available For Sole Proprietorship Businessangclaire47No ratings yet

- Value Added Tax Ust PDFDocument23 pagesValue Added Tax Ust PDFcalliemozartNo ratings yet

- Coral Bay Tax DigestDocument3 pagesCoral Bay Tax DigestJonathan Dela Cruz100% (1)

- RR No. 3-2023Document6 pagesRR No. 3-2023Anostasia NemusNo ratings yet

- CIR vs. CA - G.R. No. 125355 (Digest)Document7 pagesCIR vs. CA - G.R. No. 125355 (Digest)Karen Gina DupraNo ratings yet

- RR No. 34-2020 v2Document3 pagesRR No. 34-2020 v2JejomarNo ratings yet

- CIR v. Toshiba Information Equipment (Phils.) IncDocument2 pagesCIR v. Toshiba Information Equipment (Phils.) IncEJ PajaroNo ratings yet

- Powerpoint-03 19 22Document126 pagesPowerpoint-03 19 22CrizziaNo ratings yet

- RMC No. 50-2007 PDFDocument6 pagesRMC No. 50-2007 PDFAnonymous yKUdPvwjNo ratings yet

- Vat - 1Document20 pagesVat - 1biburaNo ratings yet

- Fort Bonifacio v. CIRDocument3 pagesFort Bonifacio v. CIRAngelique Padilla UgayNo ratings yet

- Cir Vs ToshibaDocument23 pagesCir Vs ToshibamarkNo ratings yet

- 112034-2005-Commissioner of Internal Revenue v. Toshiba20180404-1159-12ci6skDocument15 pages112034-2005-Commissioner of Internal Revenue v. Toshiba20180404-1159-12ci6skCamshtNo ratings yet

- Value Added TaxDocument20 pagesValue Added TaxJerlene Sydney Centeno100% (1)

- Revenue Memorandum Circular No. 62-05: SubjectDocument12 pagesRevenue Memorandum Circular No. 62-05: Subject김비앙카No ratings yet

- Excel Professional Services, Inc.: Management Firm of Professional Review and Training Center (PRTC)Document3 pagesExcel Professional Services, Inc.: Management Firm of Professional Review and Training Center (PRTC)Mae Angiela TansecoNo ratings yet

- BMBE SeminarDocument60 pagesBMBE SeminarBabyGiant LucasNo ratings yet

- Tranzen1A Income TaxDocument46 pagesTranzen1A Income TaxMonica SorianoNo ratings yet

- RegistrationDocument127 pagesRegistrationDa Yani ChristeeneNo ratings yet

- RMC No. 50-2007Document6 pagesRMC No. 50-2007scribe03No ratings yet

- RR No. 07-12Document53 pagesRR No. 07-12Nash Ortiz LuisNo ratings yet

- RMC No. 8-2024Document5 pagesRMC No. 8-2024Anostasia NemusNo ratings yet

- RR 3-2023 Digest FINALDocument4 pagesRR 3-2023 Digest FINALAkld D LerioNo ratings yet

- Tax 1 Case DigestsDocument50 pagesTax 1 Case Digestso6739No ratings yet

- Free Commercial ZoneDocument12 pagesFree Commercial ZoneQueenie ChongNo ratings yet

- Articles About VAT Zero-RatingDocument8 pagesArticles About VAT Zero-RatingkmoNo ratings yet

- Relevant BIR UpdatesDocument49 pagesRelevant BIR UpdatesElsha dela penaNo ratings yet

- Tax Alert - 2005 - FebDocument11 pagesTax Alert - 2005 - FebzhanleriNo ratings yet

- Rs 22,510 Rs 743 367 Rs.36,748: TotalDocument2 pagesRs 22,510 Rs 743 367 Rs.36,748: Totalasad khokharNo ratings yet

- 43677RMO 3-2009 - Suspension GroundsDocument29 pages43677RMO 3-2009 - Suspension GroundsAnonymous OyhbxcjNo ratings yet

