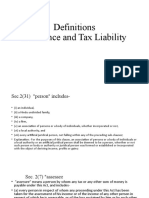

2 Residential Status

2 Residential Status

You might also like

- Sworn Statement of CapitalDocument2 pagesSworn Statement of CapitalBing Pon100% (1)

- Penyata Akaun: Tarikh Date Keterangan Description Terminal ID ID Terminal Amaun (RM) Amount (RM) Baki (RM) Balance (RM)Document2 pagesPenyata Akaun: Tarikh Date Keterangan Description Terminal ID ID Terminal Amaun (RM) Amount (RM) Baki (RM) Balance (RM)tamilselvi2907710No ratings yet

- Residential StatusDocument9 pagesResidential Statussadhana20bbaNo ratings yet

- Residential Status and Tax IncidenceDocument4 pagesResidential Status and Tax IncidenceAshok Kumar MehetaNo ratings yet

- Chapter-2 Residential StatusDocument5 pagesChapter-2 Residential StatusBrinda RNo ratings yet

- IT-02 Residential StatusDocument26 pagesIT-02 Residential StatusAkshat GoyalNo ratings yet

- Lesson 2 Residential Status & Scope of Total IncomeDocument27 pagesLesson 2 Residential Status & Scope of Total Income1A 10 ASWIN RNo ratings yet

- Residential Status and Scope of Total Income - AY 2023 - 24Document12 pagesResidential Status and Scope of Total Income - AY 2023 - 24Rajan SundararajanNo ratings yet

- Residential Status and Scope of Total IncomeDocument19 pagesResidential Status and Scope of Total IncomeSamyak JainNo ratings yet

- Residential Status and Tax IncidenceDocument3 pagesResidential Status and Tax IncidenceAshok Kumar Meheta0% (1)

- 1) Residential Status of An INDIVIDUAL Ans: Residential Status For Each Previous Year - Residential Status of An Assessee IsDocument14 pages1) Residential Status of An INDIVIDUAL Ans: Residential Status For Each Previous Year - Residential Status of An Assessee Isdhananjay7No ratings yet

- Residential Status DC 2023-24Document11 pagesResidential Status DC 2023-24avinashhpv7785No ratings yet

- Residential StatusDocument3 pagesResidential StatusMd DanishNo ratings yet

- R S T I: Esidence and Cope of Otal NcomeDocument5 pagesR S T I: Esidence and Cope of Otal NcomeMnk BhkNo ratings yet

- Residence in IndiaDocument7 pagesResidence in IndiaSuryaNo ratings yet

- Model Answers Law of TaxationDocument46 pagesModel Answers Law of Taxationlavkush1234No ratings yet

- Section 5 Which Defines The "Scope of Income" Section 6 Which Defines The "The Residential Status" of The PersonDocument8 pagesSection 5 Which Defines The "Scope of Income" Section 6 Which Defines The "The Residential Status" of The PersondipxxxNo ratings yet

- Residential StatusDocument7 pagesResidential StatusHimani AggarwalNo ratings yet

- 31162sm DTL Finalnew-May-Nov14 Cp2Document25 pages31162sm DTL Finalnew-May-Nov14 Cp2gvcNo ratings yet

- Model Answers Taxation 1. Residential Status of Assessee Under IT Act ?Document47 pagesModel Answers Taxation 1. Residential Status of Assessee Under IT Act ?Samata BohraNo ratings yet

- Model Answers Taxation 1. Residential Status of Assessee Under IT Act ?Document44 pagesModel Answers Taxation 1. Residential Status of Assessee Under IT Act ?Tejasvini KhemajiNo ratings yet

- 1328866787Chp 2 - Residence and Scope of Total IncomeDocument5 pages1328866787Chp 2 - Residence and Scope of Total IncomeMohiNo ratings yet

- Residence & Scope of Total IncomeDocument17 pagesResidence & Scope of Total IncomeSatyam Kumar AryaNo ratings yet

- Residential Status of Individuals Under Income Tax Act, 1961 - Taxguru - inDocument4 pagesResidential Status of Individuals Under Income Tax Act, 1961 - Taxguru - inSimran SinghNo ratings yet

- Law of Taxation Law of Taxation Class Notes CompressDocument48 pagesLaw of Taxation Law of Taxation Class Notes CompressThrishul MaheshNo ratings yet

