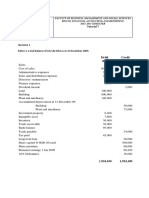

CSOCF Acquisition Both Methods Malim Nawar BHD

CSOCF Acquisition Both Methods Malim Nawar BHD

You might also like

- Lazar Blue Book Chapter 4 Solution (1 To 14 Only)Document27 pagesLazar Blue Book Chapter 4 Solution (1 To 14 Only)Shuhada Shamsuddin75% (4)

- LinkedIn ValuationDocument13 pagesLinkedIn ValuationSunil Acharya100% (1)

- ACCN 304 Revision QuestionsDocument11 pagesACCN 304 Revision Questionskelvinmunashenyamutumba100% (1)

- Tutorial - Financial StatementDocument18 pagesTutorial - Financial StatementmellNo ratings yet

- Bbaw 2103 - Financial AccountingDocument8 pagesBbaw 2103 - Financial AccountingRainie LimNo ratings yet

- TWO (2) Questions in SECTION B in The Answer Booklet Provided. SECTION A: Answer ALL Questions in This SectionDocument6 pagesTWO (2) Questions in SECTION B in The Answer Booklet Provided. SECTION A: Answer ALL Questions in This SectionRebecca TeoNo ratings yet

- FE QUESTION FIN 2224 Sept2021Document6 pagesFE QUESTION FIN 2224 Sept2021Tabish HyderNo ratings yet

- Far320 Capital Reduction ExercisesDocument7 pagesFar320 Capital Reduction ExercisesALIA MAISARA MD AKHIRNo ratings yet

- Tutorial 7 - IntangibleDocument2 pagesTutorial 7 - IntangibleABABNo ratings yet

- Chapter 7 - Financial RatiosDocument8 pagesChapter 7 - Financial RatiosNatasha GhazaliNo ratings yet

- 18 Dec 2020 ADocument8 pages18 Dec 2020 AYIN LING CHOYNo ratings yet

- 高一簿记模拟试卷Document6 pages高一簿记模拟试卷Carpenters ForeverNo ratings yet

- Assignment 2 Far110Document4 pagesAssignment 2 Far110AisyahNo ratings yet

- 2021 S2 18 Limited COmpanyDocument2 pages2021 S2 18 Limited COmpanyJingyiNo ratings yet

- Tutorial 13 14 RevisedDocument4 pagesTutorial 13 14 RevisedEsther LuehNo ratings yet

- Q8 Motswala LimitedDocument2 pagesQ8 Motswala Limitedamosmalusi5No ratings yet

- Group Project 2 Sabry Zamato SolutionDocument5 pagesGroup Project 2 Sabry Zamato SolutionSyafahani SafieNo ratings yet

- Tutorial On Inventory and FSDocument3 pagesTutorial On Inventory and FSNcediswaNo ratings yet

- ACCT 101 - Assignment Question (13861)Document5 pagesACCT 101 - Assignment Question (13861)Aneziwe ShangeNo ratings yet

- Financial Accounting and Reporting PDFDocument12 pagesFinancial Accounting and Reporting PDFanis athirahNo ratings yet

- Class Exercise 4B Changes in Shareholding Interest: Increase in ShareholdingDocument2 pagesClass Exercise 4B Changes in Shareholding Interest: Increase in ShareholdingMUHAMMAD HAMIZAN BIN ROSMAN MoeNo ratings yet

- Acc106 Assignment 2 Tie Beauty Enterprise FinalDocument15 pagesAcc106 Assignment 2 Tie Beauty Enterprise Finalnur anisNo ratings yet

- Far210.statement of Cash FlowDocument8 pagesFar210.statement of Cash FlowElsie AnnNo ratings yet

- FHBM1214 WK 8 9 Qns - LDocument3 pagesFHBM1214 WK 8 9 Qns - LKelvin LeongNo ratings yet