- Rmo 3-2009Document29 pagesRmo 3-2009sheena100% (2)

- VAT ZERO-RATED SALES - CIR V ToshibaDocument6 pagesVAT ZERO-RATED SALES - CIR V ToshibaChristine Gel MadrilejoNo ratings yet

- VAT of BangladeshDocument111 pagesVAT of BangladeshNahian HasanNo ratings yet

- Tax Brief - June 2012Document8 pagesTax Brief - June 2012Rheneir MoraNo ratings yet

- Chapter 7 MCQ'S AssignmentDocument3 pagesChapter 7 MCQ'S AssignmentMary Joy CabilNo ratings yet

- Chapter 15 - Tax IncentivesDocument26 pagesChapter 15 - Tax IncentivesForjosh VNo ratings yet

- 142 150Document7 pages142 150NikkandraNo ratings yet

- New VAT Audit FormatDocument12 pagesNew VAT Audit FormatparulshinyNo ratings yet

- Tax UpdatesDocument19 pagesTax UpdatesYeoh MaeNo ratings yet

- Commentary On Withholding RulesDocument6 pagesCommentary On Withholding RulesTanzeel Ur Rahman GazdarNo ratings yet

- Tax Vat Cases DigestDocument34 pagesTax Vat Cases DigestNievesAlarconNo ratings yet

- BIR RMC No. 62-2005Document15 pagesBIR RMC No. 62-2005dencave1No ratings yet

- 1999 BIR RulingsDocument74 pages1999 BIR Rulingschris cardinoNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- Revenue Memorandum Order No. 19-2006 Subject:: Bureau of Internal RevenueDocument2 pagesRevenue Memorandum Order No. 19-2006 Subject:: Bureau of Internal RevenueSittyNo ratings yet

- RMC No. 36-2022Document2 pagesRMC No. 36-2022SittyNo ratings yet

- Vat Zero-Rate Certification Certificate No. (YYYY - )Document2 pagesVat Zero-Rate Certification Certificate No. (YYYY - )SittyNo ratings yet

- Coa Logo For PrintingDocument2 pagesCoa Logo For PrintingSittyNo ratings yet

- Caltex Vs CoaDocument25 pagesCaltex Vs CoaSittyNo ratings yet

- (Prescribed Form) : (Place A Copy of The Mark in The Box. The Mark Should Be Clear Enough To Be Reproduced and Digitized)Document1 page(Prescribed Form) : (Place A Copy of The Mark in The Box. The Mark Should Be Clear Enough To Be Reproduced and Digitized)SittyNo ratings yet

- Wallace v. Eclipse Pocahontas Coal Co Case DigestDocument1 pageWallace v. Eclipse Pocahontas Coal Co Case DigestSitty100% (1)

- Mengyu LiDocument7 pagesMengyu LiSittyNo ratings yet

- Coa DBM - JC88 1Document3 pagesCoa DBM - JC88 1SittyNo ratings yet

- PPSAS 13 - Leases Oct - 18 2013Document3 pagesPPSAS 13 - Leases Oct - 18 2013SittyNo ratings yet

- Corliss v. Manila Railroad Co. Case DigestDocument2 pagesCorliss v. Manila Railroad Co. Case DigestSittyNo ratings yet

- Q1 M3 Worksheet CommunicativestylesDocument14 pagesQ1 M3 Worksheet CommunicativestylesBea CornelioNo ratings yet

- Case Digest - Go vs. Colegio de San Juan de LetranDocument3 pagesCase Digest - Go vs. Colegio de San Juan de Letranrobert gapasangra0% (1)

- Test Bank For American Government and Politics Today Essentials 2017 2018 Edition 19th by BardesDocument14 pagesTest Bank For American Government and Politics Today Essentials 2017 2018 Edition 19th by Bardescaradocbridget61rdNo ratings yet

