Download as pdf or txt

You might also like

- Yamaha XT 125 Service ManualDocument279 pagesYamaha XT 125 Service ManualGeorge Petre77% (30)

- Car Owner Database - CL 8826460912Document3 pagesCar Owner Database - CL 8826460912mobile number database27% (11)

- Plugin 1 s2.0 S0167691198000127 Main PDFDocument7 pagesPlugin 1 s2.0 S0167691198000127 Main PDFUsef UsefiNo ratings yet

- Input Window Size and Neural Network Predictors: XT D FXTXT XT N XT D F T T XDocument8 pagesInput Window Size and Neural Network Predictors: XT D FXTXT XT N XT D F T T Xtamas_orban4546No ratings yet

- Avr Ieee Dc1Document6 pagesAvr Ieee Dc1Diego J. AlverniaNo ratings yet

- Xperm: Fast Index Canonicalization For Tensor Computer AlgebraDocument16 pagesXperm: Fast Index Canonicalization For Tensor Computer Algebraseppi05No ratings yet

- Time Series Prediction and Neural Networks: R.J.Frank, N.Davey, S.P.HuntDocument12 pagesTime Series Prediction and Neural Networks: R.J.Frank, N.Davey, S.P.HuntDiyar MuadhNo ratings yet

- XX Paper 24Document9 pagesXX Paper 24VindhyaNo ratings yet

- Quadrature em PDFDocument13 pagesQuadrature em PDF青山漫步No ratings yet

- A Polytopic Approach To Design Controllers For Networked LPV Control SystemsDocument7 pagesA Polytopic Approach To Design Controllers For Networked LPV Control SystemsLucasduhNo ratings yet

- Pattern Recognition By: Artificial Neural Networking (Ann)Document19 pagesPattern Recognition By: Artificial Neural Networking (Ann)Nikhil MahajanNo ratings yet

- Cs 316: Algorithms (Introduction) : SPRING 2015Document44 pagesCs 316: Algorithms (Introduction) : SPRING 2015Ahmed KhairyNo ratings yet

- Lab 1: Model SelectionDocument6 pagesLab 1: Model SelectionthomasverbekeNo ratings yet

- An Insight Into Noise Covariance Estimation For Kalman Filter DesignDocument6 pagesAn Insight Into Noise Covariance Estimation For Kalman Filter DesignAzhar IqbalNo ratings yet

- CDS 110b Norms of Signals and SystemsDocument10 pagesCDS 110b Norms of Signals and SystemsSatyavir YadavNo ratings yet

- Detect Abrupt System Changes Using Identification TechniquesDocument6 pagesDetect Abrupt System Changes Using Identification TechniquesPierpaolo VergatiNo ratings yet

- Algorithms For Arbitrary Precision Floating Point ArithmeticDocument25 pagesAlgorithms For Arbitrary Precision Floating Point ArithmetictrabajadosNo ratings yet

- Calibration Using GaDocument6 pagesCalibration Using GaDinesh KumarNo ratings yet

- Matlab Aided Control System Design - ConventionalDocument36 pagesMatlab Aided Control System Design - ConventionalGaacksonNo ratings yet

- Oerder Meyer PDFDocument8 pagesOerder Meyer PDFKarthik GowdaNo ratings yet

- Bosco en El Articulo MatematicoDocument10 pagesBosco en El Articulo MatematicoartovolastiNo ratings yet

- Ex 2 SolutionDocument13 pagesEx 2 SolutionMian AlmasNo ratings yet

- L Modeling In: Issing ObservatiDocument10 pagesL Modeling In: Issing Observatidearprasanta6015No ratings yet

- Analysis of AlgorithmsDocument43 pagesAnalysis of Algorithmsdogan20021907No ratings yet

- 1 s2.0 S1474667016348947 MainDocument6 pages1 s2.0 S1474667016348947 MainfhamdiNo ratings yet

- Modelado y CalibraciónDocument40 pagesModelado y Calibraciónandres_123456No ratings yet

- System Monitoring AND Control: Unit 7Document18 pagesSystem Monitoring AND Control: Unit 7vishal100% (1)

- 3481 PDFDocument8 pages3481 PDFChikh YassineNo ratings yet

- Approximate Frequency Counts Over Data StreamsDocument87 pagesApproximate Frequency Counts Over Data StreamsVidit PathakNo ratings yet

- Monte Carlo Simulation and QueuingDocument11 pagesMonte Carlo Simulation and QueuingNeel ShethNo ratings yet

- Algorithm and ComplexityDocument42 pagesAlgorithm and ComplexityRichyNo ratings yet