- Tutorial 1 A172 Interco TransactionDocument5 pagesTutorial 1 A172 Interco TransactionNisrina NSNo ratings yet

- Axia BHD QDocument2 pagesAxia BHD QkkNo ratings yet

- Test 2 May 19 QuestionDocument4 pagesTest 2 May 19 QuestionNUR INTAN ATHIRAH MOHAMAD RAMLANNo ratings yet

- Csec Poa January 2012 p2Document9 pagesCsec Poa January 2012 p2Renelle RampersadNo ratings yet

- Tutorial 2 A192 QuestionDocument9 pagesTutorial 2 A192 QuestionMastura Abd HamidNo ratings yet

- Week 10Document3 pagesWeek 10xinghe666No ratings yet

- Duch Ravi (16ACT41sb1)Document3 pagesDuch Ravi (16ACT41sb1)chhayloeng60No ratings yet

- Company Financial Statements - FORMAT LTDDocument5 pagesCompany Financial Statements - FORMAT LTDrumelrashid_seuNo ratings yet

- Malik Group of Companies (Disposal + Acquisition) : Cfap 1: A A F RDocument1 pageMalik Group of Companies (Disposal + Acquisition) : Cfap 1: A A F R.No ratings yet

- 3.BACC III 2016 End - Docx ModeratedDocument7 pages3.BACC III 2016 End - Docx ModeratedsmlingwaNo ratings yet

- Mid Term FIN 514Document4 pagesMid Term FIN 514Showkatul IslamNo ratings yet

- ACC106 Assignment AccountDocument5 pagesACC106 Assignment AccountsyafiqahNo ratings yet

- Accounting 621Document2 pagesAccounting 621Sarah Precious NkoanaNo ratings yet

- Tutorial 12 Performance MeasurementDocument4 pagesTutorial 12 Performance MeasurementEsther LuehNo ratings yet

- Model Question PaperDocument3 pagesModel Question Paperi.am.dheeraj8463No ratings yet

- Ratio Analysis SolutionDocument7 pagesRatio Analysis SolutionYakub Ali SalimNo ratings yet

- Fa5 Nov20Document8 pagesFa5 Nov20Ridzuan SharifNo ratings yet

- Chapter 11 Financial Accounting With Adjustment: Question 1 FuguangDocument15 pagesChapter 11 Financial Accounting With Adjustment: Question 1 FuguangClaudia WongNo ratings yet

- Tutorial 2 - A202 QuestionDocument6 pagesTutorial 2 - A202 QuestionFuchoin ReikoNo ratings yet

- 20solution Far460 - Jun 2020 - StudentDocument10 pages20solution Far460 - Jun 2020 - StudentRuzaikha razaliNo ratings yet

- Cash Flow Tutorial QnsDocument13 pagesCash Flow Tutorial QnsCristian Renatus100% (1)

- Topic 6 Test ISBS 3E4Document5 pagesTopic 6 Test ISBS 3E4LynnHanNo ratings yet

- Illustration Ratio AnalysisDocument6 pagesIllustration Ratio AnalysisMUINDI MUASYA KENNEDY D190/18836/2020No ratings yet

- Jawapan Chapter 3Document7 pagesJawapan Chapter 3wawan0% (2)

- L03 - Accounting Classification and EquationsDocument29 pagesL03 - Accounting Classification and EquationsmardhiahNo ratings yet

- Apr 19Document8 pagesApr 19nur sabrinaNo ratings yet

- Acc3201 (F) Aug2014Document5 pagesAcc3201 (F) Aug2014natlyhNo ratings yet

- Solution Fin Accting FundamentalsDocument7 pagesSolution Fin Accting Fundamentalsabhaymvyas1144No ratings yet

- Income Statement - Practice Activities - FinalDocument25 pagesIncome Statement - Practice Activities - Finalkyliekristen915No ratings yet

- Sample Quiz March 2022Document2 pagesSample Quiz March 20222024916967No ratings yet

