Download as pdf or txt

You might also like

- EduTap Finance Notes For RBI GradeB Merged (144 MB - 735 Pages) PDFDocument735 pagesEduTap Finance Notes For RBI GradeB Merged (144 MB - 735 Pages) PDFYashika Garg74% (35)

- Physical Asset Markets Vs Financial Asset MarketsDocument2 pagesPhysical Asset Markets Vs Financial Asset MarketsDame Polinio33% (3)

- Role of Financial Markets and InstitutionsDocument30 pagesRole of Financial Markets and InstitutionsĒsrar BalócNo ratings yet

- Chapter Four Financial Markets in The Financial SystemDocument66 pagesChapter Four Financial Markets in The Financial SystemMikias DegwaleNo ratings yet

- Financial MarketDocument11 pagesFinancial MarketDr. Prafulla RanjanNo ratings yet

- Presentation On Underlying Market: BY:-DHAIRYA (03) KANIKA (47) DARSHANDocument30 pagesPresentation On Underlying Market: BY:-DHAIRYA (03) KANIKA (47) DARSHANDhairyaa BhardwajNo ratings yet

- Big Picture in Focus: Ulob. Differentiate The Types of Financial MarketsDocument10 pagesBig Picture in Focus: Ulob. Differentiate The Types of Financial MarketsJohn Stephen PendonNo ratings yet

- Module 2 Financial Markets and Instruments Group 1 FM7Document23 pagesModule 2 Financial Markets and Instruments Group 1 FM7hikunanaNo ratings yet

- Underlying MarketsDocument30 pagesUnderlying MarketsDhairyaa BhardwajNo ratings yet

- Capital Market 17Document4 pagesCapital Market 17divyaNo ratings yet

- Econ-3091, Chapter 3 & 4Document76 pagesEcon-3091, Chapter 3 & 4GetnetNo ratings yet

- The Financial Market EnvironmentDocument2 pagesThe Financial Market EnvironmentAbd El-Rahman El-syeoufyNo ratings yet

- Secondary Market and Stock ExchangeDocument41 pagesSecondary Market and Stock ExchangeGurwinder SinghNo ratings yet

- Finl Markets and FinDocument24 pagesFinl Markets and FinLunaNo ratings yet

- Busu CursDocument173 pagesBusu CursAndreea Cristina DiaconuNo ratings yet

- ACC 212 Chapter 2Document23 pagesACC 212 Chapter 2Aian jay EsportunoNo ratings yet

- Financial System and MarketsDocument32 pagesFinancial System and Marketsmohamedsafwan0480No ratings yet

- Ch.2 - Financial InstitutionsDocument21 pagesCh.2 - Financial InstitutionsbodyelkasabyNo ratings yet

- Chapter 4Document10 pagesChapter 4Muhammed YismawNo ratings yet

- Money and Banking 1: Dr. Rania Ramadan MoawadDocument16 pagesMoney and Banking 1: Dr. Rania Ramadan MoawadEhab HosnyNo ratings yet

- Chapter 4Document10 pagesChapter 4Tasebe GetachewNo ratings yet

- Financial MarketsDocument34 pagesFinancial Marketsmouli poliparthiNo ratings yet

- Module 2 Part 2Document65 pagesModule 2 Part 2Shivam AroraNo ratings yet

- Answer: 1. Stock ExchangeDocument4 pagesAnswer: 1. Stock Exchangeshayn delapenaNo ratings yet

- محاضرة الفرقة الثانية نقود وبنوك برنامج الدراسات القانونية باللغة الأنجليزية ليوم ٢٦-٤-٢٠٢٠Document13 pagesمحاضرة الفرقة الثانية نقود وبنوك برنامج الدراسات القانونية باللغة الأنجليزية ليوم ٢٦-٤-٢٠٢٠Abdo NasserNo ratings yet

- Indian Financial MarketsDocument24 pagesIndian Financial MarketsNidhi BothraNo ratings yet

- Financial Markets and Institutionschap 2Document8 pagesFinancial Markets and Institutionschap 2Ini IchiiiNo ratings yet

- Corporate FinanceDocument110 pagesCorporate FinanceLuckmore ChivandireNo ratings yet

