Download as pdf or txt

You might also like

- FiLLi Brand Profile 2020 LowDocument40 pagesFiLLi Brand Profile 2020 LowJoshNo ratings yet

- Consultative Selling: The Hanan Formula for High-Margin Sales at High LevelsFrom EverandConsultative Selling: The Hanan Formula for High-Margin Sales at High LevelsRating: 5 out of 5 stars5/5 (1)

- Summary of Aldi Supply ChainDocument3 pagesSummary of Aldi Supply ChainRaphaella M'BembaNo ratings yet

- Cisco Systems: Managing The Go-To-Market EvolutionDocument14 pagesCisco Systems: Managing The Go-To-Market EvolutionSupriya MurdiaNo ratings yet

- B2B Assignment: MicrosoftDocument25 pagesB2B Assignment: Microsoftmedha surNo ratings yet

- South Korean Beauty MarketDocument6 pagesSouth Korean Beauty MarketsattwaNo ratings yet

- Case Study Aldi The Dark Horse Discounter by Khair MuhamamdDocument10 pagesCase Study Aldi The Dark Horse Discounter by Khair MuhamamdKhair Muhammad67% (3)

- Presented by Lokesh Kishor Neelandra Ravi SandeepDocument23 pagesPresented by Lokesh Kishor Neelandra Ravi Sandeepkishorchandra75% (4)

- Chapter 8 - Business StrategyDocument33 pagesChapter 8 - Business StrategyNazmul H. PalashNo ratings yet

- Dess' Sari - Sari Store: A Case StudyDocument21 pagesDess' Sari - Sari Store: A Case StudyfilNo ratings yet

- The Impact of Digital Technology and Industry 4 0 On The Ripple Effect and Supply Chain Risk AnalyticsDocument19 pagesThe Impact of Digital Technology and Industry 4 0 On The Ripple Effect and Supply Chain Risk AnalyticsOUAFI KheireddineNo ratings yet

- Group 2 AldiDocument9 pagesGroup 2 AldiSupriya MurdiaNo ratings yet

- Customer Value: Mcgraw-Hill/IrwinDocument42 pagesCustomer Value: Mcgraw-Hill/IrwinHRIDAY HARIANo ratings yet

- German PLDocument32 pagesGerman PLMuhamed Najada AlimiNo ratings yet

- Aldi: The Dark Horse DiscounterDocument4 pagesAldi: The Dark Horse DiscounterAkanksha KNo ratings yet

- Walmart's Business Environment Analysis ReportDocument9 pagesWalmart's Business Environment Analysis ReportRyanNo ratings yet

- Topic 1 - Business Strategy AnalysisDocument30 pagesTopic 1 - Business Strategy AnalysisOng Zi JiunNo ratings yet

- Retail Management Module 1 NotesDocument2 pagesRetail Management Module 1 NotesFrankie CordovaNo ratings yet

- Porters Five Forces - What It Means For Your BusinessDocument4 pagesPorters Five Forces - What It Means For Your Businessanil_baddi100% (10)

- Strategic AlternativesDocument118 pagesStrategic AlternativesAdarsh DashNo ratings yet

- AldiDocument8 pagesAldiSierra MarquesNo ratings yet

- 3300 Strategy - Aldi 2020Document6 pages3300 Strategy - Aldi 2020Amariah ShairNo ratings yet

- Business Level StrategiesDocument22 pagesBusiness Level StrategiesADARSH MATHURNo ratings yet

- Section A - Group 5 - StarTechDocument10 pagesSection A - Group 5 - StarTechSubhasish BalaNo ratings yet

- Wal Mart FinalDocument28 pagesWal Mart FinalThë FähãdNo ratings yet

- Strategy & Policy Lecture Week 6 - CanvasDocument37 pagesStrategy & Policy Lecture Week 6 - CanvasPo Wai LeungNo ratings yet

- Business Level StrategyDocument28 pagesBusiness Level Strategydjayaram144No ratings yet

- A Marketing StrategyDocument27 pagesA Marketing StrategyGauri Jadhav100% (1)

- Porter's Generic StrategiesDocument22 pagesPorter's Generic StrategiesChristian GuerNo ratings yet

