New Business Registration (BIR)

New Business Registration (BIR)

You might also like

- ICAB Manual - Tax Planning & Compliance (2020)Document584 pagesICAB Manual - Tax Planning & Compliance (2020)Tasmia Binte Habib100% (5)

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

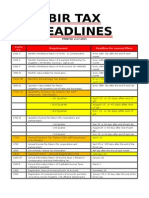

- BIR Tax Deadlines: Home About Us Services Clientele Contact UsDocument2 pagesBIR Tax Deadlines: Home About Us Services Clientele Contact UsNICKOL NAMOCNo ratings yet

- Taxation Reviewer - REODocument202 pagesTaxation Reviewer - REOtmica7260No ratings yet

- TAX PAYER GUIDE MannualDocument7 pagesTAX PAYER GUIDE MannualLevi Lazareno EugenioNo ratings yet

- Bir FormDocument3 pagesBir FormChelsea Anne VidalloNo ratings yet

- BIR Registration & Due Dates-1Document6 pagesBIR Registration & Due Dates-1jessicamarieogbinar37No ratings yet

- BIR Tax DeadlinesDocument2 pagesBIR Tax Deadlinesimports.fcfilesNo ratings yet

- Guidelines On Compliances and DocumentationDocument4 pagesGuidelines On Compliances and DocumentationJfm A Dazlac100% (1)

- Briefing MADE EASY-LUCILLEDocument51 pagesBriefing MADE EASY-LUCILLEJames Robert Marquez AlvarezNo ratings yet

- Form No. Requirement Deadline For Manual Filers: BIR Tax DeadlinesDocument7 pagesForm No. Requirement Deadline For Manual Filers: BIR Tax DeadlinesromarcambriNo ratings yet

- Compliances Under GST & Income Tax Act-KinexinDocument3 pagesCompliances Under GST & Income Tax Act-KinexinDeepak ChauhanNo ratings yet

- Bir - Webinar - New RegistrantsDocument107 pagesBir - Webinar - New RegistrantsEdward Gan100% (1)

- Taxation Laws - Ms. de CastroDocument54 pagesTaxation Laws - Ms. de CastroCC100% (1)

- Bir Vat QueriesDocument8 pagesBir Vat QueriesMinerva Bautista RoseteNo ratings yet

- Tax Remedies of The GovernmentDocument16 pagesTax Remedies of The GovernmentrmsenyoritaNo ratings yet

- Registration, Taxation & Accounting Compliance of Construction IndustryDocument52 pagesRegistration, Taxation & Accounting Compliance of Construction IndustryJohn Erick FernandezNo ratings yet

- txtn502 Part2Document21 pagestxtn502 Part2Sandra Mae Cabuenas100% (1)

- Deductions From Gross Income: Basis Ceiling RuleDocument8 pagesDeductions From Gross Income: Basis Ceiling RuleFabiano JoeyNo ratings yet

- Value-Added TaxDocument33 pagesValue-Added TaxvicsNo ratings yet

- Deadlines TaxDocument3 pagesDeadlines TaxLouremie Delos Reyes MalabayabasNo ratings yet

- Final Withholding Tax: BIR Quarterly, Monthly or Annually DeadlineDocument2 pagesFinal Withholding Tax: BIR Quarterly, Monthly or Annually DeadlineMary Christine Formiloza MacalinaoNo ratings yet

- Income Taxation Final Exam Please Show Solution (If Necessary)Document5 pagesIncome Taxation Final Exam Please Show Solution (If Necessary)E. RobertNo ratings yet

- BIR RDO 113 Taxpayers' Compliance Guide 2019Document4 pagesBIR RDO 113 Taxpayers' Compliance Guide 2019Noli Heje de Castro Jr.100% (1)

- TAX-304 (VAT Compliance Requirements)Document4 pagesTAX-304 (VAT Compliance Requirements)Ryan AllanicNo ratings yet

- GST Return FilingDocument9 pagesGST Return FilingSanthosh K SNo ratings yet

- Value Added Tax-PDocument20 pagesValue Added Tax-PMa. Corazon CaramalesNo ratings yet

- About The VAT (PDocument11 pagesAbout The VAT (PAmie Jane MirandaNo ratings yet

- GST Returns: What Is GST Return??Document11 pagesGST Returns: What Is GST Return??Yukta AgrawalNo ratings yet

- EO 98 - How To Apply TINDocument7 pagesEO 98 - How To Apply TINPeterSalas100% (1)

