Fiscal Regimes For EI: Issues and Challenges in Indonesia: Ministry of Finance of Republic of Indonesia

Fiscal Regimes For EI: Issues and Challenges in Indonesia: Ministry of Finance of Republic of Indonesia

You might also like

- Etextbook 978 1305506381 Managerial Economics Applications Strategies and TacticsDocument62 pagesEtextbook 978 1305506381 Managerial Economics Applications Strategies and Tacticsjesse.yardley161100% (55)

- Mobil Nigeria Financial Statement AnalysisDocument15 pagesMobil Nigeria Financial Statement AnalysismayorchukaNo ratings yet

- Overview of The Nigerian Oil and Gas IndustryDocument39 pagesOverview of The Nigerian Oil and Gas Industryneocentricgenius100% (4)

- Coal India 25-07-2020Document11 pagesCoal India 25-07-2020Manoj DoshiNo ratings yet

- Ch26 Incremental Cost and Budgetary ControlDocument70 pagesCh26 Incremental Cost and Budgetary ControlResha Monica PutriNo ratings yet

- Q No. 1 Assume That You Are Given Assignment To Evaluate The Capital Budgeting Projects of The CompanyDocument3 pagesQ No. 1 Assume That You Are Given Assignment To Evaluate The Capital Budgeting Projects of The CompanyMuneeb Qureshi0% (1)

- 101 Powerful Money Secrets-What The Rich.... & Life - Alex OoiDocument35 pages101 Powerful Money Secrets-What The Rich.... & Life - Alex OoiwobblegobbleNo ratings yet

- Saudi Arabias Energy Pricing Reform in A Changing Domestic and Global ContectDocument25 pagesSaudi Arabias Energy Pricing Reform in A Changing Domestic and Global Contectمحمد التهامىNo ratings yet

- Nigeria's Government Considers Petroleum Industry Bill 2020, A New Framework For The Oil and Gas SectorDocument6 pagesNigeria's Government Considers Petroleum Industry Bill 2020, A New Framework For The Oil and Gas Sectorpradeep s gillNo ratings yet

- Merak Fiscal Model Library: Italy R/T (2000)Document2 pagesMerak Fiscal Model Library: Italy R/T (2000)Tripoli ManoNo ratings yet

- The Fiscal Regime in Albania For Upstrea PDFDocument12 pagesThe Fiscal Regime in Albania For Upstrea PDFRuxandra TudorașcuNo ratings yet

- Oil and Gas IndustryDocument50 pagesOil and Gas IndustryAnand aashishNo ratings yet

- Merak Fiscal Model Library: Brunei PSC (2001)Document2 pagesMerak Fiscal Model Library: Brunei PSC (2001)Libya TripoliNo ratings yet

- Nigerian Oil and Gas Industry BriefDocument22 pagesNigerian Oil and Gas Industry BriefOlimene Babatunde100% (2)

- CHWS3DOC20 BunboonDocument19 pagesCHWS3DOC20 BunboonthuanNo ratings yet

- NNPC - Monitoring Oil Production and Revenue GenerationDocument104 pagesNNPC - Monitoring Oil Production and Revenue Generationtsar_philip2010No ratings yet

- Shivalik Institute of Management Education & ResearchDocument17 pagesShivalik Institute of Management Education & ResearchNeha SoniNo ratings yet

- Worldwide Petroleum Fiscal Regimes Development: Observations and TrendsDocument63 pagesWorldwide Petroleum Fiscal Regimes Development: Observations and TrendsBenny Lubiantara100% (7)

- NigeriaCAXS 2020Document10 pagesNigeriaCAXS 2020MalziNo ratings yet

- SPE-193470-MS Analysis of Government and Contractor Take Statistics in The Proposed Petroleum Industry Fiscal BillDocument14 pagesSPE-193470-MS Analysis of Government and Contractor Take Statistics in The Proposed Petroleum Industry Fiscal Billipali4christ_5308248No ratings yet

- Policy Brief The Petroleum Industry in Zambia Challenges and OpportunitiesDocument5 pagesPolicy Brief The Petroleum Industry in Zambia Challenges and OpportunitiesCaleb ChongoNo ratings yet

- Union Budget FY11 - Balancing The Fisc, Enhancing Growth (First Cut)Document18 pagesUnion Budget FY11 - Balancing The Fisc, Enhancing Growth (First Cut)Vijay JhalaNo ratings yet