- 2022 KZN June P1 QPDocument10 pages2022 KZN June P1 QPshandren19No ratings yet

- Busines Account AssigmentDocument9 pagesBusines Account AssigmentaqilahNo ratings yet

- Revision Question BAAB1014 May 23-1Document6 pagesRevision Question BAAB1014 May 23-1Hareen JuniorNo ratings yet

- AFI3512 Test 4 2022 QuestionDocument6 pagesAFI3512 Test 4 2022 Questionkevgoat217No ratings yet

- 04 Extra Question Pack For Chapter 4 After Initial AcquisitionDocument3 pages04 Extra Question Pack For Chapter 4 After Initial AcquisitionhlisoNo ratings yet

- Acc Chapter 5Document11 pagesAcc Chapter 5NURUL HAZWANIE HIDNI BINTI MUHAMAD SABRI MoeNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Xyz BHD Consolidated Statement of Cash Flow For The Year Ended 31 December 2018 RM Million RM Million Cash Flow From Operating ActivitiesDocument10 pagesXyz BHD Consolidated Statement of Cash Flow For The Year Ended 31 December 2018 RM Million RM Million Cash Flow From Operating ActivitiesSyafahani SafieNo ratings yet

- Faculty of Accountancy Bachelor of Accountancy (Hons.)Document8 pagesFaculty of Accountancy Bachelor of Accountancy (Hons.)Syafahani SafieNo ratings yet

- GP 2 Far 620Document17 pagesGP 2 Far 620Syafahani SafieNo ratings yet

- GP 2 Far 620Document8 pagesGP 2 Far 620Syafahani SafieNo ratings yet

- Group Project 2 Sabry Zamato SolutionDocument5 pagesGroup Project 2 Sabry Zamato SolutionSyafahani SafieNo ratings yet

- Intercompany Sale of PropertyDocument6 pagesIntercompany Sale of PropertyClauie BarsNo ratings yet

- Futures-Trade-Lifecycle - Part 2 of 2Document24 pagesFutures-Trade-Lifecycle - Part 2 of 2gupta_rajesh_621791100% (1)

- Ethan Chamo's ResumeDocument1 pageEthan Chamo's ResumeAnonymous xyjgNsNMNo ratings yet

- AF5102 Accounting Theory Introduction & Accounting Under Ideal ConditionsDocument15 pagesAF5102 Accounting Theory Introduction & Accounting Under Ideal ConditionsXinwei GuoNo ratings yet

- Finance Interview QuestionsDocument14 pagesFinance Interview QuestionsVivek SequeiraNo ratings yet

- Capital Structure Summary and Conclusions CHAPTER 17Document1 pageCapital Structure Summary and Conclusions CHAPTER 17ckkuteesaNo ratings yet

- Distressed M&ADocument2 pagesDistressed M&AKwadwo AsaseNo ratings yet

- KNM Group Annual Report 2017 PDFDocument170 pagesKNM Group Annual Report 2017 PDFgjangNo ratings yet

- HOME - PSE - SEC Form 17C - Board Resolution - April 14, 2023Document4 pagesHOME - PSE - SEC Form 17C - Board Resolution - April 14, 2023Julius Mark Carinhay TolitolNo ratings yet

- Assignment - Jackson CODocument4 pagesAssignment - Jackson COMhmd KaramNo ratings yet

- Chap016 PDFDocument249 pagesChap016 PDFJazzmin Rose NgNo ratings yet

- Chapter 1 How Management Accounting Information Supports Decision MakingDocument22 pagesChapter 1 How Management Accounting Information Supports Decision MakingGks06No ratings yet

- Accounting For Managers Question BankDocument5 pagesAccounting For Managers Question BankbhfunNo ratings yet

- Assignment # 4 26 CH 22Document6 pagesAssignment # 4 26 CH 22Ibrahim AbdallahNo ratings yet

- Techno Computer Training CenterDocument11 pagesTechno Computer Training CenterAlemnew SisayNo ratings yet