- Residential Status: A Project On Residential Status in India and The Effects of Tax On It. Made By: Somrita PalDocument17 pagesResidential Status: A Project On Residential Status in India and The Effects of Tax On It. Made By: Somrita Palsousam2387No ratings yet

- Residential Status and Tax IncidenceDocument46 pagesResidential Status and Tax IncidenceÄbhíñävJäíñNo ratings yet

- Week 4 - Residence Based TaxationDocument31 pagesWeek 4 - Residence Based Taxationkabir kapoorNo ratings yet

- B71fedca 95fa 4b5b B32e A2fa493fbdeaDocument22 pagesB71fedca 95fa 4b5b B32e A2fa493fbdeaRaj DasNo ratings yet

- 3 - Basis of Charge, Scope of Total IncomeDocument165 pages3 - Basis of Charge, Scope of Total IncomeSaurin ThakkarNo ratings yet

- 4thSem-Taxation-1-Residential Status by Avinash K Prasad - 26Apr2020-DayDocument9 pages4thSem-Taxation-1-Residential Status by Avinash K Prasad - 26Apr2020-Dayvijay anandNo ratings yet

- Residence and Scope of Total Income: After Studying This Chapter, You Would Be Able ToDocument52 pagesResidence and Scope of Total Income: After Studying This Chapter, You Would Be Able ToAnkitaNo ratings yet

- Unit 3Document20 pagesUnit 3Ram KrishnaNo ratings yet

- CHAPTER:-1 Definitions U/s - 2, Basis of Charge and Exclusions From Total IncomeDocument12 pagesCHAPTER:-1 Definitions U/s - 2, Basis of Charge and Exclusions From Total IncomeshyamiliNo ratings yet

- Residential Status and Tax IncidenceDocument3 pagesResidential Status and Tax Incidenceambarishan mrNo ratings yet

- Residential Status and Tax LiabilityDocument2 pagesResidential Status and Tax LiabilityPrachi AlungNo ratings yet

- Residence and Scope of Total Income: After Studying This Chapter, You Would Be Able ToDocument17 pagesResidence and Scope of Total Income: After Studying This Chapter, You Would Be Able ToLilyNo ratings yet

- Residential Status (194-210)Document17 pagesResidential Status (194-210)Gaurav JhaNo ratings yet

- Residential Status: Presented ByDocument17 pagesResidential Status: Presented ByRohit SinghNo ratings yet

- Basis of ChargeDocument43 pagesBasis of ChargeArpit GoyalNo ratings yet

- 2 Residential Status PDFDocument10 pages2 Residential Status PDFGiri SukumarNo ratings yet

- Kishan Kumar Income Tax Amendments May2021Document6 pagesKishan Kumar Income Tax Amendments May2021ileshrathod0No ratings yet

- Definitions Residence and Tax LiabilityDocument23 pagesDefinitions Residence and Tax LiabilityVicky DNo ratings yet

- Residential Status ppt1Document17 pagesResidential Status ppt1Prasanna ReddyNo ratings yet

- Residential Status ppt1Document17 pagesResidential Status ppt1Reddy ReddyNo ratings yet

- MB FM 03 TAX PLANNING AND FINANCIAL REPORTING New-1Document70 pagesMB FM 03 TAX PLANNING AND FINANCIAL REPORTING New-1Khushboo SinghNo ratings yet

- Income Tax and Law UNIT-1 Part2Document26 pagesIncome Tax and Law UNIT-1 Part2rashmianand712No ratings yet

- Residential Status Under Income-Tax Act, 1961Document6 pagesResidential Status Under Income-Tax Act, 1961Bharat Tailor100% (1)

- It - Lesson 3Document14 pagesIt - Lesson 3Sugandha AgarwalNo ratings yet

- Concept of Residential StatusDocument7 pagesConcept of Residential StatusJanak DandNo ratings yet

- Income TaxDocument14 pagesIncome Taxankit srivastavaNo ratings yet

- e Book PDF PDFDocument91 pagese Book PDF PDFGiri SukumarNo ratings yet

- Residential StatusDocument33 pagesResidential StatusNovel Bipin Kr SawNo ratings yet

- Non Resident Indians Under FEMADocument4 pagesNon Resident Indians Under FEMAgaurav069No ratings yet

- Residential Status: Vaibhav BanjanDocument14 pagesResidential Status: Vaibhav Banjandeepika gawasNo ratings yet

