Download as docx, pdf, or txt

You might also like

- Unit 1: Business and The Business Environment: Assignment BriefDocument5 pagesUnit 1: Business and The Business Environment: Assignment BriefNguyễn Quốc AnhNo ratings yet

- Living Under The Crescent MoonDocument20 pagesLiving Under The Crescent MoonhelenaladeiroNo ratings yet

- Unit 6 Achievement TestDocument9 pagesUnit 6 Achievement TestPablo Silva AriasNo ratings yet

- Rutkin V UsDocument10 pagesRutkin V Usבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Rutkin v. United States, 343 U.S. 130 (1952)Document14 pagesRutkin v. United States, 343 U.S. 130 (1952)Scribd Government DocsNo ratings yet

- Rutkin Final To ReadDocument5 pagesRutkin Final To Readבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- United States Court of Appeals Second Circuit.: No. 14. Docket 23455Document13 pagesUnited States Court of Appeals Second Circuit.: No. 14. Docket 23455Scribd Government DocsNo ratings yet

- Harper v. Lloyd's Factors, Inc, 214 F.2d 662, 2d Cir. (1954)Document3 pagesHarper v. Lloyd's Factors, Inc, 214 F.2d 662, 2d Cir. (1954)Scribd Government DocsNo ratings yet

- In Re International Match Corp. Ehrhorn v. International Match Realization Co., Limited, 190 F.2d 458, 2d Cir. (1951)Document21 pagesIn Re International Match Corp. Ehrhorn v. International Match Realization Co., Limited, 190 F.2d 458, 2d Cir. (1951)Scribd Government DocsNo ratings yet

- United States v. Godwin, 4th Cir. (2001)Document34 pagesUnited States v. Godwin, 4th Cir. (2001)Scribd Government DocsNo ratings yet

- Aaron R. Seward and Connie G. Seward v. Philip J. Devine, James Devine, Jr., Daniel Horan, John F. Keating, Jr., Kenneth R. Fitzsimmons, Estate of Frank L. Imparato, Jr., and Wilber National Bank, 888 F.2d 957, 2d Cir. (1989)Document9 pagesAaron R. Seward and Connie G. Seward v. Philip J. Devine, James Devine, Jr., Daniel Horan, John F. Keating, Jr., Kenneth R. Fitzsimmons, Estate of Frank L. Imparato, Jr., and Wilber National Bank, 888 F.2d 957, 2d Cir. (1989)Scribd Government DocsNo ratings yet

- Kann v. Commissioner of Internal Revenue. Kann's Estate v. Commissioner of Internal Revenue, 210 F.2d 247, 3rd Cir. (1954)Document13 pagesKann v. Commissioner of Internal Revenue. Kann's Estate v. Commissioner of Internal Revenue, 210 F.2d 247, 3rd Cir. (1954)Scribd Government DocsNo ratings yet

- San Juan Uranium Corporation v. Thomas G. Wolfe and Virginia E. Wolfe, 241 F.2d 121, 10th Cir. (1957)Document7 pagesSan Juan Uranium Corporation v. Thomas G. Wolfe and Virginia E. Wolfe, 241 F.2d 121, 10th Cir. (1957)Scribd Government DocsNo ratings yet

- Briggs v. United States. Clark v. United States, 214 F.2d 699, 4th Cir. (1954)Document5 pagesBriggs v. United States. Clark v. United States, 214 F.2d 699, 4th Cir. (1954)Scribd Government DocsNo ratings yet

- Joseph Cohen, As Trustee in Bankruptcy of New York Investors Mutual Group, Inc., Bankrupt v. Ida Sutherland, 257 F.2d 737, 2d Cir. (1958)Document7 pagesJoseph Cohen, As Trustee in Bankruptcy of New York Investors Mutual Group, Inc., Bankrupt v. Ida Sutherland, 257 F.2d 737, 2d Cir. (1958)Scribd Government DocsNo ratings yet

