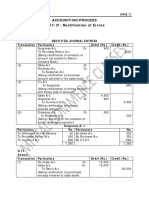

Journal Date Particulars L.F. Amt. (DR.) Amt. (CR.) : Solution Class 11 - Accountancy Test 2

Journal Date Particulars L.F. Amt. (DR.) Amt. (CR.) : Solution Class 11 - Accountancy Test 2

You might also like

- Western Constitutionalism - Andrea BurattiDocument257 pagesWestern Constitutionalism - Andrea BurattiGulrukh SadullayevaNo ratings yet

- 03 Reconstitution of Partnership Admission of Partner PDFDocument24 pages03 Reconstitution of Partnership Admission of Partner PDFBrawler Stars100% (3)

- 47 Branch AccountsDocument53 pages47 Branch AccountsShivaram Krishnan70% (10)

- ch09Document26 pagesch09Mudit Kapoor100% (1)

- Latigina A G Bazoviy Kurs Angliys Koyi Movi Z Ekonomiki Basi PDFDocument365 pagesLatigina A G Bazoviy Kurs Angliys Koyi Movi Z Ekonomiki Basi PDFfkj grdgNo ratings yet

- Solution Class 11 - Accountancy Test 1: Cash DiscountDocument4 pagesSolution Class 11 - Accountancy Test 1: Cash DiscountBHS PRAYAGRAJNo ratings yet

- CA Foundation Accounting SolutionsDocument117 pagesCA Foundation Accounting SolutionsAkash AjayNo ratings yet

- Fa2 Assignment - Ic201248Document7 pagesFa2 Assignment - Ic201248Lavisha GoyalNo ratings yet

- Anka Syllables & SarvatobhadraDocument9 pagesAnka Syllables & SarvatobhadraAnonymous Q3golGNo ratings yet

- Accounts: Journal EntriesDocument4 pagesAccounts: Journal EntriestanishaNo ratings yet

- CLASS WORK 2 (11 DEC) CHP 6Document14 pagesCLASS WORK 2 (11 DEC) CHP 6Isha KatiyarNo ratings yet

- Solutions To Text Book Exercises Partnership Accounts - II: Solution - 1Document17 pagesSolutions To Text Book Exercises Partnership Accounts - II: Solution - 1M JEEVARATHNAM NAIDUNo ratings yet

- Partnership Accounts - IDocument23 pagesPartnership Accounts - IM JEEVARATHNAM NAIDU100% (1)

- Suggested Answer CAP II December 2016Document88 pagesSuggested Answer CAP II December 2016Nirmal ShresthaNo ratings yet

- MS Accountancy Set 10Document18 pagesMS Accountancy Set 10Tanisha TibrewalNo ratings yet

- RKG Class 11 Accounts Mock 2 SolDocument13 pagesRKG Class 11 Accounts Mock 2 SolSangket MukherjeeNo ratings yet

- CCP402Document19 pagesCCP402api-3849444No ratings yet

- Journal EntriesDocument2 pagesJournal EntriespratyushNo ratings yet

- Bcoc-131: Financial Accounting Tutor Marked AssignmentDocument17 pagesBcoc-131: Financial Accounting Tutor Marked AssignmentRajni KumariNo ratings yet

- Answers To NavneetDocument12 pagesAnswers To NavneetPawan TalrejaNo ratings yet

- 14 - Accounting 4 DepreciationDocument22 pages14 - Accounting 4 DepreciationKAMAL POKHRELNo ratings yet

- CCP102Document19 pagesCCP102api-3849444No ratings yet

- RKG Class 11 Accounts Mock 1 SolDocument14 pagesRKG Class 11 Accounts Mock 1 SolSangket MukherjeeNo ratings yet

- Homework 27-02-2023 (Journal)Document3 pagesHomework 27-02-2023 (Journal)Akshayaa PrakashNo ratings yet

- Partnership Final Accounts: Tar EtDocument40 pagesPartnership Final Accounts: Tar EtVenkatesh Ramchandra100% (3)

- Hsslive Xii Acc 3 Admission of A Partner KeyDocument8 pagesHsslive Xii Acc 3 Admission of A Partner KeyShinu ShinadNo ratings yet

- Accountancy: Cbse Class 11 Accountancy Sample Paper Set-3 (Answers)Document12 pagesAccountancy: Cbse Class 11 Accountancy Sample Paper Set-3 (Answers)Aangry VermaNo ratings yet