- Omnibus AffidavitDocument2 pagesOmnibus AffidavitPatrick RodriguezNo ratings yet

- Gov94CM: International Law and International Organizations: Fall 2018, Tuesdays 3-5 P.M., CGIS Knafel K450Document10 pagesGov94CM: International Law and International Organizations: Fall 2018, Tuesdays 3-5 P.M., CGIS Knafel K450Alexandra Jima GonzálezNo ratings yet

- EDU175 Demonstration 8Document3 pagesEDU175 Demonstration 8Julita MirandaNo ratings yet

- Reply To Show Cause NoticeDocument4 pagesReply To Show Cause Noticecyberchang20002576No ratings yet

- Product Catalogue: Fixing SystemsDocument316 pagesProduct Catalogue: Fixing SystemsErvin KovacsNo ratings yet

- The Agent Agreement - Final VersionDocument4 pagesThe Agent Agreement - Final VersionDamilac DaguiwaNo ratings yet

- From (Anand Lakra (Bernard - Nliu@gmail - Com) ) - ID (551) - History - 2 - 2Document21 pagesFrom (Anand Lakra (Bernard - Nliu@gmail - Com) ) - ID (551) - History - 2 - 2siddharthNo ratings yet

- The Judicial System: Introduction To Legal SystemDocument16 pagesThe Judicial System: Introduction To Legal Systemanisah khrznNo ratings yet

- Iron Sand Contract of Agreement (Revised PT. CATUR MULTIGUNA ABADI)Document12 pagesIron Sand Contract of Agreement (Revised PT. CATUR MULTIGUNA ABADI)lbh.pancaranhati CirebonNo ratings yet

- Chart Pattern AdxDocument8 pagesChart Pattern Adx10578387No ratings yet

- Letter of Request For LRN DeactivationDocument21 pagesLetter of Request For LRN Deactivationgina procoratoNo ratings yet

- Quitclaim and Release FormDocument4 pagesQuitclaim and Release FormAlemie Blase TuaNo ratings yet

- The Governor - Constitutional Position and Political Reality - Arora and GoyalDocument15 pagesThe Governor - Constitutional Position and Political Reality - Arora and GoyalAnonymousNo ratings yet

- CCP 231 - Peremptory ChallengesDocument2 pagesCCP 231 - Peremptory ChallengesJim MayoNo ratings yet

- Chapter 2 - The Changing Legal EmphasisDocument28 pagesChapter 2 - The Changing Legal Emphasis时家欣No ratings yet

- FREEZING ORDERS - Adam CooteDocument8 pagesFREEZING ORDERS - Adam CooteJacob DahouNo ratings yet

- Tigers (Autosaved) 1Document162 pagesTigers (Autosaved) 1Manthan JindalNo ratings yet

- Maslinda BT Ishak V Mohd Tahir Bin Osman & OrsDocument7 pagesMaslinda BT Ishak V Mohd Tahir Bin Osman & OrscantikNo ratings yet

- Mathematics of Finance Canadian 8th Edition Brown Kopp Solution ManualDocument41 pagesMathematics of Finance Canadian 8th Edition Brown Kopp Solution Manualflorence100% (34)

- The Contract Labour (Regulation and Abolition) ACT, 1970Document17 pagesThe Contract Labour (Regulation and Abolition) ACT, 1970Sridhar KodaliNo ratings yet

- Gulu University: Name: Amola Arthur Isaac Course Unit: Land Transaction REG No: 18/U/1802/GBL/PS Lecturer: Mr. Paul LayooDocument9 pagesGulu University: Name: Amola Arthur Isaac Course Unit: Land Transaction REG No: 18/U/1802/GBL/PS Lecturer: Mr. Paul LayooArthur AmolaNo ratings yet

- Margdarshika 2015Document98 pagesMargdarshika 2015Sanjeev ChaudharyNo ratings yet