- Simeon Sharaf v. Commissioner of Internal Revenue, 224 F.2d 570, 1st Cir. (1955)Document5 pagesSimeon Sharaf v. Commissioner of Internal Revenue, 224 F.2d 570, 1st Cir. (1955)Scribd Government DocsNo ratings yet

- E. Penn Nicholson, Trustee For The Estate of Carolee's Combine, Inc. v. First Investment Company and Bill Beltzer, 705 F.2d 410, 1st Cir. (1983)Document8 pagesE. Penn Nicholson, Trustee For The Estate of Carolee's Combine, Inc. v. First Investment Company and Bill Beltzer, 705 F.2d 410, 1st Cir. (1983)Scribd Government DocsNo ratings yet

- United States Court of Appeals, Seventh CircuitDocument7 pagesUnited States Court of Appeals, Seventh CircuitScribd Government DocsNo ratings yet

- R. A. Bryan and Ruby M. Bryan, C. B. McNairy and Rowena A. McNairy W. H. Weaver and Edith H. Weaver v. Commissioner of Internal Revenue, 281 F.2d 238, 4th Cir. (1960)Document8 pagesR. A. Bryan and Ruby M. Bryan, C. B. McNairy and Rowena A. McNairy W. H. Weaver and Edith H. Weaver v. Commissioner of Internal Revenue, 281 F.2d 238, 4th Cir. (1960)Scribd Government DocsNo ratings yet

- Benjamin D. and Madeline Prentice Gilbert v. Commissioner of Internal Revenue, 248 F.2d 399, 2d Cir. (1957)Document17 pagesBenjamin D. and Madeline Prentice Gilbert v. Commissioner of Internal Revenue, 248 F.2d 399, 2d Cir. (1957)Scribd Government DocsNo ratings yet

- John F. BARRY, Plaintiff-Counter-Defendant-Appellant, v. Liddle, O'Connor, Finkelstein & Robinson, Defendant-Counter-Claimant-AppelleeDocument7 pagesJohn F. BARRY, Plaintiff-Counter-Defendant-Appellant, v. Liddle, O'Connor, Finkelstein & Robinson, Defendant-Counter-Claimant-AppelleeScribd Government DocsNo ratings yet

- Margolis v. Gem Factors Corp, 201 F.2d 803, 2d Cir. (1953)Document4 pagesMargolis v. Gem Factors Corp, 201 F.2d 803, 2d Cir. (1953)Scribd Government DocsNo ratings yet

- Can-Am Petroleum Company, a Colorado Corporation, Harold D. Beckwith, and Charles Laird v. Ramona Beck, Rita Stark, Mr. James Meyers, Mrs. James Meyers, and William Halpern, 331 F.2d 371, 10th Cir. (1964)Document4 pagesCan-Am Petroleum Company, a Colorado Corporation, Harold D. Beckwith, and Charles Laird v. Ramona Beck, Rita Stark, Mr. James Meyers, Mrs. James Meyers, and William Halpern, 331 F.2d 371, 10th Cir. (1964)Scribd Government DocsNo ratings yet

- Kenerson v. FDIC, 44 F.3d 19, 1st Cir. (1995)Document29 pagesKenerson v. FDIC, 44 F.3d 19, 1st Cir. (1995)Scribd Government DocsNo ratings yet

- In Re Mid-Town Produce Terminal, Inc., Bankrupt. G. J. Sinclair v. James R. Barr, Trustee, 599 F.2d 389, 10th Cir. (1979)Document7 pagesIn Re Mid-Town Produce Terminal, Inc., Bankrupt. G. J. Sinclair v. James R. Barr, Trustee, 599 F.2d 389, 10th Cir. (1979)Scribd Government DocsNo ratings yet

- Ark-Tenn Distributing Corp. v. Breidt Breidt Appeal of Breidt. Appeal of Ark-Tenn Distributing Corp, 209 F.2d 359, 3rd Cir. (1954)Document4 pagesArk-Tenn Distributing Corp. v. Breidt Breidt Appeal of Breidt. Appeal of Ark-Tenn Distributing Corp, 209 F.2d 359, 3rd Cir. (1954)Scribd Government DocsNo ratings yet

