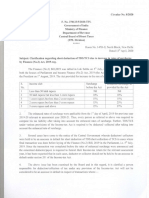

Advisory For Action Fake Itc Recipients Date 19.1.21

Advisory For Action Fake Itc Recipients Date 19.1.21

You might also like

- TEP SOP-New-23 - 09. 2016 PDFDocument10 pagesTEP SOP-New-23 - 09. 2016 PDFprakashtanwar9100% (3)

- Ceibcbic GST Investigation Instruction 2 2021 22Document5 pagesCeibcbic GST Investigation Instruction 2 2021 22KANCHIVIVEKGUPTANo ratings yet

- Page 1 of 4Document4 pagesPage 1 of 4Sunil ShahNo ratings yet

- Goods and Services TaxDocument6 pagesGoods and Services TaxbabugenuNo ratings yet

- Cir 187 19 2022 CGSTDocument3 pagesCir 187 19 2022 CGSTAtanu Kumar SenNo ratings yet

- Intouch Issue 3 2022Document21 pagesIntouch Issue 3 2022Shermadurai VNo ratings yet

- CASE DOCTRINES - 2020 Jurisprudence Updates (SC and CTA Cases)Document12 pagesCASE DOCTRINES - 2020 Jurisprudence Updates (SC and CTA Cases)Carlota VillaromanNo ratings yet

- GSSTDocument70 pagesGSSTmayankyadav.jhsNo ratings yet

- Erring in ProfiteeringDocument10 pagesErring in ProfiteeringManish SachdevaNo ratings yet

- EY Tax Alert: Executive SummaryDocument6 pagesEY Tax Alert: Executive SummaryAjay SinghNo ratings yet

- 6.case Study On Input Tax Credit Under GSTDocument17 pages6.case Study On Input Tax Credit Under GSTSUNIL PUJARINo ratings yet

- GST Update129 PDFDocument2 pagesGST Update129 PDFTharun RajNo ratings yet

- Tds Under GST Regime - Section 51 of CGST Act: Cma Utpal Kumar SahaDocument2 pagesTds Under GST Regime - Section 51 of CGST Act: Cma Utpal Kumar Sahajkmijkmi597No ratings yet

- GSTDocument40 pagesGSTsangkhawmaNo ratings yet

- Penalties Under GST: Nature of Default Penalty RemarksDocument3 pagesPenalties Under GST: Nature of Default Penalty RemarksHumanyu KabeerNo ratings yet

- Justice Teresita Leonardo-De Castro Cases (2008-2015) : TaxationDocument3 pagesJustice Teresita Leonardo-De Castro Cases (2008-2015) : TaxationNicco AcaylarNo ratings yet

- 51 Insights August 2022Document25 pages51 Insights August 2022Rheneir MoraNo ratings yet

- GST (Payment of Tax) FinalDocument6 pagesGST (Payment of Tax) FinalDARK KING GamersNo ratings yet

- CA Inter Compact Books For May 21Document216 pagesCA Inter Compact Books For May 21Rahul AgrawalNo ratings yet

- Tax Blunders ICN 3.15.12Document2 pagesTax Blunders ICN 3.15.12JianSadakoNo ratings yet

- CB LICENCE IS LIFE TIME Circular-No-17-2021-rDocument2 pagesCB LICENCE IS LIFE TIME Circular-No-17-2021-rganeshNo ratings yet

- Cir VS SonyDocument31 pagesCir VS Sonyic corNo ratings yet

- Comparative Analysis Under GST RegimeDocument5 pagesComparative Analysis Under GST RegimeAmita SinwarNo ratings yet

- Standard+Operating+Procedure+ (SOP) +for+NCLT+Cases+in+Respect+of+the+Insolvency+and+Bankruptcy+Code+ (IBC) + CBICDocument3 pagesStandard+Operating+Procedure+ (SOP) +for+NCLT+Cases+in+Respect+of+the+Insolvency+and+Bankruptcy+Code+ (IBC) + CBICKANCHIVIVEKGUPTANo ratings yet

