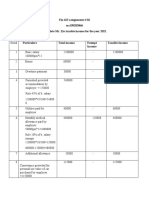

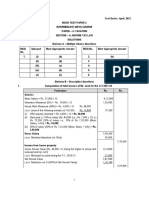

4.3 Solution To Income From Salary - Class Work & Home Assignment Questions

4.3 Solution To Income From Salary - Class Work & Home Assignment Questions

You might also like

- ACC 3013 - FWA - Revision - 202110Document14 pagesACC 3013 - FWA - Revision - 202110falnuaimi001No ratings yet

- Questions & Answers: 2 SalariesDocument26 pagesQuestions & Answers: 2 SalariesSabyasachi Ghosh67% (3)

- Internship Report On Finance Directorate of Hazara UniversityDocument96 pagesInternship Report On Finance Directorate of Hazara UniversityZubair Khan100% (1)

- Sms Sending Job DetailsDocument2 pagesSms Sending Job DetailsLofojayNo ratings yet

- Solution SalariesDocument16 pagesSolution SalariesAniket AgrawalNo ratings yet

- E1049217251 12520 1322185717213Document5 pagesE1049217251 12520 1322185717213Sumit PattanaikNo ratings yet

- 2.3 Solutions Module - 2 PDFDocument9 pages2.3 Solutions Module - 2 PDFArpita Artani100% (1)

- Salary IllustrationDocument10 pagesSalary IllustrationSarvar Pathan100% (1)

- Income Tax Tutorial QN 5Document4 pagesIncome Tax Tutorial QN 5dismas malekelaNo ratings yet

- Salary Mock Solution - March-24Document2 pagesSalary Mock Solution - March-24syedameerhamza762No ratings yet

- CTC Break Up - PGDM 1Document16 pagesCTC Break Up - PGDM 1piyush rawatNo ratings yet

- Direct Tax SLE-2 Roll No KSPMCAA012 Dev ShahDocument5 pagesDirect Tax SLE-2 Roll No KSPMCAA012 Dev ShahDev ShahNo ratings yet

- UCC E-Filling SolutionDocument5 pagesUCC E-Filling SolutionSibam BanikNo ratings yet

- Previous Year April To June July To March 2016-17 Nil 15000 2017-18 15000 16500 2018-19 16500 18000 2019-20 18000 19500Document4 pagesPrevious Year April To June July To March 2016-17 Nil 15000 2017-18 15000 16500 2018-19 16500 18000 2019-20 18000 19500Sumit PattanaikNo ratings yet

- Problems On Individual Taxation AY 2020-21 StudentsDocument9 pagesProblems On Individual Taxation AY 2020-21 StudentsAminul Islam RubelNo ratings yet

- Questions & Answers - Salary IncomeDocument14 pagesQuestions & Answers - Salary IncomeKiran BendeNo ratings yet

- Adobe Scan 11-Apr-2023Document4 pagesAdobe Scan 11-Apr-2023sanudutta191No ratings yet

- It 1Document18 pagesIt 1naheensyeda20No ratings yet

- THE State University of Zanzibar: Lecturer: Cpa Masoud Rashid Course: Taxation Group No: 3Document24 pagesTHE State University of Zanzibar: Lecturer: Cpa Masoud Rashid Course: Taxation Group No: 3tembo groupNo ratings yet

- Problems On Income From Salaries: Tax SupplementDocument20 pagesProblems On Income From Salaries: Tax SupplementJkNo ratings yet

- Principles of Taxation Solution # 3: Ans: 1 Year 1 Description Rs. Rs. Basic SalaryDocument7 pagesPrinciples of Taxation Solution # 3: Ans: 1 Year 1 Description Rs. Rs. Basic SalaryWarriach WarriachNo ratings yet

- Tax 2 RevisionDocument5 pagesTax 2 RevisionSoon Mei QiNo ratings yet

- Numerical Problems On Salary 1Document5 pagesNumerical Problems On Salary 1Shubham K RNo ratings yet

- Salary PDFDocument83 pagesSalary PDFGaurav BeniwalNo ratings yet

- Dit Sem V SolnDocument10 pagesDit Sem V Solnmaaz11052020No ratings yet

- 9.1 INCOME FROM PROPERTY Notes Questions With SolutionsDocument5 pages9.1 INCOME FROM PROPERTY Notes Questions With SolutionsHASNAT SABIRNo ratings yet