- Impact of Changes in Accounting PoliciesDocument16 pagesImpact of Changes in Accounting Policiessantosh kumar mauryaNo ratings yet

- Intangible Assets Test Bank and AnswersDocument51 pagesIntangible Assets Test Bank and AnswersNikolay CliffordNo ratings yet

- 5 6120800679993803735Document39 pages5 6120800679993803735Harmony Clement-ebereNo ratings yet

- F3 - Accounting StandardsDocument6 pagesF3 - Accounting Standardsnoor ul anumNo ratings yet

- Ilham AdzakyDocument9 pagesIlham AdzakyMoe ChannelNo ratings yet

- The Puppet Masters: How The Corrupt Use Legal Structures To Hide Stolen Assets and What To Do About ItDocument284 pagesThe Puppet Masters: How The Corrupt Use Legal Structures To Hide Stolen Assets and What To Do About ItSteve B. SalongaNo ratings yet

- Revenue Recognition and Franchise TestbankDocument43 pagesRevenue Recognition and Franchise TestbankBusiness MatterNo ratings yet

- Indian Financial SystemDocument91 pagesIndian Financial SystemAnkit Sablok100% (2)

- Deffered Tax and Tax Expense and Owner - Cheat SheetDocument5 pagesDeffered Tax and Tax Expense and Owner - Cheat SheetSayorn Monanusa ChinNo ratings yet

- Cash Flow Statement Cpale BoardDocument2 pagesCash Flow Statement Cpale BoardSharon CarilloNo ratings yet

- Unit 6 Leverages PDFDocument21 pagesUnit 6 Leverages PDFreliableplacement67% (3)

- Manish Gupta: Presented byDocument20 pagesManish Gupta: Presented byManish GuptaNo ratings yet

- Chapter 9 Financial AccountingDocument18 pagesChapter 9 Financial AccountingYukino YukinoshitaNo ratings yet

- Long-Term Performance of Seasoned Equity OfferingsDocument27 pagesLong-Term Performance of Seasoned Equity Offeringsgogayin869No ratings yet

Download as docx, pdf, or txt

You might also like

- Lazar Blue Book Chapter 4 Solution (1 To 14 Only)Document27 pagesLazar Blue Book Chapter 4 Solution (1 To 14 Only)Shuhada Shamsuddin75% (4)

- LinkedIn ValuationDocument13 pagesLinkedIn ValuationSunil Acharya100% (1)

- ACCN 304 Revision QuestionsDocument11 pagesACCN 304 Revision Questionskelvinmunashenyamutumba100% (1)

- Tutorial - Financial StatementDocument18 pagesTutorial - Financial StatementmellNo ratings yet

- Bbaw 2103 - Financial AccountingDocument8 pagesBbaw 2103 - Financial AccountingRainie LimNo ratings yet

- TWO (2) Questions in SECTION B in The Answer Booklet Provided. SECTION A: Answer ALL Questions in This SectionDocument6 pagesTWO (2) Questions in SECTION B in The Answer Booklet Provided. SECTION A: Answer ALL Questions in This SectionRebecca TeoNo ratings yet

- FE QUESTION FIN 2224 Sept2021Document6 pagesFE QUESTION FIN 2224 Sept2021Tabish HyderNo ratings yet

- Far320 Capital Reduction ExercisesDocument7 pagesFar320 Capital Reduction ExercisesALIA MAISARA MD AKHIRNo ratings yet

- Tutorial 7 - IntangibleDocument2 pagesTutorial 7 - IntangibleABABNo ratings yet

- Chapter 7 - Financial RatiosDocument8 pagesChapter 7 - Financial RatiosNatasha GhazaliNo ratings yet