- United States Court of Appeals Seventh CircuitDocument7 pagesUnited States Court of Appeals Seventh CircuitScribd Government DocsNo ratings yet

- I. A. Dress Co., Inc. v. Commissioner of Internal Revenue, 273 F.2d 543, 2d Cir. (1960)Document3 pagesI. A. Dress Co., Inc. v. Commissioner of Internal Revenue, 273 F.2d 543, 2d Cir. (1960)Scribd Government DocsNo ratings yet

- Matter of Philadelphia Penn Worsted Company, Bankrupt Barney Cramer and Harvey Mencoff, Copartners Trading As Advanced Textile Company, AppellantsDocument6 pagesMatter of Philadelphia Penn Worsted Company, Bankrupt Barney Cramer and Harvey Mencoff, Copartners Trading As Advanced Textile Company, AppellantsScribd Government DocsNo ratings yet

- Dabney v. Levy, 191 F.2d 201, 2d Cir. (1951)Document6 pagesDabney v. Levy, 191 F.2d 201, 2d Cir. (1951)Scribd Government DocsNo ratings yet

- Greenleaf v. Queen, 26 U.S. 138 (1828)Document12 pagesGreenleaf v. Queen, 26 U.S. 138 (1828)Scribd Government DocsNo ratings yet

- United States Court of Appeals, Eleventh CircuitDocument8 pagesUnited States Court of Appeals, Eleventh CircuitScribd Government DocsNo ratings yet

- Girard Trust Co. v. Windt (Kreis, Intervenor), 178 F.2d 359, 2d Cir. (1949)Document2 pagesGirard Trust Co. v. Windt (Kreis, Intervenor), 178 F.2d 359, 2d Cir. (1949)Scribd Government DocsNo ratings yet

- YbanezDocument4 pagesYbanezAlicia Jane NavarroNo ratings yet

- In Re Rader, 194 F.2d 988, 2d Cir. (1952)Document2 pagesIn Re Rader, 194 F.2d 988, 2d Cir. (1952)Scribd Government DocsNo ratings yet

- Richard S. Robie v. Edwin I. Ofgant, 306 F.2d 656, 1st Cir. (1962)Document6 pagesRichard S. Robie v. Edwin I. Ofgant, 306 F.2d 656, 1st Cir. (1962)Scribd Government DocsNo ratings yet

- Bankr. L. Rep. P 75,404 in Re Fred J. Wines, Debtor. Fred J. Wines v. Marian A. Wines, 997 F.2d 852, 11th Cir. (1993)Document7 pagesBankr. L. Rep. P 75,404 in Re Fred J. Wines, Debtor. Fred J. Wines v. Marian A. Wines, 997 F.2d 852, 11th Cir. (1993)Scribd Government DocsNo ratings yet

- In The Matter of Louis C. Ostrer, Bankrupt-Appellant, The Meadow Brook National Bank, Objecting Creditor-Appellee, 393 F.2d 646, 2d Cir. (1968)Document8 pagesIn The Matter of Louis C. Ostrer, Bankrupt-Appellant, The Meadow Brook National Bank, Objecting Creditor-Appellee, 393 F.2d 646, 2d Cir. (1968)Scribd Government DocsNo ratings yet

- Benjamin Brownstein, Successor Trustee-Appellant v. Aluminum Reserve Corp., 245 F.2d 82, 2d Cir. (1957)Document3 pagesBenjamin Brownstein, Successor Trustee-Appellant v. Aluminum Reserve Corp., 245 F.2d 82, 2d Cir. (1957)Scribd Government DocsNo ratings yet

- Matter of Einhorn Bros., Inc., Bankrupt. Textile Banking Company, Inc., 272 F.2d 434, 3rd Cir. (1959)Document12 pagesMatter of Einhorn Bros., Inc., Bankrupt. Textile Banking Company, Inc., 272 F.2d 434, 3rd Cir. (1959)Scribd Government DocsNo ratings yet

- United States Court of Appeals, Fourth CircuitDocument10 pagesUnited States Court of Appeals, Fourth CircuitScribd Government DocsNo ratings yet