- CNP 2211 Account Suggested AnswerDocument16 pagesCNP 2211 Account Suggested AnswermridulNo ratings yet

- Depreciation and Amortization Expense (AutoRecovered)Document11 pagesDepreciation and Amortization Expense (AutoRecovered)Bhavy DubeyNo ratings yet

- Paper2 Set2 SolutionDocument7 pagesPaper2 Set2 Solutionadityatiwari122006No ratings yet

- Accounts Pre Board IiDocument9 pagesAccounts Pre Board IiNihalSoniNo ratings yet

- 5.cpbe - Xii Accts - MSDocument18 pages5.cpbe - Xii Accts - MScommerce12onlineclassesNo ratings yet

- 2020-BPS - Pre - Board II-Accountancy Answer KeyDocument16 pages2020-BPS - Pre - Board II-Accountancy Answer KeyJoshi DrcpNo ratings yet

- Adobe Scan 15 Apr 2024Document17 pagesAdobe Scan 15 Apr 2024irfu1323No ratings yet

- MAA Assignment RKDocument9 pagesMAA Assignment RKKrishna RayasamNo ratings yet

- XII CBSE - Accounts HY Exam - 01-Oct-2022 (Sug)Document7 pagesXII CBSE - Accounts HY Exam - 01-Oct-2022 (Sug)naviagrawal2006No ratings yet

- Solution Ultimate Sample Paper 2Document7 pagesSolution Ultimate Sample Paper 2Nitin KumarNo ratings yet

- Pe2 Acc Nov05Document19 pagesPe2 Acc Nov05api-3825774No ratings yet

- FA-Depreciation - Inventory SolvedDocument13 pagesFA-Depreciation - Inventory SolvedAdhiraj MukherjeeNo ratings yet

- FA-Depreciation - Inventory SolvedDocument13 pagesFA-Depreciation - Inventory SolvedAdhiraj MukherjeeNo ratings yet

- Paper2 Set1 SolutionDocument5 pagesPaper2 Set1 Solutionadityatiwari122006No ratings yet

- 12 Accountancy Lyp 2017 Foreign Set3Document41 pages12 Accountancy Lyp 2017 Foreign Set3Ashish GangwalNo ratings yet

- Class 11 Accounts SP 2 Answer KeyDocument18 pagesClass 11 Accounts SP 2 Answer KeyUdyamGNo ratings yet

- Journal Problems For AssignmentDocument2 pagesJournal Problems For AssignmentMD. Arif HossainNo ratings yet

- CLASS WORK 2 (11 DEC) CHP 6Document14 pagesCLASS WORK 2 (11 DEC) CHP 6Isha KatiyarNo ratings yet

- Sample Question Paper 2022 Marking SchemeDocument16 pagesSample Question Paper 2022 Marking SchemeTûshar ThakúrNo ratings yet

- Ledger Book Question SolutionDocument78 pagesLedger Book Question SolutionAKSHAY KUMAR GUPTANo ratings yet

- Branch AccountsDocument9 pagesBranch AccountsKalpana SinghNo ratings yet

- Accounts 1Document3 pagesAccounts 1Akhil JainNo ratings yet

- T Accounts and TB by Riffat JabeenDocument4 pagesT Accounts and TB by Riffat JabeenAbie AsifNo ratings yet

- BudgetDocument7 pagesBudgetvasanthgurusamynsNo ratings yet

- Accountancy 2023-24 MSDocument11 pagesAccountancy 2023-24 MSirfanoushad15No ratings yet

- Accounts 2Document41 pagesAccounts 2SubodhSaxenaNo ratings yet

- 2023 AccountancyDocument12 pages2023 Accountancyjatt145873No ratings yet

- Adobe Scan 07-Jul-2022Document2 pagesAdobe Scan 07-Jul-2022Accounting HelpNo ratings yet

- Branch Accounting Examination BankDocument71 pagesBranch Accounting Examination BankNicole TaylorNo ratings yet

- Accountancy MSDocument11 pagesAccountancy MSmansoorbariNo ratings yet

- Accountancy-MS 23-24Document10 pagesAccountancy-MS 23-24Ashutosh SinghNo ratings yet

- 9 He Tell Ahaue Thu 4po: Pootne Plae (Ke - Oxlos AtioDocument11 pages9 He Tell Ahaue Thu 4po: Pootne Plae (Ke - Oxlos AtioDheerNo ratings yet

- Marking Scheme Mock Test I 2023 24Document9 pagesMarking Scheme Mock Test I 2023 24HARSH CHAURASIYANo ratings yet