- The New Separation of Powers - A Theory For The Modern State (PDFDrive)Document302 pagesThe New Separation of Powers - A Theory For The Modern State (PDFDrive)cyrille leandres ngonNo ratings yet

- Writ Petition No.2212 of 2023 Dr. Shireen M. Mazari Versus Federation of PakistanDocument22 pagesWrit Petition No.2212 of 2023 Dr. Shireen M. Mazari Versus Federation of Pakistanastonishingeyes26No ratings yet

- Chillicothe Police Reports For October 16th 2013Document35 pagesChillicothe Police Reports For October 16th 2013Andrew AB BurgoonNo ratings yet

Download as pdf or txt

You might also like

- Rmo 43-90 PDFDocument5 pagesRmo 43-90 PDFRieland Cuevas67% (3)

- Aws A5.02Document30 pagesAws A5.02Meilati Pasca MunaNo ratings yet

- Mental Health LawsuitDocument2 pagesMental Health LawsuitGordon L. HinsonNo ratings yet

- Bureau of Internal RevenueDocument11 pagesBureau of Internal RevenueRomer LesondatoNo ratings yet

- Module 4 - Value Added TaxDocument16 pagesModule 4 - Value Added Taxanon_455551365No ratings yet

- Cfe Brochure 2015 PDFDocument12 pagesCfe Brochure 2015 PDFSittyNo ratings yet

- RMC No. 24-2022Document13 pagesRMC No. 24-2022arnulfojr hicoNo ratings yet

- (VAT) in To: Clarifying (RR) No. The The Tax of (TaxDocument13 pages(VAT) in To: Clarifying (RR) No. The The Tax of (TaxShiela Marie Maraon100% (1)

- Who To File RPTDocument9 pagesWho To File RPTLacie Hohenheim (Doraemon)No ratings yet

- COMMISSIONER OF INTERNAL REVENUE V Cebu Toyo CorpDocument5 pagesCOMMISSIONER OF INTERNAL REVENUE V Cebu Toyo CorpAustin Viel Lagman MedinaNo ratings yet

- Commissioner of Internal Revenue vs. Toshiba Information Equipment (Phils.), Inc., 466 SCRA 211, August 09, 2005Document4 pagesCommissioner of Internal Revenue vs. Toshiba Information Equipment (Phils.), Inc., 466 SCRA 211, August 09, 2005idolbondocNo ratings yet

- Rulings2000 DigestDocument21 pagesRulings2000 DigestArriane MartinezNo ratings yet

- 2 Value Added TaxDocument216 pages2 Value Added TaxnichNo ratings yet

- Value-Added Tax Nature of VatDocument22 pagesValue-Added Tax Nature of VatDiossaNo ratings yet

- CIR vs. ToshibaDocument3 pagesCIR vs. ToshibaKayelyn Lat100% (1)

- Petitioner Respondent Litigation Division (BIR) Avisado Agan Montenegro & AssociatesDocument17 pagesPetitioner Respondent Litigation Division (BIR) Avisado Agan Montenegro & AssociatesRobert Jayson UyNo ratings yet

- Atlas Consolidated Mining V CIR (Case Digest)Document2 pagesAtlas Consolidated Mining V CIR (Case Digest)Jeng Pion100% (2)

- Module 3 Tax Preferences Available For Sole Proprietorship BusinessDocument7 pagesModule 3 Tax Preferences Available For Sole Proprietorship Businessangclaire47No ratings yet

- Value Added Tax Ust PDFDocument23 pagesValue Added Tax Ust PDFcalliemozartNo ratings yet

- Coral Bay Tax DigestDocument3 pagesCoral Bay Tax DigestJonathan Dela Cruz100% (1)

- RR No. 3-2023Document6 pagesRR No. 3-2023Anostasia NemusNo ratings yet

- CIR vs. CA - G.R. No. 125355 (Digest)Document7 pagesCIR vs. CA - G.R. No. 125355 (Digest)Karen Gina DupraNo ratings yet