- Financial/ Securities Markets Notes: For Sebi Grade A & Rbi Grade BDocument10 pagesFinancial/ Securities Markets Notes: For Sebi Grade A & Rbi Grade BAadeesh JainNo ratings yet

- FM Group Report WordDocument6 pagesFM Group Report WordHariniNo ratings yet

- Physical Asset Markets VS Financial Asset MarketsDocument2 pagesPhysical Asset Markets VS Financial Asset MarketsDame PolinioNo ratings yet

- Gemini Solutions: AMC L0 - Session 2Document19 pagesGemini Solutions: AMC L0 - Session 2divya mittalNo ratings yet

- Financial Market DefinitionDocument9 pagesFinancial Market DefinitionMARJORIE BAMBALANNo ratings yet

- Chapter 1 Role of Financial Markets and InstitutionsDocument46 pagesChapter 1 Role of Financial Markets and InstitutionsJao FloresNo ratings yet

- FIN 6030A US2018 Course OutlineDocument34 pagesFIN 6030A US2018 Course OutlineNadya SavageNo ratings yet

- Security AnalysisDocument41 pagesSecurity Analysishadassah VillarNo ratings yet

- Gen Math Stocks and BondsDocument41 pagesGen Math Stocks and BondsDaniel VillahermosaNo ratings yet

- 2.1 To 2.6 CONCEPT & FINANCIAL MARKET STRUCTURE IN INDIA PDFDocument30 pages2.1 To 2.6 CONCEPT & FINANCIAL MARKET STRUCTURE IN INDIA PDFImran KhanNo ratings yet

- Capital Market and Money MarketDocument17 pagesCapital Market and Money MarketSwastika Singh100% (1)

- Chap 4-fmDocument89 pagesChap 4-fmYeshiwork GirmaNo ratings yet

- Chapter 1 Securities Operations and Risk ManagementDocument32 pagesChapter 1 Securities Operations and Risk ManagementMRIDUL GOELNo ratings yet

- 2c - Chapter 2 Financial ManagementDocument39 pages2c - Chapter 2 Financial ManagementIni IchiiiNo ratings yet

- Introduction and Overview of Financial Markets: Prof. Annedrei Maurizze Barcarse, MBA, CSSWBDocument23 pagesIntroduction and Overview of Financial Markets: Prof. Annedrei Maurizze Barcarse, MBA, CSSWBLance-JellyVNo ratings yet

- Module 04 Financial Markets and InstrumentsDocument13 pagesModule 04 Financial Markets and InstrumentsGovindNo ratings yet

- Group 3 Financial MarketsDocument17 pagesGroup 3 Financial MarketsLady Lou Ignacio LepasanaNo ratings yet

- Presentation On Indian Debt MarketDocument55 pagesPresentation On Indian Debt Marketpriya_12345632369100% (9)

- Week 2 - SF: Role of Financial Markets and InstitutionsDocument39 pagesWeek 2 - SF: Role of Financial Markets and Institutionsciara WhiteNo ratings yet

- Chapter 10 - Financial Markets PDFDocument4 pagesChapter 10 - Financial Markets PDFKelrina D'silvaNo ratings yet

- Fundamentals of Corporate Finance 3rd Edition by Parrino Kidwell Bates ISBN Solution ManualDocument8 pagesFundamentals of Corporate Finance 3rd Edition by Parrino Kidwell Bates ISBN Solution Manualmary100% (21)

- Capital Market Management: Dr. Marites A. AndresDocument34 pagesCapital Market Management: Dr. Marites A. AndresClarky Linguis100% (1)

- The Financial Market EnvironmentDocument18 pagesThe Financial Market Environmentlayan123456No ratings yet

- Secondary MarketDocument13 pagesSecondary MarketKanchan GuptaNo ratings yet

- Siddik Sir 1Document1 pageSiddik Sir 1Numaer SiddiqueNo ratings yet

- Market Chapter OneDocument11 pagesMarket Chapter Onehaifa.s.mansourNo ratings yet

- A Detailed Project On Secondary Market.Document40 pagesA Detailed Project On Secondary Market.Jatin Anand100% (2)

- Chap 10 Short NotesDocument10 pagesChap 10 Short Notesnimisha chaddhaNo ratings yet

- CH 1Document26 pagesCH 1Chernet TeferaNo ratings yet

- Finantial Institution by ADDocument27 pagesFinantial Institution by ADDaniyal AwanNo ratings yet