- Chapter 11 - Residence and Scope of Total Income - NotesDocument14 pagesChapter 11 - Residence and Scope of Total Income - NotesAkshay PooniaNo ratings yet

- Residential Status: Vaibhav BanjanDocument14 pagesResidential Status: Vaibhav BanjanAnmolNo ratings yet

- Whoisannri?: Person Resident Outside India Means A Person Who Is Not Resident in IndiaDocument3 pagesWhoisannri?: Person Resident Outside India Means A Person Who Is Not Resident in Indiakrissh_87No ratings yet

- Chapter - Non Resident TaxationDocument162 pagesChapter - Non Resident TaxationsayanghoshNo ratings yet

- TTP Unit IDocument41 pagesTTP Unit IAafreen SiddiquiNo ratings yet

- Direct Tax Summary NotesDocument88 pagesDirect Tax Summary NotesAlisha LukeNo ratings yet

- Capital Budgeting - SOCDocument29 pagesCapital Budgeting - SOCVEDANT SAININo ratings yet

- Introduction To Corporate Finance - Unit 1Document21 pagesIntroduction To Corporate Finance - Unit 1VEDANT SAININo ratings yet

- Basic Concepts Bcom HonsDocument51 pagesBasic Concepts Bcom HonsVEDANT SAININo ratings yet

- Residential Status Practice Sums PY 21-22Document6 pagesResidential Status Practice Sums PY 21-22VEDANT SAININo ratings yet

- Classical Theory of Interest: Macro EconomicsDocument13 pagesClassical Theory of Interest: Macro EconomicsVEDANT SAININo ratings yet

- English Language AnalysisDocument15 pagesEnglish Language AnalysisVEDANT SAININo ratings yet

- Poaching: Original by Adam Lodge, Bo Love, Bowen Corbett, Jesse Fletcher, Chris Adams, & Charlie LeeDocument14 pagesPoaching: Original by Adam Lodge, Bo Love, Bowen Corbett, Jesse Fletcher, Chris Adams, & Charlie LeesachinderathkrNo ratings yet

- UST Faculty Union vs. Bitonio. GR No. 131235, Nov. 16, 1999Document7 pagesUST Faculty Union vs. Bitonio. GR No. 131235, Nov. 16, 1999Law SchoolNo ratings yet

- Inv MRK 2118 Mks SubDocument5 pagesInv MRK 2118 Mks SubM.Kurniawan.M 4DNo ratings yet

- Capitalism and Crises 1St Edition Colin Mayer Full ChapterDocument67 pagesCapitalism and Crises 1St Edition Colin Mayer Full Chapterrichard.harris150100% (7)

- TicketDocument2 pagesTicketShubham KaleNo ratings yet

- Gros, J. (2011) Failed States in Theoretical, Historical, and Policy PerspectivesDocument14 pagesGros, J. (2011) Failed States in Theoretical, Historical, and Policy PerspectivesManuel, Madeleine D.No ratings yet

- CARO TenderDocument100 pagesCARO Tenderpwdcd1No ratings yet

- Sworn Declaration of Being Affected by Calamity (HQP-HLF-453)Document1 pageSworn Declaration of Being Affected by Calamity (HQP-HLF-453)Angela CanaresNo ratings yet

- 038-16 Bir Ruling 191087-2016-Kyeryong - Construction - Industrial - Co. - Ltd.20190502-5466-1lm5il9Document4 pages038-16 Bir Ruling 191087-2016-Kyeryong - Construction - Industrial - Co. - Ltd.20190502-5466-1lm5il9KC AtinonNo ratings yet

- Terminations For Convenience - "You Want Me To Pay You What?"Document56 pagesTerminations For Convenience - "You Want Me To Pay You What?"Anonymous 94TBTBRksNo ratings yet

- Guidelines For Computation of MarksDocument5 pagesGuidelines For Computation of MarksLoolik SoliNo ratings yet

- Diamond V Diehr, Et Al. Us Supreme CourtDocument2 pagesDiamond V Diehr, Et Al. Us Supreme CourtPhi SalvadorNo ratings yet

- 1 Material Cross Cultural UnderstandingDocument31 pages1 Material Cross Cultural UnderstandingcyevicNo ratings yet

