Download as pdf or txt

You might also like

- Case Study #4 The Case of Joe and BlakeDocument3 pagesCase Study #4 The Case of Joe and BlakeJacques TuckerNo ratings yet

- Astm C469 - C469M - 14Document5 pagesAstm C469 - C469M - 14adil Rahman hassoon100% (1)

- Taxation and Tax Policies in the Middle East: Butterworths Studies in International Political EconomyFrom EverandTaxation and Tax Policies in the Middle East: Butterworths Studies in International Political EconomyRating: 5 out of 5 stars5/5 (1)

- Updated - Ooredoo at A Glance 2019Document11 pagesUpdated - Ooredoo at A Glance 2019AMR ERFANNo ratings yet

- China Vs India: Human Capital: Washington J. Wuttke April 2006Document26 pagesChina Vs India: Human Capital: Washington J. Wuttke April 2006PanvelNo ratings yet

- Agility Emerging Markets Logistics Index 2020 HighlightsDocument12 pagesAgility Emerging Markets Logistics Index 2020 Highlightsrafaelamorim34hNo ratings yet

- IFC SlidesDocument10 pagesIFC SlidesducvaNo ratings yet

- Malaria Elimination ProgramDocument37 pagesMalaria Elimination ProgramAbbi NathiNo ratings yet

- Estado Del Testing 2022Document29 pagesEstado Del Testing 2022Antu R. M.No ratings yet

- Competing For Investment Into Mining - Namibias Position in The Global ContextDocument13 pagesCompeting For Investment Into Mining - Namibias Position in The Global ContextNyanyu NoahNo ratings yet

- Advances in Spinning Preparation Technology.Document79 pagesAdvances in Spinning Preparation Technology.OUSMAN SEIDNo ratings yet

- Reg Science Conference Shenzhen 2023 01-14-23Document31 pagesReg Science Conference Shenzhen 2023 01-14-23Ajmeri KhatoonNo ratings yet

- NOC StrategiesDocument8 pagesNOC StrategiesThu NaNo ratings yet

- 2022 - 25 March Indocement Public Expose - FinalDocument35 pages2022 - 25 March Indocement Public Expose - FinalDecky PrayogaNo ratings yet

- VietNam Rice ExportDocument24 pagesVietNam Rice ExportTrang Uyên ĐàoNo ratings yet

- Cimigo Vietnam Consumer Trends 2021 5.pdf 5Document39 pagesCimigo Vietnam Consumer Trends 2021 5.pdf 5Nguyễn Thanh TùngNo ratings yet

- Cimigo Vietnam Consumer Trends 2021 5.PDF 5Document39 pagesCimigo Vietnam Consumer Trends 2021 5.PDF 5Ngọc DiệuNo ratings yet

- MOSL New Year Top Picks 2023Document19 pagesMOSL New Year Top Picks 2023dcpjimmy100% (1)

- Financial Results and Outlook: The Erawan GroupDocument30 pagesFinancial Results and Outlook: The Erawan GroupsozodaaaNo ratings yet

- Kingdom of MoroccoDocument53 pagesKingdom of MoroccoHafiz Kamran AhmedNo ratings yet

- The Indian Media & Entertainment Industry 2019: Trends & Analysis - Past, Present & FutureDocument63 pagesThe Indian Media & Entertainment Industry 2019: Trends & Analysis - Past, Present & FutureSharvari ShankarNo ratings yet

- Cairneagle - BESA Edtech SIG February 4th PresentationDocument39 pagesCairneagle - BESA Edtech SIG February 4th PresentationUtkarsh SinghNo ratings yet

- AAC060921 WillAcworthDocument31 pagesAAC060921 WillAcworthPrerna RaghuwanshiNo ratings yet

- Jari HietalaDocument49 pagesJari HietalaBùi Đăng NhậtNo ratings yet

- OTT Strategies To Acquire Subscribers in Developing MarketsDocument38 pagesOTT Strategies To Acquire Subscribers in Developing MarketsCARMEN ADRIANA CONTRERAS REYESNo ratings yet

