Download as pdf or txt

You might also like

- Chapter 5 Fkli Speculating Spreading and Arbitraging AnswersDocument6 pagesChapter 5 Fkli Speculating Spreading and Arbitraging AnswersWan Nur FatihahNo ratings yet

- Identify The Industry Analysis of Financial Statement DataDocument3 pagesIdentify The Industry Analysis of Financial Statement DataJIAXUAN WANGNo ratings yet

- Solution: P8 / (P96.50 - P2.38) 8.5%Document4 pagesSolution: P8 / (P96.50 - P2.38) 8.5%Edrielle100% (1)

- Learning MaterialsDocument38 pagesLearning MaterialsBrithney ButalidNo ratings yet

- A Study On Investors Behaviour in Stock MarketDocument5 pagesA Study On Investors Behaviour in Stock Marketaparna_sajeev0% (1)

- La Opala RGDocument19 pagesLa Opala RGrahulmkguptaNo ratings yet

- APL Apollo Initial (Ambit)Document37 pagesAPL Apollo Initial (Ambit)beza manojNo ratings yet

- Sterlite Technologies - Q4'10 Result Update - (23!04!2010)Document3 pagesSterlite Technologies - Q4'10 Result Update - (23!04!2010)kotler_2006No ratings yet

- Larsen & Toubro: On TrackDocument9 pagesLarsen & Toubro: On TrackalparathiNo ratings yet

- 2021-11-09-SWIR - OQ-RBC Capital Markets-Normalizing Following Manufacturing Disruptions-94496714Document14 pages2021-11-09-SWIR - OQ-RBC Capital Markets-Normalizing Following Manufacturing Disruptions-94496714andrewNo ratings yet

- Tins 060831Document2 pagesTins 060831Cristiano DonzaghiNo ratings yet

- Metrod-2QFY10 - 20100818 - Still Falling HardDocument5 pagesMetrod-2QFY10 - 20100818 - Still Falling Hardlimml63No ratings yet

- Wa0007.Document19 pagesWa0007.Anu SinghNo ratings yet

- Hindalco Industries: IndiaDocument8 pagesHindalco Industries: IndiaAshokNo ratings yet

- Daily Agri Report 27 Nov 2018 by Epic ResearchDocument6 pagesDaily Agri Report 27 Nov 2018 by Epic Researchepicresearch392No ratings yet

- Sterlite Industries: Management Meet NoteDocument5 pagesSterlite Industries: Management Meet NotemittleNo ratings yet

- Bartronics Update 16 Oct. 2009Document7 pagesBartronics Update 16 Oct. 2009achopra14No ratings yet

- Sterlite Industries: Worst Seems To Be Priced inDocument3 pagesSterlite Industries: Worst Seems To Be Priced inramanathanseshaNo ratings yet

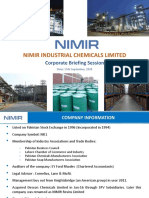

- Nimir Industrial Chemicals Limited: Corporate Briefing SessionDocument14 pagesNimir Industrial Chemicals Limited: Corporate Briefing SessionIlyas FaizNo ratings yet

- Business Standard HD Mumbai 13 01 2024Document22 pagesBusiness Standard HD Mumbai 13 01 2024Ttma TtmaNo ratings yet

- Ir PresentationDocument24 pagesIr PresentationAhmad YaniNo ratings yet

- Sterlite Ind IciciD 270110Document51 pagesSterlite Ind IciciD 270110priya3112No ratings yet

- Tokyo Visit: 16-18 February, 2011Document23 pagesTokyo Visit: 16-18 February, 2011tabhsinghiNo ratings yet

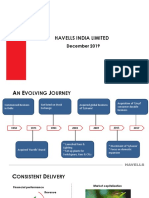

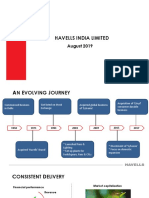

- Havells India Limited: December 2019Document25 pagesHavells India Limited: December 2019Bhushan ShendeNo ratings yet

- Company Research 20091014162453Document14 pagesCompany Research 20091014162453ranjith_999No ratings yet

- Earnings To Provide A Reality Check Sell: Reliance IndustriesDocument33 pagesEarnings To Provide A Reality Check Sell: Reliance IndustriesChetankumar ChandakNo ratings yet

- FMCG Sales: Rural India Pulls Ahead: India Inc May Report Highly Profitable Q4Document16 pagesFMCG Sales: Rural India Pulls Ahead: India Inc May Report Highly Profitable Q4Suniti ThapaNo ratings yet

- Havells India Limited Feb 2019Document25 pagesHavells India Limited Feb 2019subashreeNo ratings yet

- Havells India Limited April 2023Document35 pagesHavells India Limited April 2023shivangi.singhalNo ratings yet

- Group Project 2 Sabry Zamato SolutionDocument5 pagesGroup Project 2 Sabry Zamato SolutionSyafahani SafieNo ratings yet