- MTD Decision Robert Ladd CEO MGT CapitalDocument35 pagesMTD Decision Robert Ladd CEO MGT CapitalTeri BuhlNo ratings yet

- DR Bima Arya Sugiarto Curriculum VitaeDocument4 pagesDR Bima Arya Sugiarto Curriculum VitaeAKADEMY OfficialNo ratings yet

- DISS Social ExperimentDocument4 pagesDISS Social ExperimentCatherine MOSQUITENo ratings yet

- The Criminal Law of The Consumer Protection On Sale Buy Online Through Mass MediaDocument9 pagesThe Criminal Law of The Consumer Protection On Sale Buy Online Through Mass MediaMaica ManguiatNo ratings yet

- LegEth - 2nd Exam CasesDocument234 pagesLegEth - 2nd Exam CasesAnonymous bMJQuUO8nNo ratings yet

- New Format of Consent LetterDocument1 pageNew Format of Consent LetterSrimanta Baboo100% (1)

- David W. Blight, Brooks D. Simpson - Union & Emancipation - Essays On Politics and Race in The Civil War Era-Kent State University Press (1997)Document500 pagesDavid W. Blight, Brooks D. Simpson - Union & Emancipation - Essays On Politics and Race in The Civil War Era-Kent State University Press (1997)Levente VajdaNo ratings yet

- Intellectual CapitalDocument3 pagesIntellectual CapitalMd Mehedi HasanNo ratings yet

- Caste Is A Closed Social Stratification System in Which Membership Is Determined by Birth and Remains Fixed For LifeDocument4 pagesCaste Is A Closed Social Stratification System in Which Membership Is Determined by Birth and Remains Fixed For LifeAbarna D S 19BLA1038No ratings yet

- Nexion Zine 1.1Document93 pagesNexion Zine 1.1Avy50% (2)

- Bangladesh CM - 2020 PDFDocument249 pagesBangladesh CM - 2020 PDF음종일No ratings yet

- Labour Law AamashDocument14 pagesLabour Law AamashAamash Ali10No ratings yet

- Practice Paper Revision SocialDocument2 pagesPractice Paper Revision SocialHussain AbbasNo ratings yet

- Definition and Nature of Law & Business LawDocument6 pagesDefinition and Nature of Law & Business LawMirza Ashef Aktab AnikNo ratings yet

Download as pdf or txt

You might also like

- Sworn Statement of CapitalDocument2 pagesSworn Statement of CapitalBing Pon100% (1)

- Penyata Akaun: Tarikh Date Keterangan Description Terminal ID ID Terminal Amaun (RM) Amount (RM) Baki (RM) Balance (RM)Document2 pagesPenyata Akaun: Tarikh Date Keterangan Description Terminal ID ID Terminal Amaun (RM) Amount (RM) Baki (RM) Balance (RM)tamilselvi2907710No ratings yet

- Residential StatusDocument9 pagesResidential Statussadhana20bbaNo ratings yet

- Residential Status and Tax IncidenceDocument4 pagesResidential Status and Tax IncidenceAshok Kumar MehetaNo ratings yet

- Chapter-2 Residential StatusDocument5 pagesChapter-2 Residential StatusBrinda RNo ratings yet

- IT-02 Residential StatusDocument26 pagesIT-02 Residential StatusAkshat GoyalNo ratings yet

- Lesson 2 Residential Status & Scope of Total IncomeDocument27 pagesLesson 2 Residential Status & Scope of Total Income1A 10 ASWIN RNo ratings yet

- Residential Status and Scope of Total Income - AY 2023 - 24Document12 pagesResidential Status and Scope of Total Income - AY 2023 - 24Rajan SundararajanNo ratings yet

- Residential Status and Scope of Total IncomeDocument19 pagesResidential Status and Scope of Total IncomeSamyak JainNo ratings yet

- Residential Status and Tax IncidenceDocument3 pagesResidential Status and Tax IncidenceAshok Kumar Meheta0% (1)

- 1) Residential Status of An INDIVIDUAL Ans: Residential Status For Each Previous Year - Residential Status of An Assessee IsDocument14 pages1) Residential Status of An INDIVIDUAL Ans: Residential Status For Each Previous Year - Residential Status of An Assessee Isdhananjay7No ratings yet

- Residential Status DC 2023-24Document11 pagesResidential Status DC 2023-24avinashhpv7785No ratings yet