- Cs 6402 Design and Analysis of AlgorithmsDocument112 pagesCs 6402 Design and Analysis of Algorithmsvidhya_bineeshNo ratings yet

- Observadores Verghese SandersDocument10 pagesObservadores Verghese SandersJosé Moraes Gurgel NetoNo ratings yet

- Alvarez Is ADocument6 pagesAlvarez Is ADMarcus115No ratings yet

- Switched Observers For State and Parameter Estimation - 2014 - IFAC ProceedingsDocument6 pagesSwitched Observers For State and Parameter Estimation - 2014 - IFAC ProceedingsNguyễn Văn TrungNo ratings yet

- Square-Root Forms of The Minimum Output Energy Detector and EstimatorDocument4 pagesSquare-Root Forms of The Minimum Output Energy Detector and Estimatorsuchi87No ratings yet

- Chowyinlai 2011Document12 pagesChowyinlai 2011AlexandraNo ratings yet

- Module 4Document7 pagesModule 4WillykateKairuNo ratings yet

- Analysis of AlgorithmsDocument41 pagesAnalysis of Algorithmsgashaw asmamawNo ratings yet

- Estimation of Steady-State Power System Model ParametersDocument9 pagesEstimation of Steady-State Power System Model ParametersRonaldo PereiraNo ratings yet

- UNIT-8 Forms of Parallelism: 8.1 Simple Parallel Computation: Example 1: Numerical Integration Over Two VariablesDocument12 pagesUNIT-8 Forms of Parallelism: 8.1 Simple Parallel Computation: Example 1: Numerical Integration Over Two VariablesArshad ShaikNo ratings yet

- Nonlinear Regression Applied For Power Quality Disturbances Characterization in Grids With Wind GeneratorsDocument5 pagesNonlinear Regression Applied For Power Quality Disturbances Characterization in Grids With Wind GeneratorsSara AfzalNo ratings yet

- Practical Issues Implementing Analog-to-Information: ConvertersDocument6 pagesPractical Issues Implementing Analog-to-Information: ConvertersMimitech JohnNo ratings yet

- Identification of Reliability Models For Non RepaiDocument8 pagesIdentification of Reliability Models For Non RepaiEr Zubair HabibNo ratings yet

- Algorithm: - A Package For Estimation and Spectral Decomposition of Multivariate Autoregressive ModelsDocument6 pagesAlgorithm: - A Package For Estimation and Spectral Decomposition of Multivariate Autoregressive ModelsKush Kumar SinghNo ratings yet

- The Expectation-Maximization Algorithm: IEEE Signal Processing Magazine December 1996Document15 pagesThe Expectation-Maximization Algorithm: IEEE Signal Processing Magazine December 1996Anca DragoiNo ratings yet

- Lab 6Document9 pagesLab 6Muhammad Samay EllahiNo ratings yet

- CS8451 DAA PartA Q&A-new PDFDocument20 pagesCS8451 DAA PartA Q&A-new PDFMohan DasNo ratings yet

- Determination of Modal Residues and Residual Flexibility For Time-Domain System RealizationDocument31 pagesDetermination of Modal Residues and Residual Flexibility For Time-Domain System RealizationSamagassi SouleymaneNo ratings yet

- Chap21 SDocument55 pagesChap21 SRaghad AlnajimNo ratings yet

- Algorithms AnalysisDocument40 pagesAlgorithms AnalysisImaNo ratings yet

- Week - 1 - Daa - SMDocument28 pagesWeek - 1 - Daa - SMvidishashukla03No ratings yet

- CHAP1 enDocument45 pagesCHAP1 enDo DragonNo ratings yet

- European SemiconductorDocument14 pagesEuropean SemiconductorSimbhu Ashok CNo ratings yet

- Rao1988 PDFDocument10 pagesRao1988 PDFantonio ScacchiNo ratings yet

- Transmathematical BasisDocument10 pagesTransmathematical BasisviniciusmpsantosNo ratings yet

- Considerations About Establishing Mathematical Models Using System Identification ProceduresDocument4 pagesConsiderations About Establishing Mathematical Models Using System Identification ProceduresioncopaeNo ratings yet

- EM Algorithms For PCA and SPCADocument7 pagesEM Algorithms For PCA and SPCAMohamad NasrNo ratings yet

- Recursive Parameter Estimation of A Mechanical System in Frequency DomainDocument7 pagesRecursive Parameter Estimation of A Mechanical System in Frequency DomainFilippostanniNo ratings yet