- BS Bengaluru 30-01-2024Document20 pagesBS Bengaluru 30-01-2024srashmiiiscNo ratings yet

- Tatirosc 20100830Document2 pagesTatirosc 20100830sunnysmvduNo ratings yet

- Project Blue Nile - Take Home ONe TEmplate PDFDocument2 pagesProject Blue Nile - Take Home ONe TEmplate PDFYogesh PanwarNo ratings yet

- Market Update 10th July 2018Document1 pageMarket Update 10th July 2018Anonymous iFZbkNwNo ratings yet

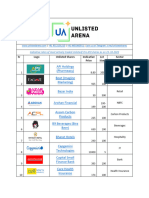

- Unlisted Arena Price List 23-10-2023Document5 pagesUnlisted Arena Price List 23-10-2023shammore97No ratings yet

- Havells India Limited: August 2019Document25 pagesHavells India Limited: August 2019srishti sharma.ayush1995No ratings yet

- Extended Quarantine Period Leads To Losses: Bloomberry Resorts CorporationDocument7 pagesExtended Quarantine Period Leads To Losses: Bloomberry Resorts CorporationJajahinaNo ratings yet

- Axiata Dialog 3Q09 ResultDocument6 pagesAxiata Dialog 3Q09 ResultseanreportsNo ratings yet

- Auto Nov20 Volume Preview - 271120 - OthersDocument9 pagesAuto Nov20 Volume Preview - 271120 - OthersRig MalikNo ratings yet

- Amara Raja Batteries: Telecoms Business Still Weak Maintaining A SellDocument6 pagesAmara Raja Batteries: Telecoms Business Still Weak Maintaining A Sellrishab agarwalNo ratings yet

- La Opala ICDocument45 pagesLa Opala ICdnsgeminiNo ratings yet

- FastrackDocument18 pagesFastrackAnkur AroraNo ratings yet

- Jara Strategy 031210Document2 pagesJara Strategy 031210shrideeppatelNo ratings yet

- HPCL Uttarakhand H2 25.11.18 PDFDocument15 pagesHPCL Uttarakhand H2 25.11.18 PDFAbhay MalikNo ratings yet

- Tata Steel - Q3FY17 Result Update - Centrum 07022017Document7 pagesTata Steel - Q3FY17 Result Update - Centrum 07022017Sreenivasulu E NNo ratings yet

- Independent Expert ReportDocument28 pagesIndependent Expert Reportandikaning prangNo ratings yet

- TWO-MUTIARA 180 23oct2019Document3 pagesTWO-MUTIARA 180 23oct2019Mohd NorsyamimNo ratings yet

- 2009 PDFDocument8 pages2009 PDFMax PascucciNo ratings yet

- Primark PresentationDocument5 pagesPrimark PresentationFernando ChávarriNo ratings yet

- P91 March District MTG Zone PresentationDocument7 pagesP91 March District MTG Zone PresentationNikki ANo ratings yet

- Highnoon Nov 26Document3 pagesHighnoon Nov 26SITU2412No ratings yet

- Price List TPDDL 5 STAR AC SchemeDocument3 pagesPrice List TPDDL 5 STAR AC SchemedragondostNo ratings yet

- Case Harsh Electrics MADocument4 pagesCase Harsh Electrics MAAbhishek PathakNo ratings yet

- For StudentsDocument97 pagesFor StudentsPravish KhareNo ratings yet

- Initiation - Comment Seadrill Limited: Initiating Coverage of SeadrillDocument25 pagesInitiation - Comment Seadrill Limited: Initiating Coverage of SeadrillocrandallNo ratings yet

- Eicher Inflation AuroPharma GAIL AshokLey TransCorp CenturyPly BoBCap PDFDocument12 pagesEicher Inflation AuroPharma GAIL AshokLey TransCorp CenturyPly BoBCap PDFKiran KudtarkarNo ratings yet

- Case Sales DistributionDocument26 pagesCase Sales Distributionalithasni45No ratings yet

- BHEL - Rock Solid - RBS - Jan2011Document8 pagesBHEL - Rock Solid - RBS - Jan2011Jitender KumarNo ratings yet

- Amverton Berhad: UnderperformDocument5 pagesAmverton Berhad: UnderperformZhi Ming CheahNo ratings yet

- Design 2 CH 2Document14 pagesDesign 2 CH 2thankikalpeshNo ratings yet

- Stock Decoder - Skipper Ltd-202402261647087215913Document1 pageStock Decoder - Skipper Ltd-202402261647087215913patelankurrhpmNo ratings yet

- Northern Region 2010-11Document2 pagesNorthern Region 2010-11btimanaNo ratings yet

- APL Apollo Tubes: Piping Gains Rating: BuyDocument28 pagesAPL Apollo Tubes: Piping Gains Rating: BuygnanaNo ratings yet

- Earnings Presentation Q1FY22Document13 pagesEarnings Presentation Q1FY22Bhav Bhagwan HaiNo ratings yet