- Residential StatusDocument3 pagesResidential StatusMd DanishNo ratings yet

- R S T I: Esidence and Cope of Otal NcomeDocument5 pagesR S T I: Esidence and Cope of Otal NcomeMnk BhkNo ratings yet

- Residence in IndiaDocument7 pagesResidence in IndiaSuryaNo ratings yet

- Model Answers Law of TaxationDocument46 pagesModel Answers Law of Taxationlavkush1234No ratings yet

- Section 5 Which Defines The "Scope of Income" Section 6 Which Defines The "The Residential Status" of The PersonDocument8 pagesSection 5 Which Defines The "Scope of Income" Section 6 Which Defines The "The Residential Status" of The PersondipxxxNo ratings yet

- Residential StatusDocument7 pagesResidential StatusHimani AggarwalNo ratings yet

- 31162sm DTL Finalnew-May-Nov14 Cp2Document25 pages31162sm DTL Finalnew-May-Nov14 Cp2gvcNo ratings yet

- Model Answers Taxation 1. Residential Status of Assessee Under IT Act ?Document47 pagesModel Answers Taxation 1. Residential Status of Assessee Under IT Act ?Samata BohraNo ratings yet

- Model Answers Taxation 1. Residential Status of Assessee Under IT Act ?Document44 pagesModel Answers Taxation 1. Residential Status of Assessee Under IT Act ?Tejasvini KhemajiNo ratings yet

- 1328866787Chp 2 - Residence and Scope of Total IncomeDocument5 pages1328866787Chp 2 - Residence and Scope of Total IncomeMohiNo ratings yet

- Residence & Scope of Total IncomeDocument17 pagesResidence & Scope of Total IncomeSatyam Kumar AryaNo ratings yet

- Residential Status of Individuals Under Income Tax Act, 1961 - Taxguru - inDocument4 pagesResidential Status of Individuals Under Income Tax Act, 1961 - Taxguru - inSimran SinghNo ratings yet

- Law of Taxation Law of Taxation Class Notes CompressDocument48 pagesLaw of Taxation Law of Taxation Class Notes CompressThrishul MaheshNo ratings yet

- Residential Status: A Project On Residential Status in India and The Effects of Tax On It. Made By: Somrita PalDocument17 pagesResidential Status: A Project On Residential Status in India and The Effects of Tax On It. Made By: Somrita Palsousam2387No ratings yet

- Residential Status and Tax IncidenceDocument46 pagesResidential Status and Tax IncidenceÄbhíñävJäíñNo ratings yet

- Week 4 - Residence Based TaxationDocument31 pagesWeek 4 - Residence Based Taxationkabir kapoorNo ratings yet

- B71fedca 95fa 4b5b B32e A2fa493fbdeaDocument22 pagesB71fedca 95fa 4b5b B32e A2fa493fbdeaRaj DasNo ratings yet

- 3 - Basis of Charge, Scope of Total IncomeDocument165 pages3 - Basis of Charge, Scope of Total IncomeSaurin ThakkarNo ratings yet

- 4thSem-Taxation-1-Residential Status by Avinash K Prasad - 26Apr2020-DayDocument9 pages4thSem-Taxation-1-Residential Status by Avinash K Prasad - 26Apr2020-Dayvijay anandNo ratings yet

- Residence and Scope of Total Income: After Studying This Chapter, You Would Be Able ToDocument52 pagesResidence and Scope of Total Income: After Studying This Chapter, You Would Be Able ToAnkitaNo ratings yet

- Unit 3Document20 pagesUnit 3Ram KrishnaNo ratings yet

- CHAPTER:-1 Definitions U/s - 2, Basis of Charge and Exclusions From Total IncomeDocument12 pagesCHAPTER:-1 Definitions U/s - 2, Basis of Charge and Exclusions From Total IncomeshyamiliNo ratings yet

- Residential Status and Tax IncidenceDocument3 pagesResidential Status and Tax Incidenceambarishan mrNo ratings yet

- Residential Status and Tax LiabilityDocument2 pagesResidential Status and Tax LiabilityPrachi AlungNo ratings yet

- Residence and Scope of Total Income: After Studying This Chapter, You Would Be Able ToDocument17 pagesResidence and Scope of Total Income: After Studying This Chapter, You Would Be Able ToLilyNo ratings yet

- Residential Status (194-210)Document17 pagesResidential Status (194-210)Gaurav JhaNo ratings yet