- United States Court of Appeals Third CircuitDocument11 pagesUnited States Court of Appeals Third CircuitScribd Government DocsNo ratings yet

- Mary O'Hara Alsop v. Commissioner of Internal Revenue, 290 F.2d 726, 2d Cir. (1961)Document5 pagesMary O'Hara Alsop v. Commissioner of Internal Revenue, 290 F.2d 726, 2d Cir. (1961)Scribd Government DocsNo ratings yet

- Gibbs & Mcdonough For Petitioner. Courtney Whitney For RespondentsDocument52 pagesGibbs & Mcdonough For Petitioner. Courtney Whitney For RespondentsJen Yzabelle SalazarNo ratings yet

- Leary vs. GledhillDocument4 pagesLeary vs. GledhillaudreyNo ratings yet

- Leary vs. GledhillDocument4 pagesLeary vs. GledhillaudreyNo ratings yet

- Dickinson v. Burnham, 197 F.2d 973, 2d Cir. (1952)Document11 pagesDickinson v. Burnham, 197 F.2d 973, 2d Cir. (1952)Scribd Government DocsNo ratings yet

- Doris Filner v. Samuel Shapiro and Southwestern Alloys Corporation, 633 F.2d 139, 2d Cir. (1980)Document6 pagesDoris Filner v. Samuel Shapiro and Southwestern Alloys Corporation, 633 F.2d 139, 2d Cir. (1980)Scribd Government DocsNo ratings yet

- Rivera-Rosario v. US Dept. of Agricult, 202 F.3d 35, 1st Cir. (2000)Document4 pagesRivera-Rosario v. US Dept. of Agricult, 202 F.3d 35, 1st Cir. (2000)Scribd Government DocsNo ratings yet

- Klaus Wilke Rita E. Wilke v. Wilder Corporation, Formerly Known As Wilder Mobile Homes, Incorporated, 74 F.3d 1235, 4th Cir. (1996)Document6 pagesKlaus Wilke Rita E. Wilke v. Wilder Corporation, Formerly Known As Wilder Mobile Homes, Incorporated, 74 F.3d 1235, 4th Cir. (1996)Scribd Government DocsNo ratings yet

- United States Court of Appeals, Tenth CircuitDocument6 pagesUnited States Court of Appeals, Tenth CircuitScribd Government DocsNo ratings yet

- Fox v. Commissioner of Internal Revenue, 190 F.2d 101, 2d Cir. (1951)Document5 pagesFox v. Commissioner of Internal Revenue, 190 F.2d 101, 2d Cir. (1951)Scribd Government DocsNo ratings yet

- Carlos Vs Abelardo 380 SCRA 361Document13 pagesCarlos Vs Abelardo 380 SCRA 361Mark Lemuel TubelloNo ratings yet

- Geraldine RIDINGS, Libelant-Appellee, v. The MOTOR VESSEL 'EFFORT,' Her Engines, Etc., Respondent, M. V. Effort, Inc., Claimant-AppellantDocument7 pagesGeraldine RIDINGS, Libelant-Appellee, v. The MOTOR VESSEL 'EFFORT,' Her Engines, Etc., Respondent, M. V. Effort, Inc., Claimant-AppellantScribd Government DocsNo ratings yet

- Carlos v. Abelardo, GR 146504Document17 pagesCarlos v. Abelardo, GR 146504Anna NicerioNo ratings yet

- Friend v. Commissioner of Internal Revenue, 198 F.2d 285, 10th Cir. (1952)Document4 pagesFriend v. Commissioner of Internal Revenue, 198 F.2d 285, 10th Cir. (1952)Scribd Government DocsNo ratings yet

- Mary Lindsay Studds and Colin A. Studds, and Cross-Appellees v. Fidelity and Deposit Company of Maryland, A Corporation, and Cross-Appellant, 267 F.2d 875, 4th Cir. (1959)Document6 pagesMary Lindsay Studds and Colin A. Studds, and Cross-Appellees v. Fidelity and Deposit Company of Maryland, A Corporation, and Cross-Appellant, 267 F.2d 875, 4th Cir. (1959)Scribd Government DocsNo ratings yet

