Download as pdf or txt

You might also like

- M2A Final Copy (V 3.9)Document181 pagesM2A Final Copy (V 3.9)Cc HyNo ratings yet

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- Chapter 1 An Overview of FinanceDocument6 pagesChapter 1 An Overview of FinanceSyrill CayetanoNo ratings yet

- Click Here 137Document23 pagesClick Here 137Nanda GroupNo ratings yet

- RBI Master CircularDocument13 pagesRBI Master Circularnaina.kim2427No ratings yet

- 1178-Addendum-Change in Sponsor - HDFC LTD To HDFC Bank - July 1, 2023Document3 pages1178-Addendum-Change in Sponsor - HDFC LTD To HDFC Bank - July 1, 2023Jai Shree Ambe EnterprisesNo ratings yet

- Current Affairs: 01st Jan To 10th Jan 2022 CADocument76 pagesCurrent Affairs: 01st Jan To 10th Jan 2022 CAShubhendu VermaNo ratings yet

- RBI Master Circular Lending To Micro Small Medium Enterprises MSME Sector 2nd July 2012KALE LAW OFFICE CORPORATE LAWYER LAW FIR TAX CONSULTANTS COMPANY LAWYER 1Document7 pagesRBI Master Circular Lending To Micro Small Medium Enterprises MSME Sector 2nd July 2012KALE LAW OFFICE CORPORATE LAWYER LAW FIR TAX CONSULTANTS COMPANY LAWYER 1Divya MewaraNo ratings yet

- Fund Front Office: Definition: Cash Reserve Ratio (CRR) in Terms of Section 42 (1) of The Reserve Bank of India ActDocument17 pagesFund Front Office: Definition: Cash Reserve Ratio (CRR) in Terms of Section 42 (1) of The Reserve Bank of India ActSouravMalikNo ratings yet

- PR689DLDocument17 pagesPR689DLDirector Bal JyotiNo ratings yet

- CCP Rbi Jul-Dec'23Document21 pagesCCP Rbi Jul-Dec'23RaviTuduNo ratings yet

- Digital Lending GuidelinesDocument6 pagesDigital Lending GuidelinesabhinavNo ratings yet

- What Are NBFCS?: Page - 1Document3 pagesWhat Are NBFCS?: Page - 1AYUSHI TYAGINo ratings yet

- Important Acts Revised CTFC 2 Nov 16Document44 pagesImportant Acts Revised CTFC 2 Nov 16Ankith BNo ratings yet

- Master Circular - Bank Finance To Non-Banking Financial Companies (NBFCS)Document10 pagesMaster Circular - Bank Finance To Non-Banking Financial Companies (NBFCS)yogendrachat4057No ratings yet

- 13-Role and Functions of Non-Regulatory Financial Institutions-01!02!2024Document18 pages13-Role and Functions of Non-Regulatory Financial Institutions-01!02!2024PRASHANT PANDEYNo ratings yet

- RBI Circular Reg Bank Finance To NBFCDocument11 pagesRBI Circular Reg Bank Finance To NBFCopparasharNo ratings yet

- Master Circular - Bank Finance To Non-Banking Financial Companies (NBFCS)Document10 pagesMaster Circular - Bank Finance To Non-Banking Financial Companies (NBFCS)HrishikeshNo ratings yet

- NBFC CompliancesDocument41 pagesNBFC CompliancesmuskanNo ratings yet

- RBI Issues Regulations Under The Amended Factoring Regulation Act, 2011Document1 pageRBI Issues Regulations Under The Amended Factoring Regulation Act, 2011Aayush GuptaNo ratings yet

- CMPCir1668 13 PDFDocument38 pagesCMPCir1668 13 PDFsunilNo ratings yet

- 503acf260214f PDFDocument16 pages503acf260214f PDFSiddhi KudalkarNo ratings yet

- Regulation of Marchet BankerDocument3 pagesRegulation of Marchet BankerAayush NamanNo ratings yet

- Mob NpaDocument44 pagesMob NpaParthNo ratings yet

- Guidelines On Credit Default Swaps (CDS) For Corporate BondsDocument15 pagesGuidelines On Credit Default Swaps (CDS) For Corporate BondsPsanitha RaoNo ratings yet

