Download as pdf or txt

You might also like

- Accor - Graphic Guidelines - L050319Document105 pagesAccor - Graphic Guidelines - L050319Mohamed OmariNo ratings yet

- Application On Resident Engineer SingaporeDocument4 pagesApplication On Resident Engineer SingaporeIz ShafiNo ratings yet

- Self Reference CriterionDocument2 pagesSelf Reference CriterionJaemarie CamachoNo ratings yet

- Companies (Accounts) Amendment Rules, 2021 - Taxguru - inDocument4 pagesCompanies (Accounts) Amendment Rules, 2021 - Taxguru - inrsoni0043No ratings yet

- 14 - Company Audit Unit - 3Document38 pages14 - Company Audit Unit - 3Belgium PropertiesNo ratings yet

- Preparation of Financial Statements Under Companies Act 2013Document70 pagesPreparation of Financial Statements Under Companies Act 2013Atul SamalNo ratings yet

- Companies Accounts Rules 2014Document40 pagesCompanies Accounts Rules 2014srscribd10No ratings yet

- Electornic Records Companies ActDocument1 pageElectornic Records Companies Actharikishan chaudhryNo ratings yet

- Chapter 6 A4Document122 pagesChapter 6 A4Dhiraj JaiswalNo ratings yet

- Audit Trail - DetailedDocument49 pagesAudit Trail - DetailedAman JaiswalNo ratings yet

- Amendment Notes For CA (Intermediate) Nov. 2022 ExamsDocument5 pagesAmendment Notes For CA (Intermediate) Nov. 2022 Examssnehadagarsd19No ratings yet

- Audit Trail Summarised PresentationDocument23 pagesAudit Trail Summarised PresentationChirag GuptaNo ratings yet

- Revenue Regulations No. 09-09: Subject: TODocument16 pagesRevenue Regulations No. 09-09: Subject: TOAbigail SyNo ratings yet

- Accounts of Companies (128 - 138Document40 pagesAccounts of Companies (128 - 138praneet singhNo ratings yet

- T.V. GanesanDocument4 pagesT.V. Ganesanabc defNo ratings yet

- Advanced AuditingDocument50 pagesAdvanced AuditingKhalid SayedNo ratings yet

- RR 9-2009-Books of AccountsDocument0 pagesRR 9-2009-Books of AccountsBehappy FamiliesNo ratings yet

- Amendments 01 01 2023-31 12 2023Document12 pagesAmendments 01 01 2023-31 12 2023ANANYA SHETTYNo ratings yet

- Accounts of CompaniesDocument43 pagesAccounts of CompaniesSaurabh KumarNo ratings yet

- Evidentiary Value of Banker's BookDocument8 pagesEvidentiary Value of Banker's BookShatakshi SinghNo ratings yet

- CFR 21 Part 11 Audit SupportDocument29 pagesCFR 21 Part 11 Audit SupportWalter JaramilloNo ratings yet

- Admissibility of Electronic Evidence inDocument10 pagesAdmissibility of Electronic Evidence innatashaNo ratings yet

- Chapter-IX Account of CompaniesDocument47 pagesChapter-IX Account of CompaniesAbhinavSinghNo ratings yet

- RR 16-2006Document7 pagesRR 16-2006NarkSunderNo ratings yet

- eCFR: 21 CFR Part 11 - Electronic Records Electronic SignaturesDocument4 pageseCFR: 21 CFR Part 11 - Electronic Records Electronic SignaturesKateNo ratings yet

- Lecture Delivered During Training Programme For District Judges Under The Aegis of 13 Finance Commission Grant at Tamil Nadu State Judicial Academy On 26.03.2011Document17 pagesLecture Delivered During Training Programme For District Judges Under The Aegis of 13 Finance Commission Grant at Tamil Nadu State Judicial Academy On 26.03.2011Ashish RajNo ratings yet

- MBA Revised Chp-12 - Final Accounts of CompaniesDocument38 pagesMBA Revised Chp-12 - Final Accounts of CompaniesNitish rajNo ratings yet

- 1.accounts of CompaniesDocument12 pages1.accounts of CompaniesKarthik ImperiousNo ratings yet

- Leaving Audit Trail Is Mandatory For All Companies - From 1st April 2023Document3 pagesLeaving Audit Trail Is Mandatory For All Companies - From 1st April 2023visshelpNo ratings yet

- Policy For Preservation of Documents Archival 538d8883f7Document7 pagesPolicy For Preservation of Documents Archival 538d8883f7rajNo ratings yet