- Upreme Ourt: 3aepublic of Tbe !) Bilippines !manilaDocument12 pagesUpreme Ourt: 3aepublic of Tbe !) Bilippines !manilaChristine Aev OlasaNo ratings yet

- Cellsons Appeal StatementDocument45 pagesCellsons Appeal Statementjenniferthanu1521No ratings yet

- GRC Minutes of Meeting 22.04.2024Document11 pagesGRC Minutes of Meeting 22.04.2024MyFinTax SolutionsNo ratings yet

- GST - Audit OffencesDocument35 pagesGST - Audit OffencesApurva DharNo ratings yet

- Talking Points GSTDocument2 pagesTalking Points GSTvikaskumar1No ratings yet

- Cbic Taxes IndiaDocument2 pagesCbic Taxes IndiaReal PlayerNo ratings yet

- Overview of GSTDocument74 pagesOverview of GSTsunil patelNo ratings yet

- Taxation Law Updates by Atty. OrtegaDocument21 pagesTaxation Law Updates by Atty. Ortegavillanueva9guapster9100% (1)

- Circular No.: Government India Department Revenue Board Direct Division)Document2 pagesCircular No.: Government India Department Revenue Board Direct Division)ashim1No ratings yet

- Instructuon No 01 2022 23 INV 1Document2 pagesInstructuon No 01 2022 23 INV 1supdtconflNo ratings yet

- Circular CGST 131 NewDocument5 pagesCircular CGST 131 NewSanjeev BorgohainNo ratings yet

- Eastern Telecom PhilsDocument14 pagesEastern Telecom Philsmadara uchihaNo ratings yet

- GST LatestAmendments Issues 01072023Document85 pagesGST LatestAmendments Issues 01072023Selvakumar MuthurajNo ratings yet

- Amendments For NOV 21: Amendment in 1 Min Series Available On InstagramDocument32 pagesAmendments For NOV 21: Amendment in 1 Min Series Available On InstagramAakriti SinghalNo ratings yet

- Tax Alert (December 2020)Document10 pagesTax Alert (December 2020)Rheneir MoraNo ratings yet

- Concept of Input Tax Credit: © Indirect Taxes Committee, ICAIDocument35 pagesConcept of Input Tax Credit: © Indirect Taxes Committee, ICAIyennamNo ratings yet

- GST Scanner by Meeta Mangal Mam PDFDocument86 pagesGST Scanner by Meeta Mangal Mam PDFRoopika Shetty100% (1)

- 2.2016 Syllabus Paper-18 - Jan21 Indirect Tax Laws & Practice Study NotesDocument972 pages2.2016 Syllabus Paper-18 - Jan21 Indirect Tax Laws & Practice Study NotesRadhakrishnaraja RameshNo ratings yet

- E - Book On Recovery of Arrears Under GST Law - Dated - 01 - 10 - 2023Document85 pagesE - Book On Recovery of Arrears Under GST Law - Dated - 01 - 10 - 2023acgstdiv4No ratings yet

- Heavy Penalties for Petty defaults in GSTDocument2 pagesHeavy Penalties for Petty defaults in GST53samsenNo ratings yet

- Do You Know GST - July 2022Document17 pagesDo You Know GST - July 2022CA Ranjan MehtaNo ratings yet

- GST Case Study-3Document6 pagesGST Case Study-3babugenuNo ratings yet

- 18 GSTDocument1,042 pages18 GSTSwetaNo ratings yet

- Final New Indirect Tax Laws Test 3 Detailed May Solution 1617180255Document17 pagesFinal New Indirect Tax Laws Test 3 Detailed May Solution 1617180255CAtestseriesNo ratings yet

- SOP For Tackling Fake InvoiceDocument7 pagesSOP For Tackling Fake InvoiceTHABIRA BAGNo ratings yet

- Tmap - Updates (August September 2017) PDFDocument12 pagesTmap - Updates (August September 2017) PDFAko Si Paula MonghitNo ratings yet