- Master Circular 01072009 - FactoringDocument28 pagesMaster Circular 01072009 - FactoringAlpana SrivastavaNo ratings yet

- Regulators Regulations Dec 2021Document44 pagesRegulators Regulations Dec 2021Ravi Shankar VermaNo ratings yet

- Module-III Banking Regulation: Course OutlineDocument36 pagesModule-III Banking Regulation: Course OutlineSanjay ParidaNo ratings yet

- Policy For Lending To Micro and Small EnterprisesDocument8 pagesPolicy For Lending To Micro and Small Enterprisespatruni sureshkumarNo ratings yet

- Loan RecoveryDocument62 pagesLoan RecoveryKaran Thakur100% (1)

- Supplement Professional Programme: For December, 2022 ExaminationDocument28 pagesSupplement Professional Programme: For December, 2022 ExaminationsukritiNo ratings yet

- NDTLDocument13 pagesNDTLPradeep PoojariNo ratings yet

- Updated Operational Circular For Issue and Listing of Commercial Paper - April 13 2022Document120 pagesUpdated Operational Circular For Issue and Listing of Commercial Paper - April 13 2022Vani PattnaikNo ratings yet

- Difference Between Banks & NBFCDocument8 pagesDifference Between Banks & NBFCSajesh BelmanNo ratings yet

- Banking & Economy PDF - September 2023 by AffairsCloud 1Document130 pagesBanking & Economy PDF - September 2023 by AffairsCloud 1Shivankshi TyagiNo ratings yet

- Banking & Finance 2022 - Jan To July - TopicWise PDF by AffairsCloud 7Document108 pagesBanking & Finance 2022 - Jan To July - TopicWise PDF by AffairsCloud 7rohit yadavNo ratings yet

- CRR-SLR in BanksDocument25 pagesCRR-SLR in BanksPrashant GargNo ratings yet

- Presentation On NBFCS: Submitted By: Manjoyt KaurDocument18 pagesPresentation On NBFCS: Submitted By: Manjoyt Kaurmanjot005No ratings yet

- Asg 3Document4 pagesAsg 3Mrugaja Gokhale AurangabadkarNo ratings yet

- Compliance Cert RBI Jan-Jun'23Document17 pagesCompliance Cert RBI Jan-Jun'23vishwesheswaran1No ratings yet

- Compliance RBI Circulars Jan'22-Jun'22Document46 pagesCompliance RBI Circulars Jan'22-Jun'22Gautam MehtaNo ratings yet

- U Uu Uupdate Pdate Pdate Pdate Pdate: B BB Bbanking Anking Anking Anking AnkingDocument16 pagesU Uu Uupdate Pdate Pdate Pdate Pdate: B BB Bbanking Anking Anking Anking AnkingAnjuRoseNo ratings yet

- Central Banking Indian Specific Issue - 0f6a19f9 9d1e 4830 87be 8557fe576fdbDocument13 pagesCentral Banking Indian Specific Issue - 0f6a19f9 9d1e 4830 87be 8557fe576fdbprachi bhattNo ratings yet

- Financial Services: A Seminar OnDocument34 pagesFinancial Services: A Seminar OnKrishna Chandran PallippuramNo ratings yet

- Reserve Bank of India - : The Ceos of The All-India Term Lending and Refinancing InstitutionsDocument64 pagesReserve Bank of India - : The Ceos of The All-India Term Lending and Refinancing InstitutionsrajivrajsNo ratings yet

- ABM RBI Jul-Dec'23Document14 pagesABM RBI Jul-Dec'23RaviTuduNo ratings yet

- NBFC ALM RBI GuidelinesDocument115 pagesNBFC ALM RBI GuidelinessrirammaliNo ratings yet

- Notes On NBFCDocument9 pagesNotes On NBFCgspkishore7953No ratings yet

- Management of Non-Performing Assets: Presentation by Mr. S. RaviDocument29 pagesManagement of Non-Performing Assets: Presentation by Mr. S. RaviRajesh MaddiNo ratings yet