- CBRE VN - ILS Quarterly Market Update (June 20)Document52 pagesCBRE VN - ILS Quarterly Market Update (June 20)Galih AnggoroNo ratings yet

- About QNB Group:: Market: Qatar Symbol: QNBK ISIN: QA0006929895 Industry: BanksDocument2 pagesAbout QNB Group:: Market: Qatar Symbol: QNBK ISIN: QA0006929895 Industry: Banksallaa mahmoudNo ratings yet

- Post Show Report 2018: VietnamDocument5 pagesPost Show Report 2018: VietnamjimmiilongNo ratings yet

- Icici Prudential Asset Allocator Fund PPT - Jan - Investor - 2021Document17 pagesIcici Prudential Asset Allocator Fund PPT - Jan - Investor - 2021hackmeatakashNo ratings yet

- Oryza Sativa: Rice - An IntroductionDocument33 pagesOryza Sativa: Rice - An IntroductionspachlangiyaNo ratings yet

- Welcomes You To The Exciting World of Export Import: Piem - 2020 (Copy Rights With Iiiem, Ahmedabad)Document19 pagesWelcomes You To The Exciting World of Export Import: Piem - 2020 (Copy Rights With Iiiem, Ahmedabad)Jeet BhuvaNo ratings yet

- 10-03-2008 Power in MEADocument30 pages10-03-2008 Power in MEAMohammed YusufNo ratings yet

- SKAGEN Kon Tiki MarchDocument83 pagesSKAGEN Kon Tiki MarchJosé Enrique MorenoNo ratings yet

- DIPM Presentation 27022016Document7 pagesDIPM Presentation 27022016Kanchanit BangthamaiNo ratings yet

- Dangote Cement Presentation FY 2023 FinalDocument30 pagesDangote Cement Presentation FY 2023 FinalAdama JusticeNo ratings yet

- Talentonomics - 2016 - Detailed Methodology - of Talent GroomingDocument15 pagesTalentonomics - 2016 - Detailed Methodology - of Talent GroomingshashankNo ratings yet

- Global and Regional Economic Outlook: James P. WalshDocument16 pagesGlobal and Regional Economic Outlook: James P. WalshFebyyanita MirzaNo ratings yet

- 7 Module 5 Resolving Intellectual Property Disputes Outside The Courts Domain Name DisputeDocument50 pages7 Module 5 Resolving Intellectual Property Disputes Outside The Courts Domain Name DisputeАндрей СергеевичNo ratings yet

- Emirates TelecommunicationsDocument6 pagesEmirates TelecommunicationsSunil KumarNo ratings yet

- The Imd Mba: Master of Business Administration Class of 202Document22 pagesThe Imd Mba: Master of Business Administration Class of 202ahmadsohanNo ratings yet

- Fintech Opportunities in IndiaDocument13 pagesFintech Opportunities in IndiaApurb KumarNo ratings yet

- 2022explain q1 eDocument22 pages2022explain q1 eNithis SkNo ratings yet

- SSS 2020 Business Plan RHB BankDocument29 pagesSSS 2020 Business Plan RHB BankMichael MyintNo ratings yet

- TB Pkbaru 08Document33 pagesTB Pkbaru 08Boedak AngauNo ratings yet

- Dec 2018 VI Program - Participant Profile BookDocument24 pagesDec 2018 VI Program - Participant Profile BookJBNo ratings yet

- Za 2022 Deloitte Global Auto Consumer Study SA DataDocument34 pagesZa 2022 Deloitte Global Auto Consumer Study SA DataAndiswa NkosiNo ratings yet

- Grameenphone LTD.: Dilip Pal, CFODocument21 pagesGrameenphone LTD.: Dilip Pal, CFONazmul IslamNo ratings yet

- E-Commerce Overview: Russia 2019 & Outline For 2020Document15 pagesE-Commerce Overview: Russia 2019 & Outline For 2020Stepan SergeevNo ratings yet

- Vietjet 2018 Business Results - Audited v1Document31 pagesVietjet 2018 Business Results - Audited v1Nhi ChuNo ratings yet

- The Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureDocument56 pagesThe Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureAnkit TiwariNo ratings yet