- Merak Fiscal Model Library: Bangladesh PSC (1993)Document2 pagesMerak Fiscal Model Library: Bangladesh PSC (1993)Tripoli ManoNo ratings yet

- Roadmap To The Goods and Services Tax: Executive Director Pricewaterhousecoopers, IndiaDocument15 pagesRoadmap To The Goods and Services Tax: Executive Director Pricewaterhousecoopers, IndiaPramod DumreNo ratings yet

- Contemporary Tax Issues PresentationDocument38 pagesContemporary Tax Issues PresentationSamuel DwumfourNo ratings yet

- Royalty Review 0815 BMO (00000002)Document25 pagesRoyalty Review 0815 BMO (00000002)TeamWildroseNo ratings yet

- KiritParekhCommitteeReport AngelDocument5 pagesKiritParekhCommitteeReport AngelshshashankNo ratings yet

- Tax Project FinalDocument9 pagesTax Project Finalmeripo_rima5857No ratings yet

- Budget 2011-12 Review: Ranjan Das Karthikeyan Barath PriyankaDocument18 pagesBudget 2011-12 Review: Ranjan Das Karthikeyan Barath Priyankakarthikeyan un reclusNo ratings yet

- Merak Fiscal Model Library: Kurdistan PSC (2006)Document2 pagesMerak Fiscal Model Library: Kurdistan PSC (2006)Libya TripoliNo ratings yet

- DanielDocument31 pagesDanielJoseph EshunNo ratings yet

- Merak Fiscal Model Library: Madagascar PSC (2006)Document2 pagesMerak Fiscal Model Library: Madagascar PSC (2006)Tripoli ManoNo ratings yet

- Lesson 6 Tax On Natural ResourcesDocument47 pagesLesson 6 Tax On Natural ResourcesakpanyapNo ratings yet

- A Guide To The Taxation of Oil Companies in Nigeria (Consolidated)Document68 pagesA Guide To The Taxation of Oil Companies in Nigeria (Consolidated)Oluwamuyiwa Adebayo Adeyemo100% (2)

- Merak Fiscal Model Library: Peru License Prod (2003)Document2 pagesMerak Fiscal Model Library: Peru License Prod (2003)Libya TripoliNo ratings yet

- SPE-203740-MS Implications of Petroleum Industry Fiscal Bill 2018 On Heavy Oil Field EconomicsDocument19 pagesSPE-203740-MS Implications of Petroleum Industry Fiscal Bill 2018 On Heavy Oil Field Economicsipali4christ_5308248No ratings yet

- Class Lecture 43Document70 pagesClass Lecture 43Tanay BansalNo ratings yet

- A Closr Look at PIBDocument17 pagesA Closr Look at PIBOluwasheyifunmi AdefullhouseNo ratings yet

- Provision of Train Law UpdatedDocument91 pagesProvision of Train Law UpdatedAldrich De VeraNo ratings yet

- SeminarDocument13 pagesSeminarManoj YadavNo ratings yet

- Oil and Natural Gas SectorDocument16 pagesOil and Natural Gas Sectorsmritim_3No ratings yet

- The Dynamics of Crude PricingDocument45 pagesThe Dynamics of Crude Pricingparmeshwar mahatoNo ratings yet

- TNF Zimbabwe Nov30 2022Document22 pagesTNF Zimbabwe Nov30 2022LOICE MANENEKANo ratings yet

- Weekly Review Is Designed To Provide You With AnDocument2 pagesWeekly Review Is Designed To Provide You With Anapi-25947462No ratings yet

- Analysis of Financial Stetement PSODocument14 pagesAnalysis of Financial Stetement PSODanish KhalidNo ratings yet

- Merak Fiscal Model Library: Brunei R/T (2000)Document2 pagesMerak Fiscal Model Library: Brunei R/T (2000)Libya TripoliNo ratings yet

- Gail Investor PresentationDocument31 pagesGail Investor Presentationsurya167No ratings yet

- Budget 2011-12 Preview: Tightrope WalkingDocument24 pagesBudget 2011-12 Preview: Tightrope WalkingSahil GargNo ratings yet

- Saudi Arabia Budget 2010Document5 pagesSaudi Arabia Budget 2010HamzaNo ratings yet

- Tackling The Gasoline, Middle DistillateDocument8 pagesTackling The Gasoline, Middle DistillateMón Quà Vô GiáNo ratings yet