- BFM Module C Chapter 18 Part IiDocument10 pagesBFM Module C Chapter 18 Part IifolinesNo ratings yet

- Para-Banking and ActivitiesDocument13 pagesPara-Banking and ActivitiesKiran Kapoor100% (1)

- Non Banking Financial InstitutionsDocument53 pagesNon Banking Financial InstitutionsVenkat RajuNo ratings yet

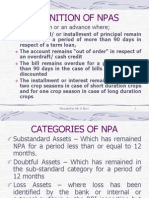

- Definition of Npas: A NPA Is A Loan or An Advance WhereDocument30 pagesDefinition of Npas: A NPA Is A Loan or An Advance WheremulchandranaNo ratings yet

- 22MCDocument63 pages22MCaspimpale1999No ratings yet

- Revised Guidelines On Credit Default Swaps (CDS) For Corporate BondsDocument15 pagesRevised Guidelines On Credit Default Swaps (CDS) For Corporate Bondsindrajit royNo ratings yet

- Master Directions On Prepaid Payment Instruments (PPIs) (Updated As On November 12, 2021)Document39 pagesMaster Directions On Prepaid Payment Instruments (PPIs) (Updated As On November 12, 2021)vaishaliNo ratings yet

- Financial Management AssignmentDocument12 pagesFinancial Management AssignmentrohanpujariNo ratings yet

- Cds Guidelines RBIDocument14 pagesCds Guidelines RBIJaiprakash ToshniwalNo ratings yet

- Policy Framework For Lending To MSE (Micro and Small Enterprises)Document7 pagesPolicy Framework For Lending To MSE (Micro and Small Enterprises)Pabitra Kumar PrustyNo ratings yet

- Note On Fund RaisingDocument5 pagesNote On Fund Raisingpranay boianapalliNo ratings yet

- CRFS RBI Circulars Jan'22-Jun'22Document19 pagesCRFS RBI Circulars Jan'22-Jun'22prahlad sharmaNo ratings yet

- Finance Current Affairs - January 2022 Week 1 Lyst4868Document30 pagesFinance Current Affairs - January 2022 Week 1 Lyst4868Bhav MathurNo ratings yet

- Government Schemes 2021-22 RBI Grade B 2022Document46 pagesGovernment Schemes 2021-22 RBI Grade B 2022Bhav MathurNo ratings yet

- PIB 247 Monthly PDF - March 2022Document52 pagesPIB 247 Monthly PDF - March 2022Bhav MathurNo ratings yet

- MONETARY POLICY 1 Lyst5834Document25 pagesMONETARY POLICY 1 Lyst5834Bhav MathurNo ratings yet

- Agriculture Infrastructure FundDocument15 pagesAgriculture Infrastructure FundBhav MathurNo ratings yet

- Finance Current Affairs May Week IiDocument18 pagesFinance Current Affairs May Week IiBhav MathurNo ratings yet

- Industrial Engineering - by LearnEngineering - inDocument197 pagesIndustrial Engineering - by LearnEngineering - inBhav MathurNo ratings yet

- Quant Checklist 85 PDF 2022 by Aashish AroraDocument78 pagesQuant Checklist 85 PDF 2022 by Aashish AroraBhav MathurNo ratings yet

- JUNE 2022 SPOTLIGHT Merged Lyst9919Document166 pagesJUNE 2022 SPOTLIGHT Merged Lyst9919Bhav MathurNo ratings yet

- Quant Checklist 81 PDF 2022 by Aashish AroraDocument78 pagesQuant Checklist 81 PDF 2022 by Aashish AroraBhav MathurNo ratings yet

- Quant Checklist 29 PDF 2022 by Aashish AroraDocument77 pagesQuant Checklist 29 PDF 2022 by Aashish AroraBhav MathurNo ratings yet

- Quant Checklist 19 PDF 2022 by Aashish AroraDocument71 pagesQuant Checklist 19 PDF 2022 by Aashish AroraBhav MathurNo ratings yet

- Case Competition GuideDocument49 pagesCase Competition GuidexxNo ratings yet

- Far210 Chap 2 Notes For Chapter 2Document11 pagesFar210 Chap 2 Notes For Chapter 2Nur ain Natasha ShaharudinNo ratings yet