- Homework 1: D09, Q2 (B) (B) (I) Due Date For Submission of Tax ReturnDocument11 pagesHomework 1: D09, Q2 (B) (B) (I) Due Date For Submission of Tax ReturnBryan EngNo ratings yet

- Income From Salary Cosolidated ProblemsDocument6 pagesIncome From Salary Cosolidated ProblemsAndalNo ratings yet

- Fin 623 Assignment # 02 mc190203866 Calculate Mr. Zia Taxable Income For The Year 2021Document2 pagesFin 623 Assignment # 02 mc190203866 Calculate Mr. Zia Taxable Income For The Year 2021Abdussalam gillNo ratings yet

- Programme Subject Commerce Semester V Semester Session No. 42 Topic Problems On Taxable Salary Created by Prof Asharani, CDocument6 pagesProgramme Subject Commerce Semester V Semester Session No. 42 Topic Problems On Taxable Salary Created by Prof Asharani, Ctharunm451No ratings yet

- CH 2.TaxSalary IncomeDocument13 pagesCH 2.TaxSalary IncomeSajid AhmedNo ratings yet

- Fin - 623 Assignment 2Document5 pagesFin - 623 Assignment 2Abdussalam gillNo ratings yet

- T12 Ans 1 (I & Ii)Document1 pageT12 Ans 1 (I & Ii)PUI TUNG CHONGNo ratings yet

- Method of Calculation of Relief U/s 89 (I)Document3 pagesMethod of Calculation of Relief U/s 89 (I)ssvrNo ratings yet

- Group 4-1Document326 pagesGroup 4-1Shohid TuhinNo ratings yet

- Tax 2 AnsDocument12 pagesTax 2 AnsCollege CollegeNo ratings yet

- Taxable Salary Problem With Solution Part 1Document2 pagesTaxable Salary Problem With Solution Part 1NagadeepaNo ratings yet

- The University of Hong Kong School of Business ACCT3107/BUSI0018 - Hong Kong Taxation Self Test Question - Personal Assessment (Answers)Document2 pagesThe University of Hong Kong School of Business ACCT3107/BUSI0018 - Hong Kong Taxation Self Test Question - Personal Assessment (Answers)Edwin LawNo ratings yet

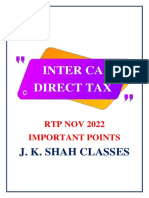

- RTP NOV 2022 Important PointsDocument4 pagesRTP NOV 2022 Important PointsDaniel TerstegenNo ratings yet

- Assignment TAX (21 AIS 039)Document18 pagesAssignment TAX (21 AIS 039)Amran OviNo ratings yet

- Salary Slip S5Document1 pageSalary Slip S5M.B TrickNo ratings yet

- Week 3 - Lecture Illustration SolutionDocument2 pagesWeek 3 - Lecture Illustration Solutionichika20010201No ratings yet

- Model Solution: Page 1 of 6Document6 pagesModel Solution: Page 1 of 6ShuvonathNo ratings yet

- SSF Not Listed-Monthly Salary Sheet With TDS Calculation 2076-2077Document29 pagesSSF Not Listed-Monthly Salary Sheet With TDS Calculation 2076-2077samNo ratings yet

- India NOV 2021Document1 pageIndia NOV 2021Sunil YadavNo ratings yet

- Salary Slip (32119327 April, 2019)Document1 pageSalary Slip (32119327 April, 2019)Hassan RanaNo ratings yet

- Tutorial 6 - Salaries TaxDocument5 pagesTutorial 6 - Salaries Tax周小荷No ratings yet

- SALARYDocument43 pagesSALARYDrishtiNo ratings yet

- India AUG 2021Document1 pageIndia AUG 2021Sunil YadavNo ratings yet

- Salary Slip (70003818 November, 2023)Document1 pageSalary Slip (70003818 November, 2023)ahnisariNo ratings yet

- India DEC 2021Document1 pageIndia DEC 2021Sunil YadavNo ratings yet

- Paper 4Document16 pagesPaper 4Kali KhannaNo ratings yet

- STT - Mock - Test - S-24 - Suggested AnswersDocument8 pagesSTT - Mock - Test - S-24 - Suggested AnswersabdullahNo ratings yet

- Income From SalaryDocument5 pagesIncome From Salarydbgdemo6No ratings yet

- Fifth PartDocument17 pagesFifth PartMahsinur RahmanNo ratings yet

- Income Tax Seminar Sum E21CO317Document2 pagesIncome Tax Seminar Sum E21CO317vidhyasri102003No ratings yet