- Class 11th, Political, 9 July 2020Document18 pagesClass 11th, Political, 9 July 2020BHS PRAYAGRAJNo ratings yet

- RKG Institute: B - 193, Sector - 52, NoidaDocument4 pagesRKG Institute: B - 193, Sector - 52, NoidaBHS PRAYAGRAJNo ratings yet

- Solution Class 11 - Accountancy Test 1: Cash DiscountDocument4 pagesSolution Class 11 - Accountancy Test 1: Cash DiscountBHS PRAYAGRAJNo ratings yet

- RKG Institute: B - 193, Sector - 52, NoidaDocument3 pagesRKG Institute: B - 193, Sector - 52, NoidaBHS PRAYAGRAJNo ratings yet

- Bien Chapter17Document2 pagesBien Chapter17Bien EstrellaNo ratings yet

- TENPINBOWLINGDocument5 pagesTENPINBOWLING石原ユリカNo ratings yet

- IT2021112401011404338Document13 pagesIT2021112401011404338ali aabisNo ratings yet

- Module 2A PDFDocument13 pagesModule 2A PDFdeepak singhalNo ratings yet

- Account Statement: NSDL Payments BankDocument3 pagesAccount Statement: NSDL Payments BankSantosh Kumar GuptaNo ratings yet

- Aristotle PDFDocument6 pagesAristotle PDFAnonymous p5jZCn100% (1)

- Engineering Preamble: Honesty and IntegrityDocument3 pagesEngineering Preamble: Honesty and IntegrityTala DonNo ratings yet

- Unit IiDocument42 pagesUnit IiArnee Jezarie AvilaNo ratings yet

- 1 Assesment Chapter Three PDFDocument62 pages1 Assesment Chapter Three PDFbathsheba ratemoNo ratings yet

- FABM 1 LAS Quarter 4 Week 4Document12 pagesFABM 1 LAS Quarter 4 Week 4Jonalyn DicdicanNo ratings yet

- Payment Due Date Extension GuidelinesDocument1 pagePayment Due Date Extension Guidelinesapi-526528055No ratings yet

- Bureau of Customs CMO-28-2017Document1 pageBureau of Customs CMO-28-2017PortCallsNo ratings yet

- Articles of The Confederation 1781 PDFDocument13 pagesArticles of The Confederation 1781 PDFRenn DallahNo ratings yet

- Infrared and Terahertz Detectors Rogalski Antoni Online Ebook Texxtbook Full Chapter PDFDocument69 pagesInfrared and Terahertz Detectors Rogalski Antoni Online Ebook Texxtbook Full Chapter PDFdeborah.pariente972100% (9)

- 01MAY DubaiDocument1 page01MAY DubaiJoeHanTeguhNo ratings yet

- PF - Criminal Procedure Cabato NotesDocument128 pagesPF - Criminal Procedure Cabato NotesglaiNo ratings yet

- Schedule HDocument26 pagesSchedule HHemant GaikwadNo ratings yet

- Lecture 1 Hierarchy of Courts in Bangladesh Legal System of BangladeshDocument5 pagesLecture 1 Hierarchy of Courts in Bangladesh Legal System of BangladeshNusrat jahanNo ratings yet

- (LCVPF Academy) 4.1. Basics of AccountingDocument46 pages(LCVPF Academy) 4.1. Basics of AccountingBayalag Munkh-ErdeneNo ratings yet

- Lesson 2 The Philippine GovernmentDocument5 pagesLesson 2 The Philippine GovernmentChealsenNo ratings yet

- Andrea Heath Survivors' LawsuitDocument65 pagesAndrea Heath Survivors' LawsuitWilliam N. GriggNo ratings yet

- ASJ Corporation and Antonio San Juan Vs Spouses Efren and MauraDocument2 pagesASJ Corporation and Antonio San Juan Vs Spouses Efren and MauraMa Lorely Liban-CanapiNo ratings yet

- New Covid Variant Xe Symptoms - Google SearchDocument1 pageNew Covid Variant Xe Symptoms - Google SearchjetaNo ratings yet

- ASTM-2030 SandDocument1 pageASTM-2030 SandSauron2014No ratings yet

- Maruti Suzuki India Limited HRM IIMDocument5 pagesMaruti Suzuki India Limited HRM IIMIIMnotes100% (1)

- The Berenstain Bears Blessed Are The PeacemakersDocument10 pagesThe Berenstain Bears Blessed Are The PeacemakersZondervan45% (20)