- 18 Dec 2020 ADocument8 pages18 Dec 2020 AYIN LING CHOYNo ratings yet

- 高一簿记模拟试卷Document6 pages高一簿记模拟试卷Carpenters ForeverNo ratings yet

- Assignment 2 Far110Document4 pagesAssignment 2 Far110AisyahNo ratings yet

- 2021 S2 18 Limited COmpanyDocument2 pages2021 S2 18 Limited COmpanyJingyiNo ratings yet

- Tutorial 13 14 RevisedDocument4 pagesTutorial 13 14 RevisedEsther LuehNo ratings yet

- Q8 Motswala LimitedDocument2 pagesQ8 Motswala Limitedamosmalusi5No ratings yet

- Group Project 2 Sabry Zamato SolutionDocument5 pagesGroup Project 2 Sabry Zamato SolutionSyafahani SafieNo ratings yet

- Tutorial On Inventory and FSDocument3 pagesTutorial On Inventory and FSNcediswaNo ratings yet

- ACCT 101 - Assignment Question (13861)Document5 pagesACCT 101 - Assignment Question (13861)Aneziwe ShangeNo ratings yet

- Financial Accounting and Reporting PDFDocument12 pagesFinancial Accounting and Reporting PDFanis athirahNo ratings yet

- Class Exercise 4B Changes in Shareholding Interest: Increase in ShareholdingDocument2 pagesClass Exercise 4B Changes in Shareholding Interest: Increase in ShareholdingMUHAMMAD HAMIZAN BIN ROSMAN MoeNo ratings yet

- Acc106 Assignment 2 Tie Beauty Enterprise FinalDocument15 pagesAcc106 Assignment 2 Tie Beauty Enterprise Finalnur anisNo ratings yet

- Far210.statement of Cash FlowDocument8 pagesFar210.statement of Cash FlowElsie AnnNo ratings yet

- FHBM1214 WK 8 9 Qns - LDocument3 pagesFHBM1214 WK 8 9 Qns - LKelvin LeongNo ratings yet

- Tutorial 1 A172 Interco TransactionDocument5 pagesTutorial 1 A172 Interco TransactionNisrina NSNo ratings yet

- Axia BHD QDocument2 pagesAxia BHD QkkNo ratings yet

- Test 2 May 19 QuestionDocument4 pagesTest 2 May 19 QuestionNUR INTAN ATHIRAH MOHAMAD RAMLANNo ratings yet

- Csec Poa January 2012 p2Document9 pagesCsec Poa January 2012 p2Renelle RampersadNo ratings yet

- Tutorial 2 A192 QuestionDocument9 pagesTutorial 2 A192 QuestionMastura Abd HamidNo ratings yet

- Week 10Document3 pagesWeek 10xinghe666No ratings yet

- Duch Ravi (16ACT41sb1)Document3 pagesDuch Ravi (16ACT41sb1)chhayloeng60No ratings yet

- Company Financial Statements - FORMAT LTDDocument5 pagesCompany Financial Statements - FORMAT LTDrumelrashid_seuNo ratings yet

- Malik Group of Companies (Disposal + Acquisition) : Cfap 1: A A F RDocument1 pageMalik Group of Companies (Disposal + Acquisition) : Cfap 1: A A F R.No ratings yet

- 3.BACC III 2016 End - Docx ModeratedDocument7 pages3.BACC III 2016 End - Docx ModeratedsmlingwaNo ratings yet

- Mid Term FIN 514Document4 pagesMid Term FIN 514Showkatul IslamNo ratings yet

- ACC106 Assignment AccountDocument5 pagesACC106 Assignment AccountsyafiqahNo ratings yet

- Accounting 621Document2 pagesAccounting 621Sarah Precious NkoanaNo ratings yet

- Tutorial 12 Performance MeasurementDocument4 pagesTutorial 12 Performance MeasurementEsther LuehNo ratings yet

- Model Question PaperDocument3 pagesModel Question Paperi.am.dheeraj8463No ratings yet

- Ratio Analysis SolutionDocument7 pagesRatio Analysis SolutionYakub Ali SalimNo ratings yet