- Arduino Measurements in Science: Advanced Techniques and Data ProjectsFrom EverandArduino Measurements in Science: Advanced Techniques and Data ProjectsNo ratings yet

- Application Note - XOR Gate Design PDFDocument5 pagesApplication Note - XOR Gate Design PDFTuan NguyenNo ratings yet

- What Is Direct Memory Access MDADocument1 pageWhat Is Direct Memory Access MDAJuan Ortega GuerraNo ratings yet

- Design Meets Technology Mora - Nova: © Med-Tronik GMBHDocument17 pagesDesign Meets Technology Mora - Nova: © Med-Tronik GMBHHaydar Ali FidanNo ratings yet

- How To Write An Effective Research Statement: TitleDocument4 pagesHow To Write An Effective Research Statement: TitlehabtamuNo ratings yet

- User ManualDocument13 pagesUser ManualAfonso D SantosNo ratings yet

- Product List Mega Global PratamaDocument9 pagesProduct List Mega Global Pratamaiman hilmanNo ratings yet

- 8chan Hacked PDFDocument192 pages8chan Hacked PDFOBEY GODNo ratings yet

- Earthing & PP MCQ Part 1Document6 pagesEarthing & PP MCQ Part 1Abhishek KumarNo ratings yet

- List of Polling Stations For Pec Election 2021-24Document8 pagesList of Polling Stations For Pec Election 2021-24Rasheed Shahwani0% (1)

- Wa0011.Document4 pagesWa0011.SHERYL SHEKINAH E ARCH-2019 BATCHNo ratings yet

- What Happens During Inbound Processing in SAP Embedded EWM?: External ProcurementDocument8 pagesWhat Happens During Inbound Processing in SAP Embedded EWM?: External ProcurementMohanish MurkuteNo ratings yet

- Input Output Symbolic Transition Systems EnrichedDocument25 pagesInput Output Symbolic Transition Systems EnrichedAlexey AbakumovNo ratings yet

- Contract Work Travel USA 2024Document6 pagesContract Work Travel USA 2024dilafruztursunboyeva9901No ratings yet

- Bu Grading SystemDocument37 pagesBu Grading Systemmanen gajoNo ratings yet

- 史都華平台之仿生物演算法模糊強化學習控制與FPGA實現Document99 pages史都華平台之仿生物演算法模糊強化學習控制與FPGA實現李金輝No ratings yet

- 2013 Sappia BollatiDocument7 pages2013 Sappia BollatiRakshithNo ratings yet

- As Relações Entre As Matas Ciliares, Os Rios e Os PeixesDocument22 pagesAs Relações Entre As Matas Ciliares, Os Rios e Os PeixesjogoalberNo ratings yet

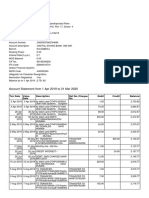

- Account Statement From 1 Apr 2019 To 31 Mar 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument7 pagesAccount Statement From 1 Apr 2019 To 31 Mar 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceawddNo ratings yet

- Resume Models in Ms Word FormatDocument8 pagesResume Models in Ms Word Formataflletwjp100% (1)

- Powerprotect DP Series Appliance Administration: Course DescriptionDocument3 pagesPowerprotect DP Series Appliance Administration: Course DescriptionSajuNo ratings yet

- Pressure Measurement: Objective of LessonDocument49 pagesPressure Measurement: Objective of LessonMohammad TahaNo ratings yet

- Study of Impact of Automation On Industry Employees Sonali JadhavDocument11 pagesStudy of Impact of Automation On Industry Employees Sonali Jadhavpallavimemane4No ratings yet

- Naukri DeepaRoyee (16y 0m)Document2 pagesNaukri DeepaRoyee (16y 0m)crazy admirerNo ratings yet

- Solving Quadratic EquationsDocument4 pagesSolving Quadratic EquationsHelen MylonaNo ratings yet

- Ibm SPSS: University of Eastern PhilippinesDocument5 pagesIbm SPSS: University of Eastern PhilippinesEdizon De Andres JaoNo ratings yet

- Information Systems in A Changing Economy and Society: MCIS2015 ProceedingsDocument490 pagesInformation Systems in A Changing Economy and Society: MCIS2015 ProceedingsDr. Hamad RazaNo ratings yet

- KPI - Akbar Pratama PutraDocument117 pagesKPI - Akbar Pratama PutraRifki Arie DarmawanNo ratings yet

- Technical Manual: Lodam Compressor Protection ModuleDocument18 pagesTechnical Manual: Lodam Compressor Protection ModuleHazem HassonNo ratings yet