- RR No. 34-2020 v2Document3 pagesRR No. 34-2020 v2JejomarNo ratings yet

- CIR v. Toshiba Information Equipment (Phils.) IncDocument2 pagesCIR v. Toshiba Information Equipment (Phils.) IncEJ PajaroNo ratings yet

- Powerpoint-03 19 22Document126 pagesPowerpoint-03 19 22CrizziaNo ratings yet

- RMC No. 50-2007 PDFDocument6 pagesRMC No. 50-2007 PDFAnonymous yKUdPvwjNo ratings yet

- Vat - 1Document20 pagesVat - 1biburaNo ratings yet

- Fort Bonifacio v. CIRDocument3 pagesFort Bonifacio v. CIRAngelique Padilla UgayNo ratings yet

- Cir Vs ToshibaDocument23 pagesCir Vs ToshibamarkNo ratings yet

- 112034-2005-Commissioner of Internal Revenue v. Toshiba20180404-1159-12ci6skDocument15 pages112034-2005-Commissioner of Internal Revenue v. Toshiba20180404-1159-12ci6skCamshtNo ratings yet

- Value Added TaxDocument20 pagesValue Added TaxJerlene Sydney Centeno100% (1)

- Revenue Memorandum Circular No. 62-05: SubjectDocument12 pagesRevenue Memorandum Circular No. 62-05: Subject김비앙카No ratings yet

- Excel Professional Services, Inc.: Management Firm of Professional Review and Training Center (PRTC)Document3 pagesExcel Professional Services, Inc.: Management Firm of Professional Review and Training Center (PRTC)Mae Angiela TansecoNo ratings yet

- BMBE SeminarDocument60 pagesBMBE SeminarBabyGiant LucasNo ratings yet

- Tranzen1A Income TaxDocument46 pagesTranzen1A Income TaxMonica SorianoNo ratings yet

- RegistrationDocument127 pagesRegistrationDa Yani ChristeeneNo ratings yet

- RMC No. 50-2007Document6 pagesRMC No. 50-2007scribe03No ratings yet

- RR No. 07-12Document53 pagesRR No. 07-12Nash Ortiz LuisNo ratings yet

- RMC No. 8-2024Document5 pagesRMC No. 8-2024Anostasia NemusNo ratings yet

- RR 3-2023 Digest FINALDocument4 pagesRR 3-2023 Digest FINALAkld D LerioNo ratings yet

- Tax 1 Case DigestsDocument50 pagesTax 1 Case Digestso6739No ratings yet

- Free Commercial ZoneDocument12 pagesFree Commercial ZoneQueenie ChongNo ratings yet

- Articles About VAT Zero-RatingDocument8 pagesArticles About VAT Zero-RatingkmoNo ratings yet

- Relevant BIR UpdatesDocument49 pagesRelevant BIR UpdatesElsha dela penaNo ratings yet

- Tax Alert - 2005 - FebDocument11 pagesTax Alert - 2005 - FebzhanleriNo ratings yet

- Rs 22,510 Rs 743 367 Rs.36,748: TotalDocument2 pagesRs 22,510 Rs 743 367 Rs.36,748: Totalasad khokharNo ratings yet

- 43677RMO 3-2009 - Suspension GroundsDocument29 pages43677RMO 3-2009 - Suspension GroundsAnonymous OyhbxcjNo ratings yet

- Rmo 3-2009Document29 pagesRmo 3-2009sheena100% (2)

- VAT ZERO-RATED SALES - CIR V ToshibaDocument6 pagesVAT ZERO-RATED SALES - CIR V ToshibaChristine Gel MadrilejoNo ratings yet

- VAT of BangladeshDocument111 pagesVAT of BangladeshNahian HasanNo ratings yet

- Tax Brief - June 2012Document8 pagesTax Brief - June 2012Rheneir MoraNo ratings yet