- Indian Petroleum Industry: Group 8Document20 pagesIndian Petroleum Industry: Group 8Arun Singh SikarwarNo ratings yet

- Analyzing The Budget 2012-13Document13 pagesAnalyzing The Budget 2012-13nikhilp60No ratings yet

- Reducing Greenhouse Gas Emmission - : Abiodun IbikunleDocument38 pagesReducing Greenhouse Gas Emmission - : Abiodun IbikunleKateryne RochaNo ratings yet

- Phasing Out Fuel Subsidies in NigeriaDocument3 pagesPhasing Out Fuel Subsidies in NigeriaEfosaUwaifoNo ratings yet

- NTPC - Cement Manufacturers AssociationDocument53 pagesNTPC - Cement Manufacturers Associationlaloo01No ratings yet

- Petro Policy Impact Analysis7jun08Document15 pagesPetro Policy Impact Analysis7jun08rajivaNo ratings yet

- KPMG 2024 Zimbabwe National Budget HighlightsDocument11 pagesKPMG 2024 Zimbabwe National Budget Highlightslindachipwanya4No ratings yet

- Budget 2012Document23 pagesBudget 2012Disha ChauhanNo ratings yet

- Oil and Gas After COVID 19 v4Document11 pagesOil and Gas After COVID 19 v4Cedie Rogel De Torres100% (1)

- Merak Fiscal Model Library: South Africa R/T (1997)Document2 pagesMerak Fiscal Model Library: South Africa R/T (1997)Tripoli ManoNo ratings yet

- Day1 - 06 - Ramona Volciuc-Ionescu - Volvic-Ionescu SCADocument21 pagesDay1 - 06 - Ramona Volciuc-Ionescu - Volvic-Ionescu SCAaegean227No ratings yet

- Ndia S Rade Olicy: Foreign Trade Balance of Payments Trade Policies Foreign Trade Policy (FTP)Document27 pagesNdia S Rade Olicy: Foreign Trade Balance of Payments Trade Policies Foreign Trade Policy (FTP)Gargi SinhaNo ratings yet

- Oil and Gas Taxation Under The Petroleum Industry ActDocument3 pagesOil and Gas Taxation Under The Petroleum Industry Actahassan2No ratings yet

- Panel4 AdrianMunandar ITC2020Document18 pagesPanel4 AdrianMunandar ITC2020diana_busrizaltiNo ratings yet

- eJTR Vol11-No3 2013Document212 pageseJTR Vol11-No3 2013diana_busrizaltiNo ratings yet

- Expert Opininon On Mine TaxationDocument57 pagesExpert Opininon On Mine Taxationdiana_busrizaltiNo ratings yet

- Ai - PPT 6 (Business Processes and Risks)Document22 pagesAi - PPT 6 (Business Processes and Risks)diana_busrizaltiNo ratings yet

- Ai - PPT 7 (Internal Control)Document30 pagesAi - PPT 7 (Internal Control)diana_busrizalti100% (1)

- VEF CalculationDocument6 pagesVEF CalculationProtyay ChakrabortyNo ratings yet

- MIcro Tutorial 5 ANSDocument5 pagesMIcro Tutorial 5 ANSBintang David SusantoNo ratings yet

- Original For Recipient: Order Number: RDF15750659Document2 pagesOriginal For Recipient: Order Number: RDF15750659Rajat DawraNo ratings yet

- Red OceanDocument17 pagesRed OceanSaipriya Raghavan0% (1)

- Appendix A Pricing Products and ServicesDocument23 pagesAppendix A Pricing Products and ServicesJaved AhmedNo ratings yet

- Chase Credit Card ApplicationDocument4 pagesChase Credit Card ApplicationJames McguireNo ratings yet

- Peachtree A Complete AnswersDocument5 pagesPeachtree A Complete AnswersPhilip JosephNo ratings yet

- Income Taxation AssignmentDocument1 pageIncome Taxation AssignmentHannah MeranoNo ratings yet

- (Financial Accounting & Reporting 2) : Lecture AidDocument18 pages(Financial Accounting & Reporting 2) : Lecture AidMay Grethel Joy PeranteNo ratings yet

- Marketing PlanDocument15 pagesMarketing Planvarooval_80No ratings yet

- Ethiopia - Starbucks PDFDocument15 pagesEthiopia - Starbucks PDFPriscilla SharonNo ratings yet

