Download as pdf or txt

You might also like

- Melinda Flowers 1040 PDFDocument2 pagesMelinda Flowers 1040 PDFCHRISTIAN RODRIGUEZ50% (4)

- Job Offer Letter J A S D Jayaweera OfferDocument2 pagesJob Offer Letter J A S D Jayaweera OfferB KASUN100% (1)

- Update To All Staff On Resolution For The Removal of MD NedcoDocument4 pagesUpdate To All Staff On Resolution For The Removal of MD NedcoThe Independent GhanaNo ratings yet

- ATO Tax Time 2022 resources now available - TaxBanterDocument7 pagesATO Tax Time 2022 resources now available - TaxBantersienna1227No ratings yet

- 26 Scheme For Reimbursement of Mobile Phone & Digital ServicesDocument3 pages26 Scheme For Reimbursement of Mobile Phone & Digital Servicesmurali krishnaNo ratings yet

- Spesifikasi Kaedah Pengiraan Berkomputer PCB 2022Document49 pagesSpesifikasi Kaedah Pengiraan Berkomputer PCB 2022jhb13No ratings yet

- Annexure II Details of AllowancesDocument4 pagesAnnexure II Details of AllowancesPravin Balasaheb GunjalNo ratings yet

- Companies Fresh Start Scheme 2020Document47 pagesCompanies Fresh Start Scheme 2020RENISH VITHALANINo ratings yet

- Decoding Indian Union BudgetDocument6 pagesDecoding Indian Union BudgetkumarNo ratings yet

- Notice To The Public: CIAP Circular No. - Series of 2020Document7 pagesNotice To The Public: CIAP Circular No. - Series of 2020danna Grace MalinaoNo ratings yet

- Guide ITProof SubmissionDocument9 pagesGuide ITProof SubmissionSrikanthNo ratings yet

- Home Computers ExplainedDocument4 pagesHome Computers Explainedneeraj_vit1073No ratings yet

- SETC Tax Credit Guide 207692Document1 pageSETC Tax Credit Guide 207692ri.chardcaldw.ellus.a1No ratings yet

- EY Tax Alert: Malaysian DevelopmentsDocument12 pagesEY Tax Alert: Malaysian DevelopmentsWong Yong Sheng WongNo ratings yet

- Other Tax and Investment DevelopmentsDocument21 pagesOther Tax and Investment DevelopmentsShandru MurthyNo ratings yet

- Week 1-3Document26 pagesWeek 1-3Aliah OdinNo ratings yet

- Accounting PoliciesDocument4 pagesAccounting PoliciesShaiju MohammedNo ratings yet

- New Labor Codes Provident Fund and Other Employment Related Updates On Account of Covid 19Document5 pagesNew Labor Codes Provident Fund and Other Employment Related Updates On Account of Covid 19Chanakya NitiNo ratings yet

- Deemed Interest IncomeDocument6 pagesDeemed Interest IncomeHaris HashimNo ratings yet

- The MendenFreiman Advisor - Spring 2022 EditionDocument4 pagesThe MendenFreiman Advisor - Spring 2022 EditionMendenFreiman LLPNo ratings yet

- SETC Tax Credit Guide 130540Document2 pagesSETC Tax Credit Guide 130540r.i.c.h.a.rdca.l.dwell.u.sa1No ratings yet

- SETC Tax Credit Guide 130316Document2 pagesSETC Tax Credit Guide 130316r.i.c.h.a.rdca.l.dwell.u.sa1No ratings yet

- TAX Budget2012 Annexa4Document40 pagesTAX Budget2012 Annexa4Fiona Jinn NNo ratings yet

- SETC Tax Credit Guide 181590Document2 pagesSETC Tax Credit Guide 181590r.i.c.h.a.rdca.l.dwell.u.sa1No ratings yet

- SETC Tax Credit Guide 217099Document2 pagesSETC Tax Credit Guide 217099r.i.c.h.a.rdca.l.dwell.u.sa1No ratings yet

- Tax Assignment - 26th January 2024Document14 pagesTax Assignment - 26th January 2024Sahil KathrotiyaNo ratings yet

- Budget 2023 CKDocument16 pagesBudget 2023 CKVenkateswar raoNo ratings yet

- Union Budget 2022Document27 pagesUnion Budget 2022NandiniGovindarajuNo ratings yet

- SETC Tax Credit Guide 173649Document2 pagesSETC Tax Credit Guide 173649r.i.c.h.a.rdca.l.dwell.u.sa1No ratings yet

- Budget Highlights Athena Law-R1Document4 pagesBudget Highlights Athena Law-R1Ashar AkhtarNo ratings yet

- BSNL Benifit MedicalDocument4 pagesBSNL Benifit MedicalharishsatheNo ratings yet