- Chapter 7 MCQ'S AssignmentDocument3 pagesChapter 7 MCQ'S AssignmentMary Joy CabilNo ratings yet

- Chapter 15 - Tax IncentivesDocument26 pagesChapter 15 - Tax IncentivesForjosh VNo ratings yet

- 142 150Document7 pages142 150NikkandraNo ratings yet

- New VAT Audit FormatDocument12 pagesNew VAT Audit FormatparulshinyNo ratings yet

- Tax UpdatesDocument19 pagesTax UpdatesYeoh MaeNo ratings yet

- Commentary On Withholding RulesDocument6 pagesCommentary On Withholding RulesTanzeel Ur Rahman GazdarNo ratings yet

- Tax Vat Cases DigestDocument34 pagesTax Vat Cases DigestNievesAlarconNo ratings yet

- BIR RMC No. 62-2005Document15 pagesBIR RMC No. 62-2005dencave1No ratings yet

- 1999 BIR RulingsDocument74 pages1999 BIR Rulingschris cardinoNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- Revenue Memorandum Order No. 19-2006 Subject:: Bureau of Internal RevenueDocument2 pagesRevenue Memorandum Order No. 19-2006 Subject:: Bureau of Internal RevenueSittyNo ratings yet

- RMC No. 36-2022Document2 pagesRMC No. 36-2022SittyNo ratings yet

- Vat Zero-Rate Certification Certificate No. (YYYY - )Document2 pagesVat Zero-Rate Certification Certificate No. (YYYY - )SittyNo ratings yet

- Coa Logo For PrintingDocument2 pagesCoa Logo For PrintingSittyNo ratings yet

- Caltex Vs CoaDocument25 pagesCaltex Vs CoaSittyNo ratings yet

- (Prescribed Form) : (Place A Copy of The Mark in The Box. The Mark Should Be Clear Enough To Be Reproduced and Digitized)Document1 page(Prescribed Form) : (Place A Copy of The Mark in The Box. The Mark Should Be Clear Enough To Be Reproduced and Digitized)SittyNo ratings yet

- Wallace v. Eclipse Pocahontas Coal Co Case DigestDocument1 pageWallace v. Eclipse Pocahontas Coal Co Case DigestSitty100% (1)

- Mengyu LiDocument7 pagesMengyu LiSittyNo ratings yet

- Coa DBM - JC88 1Document3 pagesCoa DBM - JC88 1SittyNo ratings yet

- PPSAS 13 - Leases Oct - 18 2013Document3 pagesPPSAS 13 - Leases Oct - 18 2013SittyNo ratings yet

- Corliss v. Manila Railroad Co. Case DigestDocument2 pagesCorliss v. Manila Railroad Co. Case DigestSittyNo ratings yet

- Q1 M3 Worksheet CommunicativestylesDocument14 pagesQ1 M3 Worksheet CommunicativestylesBea CornelioNo ratings yet

- Case Digest - Go vs. Colegio de San Juan de LetranDocument3 pagesCase Digest - Go vs. Colegio de San Juan de Letranrobert gapasangra0% (1)

- Test Bank For American Government and Politics Today Essentials 2017 2018 Edition 19th by BardesDocument14 pagesTest Bank For American Government and Politics Today Essentials 2017 2018 Edition 19th by Bardescaradocbridget61rdNo ratings yet

- Omnibus AffidavitDocument2 pagesOmnibus AffidavitPatrick RodriguezNo ratings yet

- Gov94CM: International Law and International Organizations: Fall 2018, Tuesdays 3-5 P.M., CGIS Knafel K450Document10 pagesGov94CM: International Law and International Organizations: Fall 2018, Tuesdays 3-5 P.M., CGIS Knafel K450Alexandra Jima GonzálezNo ratings yet

- EDU175 Demonstration 8Document3 pagesEDU175 Demonstration 8Julita MirandaNo ratings yet

