Download as pdf or txt

You might also like

- Vault Career Guide To Hedge FundsDocument224 pagesVault Career Guide To Hedge Fundssanfenqiu100% (1)

- Week 2 Tutorial Questions and SolutionsDocument3 pagesWeek 2 Tutorial Questions and Solutionsmuller1234No ratings yet

- Chapter 16Document17 pagesChapter 16Punit SharmaNo ratings yet

- Day 1Document11 pagesDay 1Abdullah EjazNo ratings yet

- The Finance Director of Stenigot Is Concerned About The LaxDocument1 pageThe Finance Director of Stenigot Is Concerned About The LaxAmit PandeyNo ratings yet

- Lahore School of Economics Financial Management II Assignment 6 Financial Planning & Forecasting - 1Document1 pageLahore School of Economics Financial Management II Assignment 6 Financial Planning & Forecasting - 1AhmedNo ratings yet

- BUSI 353 S18 Assignment 3 All RevenueDocument5 pagesBUSI 353 S18 Assignment 3 All RevenueTanNo ratings yet

- Task - Find Ps As Function ofDocument4 pagesTask - Find Ps As Function ofTinatini BakashviliNo ratings yet

- Week 1 - Problem SetDocument3 pagesWeek 1 - Problem SetIlpram YTNo ratings yet

- Wood Supply and Demand Analysis in PakistanDocument6 pagesWood Supply and Demand Analysis in PakistanMujtaba HaseebNo ratings yet

- E-14 AfrDocument5 pagesE-14 AfrInternational Iqbal ForumNo ratings yet

- 13 Standard CostingDocument32 pages13 Standard CostingMusthari KhanNo ratings yet

- Financial Reporting Final Mock: Barcelona Madrid Non-Current AssetsDocument7 pagesFinancial Reporting Final Mock: Barcelona Madrid Non-Current AssetsMuhammad AsadNo ratings yet

- Nov 06Document24 pagesNov 06Vascilly TerentievNo ratings yet

- Midlands State UniversityDocument11 pagesMidlands State UniversityIsheanesu MutusvaNo ratings yet

- IAS 02: Inventories: Requirement: SolutionDocument2 pagesIAS 02: Inventories: Requirement: SolutionMD Hafizul Islam Hafiz100% (1)

- Sources of Funding For MNC'sDocument22 pagesSources of Funding For MNC'sNeeraj Kumar80% (5)

- Question-1 I) : SKANS School of Accountancy Principles of Taxation Mid Term ExamDocument4 pagesQuestion-1 I) : SKANS School of Accountancy Principles of Taxation Mid Term ExamMuhammad ArslanNo ratings yet

- Chapter 13 PDFDocument73 pagesChapter 13 PDFMUKESH KUMARNo ratings yet

- 7 2006 Dec QDocument6 pages7 2006 Dec Qapi-19836745No ratings yet

- CAF-Business Economics PDFDocument40 pagesCAF-Business Economics PDFadnan sheikNo ratings yet

- Question Paper PDFDocument17 pagesQuestion Paper PDFSaianish KommuchikkalaNo ratings yet

- Midterm 5101Document4 pagesMidterm 5101MD Hafizul Islam HafizNo ratings yet

- Absor Pvt. LTDDocument4 pagesAbsor Pvt. LTDsam50% (2)

- November 2006 Examinations: Paper P1 - Management Accounting - Performance EvaluationDocument32 pagesNovember 2006 Examinations: Paper P1 - Management Accounting - Performance EvaluationKamisiro RizeNo ratings yet

- Lesson 9 Problems of Transfer Pricing Practical ExerciseDocument6 pagesLesson 9 Problems of Transfer Pricing Practical ExerciseMadhu kumarNo ratings yet

- December 2003 ACCA Paper 2.5 QuestionsDocument10 pagesDecember 2003 ACCA Paper 2.5 QuestionsUlanda20% (1)

- NN 5 Chap 4 Review of AccountingDocument10 pagesNN 5 Chap 4 Review of AccountingNguyet NguyenNo ratings yet

- Ilovepdf MergedDocument15 pagesIlovepdf MergedRakib KhanNo ratings yet

- Fma PaperDocument2 pagesFma Paperfishy18No ratings yet

- Working Capital AnalysisDocument9 pagesWorking Capital AnalysisDr Siddharth DarjiNo ratings yet

- Bba 122 Fai 11 AnswerDocument12 pagesBba 122 Fai 11 AnswerTomi Wayne Malenga100% (1)

- Individual Assignment Acct 232 Management Accounting 2Document3 pagesIndividual Assignment Acct 232 Management Accounting 2pfungwaNo ratings yet

- Chapter 02 - Basic Financial StatementsDocument139 pagesChapter 02 - Basic Financial StatementsElio BazNo ratings yet