- Cajournal May2021 24Document4 pagesCajournal May2021 24S M SHEKARNo ratings yet

- Input Tax Credit: Speaker: Sudhir V SDocument31 pagesInput Tax Credit: Speaker: Sudhir V Smahi_kunkuNo ratings yet

- CIR v. MirantDocument11 pagesCIR v. MirantLorenz Vergil ReyesNo ratings yet

- TAXREV D2019 Reviewer Transcript PDFDocument193 pagesTAXREV D2019 Reviewer Transcript PDFAleezah Gertrude Raymundo100% (1)

- Instruction No. 2/1/2020-GST: Y.garg@nic - inDocument1 pageInstruction No. 2/1/2020-GST: Y.garg@nic - inGuru CharanNo ratings yet

- I Phone X 256 GB (Space Grey)Document2 pagesI Phone X 256 GB (Space Grey)Omdatt KatariaNo ratings yet

- Refund of Unutilised ItcDocument6 pagesRefund of Unutilised ItcgrameshchandraNo ratings yet

- Mismatch in Tax Liabilities-No Longer A Factual ConcernDocument4 pagesMismatch in Tax Liabilities-No Longer A Factual ConcernKunwarbir Singh lohatNo ratings yet

- Interest Sec 50 GSTPWDocument2 pagesInterest Sec 50 GSTPWaekurnoolNo ratings yet

- People vs. JalosjosDocument7 pagesPeople vs. JalosjosBabes Aubrey DelaCruz AquinoNo ratings yet

- Notice: Republic of The Philippines Supreme CourtDocument11 pagesNotice: Republic of The Philippines Supreme CourtPhilip JameroNo ratings yet

- Show TempDocument24 pagesShow TempLydian CoombsNo ratings yet

- 2Document5 pages2VOJNo ratings yet

- Casus Omissus - A Thing Omitted Must Be Considered To Have Been Omitted Intentionally. Therefore, With TheDocument3 pagesCasus Omissus - A Thing Omitted Must Be Considered To Have Been Omitted Intentionally. Therefore, With TheMaria Angela GasparNo ratings yet

- People Vs Dela RosaDocument24 pagesPeople Vs Dela RosaShane Fernandez JardinicoNo ratings yet

- PRESENTATION Identification Parade (Aman Ullah Khan ADJ-I)Document61 pagesPRESENTATION Identification Parade (Aman Ullah Khan ADJ-I)Rana Shaukat AliNo ratings yet

- People V CepedaDocument7 pagesPeople V CepedaNikki Estores GonzalesNo ratings yet

- ArsonDocument53 pagesArsonIrish Martinez100% (5)

- By Kavita Singh Associate Professor Nliu: MediationDocument24 pagesBy Kavita Singh Associate Professor Nliu: MediationAkshay SarjanNo ratings yet

- Booking 03 11Document2 pagesBooking 03 11Bryan FitzgeraldNo ratings yet

- Directory and Peremptory ProvisionsDocument13 pagesDirectory and Peremptory ProvisionsEntleNo ratings yet

- Constitution of India - Wikipedia, The Free EncyclopediaDocument14 pagesConstitution of India - Wikipedia, The Free EncyclopediaJayesh RathodNo ratings yet

- Indian Penal Code: Sudhir Ch. Biswas Vs The StateDocument13 pagesIndian Penal Code: Sudhir Ch. Biswas Vs The StateLovely Kumar SapraNo ratings yet

- MIDTERSMLEGPROFDocument23 pagesMIDTERSMLEGPROFOldAccountof Ed ThereseNo ratings yet

- 16 Firestone Ceramics Vs Court of AppealsDocument3 pages16 Firestone Ceramics Vs Court of AppealsPao InfanteNo ratings yet

- Procedure and Professional EthicsDocument392 pagesProcedure and Professional EthicsNoliNo ratings yet