- TaxDocument19 pagesTaxjhevesNo ratings yet

- Value-Added Tax: DescriptionDocument26 pagesValue-Added Tax: DescriptionGIGI BODONo ratings yet

- Introduction To GST Unit 1 8 Mark Questions.Document4 pagesIntroduction To GST Unit 1 8 Mark Questions.manoharchary157No ratings yet

- Tax Advisory BIR Form Shall Be Used For VAT PDFDocument1 pageTax Advisory BIR Form Shall Be Used For VAT PDFAndrew Benedict PardilloNo ratings yet

- Janina Louise Caliboso Bsa 3A: Tax Reform For Acceleration and Inclusion (TRAIN) "Document3 pagesJanina Louise Caliboso Bsa 3A: Tax Reform For Acceleration and Inclusion (TRAIN) "Ja CalibosoNo ratings yet

- GST Return Business Process For GSTDocument72 pagesGST Return Business Process For GSTAccounting & Taxation100% (1)

- PEZA REPORTORIAL REQUIREMENTS As of Feb 2023Document2 pagesPEZA REPORTORIAL REQUIREMENTS As of Feb 2023MarkNo ratings yet

- Lecture Witholding TaxDocument152 pagesLecture Witholding Taxemytherese100% (2)

- Return: Return What Is GST ReturnDocument3 pagesReturn: Return What Is GST ReturnNagarjuna ReddyNo ratings yet

- Period When Returns Are Filed: BIR Form 1801Document4 pagesPeriod When Returns Are Filed: BIR Form 1801I Am Not DeterredNo ratings yet

- 3.2 Business Profit TaxDocument53 pages3.2 Business Profit TaxBizu AtnafuNo ratings yet

- AirbnbTaxGuide2024 Philippines ENGLISHDocument7 pagesAirbnbTaxGuide2024 Philippines ENGLISHandayarhealyn18No ratings yet

- Tax 304 - Vat Compliance RequirementsDocument5 pagesTax 304 - Vat Compliance RequirementsiBEAYNo ratings yet

- GST Return & FilingDocument14 pagesGST Return & Filingjibin samuelNo ratings yet

- Presentation On Taxation To The Construction Industry Federation of Zimbabwe (Cifoz)Document44 pagesPresentation On Taxation To The Construction Industry Federation of Zimbabwe (Cifoz)Franco DurantNo ratings yet

- Notes On Withholding Tax and Income Tax FilingDocument20 pagesNotes On Withholding Tax and Income Tax FilingnengNo ratings yet

- Revenue Regulation 2-99Document5 pagesRevenue Regulation 2-99Joanna MandapNo ratings yet

- Bir Tax Deadlines 2015Document2 pagesBir Tax Deadlines 2015Mary Grace BanezNo ratings yet

- Rulings2000 DigestDocument21 pagesRulings2000 DigestArriane MartinezNo ratings yet

- Section 44AFDocument4 pagesSection 44AFJitendra SonejaNo ratings yet

- RMC No 23-2012 - Withholding of TaxesDocument7 pagesRMC No 23-2012 - Withholding of TaxesJOHAYNIENo ratings yet

- 001 TMRAC Tax Compliance Guide Post Finance 2020 UpdatedDocument89 pages001 TMRAC Tax Compliance Guide Post Finance 2020 UpdatedHAMZA TAHIRNo ratings yet

- Mygov 1445315831190667 PDFDocument72 pagesMygov 1445315831190667 PDFjitendraktNo ratings yet

- Relationship Between Tax Compliance and Tax Dispute (Including TP Documentation)Document37 pagesRelationship Between Tax Compliance and Tax Dispute (Including TP Documentation)ryu255No ratings yet

- BIR FormsDocument1 pageBIR FormsBSA MaterialsNo ratings yet

- Frequently Asked Questions On VatDocument9 pagesFrequently Asked Questions On VatSteve SantillanNo ratings yet

- BIR FormsDocument30 pagesBIR FormsRoma Sabrina GenoguinNo ratings yet

- List of Bir FormsDocument37 pagesList of Bir FormsgachiNo ratings yet

- BMBE SeminarDocument60 pagesBMBE SeminarBabyGiant LucasNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- eFPS Home - SampleDocument2 pageseFPS Home - SampleCrizziaNo ratings yet

- GACPA, Inc. Convention Payment InstructionDocument3 pagesGACPA, Inc. Convention Payment InstructionCrizziaNo ratings yet