- Chola E-Auction Sale Notice Vishal Pandit Mahale 11.10.2023 Dhule Physical 15 DaysDocument5 pagesChola E-Auction Sale Notice Vishal Pandit Mahale 11.10.2023 Dhule Physical 15 DaysAman SainiNo ratings yet

- Ch10 DepreciationDocument18 pagesCh10 DepreciationRama KrishnaNo ratings yet

- Solution - 08.38 PDFDocument2 pagesSolution - 08.38 PDFsanNo ratings yet

- Session 04-WTC PPT (Jan 28, 2019)Document32 pagesSession 04-WTC PPT (Jan 28, 2019)MtashuNo ratings yet

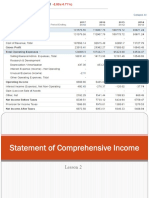

- Lesson 2 Statement of Comprehensive IncomeDocument23 pagesLesson 2 Statement of Comprehensive IncomePaulette Sarno80% (5)

- Grom PresentationDocument10 pagesGrom PresentationMathan Anto MarshineNo ratings yet

- Chapter 8Document17 pagesChapter 8Jamaica DavidNo ratings yet

- ContractsDocument12 pagesContractsriyqNo ratings yet

- Chapter 11 Pricing Strategies: Additional Considerations: Principles of Marketing, 17e (Kotler/Armstrong)Document21 pagesChapter 11 Pricing Strategies: Additional Considerations: Principles of Marketing, 17e (Kotler/Armstrong)RosyLeeNo ratings yet

- Group Assignment On Variable PricingDocument1 pageGroup Assignment On Variable PricingKowshik MoyyaNo ratings yet

- PR 10037 Canvass SheetDocument4 pagesPR 10037 Canvass SheetjaymarNo ratings yet

- Primary MarketDocument18 pagesPrimary MarketRaman RandhawaNo ratings yet

- GST Reforms-TB ChatterjeeDocument14 pagesGST Reforms-TB ChatterjeeJogender ChauhanNo ratings yet

- Sri Lanka Textile and Apparel IndustryDocument13 pagesSri Lanka Textile and Apparel IndustryAnushka IttapanaNo ratings yet

- Hedging Strategies Using FuturesDocument23 pagesHedging Strategies Using FuturesBiswajit SarmaNo ratings yet

Download as pdf or txt

You might also like

- Etextbook 978 1305506381 Managerial Economics Applications Strategies and TacticsDocument62 pagesEtextbook 978 1305506381 Managerial Economics Applications Strategies and Tacticsjesse.yardley161100% (55)

- Mobil Nigeria Financial Statement AnalysisDocument15 pagesMobil Nigeria Financial Statement AnalysismayorchukaNo ratings yet

- Overview of The Nigerian Oil and Gas IndustryDocument39 pagesOverview of The Nigerian Oil and Gas Industryneocentricgenius100% (4)

- Coal India 25-07-2020Document11 pagesCoal India 25-07-2020Manoj DoshiNo ratings yet

- Ch26 Incremental Cost and Budgetary ControlDocument70 pagesCh26 Incremental Cost and Budgetary ControlResha Monica PutriNo ratings yet

- Q No. 1 Assume That You Are Given Assignment To Evaluate The Capital Budgeting Projects of The CompanyDocument3 pagesQ No. 1 Assume That You Are Given Assignment To Evaluate The Capital Budgeting Projects of The CompanyMuneeb Qureshi0% (1)

- 101 Powerful Money Secrets-What The Rich.... & Life - Alex OoiDocument35 pages101 Powerful Money Secrets-What The Rich.... & Life - Alex OoiwobblegobbleNo ratings yet

- Saudi Arabias Energy Pricing Reform in A Changing Domestic and Global ContectDocument25 pagesSaudi Arabias Energy Pricing Reform in A Changing Domestic and Global Contectمحمد التهامىNo ratings yet

- Nigeria's Government Considers Petroleum Industry Bill 2020, A New Framework For The Oil and Gas SectorDocument6 pagesNigeria's Government Considers Petroleum Industry Bill 2020, A New Framework For The Oil and Gas Sectorpradeep s gillNo ratings yet

- Merak Fiscal Model Library: Italy R/T (2000)Document2 pagesMerak Fiscal Model Library: Italy R/T (2000)Tripoli ManoNo ratings yet

