Download as docx, pdf, or txt

You might also like

- CFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2024 Edition)From EverandCFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2024 Edition)Rating: 4.5 out of 5 stars4.5/5 (5)

- IA ReviewerDocument8 pagesIA ReviewerKaren Clarisse Alimot0% (2)

- BSA2BQuiz 3Document19 pagesBSA2BQuiz 3Monica Enrico0% (1)

- Bonds PayableDocument9 pagesBonds PayableKayla MirandaNo ratings yet

- CFP Exam Calculation Workbook: 400+ Calculations to Prepare for the CFP Exam (2018 Edition)From EverandCFP Exam Calculation Workbook: 400+ Calculations to Prepare for the CFP Exam (2018 Edition)Rating: 5 out of 5 stars5/5 (1)

- Jun18l1equ-C02 Qa PDFDocument3 pagesJun18l1equ-C02 Qa PDFjuanNo ratings yet

- Noncurrent LiabsDocument4 pagesNoncurrent Liabsrara elizalde100% (1)

- Bonds Payable Quiz Part 2Document5 pagesBonds Payable Quiz Part 2justine reine cornico100% (1)

- Identify The Choice That Best Completes The Statement or Answers The QuestionDocument11 pagesIdentify The Choice That Best Completes The Statement or Answers The QuestiontannyNo ratings yet

- Quizzer RETAINED EARNINGSDocument5 pagesQuizzer RETAINED EARNINGSPrincess Frean VillegasNo ratings yet

- Sia 3.compound Financial InstrumentDocument11 pagesSia 3.compound Financial InstrumentleneNo ratings yet

- Random Problem 2 (Pinky)Document23 pagesRandom Problem 2 (Pinky)spur iousNo ratings yet

- Random Problem 2 Pinkypdf PDF FreeDocument23 pagesRandom Problem 2 Pinkypdf PDF FreeTokis SabaNo ratings yet

- Sia 1.bonds PayableDocument13 pagesSia 1.bonds PayableYasmin MamugayNo ratings yet

- Compound Financial InstrumentDocument6 pagesCompound Financial InstrumentBeverlene BatiNo ratings yet

- Ia PPT 7Document18 pagesIa PPT 7lorriejaneNo ratings yet

- Chapter 7 BelardoDocument8 pagesChapter 7 BelardoAndrea BelardoNo ratings yet

- Compound Financial Instrument PDFDocument28 pagesCompound Financial Instrument PDFleneNo ratings yet

- Compound Financial InstrumentsDocument11 pagesCompound Financial InstrumentskyramaeNo ratings yet

- Problem:: Honey May A. Boaquaina BSA 301Document2 pagesProblem:: Honey May A. Boaquaina BSA 301Mitch Tokong MinglanaNo ratings yet

- Me AnswersDocument9 pagesMe Answersgabprems11No ratings yet

- Intermediate Accounting 2 Activity: Compound Financial InstrumentDocument2 pagesIntermediate Accounting 2 Activity: Compound Financial InstrumentMitch Tokong MinglanaNo ratings yet

- ACC314 A31 ProblemsDocument12 pagesACC314 A31 ProblemsaceNo ratings yet

- Notes Payable and Debt Restructuring (Ruma, Jamaica)Document14 pagesNotes Payable and Debt Restructuring (Ruma, Jamaica)Jamaica RumaNo ratings yet

- Bonds PayableDocument3 pagesBonds Payablegenesis roldanNo ratings yet

- Intermediate Accounting Questions PDFDocument4 pagesIntermediate Accounting Questions PDFJeanieNo ratings yet

- JUN18L1EQU/C01: Accurate About The Index?Document3 pagesJUN18L1EQU/C01: Accurate About The Index?rafav10No ratings yet

- Diara Po.Document7 pagesDiara Po.Rio Cyrel CelleroNo ratings yet

- Paper 2 Advanced Financial Management 170737012920240208100249Document25 pagesPaper 2 Advanced Financial Management 170737012920240208100249Pranav CrtNo ratings yet

- Midterm - Quiz SolutionDocument4 pagesMidterm - Quiz SolutionANSLEY CATE C. GUEVARRANo ratings yet

- Parcor TrainingDocument12 pagesParcor TrainingKarl ExacNo ratings yet

- Chapter 40 - Bond Investment: Problem 40-3 (IFRS)Document6 pagesChapter 40 - Bond Investment: Problem 40-3 (IFRS)Reinalyn MendozaNo ratings yet

- Unit Iii Assessment ProblemsDocument8 pagesUnit Iii Assessment ProblemsChin Figura100% (1)

- Bonds PayableDocument5 pagesBonds PayableJoseph AsisNo ratings yet

- Unit Iii Assessment ProblemsDocument8 pagesUnit Iii Assessment ProblemsWindie SisodNo ratings yet

- ACP Task 3 (20230328164424)Document2 pagesACP Task 3 (20230328164424)Roque LestieNo ratings yet

- Mid-term exam: Name: Kiều Vũ Kiều Anh ID: BAFNIU19054Document8 pagesMid-term exam: Name: Kiều Vũ Kiều Anh ID: BAFNIU19054Kiềuu AnnhNo ratings yet

- Mid-term exam: Name: Kiều Vũ Kiều Anh ID: BAFNIU19054Document8 pagesMid-term exam: Name: Kiều Vũ Kiều Anh ID: BAFNIU19054Kiềuu AnnhNo ratings yet

- Group-1-Chap-4 & 5Document10 pagesGroup-1-Chap-4 & 5Cherie Soriano AnanayoNo ratings yet