- Sen Po Ek V MartinezDocument2 pagesSen Po Ek V MartinezKaren Ryl Lozada BritoNo ratings yet

Download as pdf or txt

You might also like

- Western Constitutionalism - Andrea BurattiDocument257 pagesWestern Constitutionalism - Andrea BurattiGulrukh SadullayevaNo ratings yet

- 03 Reconstitution of Partnership Admission of Partner PDFDocument24 pages03 Reconstitution of Partnership Admission of Partner PDFBrawler Stars100% (3)

- 47 Branch AccountsDocument53 pages47 Branch AccountsShivaram Krishnan70% (10)

- ch09Document26 pagesch09Mudit Kapoor100% (1)

- Latigina A G Bazoviy Kurs Angliys Koyi Movi Z Ekonomiki Basi PDFDocument365 pagesLatigina A G Bazoviy Kurs Angliys Koyi Movi Z Ekonomiki Basi PDFfkj grdgNo ratings yet

- Solution Class 11 - Accountancy Test 1: Cash DiscountDocument4 pagesSolution Class 11 - Accountancy Test 1: Cash DiscountBHS PRAYAGRAJNo ratings yet

- CA Foundation Accounting SolutionsDocument117 pagesCA Foundation Accounting SolutionsAkash AjayNo ratings yet

- Fa2 Assignment - Ic201248Document7 pagesFa2 Assignment - Ic201248Lavisha GoyalNo ratings yet

- Anka Syllables & SarvatobhadraDocument9 pagesAnka Syllables & SarvatobhadraAnonymous Q3golGNo ratings yet

- Accounts: Journal EntriesDocument4 pagesAccounts: Journal EntriestanishaNo ratings yet

- CLASS WORK 2 (11 DEC) CHP 6Document14 pagesCLASS WORK 2 (11 DEC) CHP 6Isha KatiyarNo ratings yet

- Solutions To Text Book Exercises Partnership Accounts - II: Solution - 1Document17 pagesSolutions To Text Book Exercises Partnership Accounts - II: Solution - 1M JEEVARATHNAM NAIDUNo ratings yet

- Partnership Accounts - IDocument23 pagesPartnership Accounts - IM JEEVARATHNAM NAIDU100% (1)

- Suggested Answer CAP II December 2016Document88 pagesSuggested Answer CAP II December 2016Nirmal ShresthaNo ratings yet

- MS Accountancy Set 10Document18 pagesMS Accountancy Set 10Tanisha TibrewalNo ratings yet

- RKG Class 11 Accounts Mock 2 SolDocument13 pagesRKG Class 11 Accounts Mock 2 SolSangket MukherjeeNo ratings yet

- CCP402Document19 pagesCCP402api-3849444No ratings yet

- Journal EntriesDocument2 pagesJournal EntriespratyushNo ratings yet

- Bcoc-131: Financial Accounting Tutor Marked AssignmentDocument17 pagesBcoc-131: Financial Accounting Tutor Marked AssignmentRajni KumariNo ratings yet

- Answers To NavneetDocument12 pagesAnswers To NavneetPawan TalrejaNo ratings yet

- 14 - Accounting 4 DepreciationDocument22 pages14 - Accounting 4 DepreciationKAMAL POKHRELNo ratings yet

- CCP102Document19 pagesCCP102api-3849444No ratings yet

- RKG Class 11 Accounts Mock 1 SolDocument14 pagesRKG Class 11 Accounts Mock 1 SolSangket MukherjeeNo ratings yet

- Homework 27-02-2023 (Journal)Document3 pagesHomework 27-02-2023 (Journal)Akshayaa PrakashNo ratings yet

- Partnership Final Accounts: Tar EtDocument40 pagesPartnership Final Accounts: Tar EtVenkatesh Ramchandra100% (3)

- Hsslive Xii Acc 3 Admission of A Partner KeyDocument8 pagesHsslive Xii Acc 3 Admission of A Partner KeyShinu ShinadNo ratings yet

- Accountancy: Cbse Class 11 Accountancy Sample Paper Set-3 (Answers)Document12 pagesAccountancy: Cbse Class 11 Accountancy Sample Paper Set-3 (Answers)Aangry VermaNo ratings yet

- CNP 2211 Account Suggested AnswerDocument16 pagesCNP 2211 Account Suggested AnswermridulNo ratings yet

- Depreciation and Amortization Expense (AutoRecovered)Document11 pagesDepreciation and Amortization Expense (AutoRecovered)Bhavy DubeyNo ratings yet