- Section-By-Section Coronavirus Tax Relief MeasuresDocument4 pagesSection-By-Section Coronavirus Tax Relief MeasuresFox News80% (5)

- EASY AID Guide Spreadsheet ApplicationDocument12 pagesEASY AID Guide Spreadsheet Applicationtraceymazibuko16No ratings yet

- Taxation Direct and Indirect NMIMS AssignmentDocument6 pagesTaxation Direct and Indirect NMIMS AssignmentN. Karthik UdupaNo ratings yet

- Finance Bill Highlights 2012Document36 pagesFinance Bill Highlights 2012Kashmira RNo ratings yet

- SETC Tax Credit Guide 135424Document2 pagesSETC Tax Credit Guide 135424r.i.c.h.a.rdca.l.dwell.u.sa1No ratings yet

- Interimbudget 2024 25Document7 pagesInterimbudget 2024 25prasanrobomateNo ratings yet

- Effective 1 April 2021: HR VidyalayaDocument1 pageEffective 1 April 2021: HR Vidyalayarsms 1987No ratings yet

- All Document Reader 1714473368358Document43 pagesAll Document Reader 1714473368358menejameshili202No ratings yet

- Chapter 1 - Introduction To GST: Applicability of Utgst ActDocument7 pagesChapter 1 - Introduction To GST: Applicability of Utgst ActSoul of honeyNo ratings yet

- II Administration of Medical Scheme: 1. Esi Act - A Brief IntroductionDocument12 pagesII Administration of Medical Scheme: 1. Esi Act - A Brief IntroductionAkhil GNo ratings yet

- Tax ReturnDocument18 pagesTax ReturnJoachim NosikNo ratings yet

- The Rigours of TDS - An OverviewDocument31 pagesThe Rigours of TDS - An OverviewShaleenPatniNo ratings yet

- ERC DescriptionDocument3 pagesERC Descriptionjasonoutfleet1No ratings yet

- COVID-19 Paycheck Protection Program 4.7.20 - FINALDocument25 pagesCOVID-19 Paycheck Protection Program 4.7.20 - FINALJonathan FoxNo ratings yet

- Proposed Tax Changes Under The Finance Bill 2022 ALN Kenya Legal Alert April 2022Document24 pagesProposed Tax Changes Under The Finance Bill 2022 ALN Kenya Legal Alert April 2022yomak94018No ratings yet

- 2024.4.6 - lhdnm_general-faqs_6apr2024Document10 pages2024.4.6 - lhdnm_general-faqs_6apr2024tiny cocomelonsNo ratings yet

- What Did The Union Budget 2022 Do For Charitable Organisations?Document5 pagesWhat Did The Union Budget 2022 Do For Charitable Organisations?Aakash MalhotraNo ratings yet

- Principles of TaxationDocument17 pagesPrinciples of TaxationEMMANUEL ADJEINo ratings yet

- Direct Taxes Code 2010Document14 pagesDirect Taxes Code 2010musti_shahNo ratings yet

- Guidance For Employers Claiming Employee Retention Credit During Third and Fourth Quarters of 2021 (IR-2021-165)Document2 pagesGuidance For Employers Claiming Employee Retention Credit During Third and Fourth Quarters of 2021 (IR-2021-165)Ishaani AwasthiNo ratings yet

- Recent Amendments in TDS Under Income Tax - TVM BR CPE 03.09.2022Document64 pagesRecent Amendments in TDS Under Income Tax - TVM BR CPE 03.09.2022sushant980No ratings yet

- Important Changes For 2022 Payroll: Yeo & YeoDocument2 pagesImportant Changes For 2022 Payroll: Yeo & Yeolarryching_884369919No ratings yet

- Employee BenefitsDocument31 pagesEmployee BenefitsHazel PachecoNo ratings yet

- APGLI Operational Guidelines English and TeluguDocument20 pagesAPGLI Operational Guidelines English and Telugunateshnagaraju1568No ratings yet

- EY Tax Alert: Malaysian DevelopmentsDocument12 pagesEY Tax Alert: Malaysian DevelopmentsdanNo ratings yet

- A Guide To Your Personal Income TaxDocument7 pagesA Guide To Your Personal Income TaxRekha SinghNo ratings yet

- IT PolicyDocument2 pagesIT PolicyvarunNo ratings yet

- Union BudgetDocument16 pagesUnion Budgetchandan.singhbitNo ratings yet

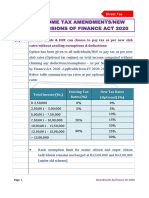

- Income Tax Amendments/New Provisions of Finance Act 2020Document46 pagesIncome Tax Amendments/New Provisions of Finance Act 2020shubhamworkNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- Income From Salary-BasicsDocument14 pagesIncome From Salary-BasicsAvishiNo ratings yet