- R175367E Tinashe Mambodza BSFB401 AssignmentDocument8 pagesR175367E Tinashe Mambodza BSFB401 AssignmentTinasheNo ratings yet

- Ratio Analysis of Eastern Bank LTD.: Bus 635 (Managerial Finance)Document19 pagesRatio Analysis of Eastern Bank LTD.: Bus 635 (Managerial Finance)shadmanNo ratings yet

- Soal-Soal Capital Budgeting # 1Document2 pagesSoal-Soal Capital Budgeting # 1Danang0% (2)

- CH 5 Bonds Book QuestionsDocument6 pagesCH 5 Bonds Book QuestionsSavy DhillonNo ratings yet

- 9706 w11 QP 21Document12 pages9706 w11 QP 21Diksha KoossoolNo ratings yet

- Financial Statements: Analysis of Attock Refinery LimitedDocument1 pageFinancial Statements: Analysis of Attock Refinery LimitedHasnain KharNo ratings yet

- Asset Recognition and Operating Assets: Fourth EditionDocument55 pagesAsset Recognition and Operating Assets: Fourth EditionAyush JainNo ratings yet

- Ias 1 & Ias 2-Bact-307-Admin-2019-1Document35 pagesIas 1 & Ias 2-Bact-307-Admin-2019-1Letsah BrightNo ratings yet

- Practice of Ratio Analysis Development of Financial StatementsDocument8 pagesPractice of Ratio Analysis Development of Financial StatementsZarish AzharNo ratings yet

- Ganesh Metal Industry Trial Balance, December 31, 2008 Account Debit (RS) Credit (RS)Document11 pagesGanesh Metal Industry Trial Balance, December 31, 2008 Account Debit (RS) Credit (RS)ayushsapkota907No ratings yet

- C.A Cost Acc P.PDocument29 pagesC.A Cost Acc P.PRaja Ubaid100% (1)

- ICAP MSA 1 AdditionalPracticeQuesDocument34 pagesICAP MSA 1 AdditionalPracticeQuesAsad TariqNo ratings yet

- Zica t1 Financial AccountingDocument363 pagesZica t1 Financial Accountinglord100% (2)

- Principles of Accounting PDFDocument2 pagesPrinciples of Accounting PDFfrank mutale0% (1)

- Ebit Eps AnalysisDocument11 pagesEbit Eps Analysismanish9890No ratings yet

- Adams Inc Acquires Clay Corporation On January 1 2012 inDocument1 pageAdams Inc Acquires Clay Corporation On January 1 2012 inMiroslav GegoskiNo ratings yet

- FIN1161 - Introduction To Finance For Business - Report 2Document6 pagesFIN1161 - Introduction To Finance For Business - Report 2thunlagbd230128No ratings yet

- CH 13Document28 pagesCH 13ReneeNo ratings yet

- Journal Entry.Document45 pagesJournal Entry.CHARAK RAYNo ratings yet

- f7 2014 Dec QDocument13 pagesf7 2014 Dec QAshraf ValappilNo ratings yet

- Accounting Principles Chapter OneDocument23 pagesAccounting Principles Chapter OneYyhh100% (1)

- Issues in Corporate GovernanceDocument15 pagesIssues in Corporate GovernanceVandana ŘwţNo ratings yet

- M 2012 June PDFDocument21 pagesM 2012 June PDFMoses LukNo ratings yet

- Corporate Financial Analysis with Microsoft ExcelFrom EverandCorporate Financial Analysis with Microsoft ExcelRating: 5 out of 5 stars5/5 (1)

- Value Chain Management Capability A Complete Guide - 2020 EditionFrom EverandValue Chain Management Capability A Complete Guide - 2020 EditionNo ratings yet

- RE Exam FA Sem I MFM MMM MHRDMDocument4 pagesRE Exam FA Sem I MFM MMM MHRDMPARAM CLOTHINGNo ratings yet

- Poa T - 11Document5 pagesPoa T - 11SHEVENA A/P VIJIANNo ratings yet

- Time Allowed: 3 Hours Max Marks: 100: Colleges 1st SimulationDocument3 pagesTime Allowed: 3 Hours Max Marks: 100: Colleges 1st SimulationKashifNo ratings yet

- PACRADocument516 pagesPACRABenjamin Banda100% (1)

- Companies and Business Booklet 2021Document65 pagesCompanies and Business Booklet 2021Benjamin BandaNo ratings yet

- Rockview University: School of Humaninities and Social SciencesDocument5 pagesRockview University: School of Humaninities and Social SciencesBenjamin BandaNo ratings yet