- The Fiscal Regime in Albania For Upstrea PDFDocument12 pagesThe Fiscal Regime in Albania For Upstrea PDFRuxandra TudorașcuNo ratings yet

- Oil and Gas IndustryDocument50 pagesOil and Gas IndustryAnand aashishNo ratings yet

- Merak Fiscal Model Library: Brunei PSC (2001)Document2 pagesMerak Fiscal Model Library: Brunei PSC (2001)Libya TripoliNo ratings yet

- Nigerian Oil and Gas Industry BriefDocument22 pagesNigerian Oil and Gas Industry BriefOlimene Babatunde100% (2)

- CHWS3DOC20 BunboonDocument19 pagesCHWS3DOC20 BunboonthuanNo ratings yet

- NNPC - Monitoring Oil Production and Revenue GenerationDocument104 pagesNNPC - Monitoring Oil Production and Revenue Generationtsar_philip2010No ratings yet

- Shivalik Institute of Management Education & ResearchDocument17 pagesShivalik Institute of Management Education & ResearchNeha SoniNo ratings yet

- Worldwide Petroleum Fiscal Regimes Development: Observations and TrendsDocument63 pagesWorldwide Petroleum Fiscal Regimes Development: Observations and TrendsBenny Lubiantara100% (7)

- NigeriaCAXS 2020Document10 pagesNigeriaCAXS 2020MalziNo ratings yet

- SPE-193470-MS Analysis of Government and Contractor Take Statistics in The Proposed Petroleum Industry Fiscal BillDocument14 pagesSPE-193470-MS Analysis of Government and Contractor Take Statistics in The Proposed Petroleum Industry Fiscal Billipali4christ_5308248No ratings yet

- Policy Brief The Petroleum Industry in Zambia Challenges and OpportunitiesDocument5 pagesPolicy Brief The Petroleum Industry in Zambia Challenges and OpportunitiesCaleb ChongoNo ratings yet

- Union Budget FY11 - Balancing The Fisc, Enhancing Growth (First Cut)Document18 pagesUnion Budget FY11 - Balancing The Fisc, Enhancing Growth (First Cut)Vijay JhalaNo ratings yet

- Merak Fiscal Model Library: Bangladesh PSC (1993)Document2 pagesMerak Fiscal Model Library: Bangladesh PSC (1993)Tripoli ManoNo ratings yet

- Roadmap To The Goods and Services Tax: Executive Director Pricewaterhousecoopers, IndiaDocument15 pagesRoadmap To The Goods and Services Tax: Executive Director Pricewaterhousecoopers, IndiaPramod DumreNo ratings yet

- Contemporary Tax Issues PresentationDocument38 pagesContemporary Tax Issues PresentationSamuel DwumfourNo ratings yet

- Royalty Review 0815 BMO (00000002)Document25 pagesRoyalty Review 0815 BMO (00000002)TeamWildroseNo ratings yet

- KiritParekhCommitteeReport AngelDocument5 pagesKiritParekhCommitteeReport AngelshshashankNo ratings yet

- Tax Project FinalDocument9 pagesTax Project Finalmeripo_rima5857No ratings yet

- Budget 2011-12 Review: Ranjan Das Karthikeyan Barath PriyankaDocument18 pagesBudget 2011-12 Review: Ranjan Das Karthikeyan Barath Priyankakarthikeyan un reclusNo ratings yet

- Merak Fiscal Model Library: Kurdistan PSC (2006)Document2 pagesMerak Fiscal Model Library: Kurdistan PSC (2006)Libya TripoliNo ratings yet

- DanielDocument31 pagesDanielJoseph EshunNo ratings yet

- Merak Fiscal Model Library: Madagascar PSC (2006)Document2 pagesMerak Fiscal Model Library: Madagascar PSC (2006)Tripoli ManoNo ratings yet

- Lesson 6 Tax On Natural ResourcesDocument47 pagesLesson 6 Tax On Natural ResourcesakpanyapNo ratings yet

- A Guide To The Taxation of Oil Companies in Nigeria (Consolidated)Document68 pagesA Guide To The Taxation of Oil Companies in Nigeria (Consolidated)Oluwamuyiwa Adebayo Adeyemo100% (2)

- Merak Fiscal Model Library: Peru License Prod (2003)Document2 pagesMerak Fiscal Model Library: Peru License Prod (2003)Libya TripoliNo ratings yet