- Scope of Total IncomeDocument17 pagesScope of Total IncomeAvishiNo ratings yet

- Accrual v. Receipt of IncomeDocument23 pagesAccrual v. Receipt of IncomeAvishiNo ratings yet

- Final IPRsDocument45 pagesFinal IPRsAvishiNo ratings yet

- Reply in Support of Cross-Motion For Summary Judgment, Federal DefendantsDocument19 pagesReply in Support of Cross-Motion For Summary Judgment, Federal DefendantsEquallyAmericanNo ratings yet

- Employee Pension Scheme Form 10 C PDFDocument1 pageEmployee Pension Scheme Form 10 C PDFSuraj BaugNo ratings yet

- Ceruila Vs DelantarDocument7 pagesCeruila Vs DelantarGhee MoralesNo ratings yet

- Unit-1.c.Classification of PrisonersDocument5 pagesUnit-1.c.Classification of PrisonersGopal SNo ratings yet

- Plaintiffs' Original PetitionDocument10 pagesPlaintiffs' Original PetitionToronto Star100% (1)

- ALTI Minutes of The Meeting 04Document3 pagesALTI Minutes of The Meeting 04Dave Jasm MatusalemNo ratings yet

- Why Afghanistan FellDocument6 pagesWhy Afghanistan Fellaqsa ilyasNo ratings yet

- CD 13. Pesigan v. Angeles, 129 SCRA 174 (1984)Document2 pagesCD 13. Pesigan v. Angeles, 129 SCRA 174 (1984)JMae MagatNo ratings yet

- Naima Niambi - COPY: PASTE "FOR IMMEDIATE RELEASE: May 24, PDFDocument3 pagesNaima Niambi - COPY: PASTE "FOR IMMEDIATE RELEASE: May 24, PDFBenjamin A Boyce100% (1)

- Clarificatory Note No. 18-001 Subject: Consolidation of OwnershipDocument6 pagesClarificatory Note No. 18-001 Subject: Consolidation of OwnershipReginald Matt Aquino SantiagoNo ratings yet

- Notice To Appear at Trial and Produce Documents For California DivorceDocument2 pagesNotice To Appear at Trial and Produce Documents For California DivorceStan Burman100% (3)

- Checklist For DPT 3 ReturnDocument1 pageChecklist For DPT 3 ReturnAbhinay KumarNo ratings yet

- Legal Studies-Mcq-1Document3 pagesLegal Studies-Mcq-1Binode SarkarNo ratings yet

- Province of Zamboanga Vs City ZamboangaDocument12 pagesProvince of Zamboanga Vs City ZamboangaLau NunezNo ratings yet

- PALE - 19. Disciplinary Proceedings Against Judges and JusticesDocument12 pagesPALE - 19. Disciplinary Proceedings Against Judges and JusticesAto TejaNo ratings yet

- Fortnightly Tax Table 2016 17Document10 pagesFortnightly Tax Table 2016 17nirpatel2No ratings yet

- The Truth About Charter Schools (NYC)Document3 pagesThe Truth About Charter Schools (NYC)Grassroots Education Movement (NYC)100% (1)

- Rates of Income TaxDocument9 pagesRates of Income TaxAiza KhanNo ratings yet

- Case AnalysisDocument14 pagesCase AnalysisAdhipatya Singh100% (2)

- Ipc SeminarDocument13 pagesIpc SeminarVibhuti SirsatNo ratings yet

- Theme 10 - Fiscal Federalism: Public EconomicsDocument38 pagesTheme 10 - Fiscal Federalism: Public EconomicsHeap Ke XinNo ratings yet

- Con Law OutlineDocument44 pagesCon Law Outlinemsegarra88No ratings yet

- Doctrine of 'Indoor Management': Leading Cases of Turquand's RuleDocument7 pagesDoctrine of 'Indoor Management': Leading Cases of Turquand's Rulepinku13No ratings yet

- Offences Against The Person Act Trinidad and TobagoDocument37 pagesOffences Against The Person Act Trinidad and TobagoGraysonNo ratings yet

- Template Letter of OfferDocument2 pagesTemplate Letter of OfferAnurag SinghNo ratings yet

- APES 205:: Conformity With Accounting Standards Fact SheetDocument2 pagesAPES 205:: Conformity With Accounting Standards Fact SheetVMRONo ratings yet

- Kurk Kendall Johnson v. State of Oklahoma, 449 U.S. 1132 (1981)Document3 pagesKurk Kendall Johnson v. State of Oklahoma, 449 U.S. 1132 (1981)Scribd Government DocsNo ratings yet

- Rti QuestionsDocument1 pageRti QuestionsVigneshNo ratings yet