- Employee BenefitsDocument20 pagesEmployee BenefitsKezNo ratings yet

- June TCSDocument1 pageJune TCSBandari GoverdhanNo ratings yet

- PayslipDocument1 pagePayslipSuyash RaulNo ratings yet

- CTC Structure FEB20Document2 pagesCTC Structure FEB20Wall Street Forex (WSFx)No ratings yet

- Total Cost To Company (TCTC) (A+B+C)Document1 pageTotal Cost To Company (TCTC) (A+B+C)Rahul AhujaNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- DDU-GKY Guidelines EngDocument68 pagesDDU-GKY Guidelines EngAmal KrishnaNo ratings yet

- Office of The Municipal Treasurer: Municipality of La TrinidadDocument3 pagesOffice of The Municipal Treasurer: Municipality of La TrinidadnormanNo ratings yet

- Sales ManagementDocument9 pagesSales ManagementrajeeevaNo ratings yet

- Emily Kate Slocum - H Argument EssayDocument7 pagesEmily Kate Slocum - H Argument Essayapi-692340121100% (1)

- UntitledDocument5 pagesUntitledjaved_hanif100% (1)

- ERECTORS INC. vs. NLRCDocument2 pagesERECTORS INC. vs. NLRCK Felix100% (2)

- PhilHealth Premium Contribution Table PDFDocument1 pagePhilHealth Premium Contribution Table PDFDaniel B. BalmoriNo ratings yet

- It Works For Me: Benefits@Wipro - Career Level B2 and B3Document2 pagesIt Works For Me: Benefits@Wipro - Career Level B2 and B3Jyotshna DhandNo ratings yet

- Hai Ramen Chapter 4Document10 pagesHai Ramen Chapter 4Jenessa BangheroNo ratings yet

- Accruals Questions - Further QuestionsDocument4 pagesAccruals Questions - Further QuestionsqasimNo ratings yet

- Budget - Instructions - 2024-25 FinalDocument53 pagesBudget - Instructions - 2024-25 FinaleerwshanamkondaNo ratings yet

- AC405 Dec 2019Document8 pagesAC405 Dec 2019hilton magagadaNo ratings yet

- Comp MGTDocument25 pagesComp MGTswatiaroranewdelhiNo ratings yet

- Ireland Versus The UKDocument9 pagesIreland Versus The UKSaidanNo ratings yet

- 7 Benchmarking Mercer 2010 MethodologyDocument17 pages7 Benchmarking Mercer 2010 MethodologyAdelina Ade100% (2)

- Office Administration SBA2222Document29 pagesOffice Administration SBA2222abbyplexx0% (1)

- Final Placement Report-2021-23 (Audited)Document18 pagesFinal Placement Report-2021-23 (Audited)Pratik RajNo ratings yet

- Compensation System of Berger Paints BanDocument18 pagesCompensation System of Berger Paints BanNur Nahar LimaNo ratings yet

- Operating CostingDocument6 pagesOperating CostingAvilash Vishal MishraNo ratings yet

- Job Evaluation Handbook (Soft Launch)Document6 pagesJob Evaluation Handbook (Soft Launch)marose_gobNo ratings yet

- Subcontinent Tax HistoryDocument3 pagesSubcontinent Tax HistoryWajih Ul hassanNo ratings yet

- GROUP ASSIGNMENT Managerial EconomicsDocument26 pagesGROUP ASSIGNMENT Managerial Economicsmahedre100% (1)

- National Trust For The Welfare of Persons With Autism Cerebral Palsy Mental Retardation and Multiple Disabilities Rules 2000Document62 pagesNational Trust For The Welfare of Persons With Autism Cerebral Palsy Mental Retardation and Multiple Disabilities Rules 2000Latest Laws TeamNo ratings yet

- 14) Aliling v. FelicianoDocument20 pages14) Aliling v. FelicianoVictoria EscobalNo ratings yet

- Recruitment Metrics at TQR SolutionsDocument2 pagesRecruitment Metrics at TQR SolutionsAnkitNo ratings yet

- The Level of Empowerment of Overseas Filipino Women WorkersDocument82 pagesThe Level of Empowerment of Overseas Filipino Women WorkersEsttie RadamNo ratings yet

- SERVICE CONTRACT Activ Moving Rewards Union Manpower Services Unskilled WorkerDocument7 pagesSERVICE CONTRACT Activ Moving Rewards Union Manpower Services Unskilled WorkerStefan VrabieNo ratings yet