- SPE-203740-MS Implications of Petroleum Industry Fiscal Bill 2018 On Heavy Oil Field EconomicsDocument19 pagesSPE-203740-MS Implications of Petroleum Industry Fiscal Bill 2018 On Heavy Oil Field Economicsipali4christ_5308248No ratings yet

- Class Lecture 43Document70 pagesClass Lecture 43Tanay BansalNo ratings yet

- A Closr Look at PIBDocument17 pagesA Closr Look at PIBOluwasheyifunmi AdefullhouseNo ratings yet

- Provision of Train Law UpdatedDocument91 pagesProvision of Train Law UpdatedAldrich De VeraNo ratings yet

- SeminarDocument13 pagesSeminarManoj YadavNo ratings yet

- Oil and Natural Gas SectorDocument16 pagesOil and Natural Gas Sectorsmritim_3No ratings yet

- The Dynamics of Crude PricingDocument45 pagesThe Dynamics of Crude Pricingparmeshwar mahatoNo ratings yet

- TNF Zimbabwe Nov30 2022Document22 pagesTNF Zimbabwe Nov30 2022LOICE MANENEKANo ratings yet

- Weekly Review Is Designed To Provide You With AnDocument2 pagesWeekly Review Is Designed To Provide You With Anapi-25947462No ratings yet

- Analysis of Financial Stetement PSODocument14 pagesAnalysis of Financial Stetement PSODanish KhalidNo ratings yet

- Merak Fiscal Model Library: Brunei R/T (2000)Document2 pagesMerak Fiscal Model Library: Brunei R/T (2000)Libya TripoliNo ratings yet

- Gail Investor PresentationDocument31 pagesGail Investor Presentationsurya167No ratings yet

- Budget 2011-12 Preview: Tightrope WalkingDocument24 pagesBudget 2011-12 Preview: Tightrope WalkingSahil GargNo ratings yet

- Saudi Arabia Budget 2010Document5 pagesSaudi Arabia Budget 2010HamzaNo ratings yet

- Tackling The Gasoline, Middle DistillateDocument8 pagesTackling The Gasoline, Middle DistillateMón Quà Vô GiáNo ratings yet

- Indian Petroleum Industry: Group 8Document20 pagesIndian Petroleum Industry: Group 8Arun Singh SikarwarNo ratings yet

- Analyzing The Budget 2012-13Document13 pagesAnalyzing The Budget 2012-13nikhilp60No ratings yet

- Reducing Greenhouse Gas Emmission - : Abiodun IbikunleDocument38 pagesReducing Greenhouse Gas Emmission - : Abiodun IbikunleKateryne RochaNo ratings yet

- Phasing Out Fuel Subsidies in NigeriaDocument3 pagesPhasing Out Fuel Subsidies in NigeriaEfosaUwaifoNo ratings yet

- NTPC - Cement Manufacturers AssociationDocument53 pagesNTPC - Cement Manufacturers Associationlaloo01No ratings yet

- Petro Policy Impact Analysis7jun08Document15 pagesPetro Policy Impact Analysis7jun08rajivaNo ratings yet

- KPMG 2024 Zimbabwe National Budget HighlightsDocument11 pagesKPMG 2024 Zimbabwe National Budget Highlightslindachipwanya4No ratings yet

- Budget 2012Document23 pagesBudget 2012Disha ChauhanNo ratings yet

- Oil and Gas After COVID 19 v4Document11 pagesOil and Gas After COVID 19 v4Cedie Rogel De Torres100% (1)

- Merak Fiscal Model Library: South Africa R/T (1997)Document2 pagesMerak Fiscal Model Library: South Africa R/T (1997)Tripoli ManoNo ratings yet

- Day1 - 06 - Ramona Volciuc-Ionescu - Volvic-Ionescu SCADocument21 pagesDay1 - 06 - Ramona Volciuc-Ionescu - Volvic-Ionescu SCAaegean227No ratings yet

- Ndia S Rade Olicy: Foreign Trade Balance of Payments Trade Policies Foreign Trade Policy (FTP)Document27 pagesNdia S Rade Olicy: Foreign Trade Balance of Payments Trade Policies Foreign Trade Policy (FTP)Gargi SinhaNo ratings yet

- Oil and Gas Taxation Under The Petroleum Industry ActDocument3 pagesOil and Gas Taxation Under The Petroleum Industry Actahassan2No ratings yet