- Residential Status: Presented ByDocument17 pagesResidential Status: Presented ByRohit SinghNo ratings yet

- Basis of ChargeDocument43 pagesBasis of ChargeArpit GoyalNo ratings yet

- 2 Residential Status PDFDocument10 pages2 Residential Status PDFGiri SukumarNo ratings yet

- Kishan Kumar Income Tax Amendments May2021Document6 pagesKishan Kumar Income Tax Amendments May2021ileshrathod0No ratings yet

- Definitions Residence and Tax LiabilityDocument23 pagesDefinitions Residence and Tax LiabilityVicky DNo ratings yet

- Residential Status ppt1Document17 pagesResidential Status ppt1Prasanna ReddyNo ratings yet

- Residential Status ppt1Document17 pagesResidential Status ppt1Reddy ReddyNo ratings yet

- MB FM 03 TAX PLANNING AND FINANCIAL REPORTING New-1Document70 pagesMB FM 03 TAX PLANNING AND FINANCIAL REPORTING New-1Khushboo SinghNo ratings yet

- Income Tax and Law UNIT-1 Part2Document26 pagesIncome Tax and Law UNIT-1 Part2rashmianand712No ratings yet

- Residential Status Under Income-Tax Act, 1961Document6 pagesResidential Status Under Income-Tax Act, 1961Bharat Tailor100% (1)

- It - Lesson 3Document14 pagesIt - Lesson 3Sugandha AgarwalNo ratings yet

- Concept of Residential StatusDocument7 pagesConcept of Residential StatusJanak DandNo ratings yet

- Income TaxDocument14 pagesIncome Taxankit srivastavaNo ratings yet

- e Book PDF PDFDocument91 pagese Book PDF PDFGiri SukumarNo ratings yet

- Residential StatusDocument33 pagesResidential StatusNovel Bipin Kr SawNo ratings yet

- Non Resident Indians Under FEMADocument4 pagesNon Resident Indians Under FEMAgaurav069No ratings yet

- Residential Status: Vaibhav BanjanDocument14 pagesResidential Status: Vaibhav Banjandeepika gawasNo ratings yet

- Chapter 11 - Residence and Scope of Total Income - NotesDocument14 pagesChapter 11 - Residence and Scope of Total Income - NotesAkshay PooniaNo ratings yet

- Residential Status: Vaibhav BanjanDocument14 pagesResidential Status: Vaibhav BanjanAnmolNo ratings yet

- Whoisannri?: Person Resident Outside India Means A Person Who Is Not Resident in IndiaDocument3 pagesWhoisannri?: Person Resident Outside India Means A Person Who Is Not Resident in Indiakrissh_87No ratings yet

- Chapter - Non Resident TaxationDocument162 pagesChapter - Non Resident TaxationsayanghoshNo ratings yet

- TTP Unit IDocument41 pagesTTP Unit IAafreen SiddiquiNo ratings yet

- Direct Tax Summary NotesDocument88 pagesDirect Tax Summary NotesAlisha LukeNo ratings yet

- Capital Budgeting - SOCDocument29 pagesCapital Budgeting - SOCVEDANT SAININo ratings yet

- Introduction To Corporate Finance - Unit 1Document21 pagesIntroduction To Corporate Finance - Unit 1VEDANT SAININo ratings yet

- Basic Concepts Bcom HonsDocument51 pagesBasic Concepts Bcom HonsVEDANT SAININo ratings yet

- Residential Status Practice Sums PY 21-22Document6 pagesResidential Status Practice Sums PY 21-22VEDANT SAININo ratings yet

- Classical Theory of Interest: Macro EconomicsDocument13 pagesClassical Theory of Interest: Macro EconomicsVEDANT SAININo ratings yet

- English Language AnalysisDocument15 pagesEnglish Language AnalysisVEDANT SAININo ratings yet

- Poaching: Original by Adam Lodge, Bo Love, Bowen Corbett, Jesse Fletcher, Chris Adams, & Charlie LeeDocument14 pagesPoaching: Original by Adam Lodge, Bo Love, Bowen Corbett, Jesse Fletcher, Chris Adams, & Charlie LeesachinderathkrNo ratings yet

- UST Faculty Union vs. Bitonio. GR No. 131235, Nov. 16, 1999Document7 pagesUST Faculty Union vs. Bitonio. GR No. 131235, Nov. 16, 1999Law SchoolNo ratings yet