- Reporting Audit Trail FY 23-24Document29 pagesReporting Audit Trail FY 23-24rsoni0043No ratings yet

- Books of AccountDocument14 pagesBooks of Accountankit nandeNo ratings yet

- Revenue Regulations No 16-2006Document31 pagesRevenue Regulations No 16-2006Imb VillapandoNo ratings yet

- Chapter IDocument6 pagesChapter IAmit JainNo ratings yet

- Accounts of Companies: Learning OutcomesDocument69 pagesAccounts of Companies: Learning OutcomesHimanshu RaghuwanshiNo ratings yet

- Audit ReportDocument2 pagesAudit ReportXarmina GullNo ratings yet

- CFR - Code of Federal Regulations Title 21: FDA Home Medical Devices DatabasesDocument6 pagesCFR - Code of Federal Regulations Title 21: FDA Home Medical Devices DatabasesAndré AblaNo ratings yet

- A.8.1 Engagement Letter 31032023 - Statutory AuditDocument4 pagesA.8.1 Engagement Letter 31032023 - Statutory AuditAyush AgrawalNo ratings yet

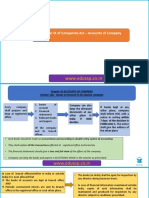

- WWW - Edutap.co - In: Chapter IX of Companies Act - Accounts of CompanyDocument15 pagesWWW - Edutap.co - In: Chapter IX of Companies Act - Accounts of Companyraahul dubeyNo ratings yet

- Manual For Patent Office Practice and ProcedureDocument174 pagesManual For Patent Office Practice and ProcedureSyed AhmedNo ratings yet

- 21 CFRDocument7 pages21 CFRishwarptl123No ratings yet

- Revenue Regulation 5-2014Document4 pagesRevenue Regulation 5-2014Clarissa Mae SawaliNo ratings yet

- Chapter 33 Caro-2020Document45 pagesChapter 33 Caro-2020ganesh PALNo ratings yet

- Accounts of CompaniesDocument4 pagesAccounts of CompaniesVishnu Teja AnnamrajuNo ratings yet

- 48343rr 9-2009Document8 pages48343rr 9-2009ChadUrginoAbarcaNo ratings yet

- Detailed Contents of As Based Schedule III BookDocument35 pagesDetailed Contents of As Based Schedule III BookanuragmandassociatesNo ratings yet

- PCC SoW GHB v2.0Document14 pagesPCC SoW GHB v2.0jch bpcNo ratings yet

- Advisory No. 002Document9 pagesAdvisory No. 002DOJ PPA R3No ratings yet

- Companies (Appointment and Qualification of Directors) Rules, 2014Document18 pagesCompanies (Appointment and Qualification of Directors) Rules, 2014Udwipt VermaNo ratings yet

- Commission On Audit: 2t/rp:uhlir NFDocument4 pagesCommission On Audit: 2t/rp:uhlir NFKatherine PacenoNo ratings yet

- COA CIRCULAR NO. 2023 006 August 2 2023Document9 pagesCOA CIRCULAR NO. 2023 006 August 2 2023Leah FlorentinoNo ratings yet

- CFR 21 Part 11Document7 pagesCFR 21 Part 11mblancolNo ratings yet

- CFR 21 Part 11 PDFDocument7 pagesCFR 21 Part 11 PDFmblancolNo ratings yet

- FDA 21 Part 11Document8 pagesFDA 21 Part 11Tuan NguyenNo ratings yet

- Standalone Financial StatementsDocument64 pagesStandalone Financial StatementsrahulNo ratings yet

- Appendix 2 - Letter of RepresentationDocument5 pagesAppendix 2 - Letter of Representationl.lawliet.ryuzaki.frNo ratings yet

- 21CFRPart11Compliance PDFDocument36 pages21CFRPart11Compliance PDFFachrurroziAs100% (1)

- Checklist For Accounting and Record MaintenanceDocument6 pagesChecklist For Accounting and Record Maintenancemukesh patelNo ratings yet

- Inter Law Amendments Notes Nov2022 Mohit PrajapatiDocument2 pagesInter Law Amendments Notes Nov2022 Mohit PrajapatiADARSH MISHRANo ratings yet