- Bureau of Fisheries v. COA (Digest)Document2 pagesBureau of Fisheries v. COA (Digest)Clyde TanNo ratings yet

Download as xlsx, pdf, or txt

You might also like

- ACC 3013 - FWA - Revision - 202110Document14 pagesACC 3013 - FWA - Revision - 202110falnuaimi001No ratings yet

- Questions & Answers: 2 SalariesDocument26 pagesQuestions & Answers: 2 SalariesSabyasachi Ghosh67% (3)

- Internship Report On Finance Directorate of Hazara UniversityDocument96 pagesInternship Report On Finance Directorate of Hazara UniversityZubair Khan100% (1)

- Sms Sending Job DetailsDocument2 pagesSms Sending Job DetailsLofojayNo ratings yet

- Solution SalariesDocument16 pagesSolution SalariesAniket AgrawalNo ratings yet

- E1049217251 12520 1322185717213Document5 pagesE1049217251 12520 1322185717213Sumit PattanaikNo ratings yet

- 2.3 Solutions Module - 2 PDFDocument9 pages2.3 Solutions Module - 2 PDFArpita Artani100% (1)

- Salary IllustrationDocument10 pagesSalary IllustrationSarvar Pathan100% (1)

- Income Tax Tutorial QN 5Document4 pagesIncome Tax Tutorial QN 5dismas malekelaNo ratings yet

- Salary Mock Solution - March-24Document2 pagesSalary Mock Solution - March-24syedameerhamza762No ratings yet

- CTC Break Up - PGDM 1Document16 pagesCTC Break Up - PGDM 1piyush rawatNo ratings yet

- Direct Tax SLE-2 Roll No KSPMCAA012 Dev ShahDocument5 pagesDirect Tax SLE-2 Roll No KSPMCAA012 Dev ShahDev ShahNo ratings yet

- UCC E-Filling SolutionDocument5 pagesUCC E-Filling SolutionSibam BanikNo ratings yet

- Previous Year April To June July To March 2016-17 Nil 15000 2017-18 15000 16500 2018-19 16500 18000 2019-20 18000 19500Document4 pagesPrevious Year April To June July To March 2016-17 Nil 15000 2017-18 15000 16500 2018-19 16500 18000 2019-20 18000 19500Sumit PattanaikNo ratings yet

- Problems On Individual Taxation AY 2020-21 StudentsDocument9 pagesProblems On Individual Taxation AY 2020-21 StudentsAminul Islam RubelNo ratings yet

- Questions & Answers - Salary IncomeDocument14 pagesQuestions & Answers - Salary IncomeKiran BendeNo ratings yet

- Adobe Scan 11-Apr-2023Document4 pagesAdobe Scan 11-Apr-2023sanudutta191No ratings yet

- It 1Document18 pagesIt 1naheensyeda20No ratings yet

- THE State University of Zanzibar: Lecturer: Cpa Masoud Rashid Course: Taxation Group No: 3Document24 pagesTHE State University of Zanzibar: Lecturer: Cpa Masoud Rashid Course: Taxation Group No: 3tembo groupNo ratings yet

- Problems On Income From Salaries: Tax SupplementDocument20 pagesProblems On Income From Salaries: Tax SupplementJkNo ratings yet

- Principles of Taxation Solution # 3: Ans: 1 Year 1 Description Rs. Rs. Basic SalaryDocument7 pagesPrinciples of Taxation Solution # 3: Ans: 1 Year 1 Description Rs. Rs. Basic SalaryWarriach WarriachNo ratings yet

- Tax 2 RevisionDocument5 pagesTax 2 RevisionSoon Mei QiNo ratings yet

- Numerical Problems On Salary 1Document5 pagesNumerical Problems On Salary 1Shubham K RNo ratings yet

- Salary PDFDocument83 pagesSalary PDFGaurav BeniwalNo ratings yet

- Dit Sem V SolnDocument10 pagesDit Sem V Solnmaaz11052020No ratings yet

- 9.1 INCOME FROM PROPERTY Notes Questions With SolutionsDocument5 pages9.1 INCOME FROM PROPERTY Notes Questions With SolutionsHASNAT SABIRNo ratings yet

- Homework 1: D09, Q2 (B) (B) (I) Due Date For Submission of Tax ReturnDocument11 pagesHomework 1: D09, Q2 (B) (B) (I) Due Date For Submission of Tax ReturnBryan EngNo ratings yet