- Earnings Presentation Q4 FY22 Jan - Mar 2022Document24 pagesEarnings Presentation Q4 FY22 Jan - Mar 2022Bhav Bhagwan HaiNo ratings yet

- Earnings-Call-Transcript Q3FY22Document17 pagesEarnings-Call-Transcript Q3FY22Bhav Bhagwan HaiNo ratings yet

- Earnings Call Transcript Q2 FY 22Document16 pagesEarnings Call Transcript Q2 FY 22Bhav Bhagwan HaiNo ratings yet

- IIFL - D-Mart - FY22 AR Analysis - 20220727Document15 pagesIIFL - D-Mart - FY22 AR Analysis - 20220727Bhav Bhagwan HaiNo ratings yet

- Motilal Oswal Financial Services2Document9 pagesMotilal Oswal Financial Services2Bhav Bhagwan HaiNo ratings yet

- Motilal Oswal Financial ServicesDocument9 pagesMotilal Oswal Financial ServicesBhav Bhagwan HaiNo ratings yet

- Investment Club PresentationDocument17 pagesInvestment Club PresentationMatthew SchifferNo ratings yet

- Adventity Valuation DCF AnalysisDocument22 pagesAdventity Valuation DCF Analysisw_fibNo ratings yet

- Investment LawDocument22 pagesInvestment Lawmee myyNo ratings yet

- Goat RaisingDocument23 pagesGoat RaisingDian Jean Cosare GanoyNo ratings yet

- Cost of Capital ppt-157233Document20 pagesCost of Capital ppt-157233kuldipNo ratings yet

- HDFC Fact SheetDocument1 pageHDFC Fact SheetAdityaNo ratings yet

- Cost of Capital - The Effect To The Firm Value and Profitability Empirical Evidences in Case of Personal Goods (Textile) Sector of KSE 100 IndexDocument7 pagesCost of Capital - The Effect To The Firm Value and Profitability Empirical Evidences in Case of Personal Goods (Textile) Sector of KSE 100 IndexKanganFatimaNo ratings yet

- TechnopreneurshipDocument3 pagesTechnopreneurshiporacion.rovjaphethNo ratings yet

- Western Telecommunication CashflowDocument3 pagesWestern Telecommunication CashflowKanishka KartikeyaNo ratings yet

- 19BBL110 Final Research Project LCFDocument19 pages19BBL110 Final Research Project LCFShubham TejasNo ratings yet

- Capital Structure TheoriesDocument26 pagesCapital Structure TheoriesSudipta BanerjeeNo ratings yet

- Financial Management EssayDocument7 pagesFinancial Management EssayQuỳnh Anh NguyễnNo ratings yet

- Teaching Suggestions Revised 22222Document54 pagesTeaching Suggestions Revised 22222Chaudhry KhurramNo ratings yet

- Zarai Taraqiati Bank Limited Consolidated Statement of Financial Position As at December 31, 2015 Note 2015 2014 Rupees in '000 AssetsDocument5 pagesZarai Taraqiati Bank Limited Consolidated Statement of Financial Position As at December 31, 2015 Note 2015 2014 Rupees in '000 AssetsFaisal AwanNo ratings yet

- Name: Curie Falentina Pandiangan Class: International MBA - 10 NIM: 20/465214/PEK/26217 Financial Management AssignmentsDocument4 pagesName: Curie Falentina Pandiangan Class: International MBA - 10 NIM: 20/465214/PEK/26217 Financial Management AssignmentsDuren JayaNo ratings yet

- 2023 Project Destined Week 3 FinalDocument18 pages2023 Project Destined Week 3 FinalSaul VillarrealNo ratings yet

- Trading-the-Majors Ebook EN PDFDocument46 pagesTrading-the-Majors Ebook EN PDFaiaiyayaNo ratings yet

- MC 0202Document16 pagesMC 0202mcchronicleNo ratings yet

- Start Up Costs CalculatorDocument5 pagesStart Up Costs CalculatorSmita KumarNo ratings yet

- De La Cuesta, de Las Alas and Callanta Law Offices For Petitioners. The Solicitor General For RespondentsDocument27 pagesDe La Cuesta, de Las Alas and Callanta Law Offices For Petitioners. The Solicitor General For RespondentsAmber QuiñonesNo ratings yet

- Arwana Citramulia TBK.: Company Report: January 2019 As of 31 January 2019Document3 pagesArwana Citramulia TBK.: Company Report: January 2019 As of 31 January 2019dindakharismaNo ratings yet

- What Are The Different Types of DebenturesDocument2 pagesWhat Are The Different Types of DebenturesUsman NadeemNo ratings yet

- Decision Analysis ProblemDocument2 pagesDecision Analysis ProblemGeejayFerrerPaculdo50% (2)

- Real People Who Makes Real Money Online: 1. Carlo OcabDocument7 pagesReal People Who Makes Real Money Online: 1. Carlo OcabAnarix PalconitNo ratings yet

- CH 08Document19 pagesCH 08Ahmed Al EkamNo ratings yet