- Paper2 Set2 SolutionDocument7 pagesPaper2 Set2 Solutionadityatiwari122006No ratings yet

- Accounts Pre Board IiDocument9 pagesAccounts Pre Board IiNihalSoniNo ratings yet

- 5.cpbe - Xii Accts - MSDocument18 pages5.cpbe - Xii Accts - MScommerce12onlineclassesNo ratings yet

- 2020-BPS - Pre - Board II-Accountancy Answer KeyDocument16 pages2020-BPS - Pre - Board II-Accountancy Answer KeyJoshi DrcpNo ratings yet

- Adobe Scan 15 Apr 2024Document17 pagesAdobe Scan 15 Apr 2024irfu1323No ratings yet

- MAA Assignment RKDocument9 pagesMAA Assignment RKKrishna RayasamNo ratings yet

- XII CBSE - Accounts HY Exam - 01-Oct-2022 (Sug)Document7 pagesXII CBSE - Accounts HY Exam - 01-Oct-2022 (Sug)naviagrawal2006No ratings yet

- Solution Ultimate Sample Paper 2Document7 pagesSolution Ultimate Sample Paper 2Nitin KumarNo ratings yet

- Pe2 Acc Nov05Document19 pagesPe2 Acc Nov05api-3825774No ratings yet

- FA-Depreciation - Inventory SolvedDocument13 pagesFA-Depreciation - Inventory SolvedAdhiraj MukherjeeNo ratings yet

- FA-Depreciation - Inventory SolvedDocument13 pagesFA-Depreciation - Inventory SolvedAdhiraj MukherjeeNo ratings yet

- Paper2 Set1 SolutionDocument5 pagesPaper2 Set1 Solutionadityatiwari122006No ratings yet

- 12 Accountancy Lyp 2017 Foreign Set3Document41 pages12 Accountancy Lyp 2017 Foreign Set3Ashish GangwalNo ratings yet

- Class 11 Accounts SP 2 Answer KeyDocument18 pagesClass 11 Accounts SP 2 Answer KeyUdyamGNo ratings yet

- Journal Problems For AssignmentDocument2 pagesJournal Problems For AssignmentMD. Arif HossainNo ratings yet

- CLASS WORK 2 (11 DEC) CHP 6Document14 pagesCLASS WORK 2 (11 DEC) CHP 6Isha KatiyarNo ratings yet

- Sample Question Paper 2022 Marking SchemeDocument16 pagesSample Question Paper 2022 Marking SchemeTûshar ThakúrNo ratings yet

- Ledger Book Question SolutionDocument78 pagesLedger Book Question SolutionAKSHAY KUMAR GUPTANo ratings yet

- Branch AccountsDocument9 pagesBranch AccountsKalpana SinghNo ratings yet

- Accounts 1Document3 pagesAccounts 1Akhil JainNo ratings yet

- T Accounts and TB by Riffat JabeenDocument4 pagesT Accounts and TB by Riffat JabeenAbie AsifNo ratings yet

- BudgetDocument7 pagesBudgetvasanthgurusamynsNo ratings yet

- Accountancy 2023-24 MSDocument11 pagesAccountancy 2023-24 MSirfanoushad15No ratings yet

- Accounts 2Document41 pagesAccounts 2SubodhSaxenaNo ratings yet

- 2023 AccountancyDocument12 pages2023 Accountancyjatt145873No ratings yet

- Adobe Scan 07-Jul-2022Document2 pagesAdobe Scan 07-Jul-2022Accounting HelpNo ratings yet

- Branch Accounting Examination BankDocument71 pagesBranch Accounting Examination BankNicole TaylorNo ratings yet

- Accountancy MSDocument11 pagesAccountancy MSmansoorbariNo ratings yet

- Accountancy-MS 23-24Document10 pagesAccountancy-MS 23-24Ashutosh SinghNo ratings yet

- 9 He Tell Ahaue Thu 4po: Pootne Plae (Ke - Oxlos AtioDocument11 pages9 He Tell Ahaue Thu 4po: Pootne Plae (Ke - Oxlos AtioDheerNo ratings yet

- Marking Scheme Mock Test I 2023 24Document9 pagesMarking Scheme Mock Test I 2023 24HARSH CHAURASIYANo ratings yet

- Class 11th, Political, 9 July 2020Document18 pagesClass 11th, Political, 9 July 2020BHS PRAYAGRAJNo ratings yet