- Equity Investment for CFA level 1: CFA level 1, #2From EverandEquity Investment for CFA level 1: CFA level 1, #2Rating: 5 out of 5 stars5/5 (1)

- Detailed Lesson Plan in ABMDocument5 pagesDetailed Lesson Plan in ABMAnonymous QZsOxQsJNo ratings yet

- UNISEL Guide To Registration 2014Document21 pagesUNISEL Guide To Registration 2014IscUniselNo ratings yet

- Exam For InternsDocument24 pagesExam For InternsVishvesh SharmaNo ratings yet

- Recruitment and Selection ProcessDocument33 pagesRecruitment and Selection Processurmi_patel22No ratings yet

- Dubai Induction HandbookDocument34 pagesDubai Induction HandbookTariq Hafeez KhanNo ratings yet

- Dealership Agreement Autos AskariDocument9 pagesDealership Agreement Autos AskariFakhar QureshiNo ratings yet

- Siptu Sign Up Form 1Document2 pagesSiptu Sign Up Form 1JohnNo ratings yet

- Bali Honeymoon Winter Special 4N/5D - 4 Hotels Package Starts From 31,168Document13 pagesBali Honeymoon Winter Special 4N/5D - 4 Hotels Package Starts From 31,168Leo ThomasNo ratings yet

- Seminar On ICT Trends in Microfinance Tanzania, 18 June 2007Document9 pagesSeminar On ICT Trends in Microfinance Tanzania, 18 June 2007Eric MitegoNo ratings yet

- MCASHPOINT Know Your Customers Form-1Document1 pageMCASHPOINT Know Your Customers Form-1Sandra CristinmNo ratings yet

- RBI Discussion PaperDocument18 pagesRBI Discussion PaperRuletaNo ratings yet

- Fybca Updated First Sem SlipsDocument35 pagesFybca Updated First Sem SlipsTejuNo ratings yet

- Step-by-Step Guide To Enrolling Online: Ready To Enrol? Enrolment StepsDocument11 pagesStep-by-Step Guide To Enrolling Online: Ready To Enrol? Enrolment Stepscrescentarian77No ratings yet

- Suspicious Activity ReportDocument6 pagesSuspicious Activity Reportpenlandwatch100% (2)

- JP Morgan Latam 2011Document160 pagesJP Morgan Latam 2011Saulo SturaroNo ratings yet

- FaqDocument3 pagesFaqLek Chun CheunNo ratings yet

- 26082023-0918 Grafic RambursareDocument11 pages26082023-0918 Grafic RambursareLuiza TanaseNo ratings yet

- Meezan Bank & Fayasl Bank Product Comparison Offer To CustomersDocument21 pagesMeezan Bank & Fayasl Bank Product Comparison Offer To CustomersMuhammad Muavia Khan88% (8)

- Financial MarketsDocument94 pagesFinancial MarketsEman AhmedNo ratings yet

- Country InfoDocument12 pagesCountry InfoEko YuliantoNo ratings yet

- Deposition of Claire SwazeyDocument119 pagesDeposition of Claire SwazeySTOP RCO NOWNo ratings yet

- Trial Balance DECDocument1 pageTrial Balance DECDom CarlobosNo ratings yet

- Audit Due Diligence PackageDocument3 pagesAudit Due Diligence Packageapi-285461030No ratings yet

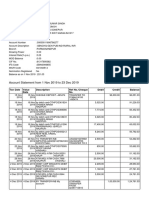

- Account Statement From 1 Nov 2019 To 23 Dec 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 1 Nov 2019 To 23 Dec 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRitesh Kumar TiwariNo ratings yet

- Ventas y Cambio Pago MovilDocument6 pagesVentas y Cambio Pago MovilusadarwsNo ratings yet

- SrishtiDocument81 pagesSrishtiKavanya SuroliaNo ratings yet

- Importance of Service Sector in Our EconomyDocument3 pagesImportance of Service Sector in Our EconomyIbe Collins100% (1)

- Koert Working Experience in China - Page 15/16Document40 pagesKoert Working Experience in China - Page 15/16koertb3167No ratings yet

- Access To Energy Services: Case StudiesDocument14 pagesAccess To Energy Services: Case StudiesmaveryqNo ratings yet