- DMart RetailingDocument10 pagesDMart RetailingAnkush100% (1)

- Supply Chain CasesDocument21 pagesSupply Chain CasesAtique AhmedNo ratings yet

- Marketing of Services Assignment.Document4 pagesMarketing of Services Assignment.RICHARD BAGENo ratings yet

- Group - 8 - Barilla SPA Case StudyDocument9 pagesGroup - 8 - Barilla SPA Case Studykanishk khandelwalNo ratings yet

- Retail Strategy: MarketingDocument14 pagesRetail Strategy: MarketingANVESHI SHARMANo ratings yet

- 06 Pricing in Theory and Practice 2021Document54 pages06 Pricing in Theory and Practice 2021Mad MuxNo ratings yet

- Retail Supply Chain ManagementDocument12 pagesRetail Supply Chain Managementsaurav singhNo ratings yet

- Summary of The DocumentDocument4 pagesSummary of The DocumentBhakteshNo ratings yet

- BK - Porter Generic StrategiesDocument10 pagesBK - Porter Generic StrategiesBagas PambudiNo ratings yet

- Ch2 Achieving Strategic Fit in A Supply ChainDocument31 pagesCh2 Achieving Strategic Fit in A Supply Chainatharv.official2000No ratings yet

- Topic 2: Business Strategy and Competitive Advantage: Value Creation, Value Captured and Willingness To Buy and SellDocument20 pagesTopic 2: Business Strategy and Competitive Advantage: Value Creation, Value Captured and Willingness To Buy and SellNainika KhannaNo ratings yet

- Wal-Mart and Bharti: Transforming Retail in India: Presented To: Prof. Ajith Kumar Presented By: Group 7Document27 pagesWal-Mart and Bharti: Transforming Retail in India: Presented To: Prof. Ajith Kumar Presented By: Group 7Anupam ChaplotNo ratings yet

- Porter Generic StrategiesDocument11 pagesPorter Generic StrategiesebustosfNo ratings yet

- Aldi Case AnalysisDocument7 pagesAldi Case AnalysisAnju RajbangshiNo ratings yet

- Channel Institutions: Amity Business SchoolDocument29 pagesChannel Institutions: Amity Business SchoolDil EepNo ratings yet

- Marketing S15 - Retailing PDFDocument27 pagesMarketing S15 - Retailing PDFAnant SinghalNo ratings yet

- Handout On Market AttractivenessDocument9 pagesHandout On Market AttractivenessbgrhmjjcdfNo ratings yet

- 08 Chapter 1Document50 pages08 Chapter 1Rajendra Babu DaraNo ratings yet

- SM - FinalDocument2 pagesSM - FinalRaihanNo ratings yet

- Channel DesignDocument27 pagesChannel DesignchetanNo ratings yet

- The Five Competitive Forces That Shape StrategyDocument10 pagesThe Five Competitive Forces That Shape StrategyDuong Do100% (1)

- How To Design For Agile Line Production?Document21 pagesHow To Design For Agile Line Production?SudamBeheraNo ratings yet

- Wal Mart FinalDocument21 pagesWal Mart FinalFaizan UsmaniNo ratings yet

- External Audit NotesDocument3 pagesExternal Audit NotesPatricia May CayagoNo ratings yet

- HITTING BACK: Strategic Responses To Low-Cost Rivals: Edward Rahardian Wijayanto 117.09.2004Document8 pagesHITTING BACK: Strategic Responses To Low-Cost Rivals: Edward Rahardian Wijayanto 117.09.2004ong_edwardNo ratings yet

- Strategicmanagement 110327110722 Phpapp02 PDFDocument19 pagesStrategicmanagement 110327110722 Phpapp02 PDFtazeem khanNo ratings yet

- Porters Generic StrategyDocument19 pagesPorters Generic StrategyMuhammad TalhaNo ratings yet

- Assignment1 WalmartCaseDocument3 pagesAssignment1 WalmartCaseShriya MNo ratings yet

- Stratma 1.1Document4 pagesStratma 1.1Patrick AlvinNo ratings yet

- IBUS 305 Lecture 2 - Managing Industry CompetitionDocument3 pagesIBUS 305 Lecture 2 - Managing Industry Competitionmohit verrmaNo ratings yet