- RKG Institute: B - 193, Sector - 52, NoidaDocument4 pagesRKG Institute: B - 193, Sector - 52, NoidaBHS PRAYAGRAJNo ratings yet

- Solution Class 11 - Accountancy Test 1: Cash DiscountDocument4 pagesSolution Class 11 - Accountancy Test 1: Cash DiscountBHS PRAYAGRAJNo ratings yet

- RKG Institute: B - 193, Sector - 52, NoidaDocument3 pagesRKG Institute: B - 193, Sector - 52, NoidaBHS PRAYAGRAJNo ratings yet

- Bien Chapter17Document2 pagesBien Chapter17Bien EstrellaNo ratings yet

- TENPINBOWLINGDocument5 pagesTENPINBOWLING石原ユリカNo ratings yet

- IT2021112401011404338Document13 pagesIT2021112401011404338ali aabisNo ratings yet

- Module 2A PDFDocument13 pagesModule 2A PDFdeepak singhalNo ratings yet

- Account Statement: NSDL Payments BankDocument3 pagesAccount Statement: NSDL Payments BankSantosh Kumar GuptaNo ratings yet

- Aristotle PDFDocument6 pagesAristotle PDFAnonymous p5jZCn100% (1)

- Engineering Preamble: Honesty and IntegrityDocument3 pagesEngineering Preamble: Honesty and IntegrityTala DonNo ratings yet

- Unit IiDocument42 pagesUnit IiArnee Jezarie AvilaNo ratings yet

- 1 Assesment Chapter Three PDFDocument62 pages1 Assesment Chapter Three PDFbathsheba ratemoNo ratings yet

- FABM 1 LAS Quarter 4 Week 4Document12 pagesFABM 1 LAS Quarter 4 Week 4Jonalyn DicdicanNo ratings yet

- Payment Due Date Extension GuidelinesDocument1 pagePayment Due Date Extension Guidelinesapi-526528055No ratings yet

- Bureau of Customs CMO-28-2017Document1 pageBureau of Customs CMO-28-2017PortCallsNo ratings yet

- Articles of The Confederation 1781 PDFDocument13 pagesArticles of The Confederation 1781 PDFRenn DallahNo ratings yet

- Infrared and Terahertz Detectors Rogalski Antoni Online Ebook Texxtbook Full Chapter PDFDocument69 pagesInfrared and Terahertz Detectors Rogalski Antoni Online Ebook Texxtbook Full Chapter PDFdeborah.pariente972100% (9)

- 01MAY DubaiDocument1 page01MAY DubaiJoeHanTeguhNo ratings yet

- PF - Criminal Procedure Cabato NotesDocument128 pagesPF - Criminal Procedure Cabato NotesglaiNo ratings yet

- Schedule HDocument26 pagesSchedule HHemant GaikwadNo ratings yet

- Lecture 1 Hierarchy of Courts in Bangladesh Legal System of BangladeshDocument5 pagesLecture 1 Hierarchy of Courts in Bangladesh Legal System of BangladeshNusrat jahanNo ratings yet

- (LCVPF Academy) 4.1. Basics of AccountingDocument46 pages(LCVPF Academy) 4.1. Basics of AccountingBayalag Munkh-ErdeneNo ratings yet

- Lesson 2 The Philippine GovernmentDocument5 pagesLesson 2 The Philippine GovernmentChealsenNo ratings yet

- Andrea Heath Survivors' LawsuitDocument65 pagesAndrea Heath Survivors' LawsuitWilliam N. GriggNo ratings yet

- ASJ Corporation and Antonio San Juan Vs Spouses Efren and MauraDocument2 pagesASJ Corporation and Antonio San Juan Vs Spouses Efren and MauraMa Lorely Liban-CanapiNo ratings yet

- New Covid Variant Xe Symptoms - Google SearchDocument1 pageNew Covid Variant Xe Symptoms - Google SearchjetaNo ratings yet

- ASTM-2030 SandDocument1 pageASTM-2030 SandSauron2014No ratings yet

- Maruti Suzuki India Limited HRM IIMDocument5 pagesMaruti Suzuki India Limited HRM IIMIIMnotes100% (1)

- The Berenstain Bears Blessed Are The PeacemakersDocument10 pagesThe Berenstain Bears Blessed Are The PeacemakersZondervan45% (20)

- Sen Po Ek V MartinezDocument2 pagesSen Po Ek V MartinezKaren Ryl Lozada BritoNo ratings yet