- Fa5 Nov20Document8 pagesFa5 Nov20Ridzuan SharifNo ratings yet

- Chapter 11 Financial Accounting With Adjustment: Question 1 FuguangDocument15 pagesChapter 11 Financial Accounting With Adjustment: Question 1 FuguangClaudia WongNo ratings yet

- Tutorial 2 - A202 QuestionDocument6 pagesTutorial 2 - A202 QuestionFuchoin ReikoNo ratings yet

- 20solution Far460 - Jun 2020 - StudentDocument10 pages20solution Far460 - Jun 2020 - StudentRuzaikha razaliNo ratings yet

- Cash Flow Tutorial QnsDocument13 pagesCash Flow Tutorial QnsCristian Renatus100% (1)

- Topic 6 Test ISBS 3E4Document5 pagesTopic 6 Test ISBS 3E4LynnHanNo ratings yet

- Illustration Ratio AnalysisDocument6 pagesIllustration Ratio AnalysisMUINDI MUASYA KENNEDY D190/18836/2020No ratings yet

- Jawapan Chapter 3Document7 pagesJawapan Chapter 3wawan0% (2)

- L03 - Accounting Classification and EquationsDocument29 pagesL03 - Accounting Classification and EquationsmardhiahNo ratings yet

- Apr 19Document8 pagesApr 19nur sabrinaNo ratings yet

- Acc3201 (F) Aug2014Document5 pagesAcc3201 (F) Aug2014natlyhNo ratings yet

- Solution Fin Accting FundamentalsDocument7 pagesSolution Fin Accting Fundamentalsabhaymvyas1144No ratings yet

- Income Statement - Practice Activities - FinalDocument25 pagesIncome Statement - Practice Activities - Finalkyliekristen915No ratings yet

- Sample Quiz March 2022Document2 pagesSample Quiz March 20222024916967No ratings yet

- 2022 KZN June P1 QPDocument10 pages2022 KZN June P1 QPshandren19No ratings yet

- Busines Account AssigmentDocument9 pagesBusines Account AssigmentaqilahNo ratings yet

- Revision Question BAAB1014 May 23-1Document6 pagesRevision Question BAAB1014 May 23-1Hareen JuniorNo ratings yet

- AFI3512 Test 4 2022 QuestionDocument6 pagesAFI3512 Test 4 2022 Questionkevgoat217No ratings yet

- 04 Extra Question Pack For Chapter 4 After Initial AcquisitionDocument3 pages04 Extra Question Pack For Chapter 4 After Initial AcquisitionhlisoNo ratings yet

- Acc Chapter 5Document11 pagesAcc Chapter 5NURUL HAZWANIE HIDNI BINTI MUHAMAD SABRI MoeNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Xyz BHD Consolidated Statement of Cash Flow For The Year Ended 31 December 2018 RM Million RM Million Cash Flow From Operating ActivitiesDocument10 pagesXyz BHD Consolidated Statement of Cash Flow For The Year Ended 31 December 2018 RM Million RM Million Cash Flow From Operating ActivitiesSyafahani SafieNo ratings yet

- Faculty of Accountancy Bachelor of Accountancy (Hons.)Document8 pagesFaculty of Accountancy Bachelor of Accountancy (Hons.)Syafahani SafieNo ratings yet

- GP 2 Far 620Document17 pagesGP 2 Far 620Syafahani SafieNo ratings yet

- GP 2 Far 620Document8 pagesGP 2 Far 620Syafahani SafieNo ratings yet

- Group Project 2 Sabry Zamato SolutionDocument5 pagesGroup Project 2 Sabry Zamato SolutionSyafahani SafieNo ratings yet

- Intercompany Sale of PropertyDocument6 pagesIntercompany Sale of PropertyClauie BarsNo ratings yet

- Futures-Trade-Lifecycle - Part 2 of 2Document24 pagesFutures-Trade-Lifecycle - Part 2 of 2gupta_rajesh_621791100% (1)