- Metropolitan Bank Vs ReynaldoDocument11 pagesMetropolitan Bank Vs ReynaldoRelmie TaasanNo ratings yet

- Plaintiff-Appellee Vs Vs Accused-Appellant The Solicitor General Public Attorney's OfficeDocument15 pagesPlaintiff-Appellee Vs Vs Accused-Appellant The Solicitor General Public Attorney's OfficeVener MargalloNo ratings yet

- Soquillo v. TortollaDocument13 pagesSoquillo v. TortollaLaura MangantulaoNo ratings yet

- PAO - Legal FormsDocument171 pagesPAO - Legal FormsBianca Rodriguez100% (1)

- United States v. Angel Cerceda, United States of America v. Courtney Ricardo Alford, A.K.A. "Rickey," Edward Bernard Williams, A.K.A. "Bernard," Nathaniel Dean, United States of America v. Hector Fernandez-Dominguez, United States of America v. Jesus E. Cardona, United States of America v. Carlos Hernandez, United States of America v. Adolfo Mestril, A.K.A. "El Gordo," Jose Herminio Benitez, A.K.A. "William Muniz," A.K.A "Emilio," Heriberto Alvarez, Elpidio, Pedro Iglesias-Cruz, A.K.A. "Budweiser," United States of America v. Minnie Ruth Williams, Ralph W. Corker, United States of America v. Hiram Martinez, Jr., United States of America v. Diogenes Palacios, United States of America v. Fred De La Mata, Manuel A. Calas, Oscar Castilla and Enrique Fernandez, United States of America v. Steven Johnson, United States of America v. Francisco Jose Arias, Gustavo Javier Pirela-Avila, United States of America v. Enrique Acosta, Milciades Jiminez, United States of America v. Carlos A. Zapata, UDocument5 pagesUnited States v. Angel Cerceda, United States of America v. Courtney Ricardo Alford, A.K.A. "Rickey," Edward Bernard Williams, A.K.A. "Bernard," Nathaniel Dean, United States of America v. Hector Fernandez-Dominguez, United States of America v. Jesus E. Cardona, United States of America v. Carlos Hernandez, United States of America v. Adolfo Mestril, A.K.A. "El Gordo," Jose Herminio Benitez, A.K.A. "William Muniz," A.K.A "Emilio," Heriberto Alvarez, Elpidio, Pedro Iglesias-Cruz, A.K.A. "Budweiser," United States of America v. Minnie Ruth Williams, Ralph W. Corker, United States of America v. Hiram Martinez, Jr., United States of America v. Diogenes Palacios, United States of America v. Fred De La Mata, Manuel A. Calas, Oscar Castilla and Enrique Fernandez, United States of America v. Steven Johnson, United States of America v. Francisco Jose Arias, Gustavo Javier Pirela-Avila, United States of America v. Enrique Acosta, Milciades Jiminez, United States of America v. Carlos A. Zapata, UScribd Government DocsNo ratings yet

- Douglas Thames Arrest WarrantDocument25 pagesDouglas Thames Arrest WarrantMichael_Lee_RobertsNo ratings yet

- G.R. No. 173858 July 17, 2007Document2 pagesG.R. No. 173858 July 17, 2007TimNo ratings yet

- Judicial Review Vs Judicial Activism: A Project Submitted ToDocument13 pagesJudicial Review Vs Judicial Activism: A Project Submitted TokingNo ratings yet

- CIT v. Vegetable Products Ltd.Document4 pagesCIT v. Vegetable Products Ltd.Karsin ManochaNo ratings yet

- Appeal CR PC Additionla Notes 26.09.2022Document6 pagesAppeal CR PC Additionla Notes 26.09.2022Garvish DosiNo ratings yet

- Kho vs. Republic, G.R. No. 187462, June 1, 2016 - AdditionalDocument4 pagesKho vs. Republic, G.R. No. 187462, June 1, 2016 - AdditionalFrancise Mae Montilla MordenoNo ratings yet