- Spe 111 BehaviorDocument3 pagesSpe 111 BehaviorBenjamin BandaNo ratings yet

- David LivingstonDocument4 pagesDavid LivingstonBenjamin BandaNo ratings yet

- Bantu MigrationDocument7 pagesBantu MigrationBenjamin BandaNo ratings yet

- Bureaucracy Is A System of Government in Which Most of The Important Decisions Are Taken by State Officials Rather Than by Elected RepresentativesDocument6 pagesBureaucracy Is A System of Government in Which Most of The Important Decisions Are Taken by State Officials Rather Than by Elected RepresentativesBenjamin BandaNo ratings yet

- Shipping Agents - Freight ForwardersDocument48 pagesShipping Agents - Freight ForwardersKunwar Saigal100% (1)

- A Complete Guide To Volume Price Analysis Read The Book Then Read The Market by Anna Coulling (Z-Lib - Org) (241-273)Document33 pagesA Complete Guide To Volume Price Analysis Read The Book Then Read The Market by Anna Coulling (Z-Lib - Org) (241-273)Getulio José Mattos Do Amaral FilhoNo ratings yet

- Letter To The Mayor and City ManagerDocument2 pagesLetter To The Mayor and City ManagerCincinnatiEnquirerNo ratings yet

- KP Gxie-1Document41 pagesKP Gxie-1Muhammad AswanNo ratings yet

- Trade Expose Final PDFDocument19 pagesTrade Expose Final PDFGhizwaNo ratings yet

- Daniel D. AbshirDocument60 pagesDaniel D. AbshirberiNo ratings yet

- Capitec Fees 2023Document4 pagesCapitec Fees 2023bok kopNo ratings yet

- KPK MRS-2020 PDFDocument411 pagesKPK MRS-2020 PDFKalsoom Khan100% (4)

- Literature Review On Debt FinancingDocument4 pagesLiterature Review On Debt Financingafmzzaadfjygyf100% (1)

- Pref 4 Listening 1 4 Revision Del IntentoDocument2 pagesPref 4 Listening 1 4 Revision Del IntentosdsdsNo ratings yet

- B1-1.MAINPAPER-Steel For Sustainable Development-AdeAjayiDocument7 pagesB1-1.MAINPAPER-Steel For Sustainable Development-AdeAjayiDonald rayNo ratings yet

- GE 3 - Reviewer THE CONTEMPORARY WORLDDocument7 pagesGE 3 - Reviewer THE CONTEMPORARY WORLDKissey EstrellaNo ratings yet

- 03 18 2021 PNL Faelnar, Queenie JoyDocument1 page03 18 2021 PNL Faelnar, Queenie JoyKweeng Tayrus FaelnarNo ratings yet

- GM 06Document3 pagesGM 06ivofimfNo ratings yet

- Handout 3 - 4 - Review Exercises - Questions in TextDocument6 pagesHandout 3 - 4 - Review Exercises - Questions in Text6kb4nm24vjNo ratings yet

- 21-2 ECO 501 - Assignment 1Document3 pages21-2 ECO 501 - Assignment 1Rusab IslamNo ratings yet

- Security Analysis and Portfolio Management by Rohini Singh 2018Document446 pagesSecurity Analysis and Portfolio Management by Rohini Singh 2018Aman Kumar SharanNo ratings yet

- How To Develop A Profitable Trading System PDFDocument3 pagesHow To Develop A Profitable Trading System PDFJoe DNo ratings yet

- Why Engage in International BusinessDocument3 pagesWhy Engage in International Businesslkarpaiya100% (2)

- Đề Thi Thử Tốt Nghiệp THPTDocument108 pagesĐề Thi Thử Tốt Nghiệp THPTMẫn NghiNo ratings yet

- XUIHq MJ Ev Yr BN VFuDocument7 pagesXUIHq MJ Ev Yr BN VFuAbhijit SahaNo ratings yet

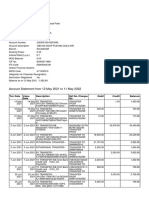

- Revolut Business Statement EUR 2 1Document1 pageRevolut Business Statement EUR 2 1JakcNo ratings yet

- ESG World Frameworks Philippines (080822)Document10 pagesESG World Frameworks Philippines (080822)TitoNo ratings yet

- Satılacak Rulman ListesiDocument21 pagesSatılacak Rulman ListesiIbrahim sofiNo ratings yet

- Nielsen PastasDocument31 pagesNielsen PastasGabriela Veronica FranzoniNo ratings yet

- BR Act 1949Document16 pagesBR Act 1949Sanjana SinghNo ratings yet

- Arcelormittal Signs Landmark Agreement With Government of Liberia Signals Commencement of One of The Largest Mining Projects in West AfricaDocument3 pagesArcelormittal Signs Landmark Agreement With Government of Liberia Signals Commencement of One of The Largest Mining Projects in West AfricaDuyan M. PeweeNo ratings yet

- Work AllocationDocument4 pagesWork AllocationNguyen Thanh Duc (FGW HCM)No ratings yet