- Tax Planning Strategies - March.2022.pagaspasDocument15 pagesTax Planning Strategies - March.2022.pagaspasCrizziaNo ratings yet

- Powerpoint-03 19 22Document126 pagesPowerpoint-03 19 22CrizziaNo ratings yet

- Roles of Finance - SlidesDocument77 pagesRoles of Finance - SlidesCrizziaNo ratings yet

- 03 - Residence and Scope of Total IncomeDocument44 pages03 - Residence and Scope of Total IncomeTushar RathiNo ratings yet

- 1 Cpa Reviewer in Taxation by Tabag 2021Document145 pages1 Cpa Reviewer in Taxation by Tabag 2021Philip Rosos100% (4)

- CIR Vs COMELECDocument25 pagesCIR Vs COMELECEm EmNo ratings yet

- TaxxxxDocument3 pagesTaxxxxfaye gNo ratings yet

- J. Bersamin TaxDocument14 pagesJ. Bersamin TaxJessica JungNo ratings yet

- ATO Top 500 GST Assurance ProgramDocument206 pagesATO Top 500 GST Assurance Program8nkwv7q272No ratings yet

- Taxation Notes I. Taxation 1. Definition of Taxation Taxation As A PowerDocument17 pagesTaxation Notes I. Taxation 1. Definition of Taxation Taxation As A PowerReynaldo YuNo ratings yet

- Rule: Income Taxes: Corporate Estimated TaxDocument30 pagesRule: Income Taxes: Corporate Estimated TaxJustia.comNo ratings yet

- NoticeDocument4 pagesNoticeAl OkNo ratings yet

- Tax 1 FinalsDocument16 pagesTax 1 FinalsDenise DuriasNo ratings yet

- 12 - Republic V Lim Tian Teng SonsDocument6 pages12 - Republic V Lim Tian Teng SonsParis LisonNo ratings yet

- Black Book PDFDocument101 pagesBlack Book PDFA 53 Gracy AsirNo ratings yet

- Internship ReportDocument56 pagesInternship Reportsharma.harshita2019No ratings yet

- 10-Practical Questions of Individuals (78-113)Document38 pages10-Practical Questions of Individuals (78-113)Sajid Saith0% (1)

- Effect of Taxation On Small BusinessDocument37 pagesEffect of Taxation On Small BusinessBhanu pratap singh100% (1)

- Assessment of Collection Problem and The Cause With Regard To Profit Tax and Value Added Tax Taxpayer Found in Arbaminch TownDocument59 pagesAssessment of Collection Problem and The Cause With Regard To Profit Tax and Value Added Tax Taxpayer Found in Arbaminch Townmubarek oumerNo ratings yet

- Current Botswana Personal Income Tax Calculations (2020)Document4 pagesCurrent Botswana Personal Income Tax Calculations (2020)Eunice AdjeiNo ratings yet

- Chapter 8 VDocument28 pagesChapter 8 VAdd AllNo ratings yet

- Page 1 of 3Document3 pagesPage 1 of 3Chellezea UrsabiaNo ratings yet

- This Study Resource Was: TAX-702A: Income TAX Rates Corporations (A)Document7 pagesThis Study Resource Was: TAX-702A: Income TAX Rates Corporations (A)Erika Bermas MedenillaNo ratings yet

- Internship Report On ESMLDocument43 pagesInternship Report On ESMLZaighum AliNo ratings yet

- Presentation On Income TaxDocument9 pagesPresentation On Income TaxUnnati GuptaNo ratings yet

- Walunj 2424Document10 pagesWalunj 2424gurpNo ratings yet

- Residence in IndiaDocument7 pagesResidence in IndiaSuryaNo ratings yet

- Income TaxesDocument4 pagesIncome TaxesHana Grace MamangunNo ratings yet

- Ram Baan - Direct Tax MAY - 23: Ca Vikram BiyaniDocument179 pagesRam Baan - Direct Tax MAY - 23: Ca Vikram Biyanigirish bhattNo ratings yet

- Facts: Petitioners: Conwi, Et - Al. vs. CTA and CIRDocument3 pagesFacts: Petitioners: Conwi, Et - Al. vs. CTA and CIRBurn-Cindy AbadNo ratings yet

- ACC 311 Sample Problem General Instructions:: ST ND RD THDocument1 pageACC 311 Sample Problem General Instructions:: ST ND RD THexquisiteNo ratings yet