- Panel4 AdrianMunandar ITC2020Document18 pagesPanel4 AdrianMunandar ITC2020diana_busrizaltiNo ratings yet

- eJTR Vol11-No3 2013Document212 pageseJTR Vol11-No3 2013diana_busrizaltiNo ratings yet

- Expert Opininon On Mine TaxationDocument57 pagesExpert Opininon On Mine Taxationdiana_busrizaltiNo ratings yet

- Ai - PPT 6 (Business Processes and Risks)Document22 pagesAi - PPT 6 (Business Processes and Risks)diana_busrizaltiNo ratings yet

- Ai - PPT 7 (Internal Control)Document30 pagesAi - PPT 7 (Internal Control)diana_busrizalti100% (1)

- VEF CalculationDocument6 pagesVEF CalculationProtyay ChakrabortyNo ratings yet

- MIcro Tutorial 5 ANSDocument5 pagesMIcro Tutorial 5 ANSBintang David SusantoNo ratings yet

- Original For Recipient: Order Number: RDF15750659Document2 pagesOriginal For Recipient: Order Number: RDF15750659Rajat DawraNo ratings yet

- Red OceanDocument17 pagesRed OceanSaipriya Raghavan0% (1)

- Appendix A Pricing Products and ServicesDocument23 pagesAppendix A Pricing Products and ServicesJaved AhmedNo ratings yet

- Chase Credit Card ApplicationDocument4 pagesChase Credit Card ApplicationJames McguireNo ratings yet

- Peachtree A Complete AnswersDocument5 pagesPeachtree A Complete AnswersPhilip JosephNo ratings yet

- Income Taxation AssignmentDocument1 pageIncome Taxation AssignmentHannah MeranoNo ratings yet

- (Financial Accounting & Reporting 2) : Lecture AidDocument18 pages(Financial Accounting & Reporting 2) : Lecture AidMay Grethel Joy PeranteNo ratings yet

- Marketing PlanDocument15 pagesMarketing Planvarooval_80No ratings yet

- Ethiopia - Starbucks PDFDocument15 pagesEthiopia - Starbucks PDFPriscilla SharonNo ratings yet

- Chola E-Auction Sale Notice Vishal Pandit Mahale 11.10.2023 Dhule Physical 15 DaysDocument5 pagesChola E-Auction Sale Notice Vishal Pandit Mahale 11.10.2023 Dhule Physical 15 DaysAman SainiNo ratings yet

- Ch10 DepreciationDocument18 pagesCh10 DepreciationRama KrishnaNo ratings yet

- Solution - 08.38 PDFDocument2 pagesSolution - 08.38 PDFsanNo ratings yet

- Session 04-WTC PPT (Jan 28, 2019)Document32 pagesSession 04-WTC PPT (Jan 28, 2019)MtashuNo ratings yet

- Lesson 2 Statement of Comprehensive IncomeDocument23 pagesLesson 2 Statement of Comprehensive IncomePaulette Sarno80% (5)

- Grom PresentationDocument10 pagesGrom PresentationMathan Anto MarshineNo ratings yet

- Chapter 8Document17 pagesChapter 8Jamaica DavidNo ratings yet

- ContractsDocument12 pagesContractsriyqNo ratings yet

- Chapter 11 Pricing Strategies: Additional Considerations: Principles of Marketing, 17e (Kotler/Armstrong)Document21 pagesChapter 11 Pricing Strategies: Additional Considerations: Principles of Marketing, 17e (Kotler/Armstrong)RosyLeeNo ratings yet

- Group Assignment On Variable PricingDocument1 pageGroup Assignment On Variable PricingKowshik MoyyaNo ratings yet

- PR 10037 Canvass SheetDocument4 pagesPR 10037 Canvass SheetjaymarNo ratings yet

- Primary MarketDocument18 pagesPrimary MarketRaman RandhawaNo ratings yet

- GST Reforms-TB ChatterjeeDocument14 pagesGST Reforms-TB ChatterjeeJogender ChauhanNo ratings yet

- Sri Lanka Textile and Apparel IndustryDocument13 pagesSri Lanka Textile and Apparel IndustryAnushka IttapanaNo ratings yet

- Hedging Strategies Using FuturesDocument23 pagesHedging Strategies Using FuturesBiswajit SarmaNo ratings yet