- Res JudicataDocument8 pagesRes JudicataPranav GhabrooNo ratings yet

- Case 125,127&132Document6 pagesCase 125,127&132Davenry AtgabNo ratings yet

Download as pdf or txt

You might also like

- TEP SOP-New-23 - 09. 2016 PDFDocument10 pagesTEP SOP-New-23 - 09. 2016 PDFprakashtanwar9100% (3)

- Ceibcbic GST Investigation Instruction 2 2021 22Document5 pagesCeibcbic GST Investigation Instruction 2 2021 22KANCHIVIVEKGUPTANo ratings yet

- Page 1 of 4Document4 pagesPage 1 of 4Sunil ShahNo ratings yet

- Goods and Services TaxDocument6 pagesGoods and Services TaxbabugenuNo ratings yet

- Cir 187 19 2022 CGSTDocument3 pagesCir 187 19 2022 CGSTAtanu Kumar SenNo ratings yet

- Intouch Issue 3 2022Document21 pagesIntouch Issue 3 2022Shermadurai VNo ratings yet

- CASE DOCTRINES - 2020 Jurisprudence Updates (SC and CTA Cases)Document12 pagesCASE DOCTRINES - 2020 Jurisprudence Updates (SC and CTA Cases)Carlota VillaromanNo ratings yet

- GSSTDocument70 pagesGSSTmayankyadav.jhsNo ratings yet

- Erring in ProfiteeringDocument10 pagesErring in ProfiteeringManish SachdevaNo ratings yet

- EY Tax Alert: Executive SummaryDocument6 pagesEY Tax Alert: Executive SummaryAjay SinghNo ratings yet

- 6.case Study On Input Tax Credit Under GSTDocument17 pages6.case Study On Input Tax Credit Under GSTSUNIL PUJARINo ratings yet

- GST Update129 PDFDocument2 pagesGST Update129 PDFTharun RajNo ratings yet

- Tds Under GST Regime - Section 51 of CGST Act: Cma Utpal Kumar SahaDocument2 pagesTds Under GST Regime - Section 51 of CGST Act: Cma Utpal Kumar Sahajkmijkmi597No ratings yet

- GSTDocument40 pagesGSTsangkhawmaNo ratings yet

- Penalties Under GST: Nature of Default Penalty RemarksDocument3 pagesPenalties Under GST: Nature of Default Penalty RemarksHumanyu KabeerNo ratings yet

- Justice Teresita Leonardo-De Castro Cases (2008-2015) : TaxationDocument3 pagesJustice Teresita Leonardo-De Castro Cases (2008-2015) : TaxationNicco AcaylarNo ratings yet

- 51 Insights August 2022Document25 pages51 Insights August 2022Rheneir MoraNo ratings yet

- GST (Payment of Tax) FinalDocument6 pagesGST (Payment of Tax) FinalDARK KING GamersNo ratings yet

- CA Inter Compact Books For May 21Document216 pagesCA Inter Compact Books For May 21Rahul AgrawalNo ratings yet

- Tax Blunders ICN 3.15.12Document2 pagesTax Blunders ICN 3.15.12JianSadakoNo ratings yet

- CB LICENCE IS LIFE TIME Circular-No-17-2021-rDocument2 pagesCB LICENCE IS LIFE TIME Circular-No-17-2021-rganeshNo ratings yet

- Cir VS SonyDocument31 pagesCir VS Sonyic corNo ratings yet

- Comparative Analysis Under GST RegimeDocument5 pagesComparative Analysis Under GST RegimeAmita SinwarNo ratings yet

- Standard+Operating+Procedure+ (SOP) +for+NCLT+Cases+in+Respect+of+the+Insolvency+and+Bankruptcy+Code+ (IBC) + CBICDocument3 pagesStandard+Operating+Procedure+ (SOP) +for+NCLT+Cases+in+Respect+of+the+Insolvency+and+Bankruptcy+Code+ (IBC) + CBICKANCHIVIVEKGUPTANo ratings yet