- Taxation PDFDocument69 pagesTaxation PDFcpasl123No ratings yet

Download as pdf or txt

You might also like

- ICAB Manual - Tax Planning & Compliance (2020)Document584 pagesICAB Manual - Tax Planning & Compliance (2020)Tasmia Binte Habib100% (5)

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- BIR Tax Deadlines: Home About Us Services Clientele Contact UsDocument2 pagesBIR Tax Deadlines: Home About Us Services Clientele Contact UsNICKOL NAMOCNo ratings yet

- Taxation Reviewer - REODocument202 pagesTaxation Reviewer - REOtmica7260No ratings yet

- TAX PAYER GUIDE MannualDocument7 pagesTAX PAYER GUIDE MannualLevi Lazareno EugenioNo ratings yet

- Bir FormDocument3 pagesBir FormChelsea Anne VidalloNo ratings yet

- BIR Registration & Due Dates-1Document6 pagesBIR Registration & Due Dates-1jessicamarieogbinar37No ratings yet

- BIR Tax DeadlinesDocument2 pagesBIR Tax Deadlinesimports.fcfilesNo ratings yet

- Guidelines On Compliances and DocumentationDocument4 pagesGuidelines On Compliances and DocumentationJfm A Dazlac100% (1)

- Briefing MADE EASY-LUCILLEDocument51 pagesBriefing MADE EASY-LUCILLEJames Robert Marquez AlvarezNo ratings yet

- Form No. Requirement Deadline For Manual Filers: BIR Tax DeadlinesDocument7 pagesForm No. Requirement Deadline For Manual Filers: BIR Tax DeadlinesromarcambriNo ratings yet

- Compliances Under GST & Income Tax Act-KinexinDocument3 pagesCompliances Under GST & Income Tax Act-KinexinDeepak ChauhanNo ratings yet

- Bir - Webinar - New RegistrantsDocument107 pagesBir - Webinar - New RegistrantsEdward Gan100% (1)

- Taxation Laws - Ms. de CastroDocument54 pagesTaxation Laws - Ms. de CastroCC100% (1)

- Bir Vat QueriesDocument8 pagesBir Vat QueriesMinerva Bautista RoseteNo ratings yet

- Tax Remedies of The GovernmentDocument16 pagesTax Remedies of The GovernmentrmsenyoritaNo ratings yet

- Registration, Taxation & Accounting Compliance of Construction IndustryDocument52 pagesRegistration, Taxation & Accounting Compliance of Construction IndustryJohn Erick FernandezNo ratings yet

- txtn502 Part2Document21 pagestxtn502 Part2Sandra Mae Cabuenas100% (1)

- Deductions From Gross Income: Basis Ceiling RuleDocument8 pagesDeductions From Gross Income: Basis Ceiling RuleFabiano JoeyNo ratings yet

- Value-Added TaxDocument33 pagesValue-Added TaxvicsNo ratings yet

- Deadlines TaxDocument3 pagesDeadlines TaxLouremie Delos Reyes MalabayabasNo ratings yet

- Final Withholding Tax: BIR Quarterly, Monthly or Annually DeadlineDocument2 pagesFinal Withholding Tax: BIR Quarterly, Monthly or Annually DeadlineMary Christine Formiloza MacalinaoNo ratings yet

- Income Taxation Final Exam Please Show Solution (If Necessary)Document5 pagesIncome Taxation Final Exam Please Show Solution (If Necessary)E. RobertNo ratings yet

- BIR RDO 113 Taxpayers' Compliance Guide 2019Document4 pagesBIR RDO 113 Taxpayers' Compliance Guide 2019Noli Heje de Castro Jr.100% (1)

- TAX-304 (VAT Compliance Requirements)Document4 pagesTAX-304 (VAT Compliance Requirements)Ryan AllanicNo ratings yet

- GST Return FilingDocument9 pagesGST Return FilingSanthosh K SNo ratings yet

- Value Added Tax-PDocument20 pagesValue Added Tax-PMa. Corazon CaramalesNo ratings yet

- About The VAT (PDocument11 pagesAbout The VAT (PAmie Jane MirandaNo ratings yet

- GST Returns: What Is GST Return??Document11 pagesGST Returns: What Is GST Return??Yukta AgrawalNo ratings yet

- EO 98 - How To Apply TINDocument7 pagesEO 98 - How To Apply TINPeterSalas100% (1)