- LPA Business Climate Survey 2021 FinalDocument23 pagesLPA Business Climate Survey 2021 FinalmohamedNo ratings yet

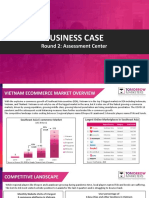

- Business Case: Round 2: Assessment CenterDocument9 pagesBusiness Case: Round 2: Assessment CenterMy Nguyen Thi Tra VOCFNo ratings yet

- MiceDocument9 pagesMicearun_gauravNo ratings yet

- Research Paper Vietnam S Competitive AdvantageDocument8 pagesResearch Paper Vietnam S Competitive AdvantageMinh PhúcNo ratings yet

- Autotech Automotive After Market Report 2022Document10 pagesAutotech Automotive After Market Report 2022ayman saberNo ratings yet

- McKinsey InovaçãoDocument28 pagesMcKinsey InovaçãoVasco Duarte BarbosaNo ratings yet

- Reliance Communications: Group 8 Presented By: Nichelle Kamath Mitali Mistry Komal Tambade - F65 Mansi Morajkar - F39Document31 pagesReliance Communications: Group 8 Presented By: Nichelle Kamath Mitali Mistry Komal Tambade - F65 Mansi Morajkar - F39sachinborade11997No ratings yet

- 2008 - Pyramid Research - VN Communication MarketDocument25 pages2008 - Pyramid Research - VN Communication MarketNam BuiNo ratings yet

- B P O Presentation 1Document20 pagesB P O Presentation 1vvikash100% (1)

- Beyond the Annual Budget: Global Experience with Medium Term Expenditure FrameworksFrom EverandBeyond the Annual Budget: Global Experience with Medium Term Expenditure FrameworksNo ratings yet

- International Debt Report 2022: Updated International Debt StatisticsFrom EverandInternational Debt Report 2022: Updated International Debt StatisticsNo ratings yet

- GovTech Maturity Index: The State of Public Sector Digital TransformationFrom EverandGovTech Maturity Index: The State of Public Sector Digital TransformationNo ratings yet

- 09.30 Bruno Fux INSEE EcocycleDocument19 pages09.30 Bruno Fux INSEE EcocycleParamananda SinghNo ratings yet

- 11.00 Paul Roger Exane BNP ParibasDocument41 pages11.00 Paul Roger Exane BNP ParibasParamananda SinghNo ratings yet

- 12.00 Kare Helge Karstensen SINTEFDocument137 pages12.00 Kare Helge Karstensen SINTEFParamananda SinghNo ratings yet

- 09.00 Hiroyuki Egawa Taiheiyo Cement CorporationDocument24 pages09.00 Hiroyuki Egawa Taiheiyo Cement CorporationParamananda SinghNo ratings yet

- Indonesia Cement Industry Updates 2020-2021: June 21 2021, Asosiasi Semen Indonesia Widodo SantosoDocument20 pagesIndonesia Cement Industry Updates 2020-2021: June 21 2021, Asosiasi Semen Indonesia Widodo SantosoParamananda SinghNo ratings yet

- 08.00 Raju Goyal CTO UltraTech CementDocument11 pages08.00 Raju Goyal CTO UltraTech CementParamananda SinghNo ratings yet

- Optimization of Rawmix design..NCCBMDocument9 pagesOptimization of Rawmix design..NCCBMParamananda SinghNo ratings yet

- S. Testing of Raw Materials: Method-1 (Using 0.5N Hci and 0.25N Naoh Solutions)Document5 pagesS. Testing of Raw Materials: Method-1 (Using 0.5N Hci and 0.25N Naoh Solutions)Paramananda SinghNo ratings yet

- GrandStream GXV-3175 - User Manual EnglishDocument130 pagesGrandStream GXV-3175 - User Manual Englishซิสทูยู ออนไลน์No ratings yet

- DIY GREENHOUSE by KMS - ChangelogDocument4 pagesDIY GREENHOUSE by KMS - Changeloglm pronNo ratings yet