- Upreme Ourt: 3aepublic of Tbe !) Bilippines !manilaDocument12 pagesUpreme Ourt: 3aepublic of Tbe !) Bilippines !manilaChristine Aev OlasaNo ratings yet

- Cellsons Appeal StatementDocument45 pagesCellsons Appeal Statementjenniferthanu1521No ratings yet

- GRC Minutes of Meeting 22.04.2024Document11 pagesGRC Minutes of Meeting 22.04.2024MyFinTax SolutionsNo ratings yet

- GST - Audit OffencesDocument35 pagesGST - Audit OffencesApurva DharNo ratings yet

- Talking Points GSTDocument2 pagesTalking Points GSTvikaskumar1No ratings yet

- Cbic Taxes IndiaDocument2 pagesCbic Taxes IndiaReal PlayerNo ratings yet

- Overview of GSTDocument74 pagesOverview of GSTsunil patelNo ratings yet

- Taxation Law Updates by Atty. OrtegaDocument21 pagesTaxation Law Updates by Atty. Ortegavillanueva9guapster9100% (1)

- Circular No.: Government India Department Revenue Board Direct Division)Document2 pagesCircular No.: Government India Department Revenue Board Direct Division)ashim1No ratings yet

- Instructuon No 01 2022 23 INV 1Document2 pagesInstructuon No 01 2022 23 INV 1supdtconflNo ratings yet

- Circular CGST 131 NewDocument5 pagesCircular CGST 131 NewSanjeev BorgohainNo ratings yet

- Eastern Telecom PhilsDocument14 pagesEastern Telecom Philsmadara uchihaNo ratings yet

- GST LatestAmendments Issues 01072023Document85 pagesGST LatestAmendments Issues 01072023Selvakumar MuthurajNo ratings yet

- Amendments For NOV 21: Amendment in 1 Min Series Available On InstagramDocument32 pagesAmendments For NOV 21: Amendment in 1 Min Series Available On InstagramAakriti SinghalNo ratings yet

- Tax Alert (December 2020)Document10 pagesTax Alert (December 2020)Rheneir MoraNo ratings yet

- Concept of Input Tax Credit: © Indirect Taxes Committee, ICAIDocument35 pagesConcept of Input Tax Credit: © Indirect Taxes Committee, ICAIyennamNo ratings yet

- GST Scanner by Meeta Mangal Mam PDFDocument86 pagesGST Scanner by Meeta Mangal Mam PDFRoopika Shetty100% (1)

- 2.2016 Syllabus Paper-18 - Jan21 Indirect Tax Laws & Practice Study NotesDocument972 pages2.2016 Syllabus Paper-18 - Jan21 Indirect Tax Laws & Practice Study NotesRadhakrishnaraja RameshNo ratings yet

- E - Book On Recovery of Arrears Under GST Law - Dated - 01 - 10 - 2023Document85 pagesE - Book On Recovery of Arrears Under GST Law - Dated - 01 - 10 - 2023acgstdiv4No ratings yet

- Heavy Penalties for Petty defaults in GSTDocument2 pagesHeavy Penalties for Petty defaults in GST53samsenNo ratings yet

- Do You Know GST - July 2022Document17 pagesDo You Know GST - July 2022CA Ranjan MehtaNo ratings yet

- GST Case Study-3Document6 pagesGST Case Study-3babugenuNo ratings yet

- 18 GSTDocument1,042 pages18 GSTSwetaNo ratings yet

- Final New Indirect Tax Laws Test 3 Detailed May Solution 1617180255Document17 pagesFinal New Indirect Tax Laws Test 3 Detailed May Solution 1617180255CAtestseriesNo ratings yet

- SOP For Tackling Fake InvoiceDocument7 pagesSOP For Tackling Fake InvoiceTHABIRA BAGNo ratings yet

- Tmap - Updates (August September 2017) PDFDocument12 pagesTmap - Updates (August September 2017) PDFAko Si Paula MonghitNo ratings yet

- Cajournal May2021 24Document4 pagesCajournal May2021 24S M SHEKARNo ratings yet