- TaxDocument19 pagesTaxjhevesNo ratings yet

- Value-Added Tax: DescriptionDocument26 pagesValue-Added Tax: DescriptionGIGI BODONo ratings yet

- Introduction To GST Unit 1 8 Mark Questions.Document4 pagesIntroduction To GST Unit 1 8 Mark Questions.manoharchary157No ratings yet

- Tax Advisory BIR Form Shall Be Used For VAT PDFDocument1 pageTax Advisory BIR Form Shall Be Used For VAT PDFAndrew Benedict PardilloNo ratings yet

- Janina Louise Caliboso Bsa 3A: Tax Reform For Acceleration and Inclusion (TRAIN) "Document3 pagesJanina Louise Caliboso Bsa 3A: Tax Reform For Acceleration and Inclusion (TRAIN) "Ja CalibosoNo ratings yet

- GST Return Business Process For GSTDocument72 pagesGST Return Business Process For GSTAccounting & Taxation100% (1)

- PEZA REPORTORIAL REQUIREMENTS As of Feb 2023Document2 pagesPEZA REPORTORIAL REQUIREMENTS As of Feb 2023MarkNo ratings yet

- Lecture Witholding TaxDocument152 pagesLecture Witholding Taxemytherese100% (2)

- Return: Return What Is GST ReturnDocument3 pagesReturn: Return What Is GST ReturnNagarjuna ReddyNo ratings yet

- Period When Returns Are Filed: BIR Form 1801Document4 pagesPeriod When Returns Are Filed: BIR Form 1801I Am Not DeterredNo ratings yet

- 3.2 Business Profit TaxDocument53 pages3.2 Business Profit TaxBizu AtnafuNo ratings yet

- AirbnbTaxGuide2024 Philippines ENGLISHDocument7 pagesAirbnbTaxGuide2024 Philippines ENGLISHandayarhealyn18No ratings yet

- Tax 304 - Vat Compliance RequirementsDocument5 pagesTax 304 - Vat Compliance RequirementsiBEAYNo ratings yet

- GST Return & FilingDocument14 pagesGST Return & Filingjibin samuelNo ratings yet

- Presentation On Taxation To The Construction Industry Federation of Zimbabwe (Cifoz)Document44 pagesPresentation On Taxation To The Construction Industry Federation of Zimbabwe (Cifoz)Franco DurantNo ratings yet

- Notes On Withholding Tax and Income Tax FilingDocument20 pagesNotes On Withholding Tax and Income Tax FilingnengNo ratings yet

- Revenue Regulation 2-99Document5 pagesRevenue Regulation 2-99Joanna MandapNo ratings yet

- Bir Tax Deadlines 2015Document2 pagesBir Tax Deadlines 2015Mary Grace BanezNo ratings yet

- Rulings2000 DigestDocument21 pagesRulings2000 DigestArriane MartinezNo ratings yet

- Section 44AFDocument4 pagesSection 44AFJitendra SonejaNo ratings yet

- RMC No 23-2012 - Withholding of TaxesDocument7 pagesRMC No 23-2012 - Withholding of TaxesJOHAYNIENo ratings yet

- 001 TMRAC Tax Compliance Guide Post Finance 2020 UpdatedDocument89 pages001 TMRAC Tax Compliance Guide Post Finance 2020 UpdatedHAMZA TAHIRNo ratings yet

- Mygov 1445315831190667 PDFDocument72 pagesMygov 1445315831190667 PDFjitendraktNo ratings yet

- Relationship Between Tax Compliance and Tax Dispute (Including TP Documentation)Document37 pagesRelationship Between Tax Compliance and Tax Dispute (Including TP Documentation)ryu255No ratings yet

- BIR FormsDocument1 pageBIR FormsBSA MaterialsNo ratings yet

- Frequently Asked Questions On VatDocument9 pagesFrequently Asked Questions On VatSteve SantillanNo ratings yet

- BIR FormsDocument30 pagesBIR FormsRoma Sabrina GenoguinNo ratings yet

- List of Bir FormsDocument37 pagesList of Bir FormsgachiNo ratings yet

- BMBE SeminarDocument60 pagesBMBE SeminarBabyGiant LucasNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- eFPS Home - SampleDocument2 pageseFPS Home - SampleCrizziaNo ratings yet

- GACPA, Inc. Convention Payment InstructionDocument3 pagesGACPA, Inc. Convention Payment InstructionCrizziaNo ratings yet