- Reply To Show Cause NoticeDocument4 pagesReply To Show Cause Noticecyberchang20002576No ratings yet

- Product Catalogue: Fixing SystemsDocument316 pagesProduct Catalogue: Fixing SystemsErvin KovacsNo ratings yet

- The Agent Agreement - Final VersionDocument4 pagesThe Agent Agreement - Final VersionDamilac DaguiwaNo ratings yet

- From (Anand Lakra (Bernard - Nliu@gmail - Com) ) - ID (551) - History - 2 - 2Document21 pagesFrom (Anand Lakra (Bernard - Nliu@gmail - Com) ) - ID (551) - History - 2 - 2siddharthNo ratings yet

- The Judicial System: Introduction To Legal SystemDocument16 pagesThe Judicial System: Introduction To Legal Systemanisah khrznNo ratings yet

- Iron Sand Contract of Agreement (Revised PT. CATUR MULTIGUNA ABADI)Document12 pagesIron Sand Contract of Agreement (Revised PT. CATUR MULTIGUNA ABADI)lbh.pancaranhati CirebonNo ratings yet

- Chart Pattern AdxDocument8 pagesChart Pattern Adx10578387No ratings yet

- Letter of Request For LRN DeactivationDocument21 pagesLetter of Request For LRN Deactivationgina procoratoNo ratings yet

- Quitclaim and Release FormDocument4 pagesQuitclaim and Release FormAlemie Blase TuaNo ratings yet

- The Governor - Constitutional Position and Political Reality - Arora and GoyalDocument15 pagesThe Governor - Constitutional Position and Political Reality - Arora and GoyalAnonymousNo ratings yet

- CCP 231 - Peremptory ChallengesDocument2 pagesCCP 231 - Peremptory ChallengesJim MayoNo ratings yet

- Chapter 2 - The Changing Legal EmphasisDocument28 pagesChapter 2 - The Changing Legal Emphasis时家欣No ratings yet

- FREEZING ORDERS - Adam CooteDocument8 pagesFREEZING ORDERS - Adam CooteJacob DahouNo ratings yet

- Tigers (Autosaved) 1Document162 pagesTigers (Autosaved) 1Manthan JindalNo ratings yet

- Maslinda BT Ishak V Mohd Tahir Bin Osman & OrsDocument7 pagesMaslinda BT Ishak V Mohd Tahir Bin Osman & OrscantikNo ratings yet

- Mathematics of Finance Canadian 8th Edition Brown Kopp Solution ManualDocument41 pagesMathematics of Finance Canadian 8th Edition Brown Kopp Solution Manualflorence100% (34)

- The Contract Labour (Regulation and Abolition) ACT, 1970Document17 pagesThe Contract Labour (Regulation and Abolition) ACT, 1970Sridhar KodaliNo ratings yet

- Gulu University: Name: Amola Arthur Isaac Course Unit: Land Transaction REG No: 18/U/1802/GBL/PS Lecturer: Mr. Paul LayooDocument9 pagesGulu University: Name: Amola Arthur Isaac Course Unit: Land Transaction REG No: 18/U/1802/GBL/PS Lecturer: Mr. Paul LayooArthur AmolaNo ratings yet

- Margdarshika 2015Document98 pagesMargdarshika 2015Sanjeev ChaudharyNo ratings yet

- The New Separation of Powers - A Theory For The Modern State (PDFDrive)Document302 pagesThe New Separation of Powers - A Theory For The Modern State (PDFDrive)cyrille leandres ngonNo ratings yet

- Writ Petition No.2212 of 2023 Dr. Shireen M. Mazari Versus Federation of PakistanDocument22 pagesWrit Petition No.2212 of 2023 Dr. Shireen M. Mazari Versus Federation of Pakistanastonishingeyes26No ratings yet

- Chillicothe Police Reports For October 16th 2013Document35 pagesChillicothe Police Reports For October 16th 2013Andrew AB BurgoonNo ratings yet