- Input Tax Credit: Speaker: Sudhir V SDocument31 pagesInput Tax Credit: Speaker: Sudhir V Smahi_kunkuNo ratings yet

- CIR v. MirantDocument11 pagesCIR v. MirantLorenz Vergil ReyesNo ratings yet

- TAXREV D2019 Reviewer Transcript PDFDocument193 pagesTAXREV D2019 Reviewer Transcript PDFAleezah Gertrude Raymundo100% (1)

- Instruction No. 2/1/2020-GST: Y.garg@nic - inDocument1 pageInstruction No. 2/1/2020-GST: Y.garg@nic - inGuru CharanNo ratings yet

- I Phone X 256 GB (Space Grey)Document2 pagesI Phone X 256 GB (Space Grey)Omdatt KatariaNo ratings yet

- Refund of Unutilised ItcDocument6 pagesRefund of Unutilised ItcgrameshchandraNo ratings yet

- Mismatch in Tax Liabilities-No Longer A Factual ConcernDocument4 pagesMismatch in Tax Liabilities-No Longer A Factual ConcernKunwarbir Singh lohatNo ratings yet

- Interest Sec 50 GSTPWDocument2 pagesInterest Sec 50 GSTPWaekurnoolNo ratings yet

- People vs. JalosjosDocument7 pagesPeople vs. JalosjosBabes Aubrey DelaCruz AquinoNo ratings yet

- Notice: Republic of The Philippines Supreme CourtDocument11 pagesNotice: Republic of The Philippines Supreme CourtPhilip JameroNo ratings yet

- Show TempDocument24 pagesShow TempLydian CoombsNo ratings yet

- 2Document5 pages2VOJNo ratings yet

- Casus Omissus - A Thing Omitted Must Be Considered To Have Been Omitted Intentionally. Therefore, With TheDocument3 pagesCasus Omissus - A Thing Omitted Must Be Considered To Have Been Omitted Intentionally. Therefore, With TheMaria Angela GasparNo ratings yet

- People Vs Dela RosaDocument24 pagesPeople Vs Dela RosaShane Fernandez JardinicoNo ratings yet

- PRESENTATION Identification Parade (Aman Ullah Khan ADJ-I)Document61 pagesPRESENTATION Identification Parade (Aman Ullah Khan ADJ-I)Rana Shaukat AliNo ratings yet

- People V CepedaDocument7 pagesPeople V CepedaNikki Estores GonzalesNo ratings yet

- ArsonDocument53 pagesArsonIrish Martinez100% (5)

- By Kavita Singh Associate Professor Nliu: MediationDocument24 pagesBy Kavita Singh Associate Professor Nliu: MediationAkshay SarjanNo ratings yet

- Booking 03 11Document2 pagesBooking 03 11Bryan FitzgeraldNo ratings yet

- Directory and Peremptory ProvisionsDocument13 pagesDirectory and Peremptory ProvisionsEntleNo ratings yet

- Constitution of India - Wikipedia, The Free EncyclopediaDocument14 pagesConstitution of India - Wikipedia, The Free EncyclopediaJayesh RathodNo ratings yet

- Indian Penal Code: Sudhir Ch. Biswas Vs The StateDocument13 pagesIndian Penal Code: Sudhir Ch. Biswas Vs The StateLovely Kumar SapraNo ratings yet

- MIDTERSMLEGPROFDocument23 pagesMIDTERSMLEGPROFOldAccountof Ed ThereseNo ratings yet

- 16 Firestone Ceramics Vs Court of AppealsDocument3 pages16 Firestone Ceramics Vs Court of AppealsPao InfanteNo ratings yet

- Procedure and Professional EthicsDocument392 pagesProcedure and Professional EthicsNoliNo ratings yet

- Metropolitan Bank Vs ReynaldoDocument11 pagesMetropolitan Bank Vs ReynaldoRelmie TaasanNo ratings yet