- Tax Planning Strategies - March.2022.pagaspasDocument15 pagesTax Planning Strategies - March.2022.pagaspasCrizziaNo ratings yet

- Powerpoint-03 19 22Document126 pagesPowerpoint-03 19 22CrizziaNo ratings yet

- Roles of Finance - SlidesDocument77 pagesRoles of Finance - SlidesCrizziaNo ratings yet

- 03 - Residence and Scope of Total IncomeDocument44 pages03 - Residence and Scope of Total IncomeTushar RathiNo ratings yet

- 1 Cpa Reviewer in Taxation by Tabag 2021Document145 pages1 Cpa Reviewer in Taxation by Tabag 2021Philip Rosos100% (4)

- CIR Vs COMELECDocument25 pagesCIR Vs COMELECEm EmNo ratings yet

- TaxxxxDocument3 pagesTaxxxxfaye gNo ratings yet

- J. Bersamin TaxDocument14 pagesJ. Bersamin TaxJessica JungNo ratings yet

- ATO Top 500 GST Assurance ProgramDocument206 pagesATO Top 500 GST Assurance Program8nkwv7q272No ratings yet

- Taxation Notes I. Taxation 1. Definition of Taxation Taxation As A PowerDocument17 pagesTaxation Notes I. Taxation 1. Definition of Taxation Taxation As A PowerReynaldo YuNo ratings yet

- Rule: Income Taxes: Corporate Estimated TaxDocument30 pagesRule: Income Taxes: Corporate Estimated TaxJustia.comNo ratings yet

- NoticeDocument4 pagesNoticeAl OkNo ratings yet

- Tax 1 FinalsDocument16 pagesTax 1 FinalsDenise DuriasNo ratings yet

- 12 - Republic V Lim Tian Teng SonsDocument6 pages12 - Republic V Lim Tian Teng SonsParis LisonNo ratings yet

- Black Book PDFDocument101 pagesBlack Book PDFA 53 Gracy AsirNo ratings yet

- Internship ReportDocument56 pagesInternship Reportsharma.harshita2019No ratings yet

- 10-Practical Questions of Individuals (78-113)Document38 pages10-Practical Questions of Individuals (78-113)Sajid Saith0% (1)

- Effect of Taxation On Small BusinessDocument37 pagesEffect of Taxation On Small BusinessBhanu pratap singh100% (1)

- Assessment of Collection Problem and The Cause With Regard To Profit Tax and Value Added Tax Taxpayer Found in Arbaminch TownDocument59 pagesAssessment of Collection Problem and The Cause With Regard To Profit Tax and Value Added Tax Taxpayer Found in Arbaminch Townmubarek oumerNo ratings yet

- Current Botswana Personal Income Tax Calculations (2020)Document4 pagesCurrent Botswana Personal Income Tax Calculations (2020)Eunice AdjeiNo ratings yet

- Chapter 8 VDocument28 pagesChapter 8 VAdd AllNo ratings yet

- Page 1 of 3Document3 pagesPage 1 of 3Chellezea UrsabiaNo ratings yet

- This Study Resource Was: TAX-702A: Income TAX Rates Corporations (A)Document7 pagesThis Study Resource Was: TAX-702A: Income TAX Rates Corporations (A)Erika Bermas MedenillaNo ratings yet

- Internship Report On ESMLDocument43 pagesInternship Report On ESMLZaighum AliNo ratings yet

- Presentation On Income TaxDocument9 pagesPresentation On Income TaxUnnati GuptaNo ratings yet

- Walunj 2424Document10 pagesWalunj 2424gurpNo ratings yet

- Residence in IndiaDocument7 pagesResidence in IndiaSuryaNo ratings yet

- Income TaxesDocument4 pagesIncome TaxesHana Grace MamangunNo ratings yet

- Ram Baan - Direct Tax MAY - 23: Ca Vikram BiyaniDocument179 pagesRam Baan - Direct Tax MAY - 23: Ca Vikram Biyanigirish bhattNo ratings yet

- Facts: Petitioners: Conwi, Et - Al. vs. CTA and CIRDocument3 pagesFacts: Petitioners: Conwi, Et - Al. vs. CTA and CIRBurn-Cindy AbadNo ratings yet

- ACC 311 Sample Problem General Instructions:: ST ND RD THDocument1 pageACC 311 Sample Problem General Instructions:: ST ND RD THexquisiteNo ratings yet

- Taxation PDFDocument69 pagesTaxation PDFcpasl123No ratings yet