- Ethan Chamo's ResumeDocument1 pageEthan Chamo's ResumeAnonymous xyjgNsNMNo ratings yet

- AF5102 Accounting Theory Introduction & Accounting Under Ideal ConditionsDocument15 pagesAF5102 Accounting Theory Introduction & Accounting Under Ideal ConditionsXinwei GuoNo ratings yet

- Finance Interview QuestionsDocument14 pagesFinance Interview QuestionsVivek SequeiraNo ratings yet

- Capital Structure Summary and Conclusions CHAPTER 17Document1 pageCapital Structure Summary and Conclusions CHAPTER 17ckkuteesaNo ratings yet

- Distressed M&ADocument2 pagesDistressed M&AKwadwo AsaseNo ratings yet

- KNM Group Annual Report 2017 PDFDocument170 pagesKNM Group Annual Report 2017 PDFgjangNo ratings yet

- HOME - PSE - SEC Form 17C - Board Resolution - April 14, 2023Document4 pagesHOME - PSE - SEC Form 17C - Board Resolution - April 14, 2023Julius Mark Carinhay TolitolNo ratings yet

- Assignment - Jackson CODocument4 pagesAssignment - Jackson COMhmd KaramNo ratings yet

- Chap016 PDFDocument249 pagesChap016 PDFJazzmin Rose NgNo ratings yet

- Chapter 1 How Management Accounting Information Supports Decision MakingDocument22 pagesChapter 1 How Management Accounting Information Supports Decision MakingGks06No ratings yet

- Accounting For Managers Question BankDocument5 pagesAccounting For Managers Question BankbhfunNo ratings yet

- Assignment # 4 26 CH 22Document6 pagesAssignment # 4 26 CH 22Ibrahim AbdallahNo ratings yet

- Techno Computer Training CenterDocument11 pagesTechno Computer Training CenterAlemnew SisayNo ratings yet

- Impact of Changes in Accounting PoliciesDocument16 pagesImpact of Changes in Accounting Policiessantosh kumar mauryaNo ratings yet

- Intangible Assets Test Bank and AnswersDocument51 pagesIntangible Assets Test Bank and AnswersNikolay CliffordNo ratings yet

- 5 6120800679993803735Document39 pages5 6120800679993803735Harmony Clement-ebereNo ratings yet

- F3 - Accounting StandardsDocument6 pagesF3 - Accounting Standardsnoor ul anumNo ratings yet

- Ilham AdzakyDocument9 pagesIlham AdzakyMoe ChannelNo ratings yet

- The Puppet Masters: How The Corrupt Use Legal Structures To Hide Stolen Assets and What To Do About ItDocument284 pagesThe Puppet Masters: How The Corrupt Use Legal Structures To Hide Stolen Assets and What To Do About ItSteve B. SalongaNo ratings yet

- Revenue Recognition and Franchise TestbankDocument43 pagesRevenue Recognition and Franchise TestbankBusiness MatterNo ratings yet

- Indian Financial SystemDocument91 pagesIndian Financial SystemAnkit Sablok100% (2)

- Deffered Tax and Tax Expense and Owner - Cheat SheetDocument5 pagesDeffered Tax and Tax Expense and Owner - Cheat SheetSayorn Monanusa ChinNo ratings yet

- Cash Flow Statement Cpale BoardDocument2 pagesCash Flow Statement Cpale BoardSharon CarilloNo ratings yet

- Unit 6 Leverages PDFDocument21 pagesUnit 6 Leverages PDFreliableplacement67% (3)

- Manish Gupta: Presented byDocument20 pagesManish Gupta: Presented byManish GuptaNo ratings yet

- Chapter 9 Financial AccountingDocument18 pagesChapter 9 Financial AccountingYukino YukinoshitaNo ratings yet

- Long-Term Performance of Seasoned Equity OfferingsDocument27 pagesLong-Term Performance of Seasoned Equity Offeringsgogayin869No ratings yet