- Director RulesDocument17 pagesDirector RulesSOHAM DASNo ratings yet

- BIR RMO No. 9-2021Document11 pagesBIR RMO No. 9-2021Earl PatrickNo ratings yet

- Sirc Itgc 21062023Document46 pagesSirc Itgc 21062023MurthyNo ratings yet

- Cttplus HandbookDocument36 pagesCttplus HandbookgcarreongNo ratings yet

- Gate 2 ESPDocument10 pagesGate 2 ESPFran LordNo ratings yet

- Slides Chapter 3Document18 pagesSlides Chapter 3Reebeeccal LeeNo ratings yet

- Sist en 13726 1 2002Document9 pagesSist en 13726 1 2002NisaNo ratings yet

- UTAMU Procurement and Disposal of Assets Policy 2017Document46 pagesUTAMU Procurement and Disposal of Assets Policy 2017Abdulai WakoNo ratings yet

- SMK Bandaraya Kota Kinabalu English Language Lesson Plan: MondayDocument6 pagesSMK Bandaraya Kota Kinabalu English Language Lesson Plan: MondaySITI NORZUANI BINTI BAHARUDDIN MoeNo ratings yet

- Basic COMPETENCIES Module of InstructionDocument18 pagesBasic COMPETENCIES Module of InstructionMarveen TingkahanNo ratings yet

- Actividad Integradora 6. Opening Ceremony Name: Mariela Pérez Pardiño Adviser: Cristina Peña Rodriguez Group: M7C1G32-017 Date: 29/05/2022Document3 pagesActividad Integradora 6. Opening Ceremony Name: Mariela Pérez Pardiño Adviser: Cristina Peña Rodriguez Group: M7C1G32-017 Date: 29/05/2022marielaNo ratings yet

- The Gmo Emperor Has No Clothes PDFDocument251 pagesThe Gmo Emperor Has No Clothes PDFkouadio yao Armand100% (1)

- Instrumentation and Control of Heat ExchangerDocument29 pagesInstrumentation and Control of Heat Exchangerpra578No ratings yet

- Welder's Qualification Test CertificateDocument1 pageWelder's Qualification Test CertificatekannanNo ratings yet

- Preguntas Itil v3Document91 pagesPreguntas Itil v3Leo Duran TNo ratings yet

- 銘板貼紙新Document8 pages銘板貼紙新Nguyễn Hoàng SơnNo ratings yet

- Truck Evo Manual FinalDocument28 pagesTruck Evo Manual FinalRodrigo Zuñiga RosselNo ratings yet

- SECOND Periodic Test in AP 4 With TOS SY 2022 2023Document6 pagesSECOND Periodic Test in AP 4 With TOS SY 2022 2023MICHAEL VERINANo ratings yet

- Financial Services IBEFDocument34 pagesFinancial Services IBEFsanasarin1311No ratings yet

- MENTOR FEEDBACK FORM March 2022Document2 pagesMENTOR FEEDBACK FORM March 2022Darius NixNo ratings yet

- SD220511 01Document1 pageSD220511 01Minh TranNo ratings yet

- HMBD 50B Drain ManualDocument14 pagesHMBD 50B Drain Manualindra bayujagadNo ratings yet

- Impacts of Economic, Cultural, Social, Individual and Environmental Factors On Demands For Cinema: Case Study of TehranDocument15 pagesImpacts of Economic, Cultural, Social, Individual and Environmental Factors On Demands For Cinema: Case Study of Tehran14-Fy arts Div A Nikhil SharmaNo ratings yet

- 02 Kinematics Tutorial Solutions 2017Document12 pages02 Kinematics Tutorial Solutions 2017Victoria YongNo ratings yet

- Passenger/Itinerary Receipt: Electronic Ticket 220-2332362081Document2 pagesPassenger/Itinerary Receipt: Electronic Ticket 220-2332362081Dzeri LoganNo ratings yet

- Time Response AnalysisDocument43 pagesTime Response AnalysisAkmal IsnaeniNo ratings yet

- Economics:Presentation On Law of Equi Marginal Utility...Document11 pagesEconomics:Presentation On Law of Equi Marginal Utility...vinay rakshithNo ratings yet

- Internal Aids To Construction: Project BY: Mansi Verma 133/18Document18 pagesInternal Aids To Construction: Project BY: Mansi Verma 133/18Mansi VermaNo ratings yet

- Corrosión Manual NalcoDocument126 pagesCorrosión Manual NalcotinovelazquezNo ratings yet

- Lab Exercise No. 5 Mesh Analysis: Danica Marie Dumalagan, Kristoffer John Giganto, Jhury Kevin LastreDocument2 pagesLab Exercise No. 5 Mesh Analysis: Danica Marie Dumalagan, Kristoffer John Giganto, Jhury Kevin LastreKristoffer John GigantoNo ratings yet