- IA2 Worksheet-BONDS PAYABLE - 101010Document11 pagesIA2 Worksheet-BONDS PAYABLE - 101010aehy lznuscrfbjNo ratings yet

- ANS KEY - QUIZ ON RECEIVABLE FINANCING 12 OctDocument4 pagesANS KEY - QUIZ ON RECEIVABLE FINANCING 12 OctAzzariah DeniseNo ratings yet

- Chapter 17Document12 pagesChapter 17Alainne DecylleNo ratings yet

- Working Papers For CorporationDocument8 pagesWorking Papers For CorporationcaraaatbongNo ratings yet

- Quiz EiDocument3 pagesQuiz EiJOY LYN REFUGIONo ratings yet

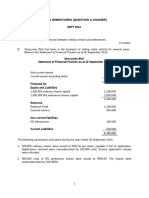

- Sept 2014 - 230716 - 233727Document22 pagesSept 2014 - 230716 - 233727mohddanialhanaffimustaffiNo ratings yet

- Accounting 3Document6 pagesAccounting 3Princess Frean VillegasNo ratings yet

- Quiz Chapter-15 Eps 2021-1Document4 pagesQuiz Chapter-15 Eps 2021-1Dale JimenoNo ratings yet

- Compound Financial InstrumentDocument2 pagesCompound Financial Instrumenthae1234No ratings yet

- Audit of EquityDocument6 pagesAudit of EquityEdmar HalogNo ratings yet

- QuizDocument8 pagesQuizMhea Ann Pauline ArsinoNo ratings yet

- Compound Financial Instruments Pas 32 Pfrs 9Document14 pagesCompound Financial Instruments Pas 32 Pfrs 9SamNo ratings yet

- 102 Quiz 1 She 2020Document6 pages102 Quiz 1 She 2020Eunice MartinezNo ratings yet

- FA II - Chapter 2 & 3 Part IIDocument21 pagesFA II - Chapter 2 & 3 Part IISitra AbduNo ratings yet

- University of Caloocan City Bachelor of Science in AccountancyDocument5 pagesUniversity of Caloocan City Bachelor of Science in AccountancyLumingNo ratings yet

- Self Test 9 - LiabilitiesDocument4 pagesSelf Test 9 - LiabilitiesBasketball WorldNo ratings yet

- Self Test 9 - LiabilitiesDocument4 pagesSelf Test 9 - LiabilitiesLennier ArvinNo ratings yet

- Chapter 3 Problem 6 LenzierDocument25 pagesChapter 3 Problem 6 LenzierJohn Lenzier TurtorNo ratings yet

- Stock Shares Price ($) Market Value of AssetsDocument34 pagesStock Shares Price ($) Market Value of AssetsRADHIKA BANSALNo ratings yet

- Managing Concentrated Stock Wealth: An Advisor's Guide to Building Customized SolutionsFrom EverandManaging Concentrated Stock Wealth: An Advisor's Guide to Building Customized SolutionsNo ratings yet

- Assigned TopicsDocument2 pagesAssigned TopicsClaudine LobrigasNo ratings yet

- Rizals Life and Works ReferencesDocument2 pagesRizals Life and Works ReferencesClaudine LobrigasNo ratings yet

- Lobrigas Unit4 Topic1 AssessmentDocument4 pagesLobrigas Unit4 Topic1 AssessmentClaudine LobrigasNo ratings yet

- Lobrigas Unit5 Topic5 AssessmentDocument6 pagesLobrigas Unit5 Topic5 AssessmentClaudine LobrigasNo ratings yet

- Lobrigas Unit5 Topic1 AssessmentDocument3 pagesLobrigas Unit5 Topic1 AssessmentClaudine LobrigasNo ratings yet

- Lobrigas Unit4 Topic2 AssessmentDocument7 pagesLobrigas Unit4 Topic2 AssessmentClaudine LobrigasNo ratings yet

- Lobrigas Unit4 PretestDocument2 pagesLobrigas Unit4 PretestClaudine LobrigasNo ratings yet

- Sevilla Unit10 Topic1 AssessmentDocument6 pagesSevilla Unit10 Topic1 AssessmentClaudine LobrigasNo ratings yet

- Sevilla Unit10 Topic2 AssessmentDocument7 pagesSevilla Unit10 Topic2 AssessmentClaudine LobrigasNo ratings yet

- Sevilla Unit9 Topic1 AssessmentDocument2 pagesSevilla Unit9 Topic1 AssessmentClaudine LobrigasNo ratings yet

- Lobrigas Unit3 Topic1 AssessmentDocument9 pagesLobrigas Unit3 Topic1 AssessmentClaudine LobrigasNo ratings yet

- Lobrigas Unit3 Topic2 AssessmentDocument6 pagesLobrigas Unit3 Topic2 AssessmentClaudine LobrigasNo ratings yet

- Lobrigas Unit3 PretestDocument4 pagesLobrigas Unit3 PretestClaudine LobrigasNo ratings yet

- Lobrigas Unit2 Topic2 AssessmentDocument5 pagesLobrigas Unit2 Topic2 AssessmentClaudine LobrigasNo ratings yet

- Lobrigas Unit1 AssessmentDocument5 pagesLobrigas Unit1 AssessmentClaudine LobrigasNo ratings yet

- Lobrigas Unit2 Topic1 AssessmentDocument5 pagesLobrigas Unit2 Topic1 AssessmentClaudine LobrigasNo ratings yet