- Income From Salary Cosolidated ProblemsDocument6 pagesIncome From Salary Cosolidated ProblemsAndalNo ratings yet

- Fin 623 Assignment # 02 mc190203866 Calculate Mr. Zia Taxable Income For The Year 2021Document2 pagesFin 623 Assignment # 02 mc190203866 Calculate Mr. Zia Taxable Income For The Year 2021Abdussalam gillNo ratings yet

- Programme Subject Commerce Semester V Semester Session No. 42 Topic Problems On Taxable Salary Created by Prof Asharani, CDocument6 pagesProgramme Subject Commerce Semester V Semester Session No. 42 Topic Problems On Taxable Salary Created by Prof Asharani, Ctharunm451No ratings yet

- CH 2.TaxSalary IncomeDocument13 pagesCH 2.TaxSalary IncomeSajid AhmedNo ratings yet

- Fin - 623 Assignment 2Document5 pagesFin - 623 Assignment 2Abdussalam gillNo ratings yet

- T12 Ans 1 (I & Ii)Document1 pageT12 Ans 1 (I & Ii)PUI TUNG CHONGNo ratings yet

- Method of Calculation of Relief U/s 89 (I)Document3 pagesMethod of Calculation of Relief U/s 89 (I)ssvrNo ratings yet

- Group 4-1Document326 pagesGroup 4-1Shohid TuhinNo ratings yet

- Tax 2 AnsDocument12 pagesTax 2 AnsCollege CollegeNo ratings yet

- Taxable Salary Problem With Solution Part 1Document2 pagesTaxable Salary Problem With Solution Part 1NagadeepaNo ratings yet

- The University of Hong Kong School of Business ACCT3107/BUSI0018 - Hong Kong Taxation Self Test Question - Personal Assessment (Answers)Document2 pagesThe University of Hong Kong School of Business ACCT3107/BUSI0018 - Hong Kong Taxation Self Test Question - Personal Assessment (Answers)Edwin LawNo ratings yet

- RTP NOV 2022 Important PointsDocument4 pagesRTP NOV 2022 Important PointsDaniel TerstegenNo ratings yet

- Assignment TAX (21 AIS 039)Document18 pagesAssignment TAX (21 AIS 039)Amran OviNo ratings yet

- Salary Slip S5Document1 pageSalary Slip S5M.B TrickNo ratings yet

- Week 3 - Lecture Illustration SolutionDocument2 pagesWeek 3 - Lecture Illustration Solutionichika20010201No ratings yet

- Model Solution: Page 1 of 6Document6 pagesModel Solution: Page 1 of 6ShuvonathNo ratings yet

- SSF Not Listed-Monthly Salary Sheet With TDS Calculation 2076-2077Document29 pagesSSF Not Listed-Monthly Salary Sheet With TDS Calculation 2076-2077samNo ratings yet

- India NOV 2021Document1 pageIndia NOV 2021Sunil YadavNo ratings yet

- Salary Slip (32119327 April, 2019)Document1 pageSalary Slip (32119327 April, 2019)Hassan RanaNo ratings yet

- Tutorial 6 - Salaries TaxDocument5 pagesTutorial 6 - Salaries Tax周小荷No ratings yet

- SALARYDocument43 pagesSALARYDrishtiNo ratings yet

- India AUG 2021Document1 pageIndia AUG 2021Sunil YadavNo ratings yet

- Salary Slip (70003818 November, 2023)Document1 pageSalary Slip (70003818 November, 2023)ahnisariNo ratings yet

- India DEC 2021Document1 pageIndia DEC 2021Sunil YadavNo ratings yet

- Paper 4Document16 pagesPaper 4Kali KhannaNo ratings yet

- STT - Mock - Test - S-24 - Suggested AnswersDocument8 pagesSTT - Mock - Test - S-24 - Suggested AnswersabdullahNo ratings yet

- Income From SalaryDocument5 pagesIncome From Salarydbgdemo6No ratings yet

- Fifth PartDocument17 pagesFifth PartMahsinur RahmanNo ratings yet

- Income Tax Seminar Sum E21CO317Document2 pagesIncome Tax Seminar Sum E21CO317vidhyasri102003No ratings yet