- David Wise v. Commissioner of Internal Revenue, 311 F.2d 743, 2d Cir. (1963)Document2 pagesDavid Wise v. Commissioner of Internal Revenue, 311 F.2d 743, 2d Cir. (1963)Scribd Government DocsNo ratings yet

- Sofie Eger v. Commissioner of Internal Revenue, 393 F.2d 243, 2d Cir. (1968)Document8 pagesSofie Eger v. Commissioner of Internal Revenue, 393 F.2d 243, 2d Cir. (1968)Scribd Government DocsNo ratings yet

- Livingstone Securities Corporation v. Dean Martin, 327 F.2d 937, 1st Cir. (1964)Document5 pagesLivingstone Securities Corporation v. Dean Martin, 327 F.2d 937, 1st Cir. (1964)Scribd Government DocsNo ratings yet

- Gill v. Oliver's Executors, 52 U.S. 529 (1851)Document23 pagesGill v. Oliver's Executors, 52 U.S. 529 (1851)Scribd Government DocsNo ratings yet

- Ben B. Conford v. United States, 336 F.2d 285, 10th Cir. (1964)Document6 pagesBen B. Conford v. United States, 336 F.2d 285, 10th Cir. (1964)Scribd Government DocsNo ratings yet

- The Importance of The Criminal Justice System and TodayDocument4 pagesThe Importance of The Criminal Justice System and Todayבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- BailDocument7 pagesBailבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Related QuestionsDocument2 pagesRelated Questionsבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Jürgen FrostDocument26 pagesJürgen Frostבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Human Rights in The PhilippinesDocument7 pagesHuman Rights in The Philippinesבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- BondDocument7 pagesBondבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Ethics in The Criminal Justice ProfessionsDocument12 pagesEthics in The Criminal Justice Professionsבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Lawmakers Rally Against The Death Penalty in The PhilippinesDocument2 pagesLawmakers Rally Against The Death Penalty in The Philippinesבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Despite Being Considered As A Rapidly Growing Country Both Economically and SociallyDocument3 pagesDespite Being Considered As A Rapidly Growing Country Both Economically and Sociallyבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Santos-Cliff-Anthony-T Col Quiz Nov27Document4 pagesSantos-Cliff-Anthony-T Col Quiz Nov27בנדר-עלי אימאם טינגאו בתולהNo ratings yet

- BlakeDocument2 pagesBlakeבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Civil Procedure Flow ChartDocument4 pagesCivil Procedure Flow Chartבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Qdoc - Tips - Conflict of Laws ReviewerDocument63 pagesQdoc - Tips - Conflict of Laws Reviewerבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Anizza Melijah Kalis Santos Col Quiz 6 FinalsDocument3 pagesAnizza Melijah Kalis Santos Col Quiz 6 Finalsבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Carin 11272022Document2 pagesCarin 11272022בנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Gullas V PNBDocument1 pageGullas V PNBבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- 234Document2 pages234בנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Great Asian Sales V CaDocument1 pageGreat Asian Sales V Caבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Gempesaw V CaDocument2 pagesGempesaw V Caבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Gsis V CaDocument1 pageGsis V Caבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Bdo V Equitable BankingDocument2 pagesBdo V Equitable Bankingבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Associated Bank V CaDocument1 pageAssociated Bank V Caבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Cir V Ca 2Document8 pagesCir V Ca 2בנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Rutkin V UsDocument10 pagesRutkin V Usבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Cir V Ca 3Document3 pagesCir V Ca 3בנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Asia Banking V JavierDocument1 pageAsia Banking V Javierבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Doña Carmen: CIR V CA January 20, 1999Document2 pagesDoña Carmen: CIR V CA January 20, 1999בנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Rutkin Final To ReadDocument5 pagesRutkin Final To Readבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- CIR V BOAC CDDocument7 pagesCIR V BOAC CDבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- CIR V BOAC FTDocument20 pagesCIR V BOAC FTבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- Artiste List CompleteDocument165 pagesArtiste List CompleteDorego TaofeeqNo ratings yet