- Inv MRK 2118 Mks SubDocument5 pagesInv MRK 2118 Mks SubM.Kurniawan.M 4DNo ratings yet

- Capitalism and Crises 1St Edition Colin Mayer Full ChapterDocument67 pagesCapitalism and Crises 1St Edition Colin Mayer Full Chapterrichard.harris150100% (7)

- TicketDocument2 pagesTicketShubham KaleNo ratings yet

- Gros, J. (2011) Failed States in Theoretical, Historical, and Policy PerspectivesDocument14 pagesGros, J. (2011) Failed States in Theoretical, Historical, and Policy PerspectivesManuel, Madeleine D.No ratings yet

- CARO TenderDocument100 pagesCARO Tenderpwdcd1No ratings yet

- Sworn Declaration of Being Affected by Calamity (HQP-HLF-453)Document1 pageSworn Declaration of Being Affected by Calamity (HQP-HLF-453)Angela CanaresNo ratings yet

- 038-16 Bir Ruling 191087-2016-Kyeryong - Construction - Industrial - Co. - Ltd.20190502-5466-1lm5il9Document4 pages038-16 Bir Ruling 191087-2016-Kyeryong - Construction - Industrial - Co. - Ltd.20190502-5466-1lm5il9KC AtinonNo ratings yet

- Terminations For Convenience - "You Want Me To Pay You What?"Document56 pagesTerminations For Convenience - "You Want Me To Pay You What?"Anonymous 94TBTBRksNo ratings yet

- Guidelines For Computation of MarksDocument5 pagesGuidelines For Computation of MarksLoolik SoliNo ratings yet

- Diamond V Diehr, Et Al. Us Supreme CourtDocument2 pagesDiamond V Diehr, Et Al. Us Supreme CourtPhi SalvadorNo ratings yet

- 1 Material Cross Cultural UnderstandingDocument31 pages1 Material Cross Cultural UnderstandingcyevicNo ratings yet

- MTD Decision Robert Ladd CEO MGT CapitalDocument35 pagesMTD Decision Robert Ladd CEO MGT CapitalTeri BuhlNo ratings yet

- DR Bima Arya Sugiarto Curriculum VitaeDocument4 pagesDR Bima Arya Sugiarto Curriculum VitaeAKADEMY OfficialNo ratings yet

- DISS Social ExperimentDocument4 pagesDISS Social ExperimentCatherine MOSQUITENo ratings yet

- The Criminal Law of The Consumer Protection On Sale Buy Online Through Mass MediaDocument9 pagesThe Criminal Law of The Consumer Protection On Sale Buy Online Through Mass MediaMaica ManguiatNo ratings yet

- LegEth - 2nd Exam CasesDocument234 pagesLegEth - 2nd Exam CasesAnonymous bMJQuUO8nNo ratings yet

- New Format of Consent LetterDocument1 pageNew Format of Consent LetterSrimanta Baboo100% (1)

- David W. Blight, Brooks D. Simpson - Union & Emancipation - Essays On Politics and Race in The Civil War Era-Kent State University Press (1997)Document500 pagesDavid W. Blight, Brooks D. Simpson - Union & Emancipation - Essays On Politics and Race in The Civil War Era-Kent State University Press (1997)Levente VajdaNo ratings yet

- Intellectual CapitalDocument3 pagesIntellectual CapitalMd Mehedi HasanNo ratings yet

- Caste Is A Closed Social Stratification System in Which Membership Is Determined by Birth and Remains Fixed For LifeDocument4 pagesCaste Is A Closed Social Stratification System in Which Membership Is Determined by Birth and Remains Fixed For LifeAbarna D S 19BLA1038No ratings yet

- Nexion Zine 1.1Document93 pagesNexion Zine 1.1Avy50% (2)

- Bangladesh CM - 2020 PDFDocument249 pagesBangladesh CM - 2020 PDF음종일No ratings yet

- Labour Law AamashDocument14 pagesLabour Law AamashAamash Ali10No ratings yet

- Practice Paper Revision SocialDocument2 pagesPractice Paper Revision SocialHussain AbbasNo ratings yet

- Definition and Nature of Law & Business LawDocument6 pagesDefinition and Nature of Law & Business LawMirza Ashef Aktab AnikNo ratings yet