- 3 Case Sports ObermeyerDocument56 pages3 Case Sports ObermeyerSinem DüdenNo ratings yet

- Handouts Retail MGMT SBUP Sessions Till 9-SeptDocument18 pagesHandouts Retail MGMT SBUP Sessions Till 9-SeptVaibhav AdeNo ratings yet

- CROMA FinalDocument21 pagesCROMA Finalsharajain0% (1)

- 1 DMart Itself Isn MonojDocument4 pages1 DMart Itself Isn MonojAanya SinghNo ratings yet

- The Profit Zone (Review and Analysis of Slywotzky and Morrison's Book)From EverandThe Profit Zone (Review and Analysis of Slywotzky and Morrison's Book)No ratings yet

- Wal-Mart Stores, Inc., Global Retailer case study, the GUIDE editionFrom EverandWal-Mart Stores, Inc., Global Retailer case study, the GUIDE editionNo ratings yet

- Direct Salesforcevs Independent RepsDocument18 pagesDirect Salesforcevs Independent RepsSupriya MurdiaNo ratings yet

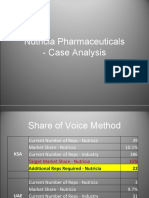

- Session 10 Case Analysis Nutricia PharmaceuticalDocument8 pagesSession 10 Case Analysis Nutricia PharmaceuticalSupriya MurdiaNo ratings yet

- The Kingsmen IIM B VFDocument19 pagesThe Kingsmen IIM B VFSupriya MurdiaNo ratings yet

- Managing Salesforce Compensation During The Growth Stage: A Financial Modelling ApproachDocument16 pagesManaging Salesforce Compensation During The Growth Stage: A Financial Modelling ApproachSupriya MurdiaNo ratings yet

- SDM NutriciaDocument11 pagesSDM NutriciaSupriya MurdiaNo ratings yet

- Creative Lab: Overcoming The Global-Local Challenge in Communication'Document24 pagesCreative Lab: Overcoming The Global-Local Challenge in Communication'Supriya MurdiaNo ratings yet

- Cisco - Group 1Document10 pagesCisco - Group 1Supriya MurdiaNo ratings yet

- Group 2 AldiDocument9 pagesGroup 2 AldiSupriya MurdiaNo ratings yet

- Group 4 Amazon - Com (2021) VFDocument8 pagesGroup 4 Amazon - Com (2021) VFSupriya MurdiaNo ratings yet

- Cultural Symbolism - Group 6Document20 pagesCultural Symbolism - Group 6Supriya MurdiaNo ratings yet

- Hult@IIMB Information DocumentDocument6 pagesHult@IIMB Information DocumentSupriya MurdiaNo ratings yet

- Exchange Committee - TaskDocument1 pageExchange Committee - TaskSupriya MurdiaNo ratings yet

- Disseration ReportDocument98 pagesDisseration ReportSupriya MurdiaNo ratings yet

- Eximius Oc: Name Phone Email ID VerticalDocument3 pagesEximius Oc: Name Phone Email ID VerticalSupriya MurdiaNo ratings yet

- Revisiting Secretary ProblemDocument25 pagesRevisiting Secretary ProblemSupriya MurdiaNo ratings yet

- Product at Sharechat - Strategy at Oyo - Consulting at Indus, PWCDocument1 pageProduct at Sharechat - Strategy at Oyo - Consulting at Indus, PWCSupriya MurdiaNo ratings yet

- Brainpan Innovations Disease Matrix 161213Document25 pagesBrainpan Innovations Disease Matrix 161213Supriya MurdiaNo ratings yet

- Helping Hands All AdminsDocument2 pagesHelping Hands All AdminsSupriya MurdiaNo ratings yet

- Celebrate The Sea Festival SCMP ArticleDocument1 pageCelebrate The Sea Festival SCMP ArticleSupriya MurdiaNo ratings yet

- Sample CV 3Document1 pageSample CV 3Supriya MurdiaNo ratings yet

- Andersen, Fusari, Todorov - 2015 - ECON - Parametric Inference and Dynamic State Recovery From Option PanelsDocument65 pagesAndersen, Fusari, Todorov - 2015 - ECON - Parametric Inference and Dynamic State Recovery From Option PanelsSupriya MurdiaNo ratings yet