- Music CollectionDocument17 pagesMusic CollectionPuran Singh LabanaNo ratings yet

- 101-98-Magazine For The Month of March-2022-FinalDocument138 pages101-98-Magazine For The Month of March-2022-FinalPratyush BalNo ratings yet

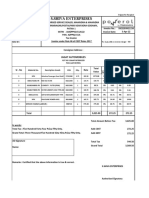

- S.Shiva Enterprises: Jagat AutomobilesDocument2 pagesS.Shiva Enterprises: Jagat AutomobilesS.SHIVA ENTERPRISESNo ratings yet

- Lumbini Pradesh - WikipediaDocument16 pagesLumbini Pradesh - WikipediaPramish PMNo ratings yet

- STHP Mock Test-07 ME AcademyDocument18 pagesSTHP Mock Test-07 ME AcademyAnand Hanjh100% (1)

- Bell Atlantic Corp v. TwomblyDocument4 pagesBell Atlantic Corp v. Twomblylfei1216No ratings yet

- GAD Action PlanDocument4 pagesGAD Action PlanLance Aldrin Adion100% (1)

- Stock Screener, Technical Analysis ScannerDocument82 pagesStock Screener, Technical Analysis Scannerravi kumarNo ratings yet

- 33 Al Ahzab TranslationDocument18 pages33 Al Ahzab TranslationAbbey IshaqNo ratings yet

- God Destruction Illuminatus 2012Document3 pagesGod Destruction Illuminatus 2012JoanneNo ratings yet

- The McKinsey 7S ModelDocument14 pagesThe McKinsey 7S ModelLilibeth Amparo100% (1)

- Human Action: A Treatise On Economics by Ludwig Von MisesDocument6 pagesHuman Action: A Treatise On Economics by Ludwig Von MisesHospodar VibescuNo ratings yet

- ShowfileDocument179 pagesShowfileSukumar NayakNo ratings yet

- Texto en Ingles Sobre El AbortoDocument1 pageTexto en Ingles Sobre El AbortoEsteban RodriguezNo ratings yet

- I. Product Design II. Planning and Scheduling III. Production Operations IV. Cost AccountingDocument15 pagesI. Product Design II. Planning and Scheduling III. Production Operations IV. Cost Accountingوائل مصطفىNo ratings yet

- Early Life and Military Career: Milan Nedić (Document10 pagesEarly Life and Military Career: Milan Nedić (Jovan PerićNo ratings yet

- Heritage Christian Academy Family Handbook: Able OF OntentsDocument37 pagesHeritage Christian Academy Family Handbook: Able OF OntentsNathan Brony ThomasNo ratings yet

- Vegan News - Issue 1 (1944)Document4 pagesVegan News - Issue 1 (1944)Vegan FutureNo ratings yet

- Bear Stearns and The Seeds of Its DemiseDocument15 pagesBear Stearns and The Seeds of Its DemiseJaja JANo ratings yet

- Taruc vs. Bishop Dela Cruz, G.R. No. 144801. March 10, 2005Document1 pageTaruc vs. Bishop Dela Cruz, G.R. No. 144801. March 10, 2005JenNo ratings yet

- People v. MadsaliDocument3 pagesPeople v. MadsaliNoreenesse SantosNo ratings yet

- Guidelines For Form 4 Subject Choice 2024Document6 pagesGuidelines For Form 4 Subject Choice 2024api-484150872No ratings yet

- Literature Review of Service Quality in RestaurantsDocument7 pagesLiterature Review of Service Quality in RestaurantsuifjzvrifNo ratings yet

- 1MS Pre-Sequence Days MonthsDocument6 pages1MS Pre-Sequence Days Monthssabrina's worldNo ratings yet

- Useful ZikrDocument4 pagesUseful ZikrKamata MasjidNo ratings yet

- René Guénon and InitiationDocument6 pagesRené Guénon and Initiationabaris13No ratings yet