- Employee BenefitsDocument20 pagesEmployee BenefitsKezNo ratings yet

- June TCSDocument1 pageJune TCSBandari GoverdhanNo ratings yet

- PayslipDocument1 pagePayslipSuyash RaulNo ratings yet

- CTC Structure FEB20Document2 pagesCTC Structure FEB20Wall Street Forex (WSFx)No ratings yet

- Total Cost To Company (TCTC) (A+B+C)Document1 pageTotal Cost To Company (TCTC) (A+B+C)Rahul AhujaNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- DDU-GKY Guidelines EngDocument68 pagesDDU-GKY Guidelines EngAmal KrishnaNo ratings yet

- Office of The Municipal Treasurer: Municipality of La TrinidadDocument3 pagesOffice of The Municipal Treasurer: Municipality of La TrinidadnormanNo ratings yet

- Sales ManagementDocument9 pagesSales ManagementrajeeevaNo ratings yet

- Emily Kate Slocum - H Argument EssayDocument7 pagesEmily Kate Slocum - H Argument Essayapi-692340121100% (1)

- UntitledDocument5 pagesUntitledjaved_hanif100% (1)

- ERECTORS INC. vs. NLRCDocument2 pagesERECTORS INC. vs. NLRCK Felix100% (2)

- PhilHealth Premium Contribution Table PDFDocument1 pagePhilHealth Premium Contribution Table PDFDaniel B. BalmoriNo ratings yet

- It Works For Me: Benefits@Wipro - Career Level B2 and B3Document2 pagesIt Works For Me: Benefits@Wipro - Career Level B2 and B3Jyotshna DhandNo ratings yet

- Hai Ramen Chapter 4Document10 pagesHai Ramen Chapter 4Jenessa BangheroNo ratings yet

- Accruals Questions - Further QuestionsDocument4 pagesAccruals Questions - Further QuestionsqasimNo ratings yet

- Budget - Instructions - 2024-25 FinalDocument53 pagesBudget - Instructions - 2024-25 FinaleerwshanamkondaNo ratings yet

- AC405 Dec 2019Document8 pagesAC405 Dec 2019hilton magagadaNo ratings yet

- Comp MGTDocument25 pagesComp MGTswatiaroranewdelhiNo ratings yet

- Ireland Versus The UKDocument9 pagesIreland Versus The UKSaidanNo ratings yet

- 7 Benchmarking Mercer 2010 MethodologyDocument17 pages7 Benchmarking Mercer 2010 MethodologyAdelina Ade100% (2)

- Office Administration SBA2222Document29 pagesOffice Administration SBA2222abbyplexx0% (1)

- Final Placement Report-2021-23 (Audited)Document18 pagesFinal Placement Report-2021-23 (Audited)Pratik RajNo ratings yet

- Compensation System of Berger Paints BanDocument18 pagesCompensation System of Berger Paints BanNur Nahar LimaNo ratings yet

- Operating CostingDocument6 pagesOperating CostingAvilash Vishal MishraNo ratings yet

- Job Evaluation Handbook (Soft Launch)Document6 pagesJob Evaluation Handbook (Soft Launch)marose_gobNo ratings yet

- Subcontinent Tax HistoryDocument3 pagesSubcontinent Tax HistoryWajih Ul hassanNo ratings yet

- GROUP ASSIGNMENT Managerial EconomicsDocument26 pagesGROUP ASSIGNMENT Managerial Economicsmahedre100% (1)

- National Trust For The Welfare of Persons With Autism Cerebral Palsy Mental Retardation and Multiple Disabilities Rules 2000Document62 pagesNational Trust For The Welfare of Persons With Autism Cerebral Palsy Mental Retardation and Multiple Disabilities Rules 2000Latest Laws TeamNo ratings yet

- 14) Aliling v. FelicianoDocument20 pages14) Aliling v. FelicianoVictoria EscobalNo ratings yet

- Recruitment Metrics at TQR SolutionsDocument2 pagesRecruitment Metrics at TQR SolutionsAnkitNo ratings yet

- The Level of Empowerment of Overseas Filipino Women WorkersDocument82 pagesThe Level of Empowerment of Overseas Filipino Women WorkersEsttie RadamNo ratings yet

- SERVICE CONTRACT Activ Moving Rewards Union Manpower Services Unskilled WorkerDocument7 pagesSERVICE CONTRACT Activ Moving Rewards Union Manpower Services Unskilled WorkerStefan VrabieNo ratings yet

- Bureau of Fisheries v. COA (Digest)Document2 pagesBureau of Fisheries v. COA (Digest)Clyde TanNo ratings yet