- Executive StatementDocument2 pagesExecutive StatementSupriya MurdiaNo ratings yet

- HCCB Case Competition: Elevator PitchDocument3 pagesHCCB Case Competition: Elevator PitchSupriya MurdiaNo ratings yet

- Zero Beta PresentationDocument57 pagesZero Beta PresentationSupriya MurdiaNo ratings yet

- A Project Human Resource Management in HeritageDocument96 pagesA Project Human Resource Management in HeritageNagireddy Kalluri100% (1)

- Zoning OrdinanceDocument55 pagesZoning OrdinanceErnan BaldomeroNo ratings yet

- China HandbookDocument210 pagesChina HandbookPMNo ratings yet

- CHY Mall Business - FinalDocument11 pagesCHY Mall Business - FinalErnest SUNDAYNo ratings yet

- Mandatory Infants and Children Health Immunization Act of 2011Document13 pagesMandatory Infants and Children Health Immunization Act of 2011Divine MacaibaNo ratings yet

- JD VirbacDocument3 pagesJD VirbacSarvesh DubeyNo ratings yet

- The Savannah Hypothesis of Shopping - Charles DennisDocument6 pagesThe Savannah Hypothesis of Shopping - Charles DennisarchanasridharaNo ratings yet

- It in Retail SectorDocument25 pagesIt in Retail Sectorakhilraj005No ratings yet

- DLF Group Market Survey ReportDocument43 pagesDLF Group Market Survey ReportcheersinghNo ratings yet

- Three Potentials of Indonesia Water Purifier MarketDocument5 pagesThree Potentials of Indonesia Water Purifier MarketNilofar KhanNo ratings yet

- Questionnaire Factors Influencing Consumer Satisfaction Towards Online Shopping PDFDocument5 pagesQuestionnaire Factors Influencing Consumer Satisfaction Towards Online Shopping PDFTalNo ratings yet

- Bai Giang Khoa C - File G I SVDocument49 pagesBai Giang Khoa C - File G I SVMinh PhươnggNo ratings yet

- Breeders Own Pet Food Inc Case AnalysisDocument11 pagesBreeders Own Pet Food Inc Case Analysisapi-528136913100% (1)

- Catman 3-0 Introduction FinalDocument3 pagesCatman 3-0 Introduction FinalMuthu PattarNo ratings yet

- Ikea China Case StudyDocument5 pagesIkea China Case StudyJanani PsNo ratings yet

- Information Gathering and Processing in Retailing: Retail Management: A Strategic ApproachDocument28 pagesInformation Gathering and Processing in Retailing: Retail Management: A Strategic ApproachSneha AgarwalNo ratings yet

- Strategic Management ProjectDocument9 pagesStrategic Management ProjectUsama AdenwalaNo ratings yet

- Amanuel Tsegay Final VerDocument79 pagesAmanuel Tsegay Final VerYayew MaruNo ratings yet

- Political EnviornmentDocument8 pagesPolitical EnviornmentKhoai TâyNo ratings yet

- External Analysis For Macy S Departmental Stores IncDocument12 pagesExternal Analysis For Macy S Departmental Stores IncRaduan B. AbdullahNo ratings yet

- Marketing Plan-Oxfam AustraliaDocument11 pagesMarketing Plan-Oxfam Australiahandyjohn123No ratings yet

- Session 4 - Marketing Mix - TranscriptDocument17 pagesSession 4 - Marketing Mix - TranscriptIRONY - Being Alive Being VocalNo ratings yet

- Us 2022 Outlook Oil and GasDocument11 pagesUs 2022 Outlook Oil and GasChib DavidNo ratings yet

- Soumya Singh 2019 - Analysis of Delivery Issues That Customer Face Upon E-Commerce ShoppingDocument14 pagesSoumya Singh 2019 - Analysis of Delivery Issues That Customer Face Upon E-Commerce ShoppingLevi NguyenNo ratings yet

- 5 SustainableMarketingDocument554 pages5 SustainableMarketingSandesh TariNo ratings yet