- Free Batchography: The Art of Batch Files Programming PDF DownloadDocument2 pagesFree Batchography: The Art of Batch Files Programming PDF Downloadgeorge capozziNo ratings yet

- PSI Framework Components - EnglishDocument20 pagesPSI Framework Components - Englishalejandrosag0% (1)

- TATA MOTORS STP AnalysisDocument7 pagesTATA MOTORS STP AnalysisBharat RachuriNo ratings yet

- Front Office Final ExaminationDocument5 pagesFront Office Final ExaminationLeonardo FloresNo ratings yet

- Siliporite Opx Pellets Revision 11 - 2017Document2 pagesSiliporite Opx Pellets Revision 11 - 2017Juan Victor Sulvaran Arellano100% (2)

- Contaminants in Oils and Fats: Li D Lti Analysis and RegulationsDocument30 pagesContaminants in Oils and Fats: Li D Lti Analysis and RegulationsediasianagriNo ratings yet

- Sri Chaitanya IIT Academy, India: Grand Test-5Document31 pagesSri Chaitanya IIT Academy, India: Grand Test-5ashrithNo ratings yet

- 4 - 20140515034803 - 1 Coase, R.H. 1937 The Nature of The FirmDocument24 pages4 - 20140515034803 - 1 Coase, R.H. 1937 The Nature of The FirmFelicia AprilianiNo ratings yet

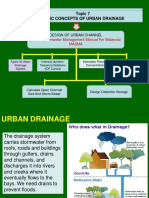

- Topic 7 Basic Concepts of Urban Drainage: (Urban Stormwater Management Manual For Malaysia) MasmaDocument29 pagesTopic 7 Basic Concepts of Urban Drainage: (Urban Stormwater Management Manual For Malaysia) MasmaAzhar SabriNo ratings yet

- Emma's Daily Routine - ReadingDocument2 pagesEmma's Daily Routine - ReadingEl Brayan'TVNo ratings yet

- Lab Manual DLD LabDocument113 pagesLab Manual DLD Labqudratullah ehsan0% (1)

- Mfx2550 Field Engineering ManualDocument415 pagesMfx2550 Field Engineering ManualJoeNo ratings yet

- The Great Gatsby (1925)Document100 pagesThe Great Gatsby (1925)Radu-Alexandru BulaiNo ratings yet

- (Oral Ana) Molars Gen CharacteristicsDocument24 pages(Oral Ana) Molars Gen CharacteristicsVT Superticioso Facto - TampusNo ratings yet

- HelicoptersDocument11 pagesHelicoptersJordan MosesNo ratings yet

- Dicrete StructureDocument125 pagesDicrete StructureVishal GojeNo ratings yet

- Curriculum Vitae: EducationDocument4 pagesCurriculum Vitae: EducationHetav MehtaNo ratings yet

- Symbiosis PresentationDocument7 pagesSymbiosis Presentationmisterbrowner@yahoo.com100% (1)

- Product Sheet Damen FCS 5009Document2 pagesProduct Sheet Damen FCS 5009Juan ResendizNo ratings yet

- CochinBase Tender E 13042021detailDocument27 pagesCochinBase Tender E 13042021detailisan.structural TjsvgalavanNo ratings yet

- Exadata and Database Machine Administration Workshop PDFDocument316 pagesExadata and Database Machine Administration Workshop PDFusman newtonNo ratings yet

- EDFD 211: Psychological Foundations in Education First Semester SY 2016-17 Course DescriptionDocument4 pagesEDFD 211: Psychological Foundations in Education First Semester SY 2016-17 Course DescriptionLeezl Campoamor OlegarioNo ratings yet

- GeM Bidding 4660207Document5 pagesGeM Bidding 4660207Hemanth KumarNo ratings yet

- UNIT-I (Sem-I) EVS - Environment & EcosystemDocument16 pagesUNIT-I (Sem-I) EVS - Environment & Ecosystemwalid ben aliNo ratings yet

- Form 5 ElectrolysisDocument2 pagesForm 5 ElectrolysisgrimyNo ratings yet

- AREVA in NigerDocument20 pagesAREVA in Nigermushava nyokaNo ratings yet