- Plaintiff-Appellee Vs Vs Accused-Appellant The Solicitor General Public Attorney's OfficeDocument15 pagesPlaintiff-Appellee Vs Vs Accused-Appellant The Solicitor General Public Attorney's OfficeVener MargalloNo ratings yet

- Soquillo v. TortollaDocument13 pagesSoquillo v. TortollaLaura MangantulaoNo ratings yet

- PAO - Legal FormsDocument171 pagesPAO - Legal FormsBianca Rodriguez100% (1)

- United States v. Angel Cerceda, United States of America v. Courtney Ricardo Alford, A.K.A. "Rickey," Edward Bernard Williams, A.K.A. "Bernard," Nathaniel Dean, United States of America v. Hector Fernandez-Dominguez, United States of America v. Jesus E. Cardona, United States of America v. Carlos Hernandez, United States of America v. Adolfo Mestril, A.K.A. "El Gordo," Jose Herminio Benitez, A.K.A. "William Muniz," A.K.A "Emilio," Heriberto Alvarez, Elpidio, Pedro Iglesias-Cruz, A.K.A. "Budweiser," United States of America v. Minnie Ruth Williams, Ralph W. Corker, United States of America v. Hiram Martinez, Jr., United States of America v. Diogenes Palacios, United States of America v. Fred De La Mata, Manuel A. Calas, Oscar Castilla and Enrique Fernandez, United States of America v. Steven Johnson, United States of America v. Francisco Jose Arias, Gustavo Javier Pirela-Avila, United States of America v. Enrique Acosta, Milciades Jiminez, United States of America v. Carlos A. Zapata, UDocument5 pagesUnited States v. Angel Cerceda, United States of America v. Courtney Ricardo Alford, A.K.A. "Rickey," Edward Bernard Williams, A.K.A. "Bernard," Nathaniel Dean, United States of America v. Hector Fernandez-Dominguez, United States of America v. Jesus E. Cardona, United States of America v. Carlos Hernandez, United States of America v. Adolfo Mestril, A.K.A. "El Gordo," Jose Herminio Benitez, A.K.A. "William Muniz," A.K.A "Emilio," Heriberto Alvarez, Elpidio, Pedro Iglesias-Cruz, A.K.A. "Budweiser," United States of America v. Minnie Ruth Williams, Ralph W. Corker, United States of America v. Hiram Martinez, Jr., United States of America v. Diogenes Palacios, United States of America v. Fred De La Mata, Manuel A. Calas, Oscar Castilla and Enrique Fernandez, United States of America v. Steven Johnson, United States of America v. Francisco Jose Arias, Gustavo Javier Pirela-Avila, United States of America v. Enrique Acosta, Milciades Jiminez, United States of America v. Carlos A. Zapata, UScribd Government DocsNo ratings yet

- Douglas Thames Arrest WarrantDocument25 pagesDouglas Thames Arrest WarrantMichael_Lee_RobertsNo ratings yet

- G.R. No. 173858 July 17, 2007Document2 pagesG.R. No. 173858 July 17, 2007TimNo ratings yet

- Judicial Review Vs Judicial Activism: A Project Submitted ToDocument13 pagesJudicial Review Vs Judicial Activism: A Project Submitted TokingNo ratings yet

- CIT v. Vegetable Products Ltd.Document4 pagesCIT v. Vegetable Products Ltd.Karsin ManochaNo ratings yet

- Appeal CR PC Additionla Notes 26.09.2022Document6 pagesAppeal CR PC Additionla Notes 26.09.2022Garvish DosiNo ratings yet

- Kho vs. Republic, G.R. No. 187462, June 1, 2016 - AdditionalDocument4 pagesKho vs. Republic, G.R. No. 187462, June 1, 2016 - AdditionalFrancise Mae Montilla MordenoNo ratings yet

- Res JudicataDocument8 pagesRes JudicataPranav GhabrooNo ratings yet

- Case 125,127&132Document6 pagesCase 125,127&132Davenry AtgabNo ratings yet