- An Introduction To Financial System, Its Components: Unit 1Document16 pagesAn Introduction To Financial System, Its Components: Unit 1bhavyaNo ratings yet

- Audit of BPO & Construction Industry (Reviewer)Document8 pagesAudit of BPO & Construction Industry (Reviewer)PunkkaroNo ratings yet

- Index Executive Summary of Capital Markets Chapter 1 Investment BasicsDocument23 pagesIndex Executive Summary of Capital Markets Chapter 1 Investment Basicsswapnil_bNo ratings yet

- Fsa NotesDocument26 pagesFsa Notessanu sayedNo ratings yet

- Calgary Cooperative Funeral Services - Business PlanDocument21 pagesCalgary Cooperative Funeral Services - Business PlanastuteNo ratings yet

- Final ThesisDocument84 pagesFinal ThesisHari Sundar Kusi82% (11)

- Introduction To Financial Law NotesDocument10 pagesIntroduction To Financial Law Notesaustinmaina560No ratings yet

- UNIT 2 Company LawDocument34 pagesUNIT 2 Company Lawathought60No ratings yet

- Capital Structure and Leverages-ProblemsDocument7 pagesCapital Structure and Leverages-ProblemsUday GowdaNo ratings yet

- Fpo Bank of KathmanduDocument7 pagesFpo Bank of KathmanduPravin Sagar ThapaNo ratings yet

- 1.1 Financial PerformanceDocument132 pages1.1 Financial PerformanceGary ANo ratings yet

- Marris's Model of The Managerial Enterprise (With Diagrams)Document22 pagesMarris's Model of The Managerial Enterprise (With Diagrams)ndmudhosiNo ratings yet

- Financing DecisionDocument64 pagesFinancing DecisiontemekeNo ratings yet

- MM Theory of Capital StructureDocument12 pagesMM Theory of Capital StructureAliNo ratings yet

- Mediating Role Working Capital Management in Corporate Governance and Firm's PerformanceDocument5 pagesMediating Role Working Capital Management in Corporate Governance and Firm's PerformanceZahra زاهراNo ratings yet

- Chapter 02 - Test Bank: Multiple Choice QuestionsDocument23 pagesChapter 02 - Test Bank: Multiple Choice QuestionsKhang LeNo ratings yet

- CA Inter FM Short Theory by CA Aaditya Jain For Dec 21 Exam OnlyDocument35 pagesCA Inter FM Short Theory by CA Aaditya Jain For Dec 21 Exam OnlyJiya ChawlaNo ratings yet

- MBI 2020-2021 Corporate Finance Session 1 Course Outline Introduction To Corporate FinanceDocument92 pagesMBI 2020-2021 Corporate Finance Session 1 Course Outline Introduction To Corporate Financejonas sserumagaNo ratings yet

- Sources of Long-Term FinanceDocument17 pagesSources of Long-Term FinanceGaurav AgarwalNo ratings yet

- BSCPL Aurang Tollway LimitedDocument7 pagesBSCPL Aurang Tollway Limited10y.p.singh1010No ratings yet

- Inancial Arkets: Learning ObjectivesDocument24 pagesInancial Arkets: Learning Objectivessourav goyalNo ratings yet

- BUS 485 Life InsuranceDocument27 pagesBUS 485 Life InsuranceF.T. BhuiyanNo ratings yet

- Definations of Every Word Used in Stock Market To Be Known.............. Must READ - December 9th, 2007Document24 pagesDefinations of Every Word Used in Stock Market To Be Known.............. Must READ - December 9th, 2007rimolahaNo ratings yet

- Leverage and Capital StructureDocument14 pagesLeverage and Capital StructureQueenie AstilloNo ratings yet

- HSC Economics Distinguish & Agree-DisagreeDocument21 pagesHSC Economics Distinguish & Agree-DisagreeL.D TECHNICAL POINTNo ratings yet

- Financial Performance Analysis of Kotak Mahindra BankDocument60 pagesFinancial Performance Analysis of Kotak Mahindra Bankvaibhav pachputeNo ratings yet