DT Theory Compressed

DT Theory Compressed

You might also like

- Notice of Assessment - Year Ended 30 June 2020: Ms Elaine S Ross 64 Corrofin ST Ferny Grove QLD 4055Document2 pagesNotice of Assessment - Year Ended 30 June 2020: Ms Elaine S Ross 64 Corrofin ST Ferny Grove QLD 4055Vaccine ScamNo ratings yet

- Chapter 1 Introduction - Shajaratulmuttaqin 829469Document32 pagesChapter 1 Introduction - Shajaratulmuttaqin 829469Scha AzizanNo ratings yet

- Nagarro Pool Campus Drive 2023 BatchDocument1 pageNagarro Pool Campus Drive 2023 BatchKuldeep BilloreNo ratings yet

- First Announcement COE - 70 - MedanDocument23 pagesFirst Announcement COE - 70 - MedanHeru HermantrieNo ratings yet

- Io LS-F111P 20170718 PDFDocument7 pagesIo LS-F111P 20170718 PDFJess RojasNo ratings yet

- FPPC Complaint Re: Marin Resource Conservation DistrictDocument27 pagesFPPC Complaint Re: Marin Resource Conservation DistrictWill HoustonNo ratings yet

- Terrorism (Prevention and Prohibition) Act 2022Document89 pagesTerrorism (Prevention and Prohibition) Act 2022jideNo ratings yet

- Gamasutra - Jason Bakker's Blog - A GDD Template For The Indie DeveloperDocument5 pagesGamasutra - Jason Bakker's Blog - A GDD Template For The Indie DeveloperDaniel HuertaNo ratings yet

- GRI2009 EBrochureDocument27 pagesGRI2009 EBrochurenjaloualiNo ratings yet

- Taxation Law ProjectDocument26 pagesTaxation Law Projectshekhar singhNo ratings yet

- 1 s2.0 S0969698923000097 MainDocument12 pages1 s2.0 S0969698923000097 MainabidanayatNo ratings yet

- Chapter 10 (Crafting The Positioning & Differentiation)Document21 pagesChapter 10 (Crafting The Positioning & Differentiation)Magued MamdouhNo ratings yet

- Bajaj Allianz General Insurance 2021Document168 pagesBajaj Allianz General Insurance 2021Mohammad Ahtesham AvezNo ratings yet

- Summoning Osean FederationDocument128 pagesSummoning Osean FederationRadja RadjaNo ratings yet

- PMP - 2Document53 pagesPMP - 2Zain Ul Abidin RanaNo ratings yet

- GRE Vocabulary04Document36 pagesGRE Vocabulary04refdoc512No ratings yet

- Coleman Report 151.6DPDocument73 pagesColeman Report 151.6DPZviad MiminoshviliNo ratings yet

- PorterDocument2 pagesPorterJasonHrvyNo ratings yet

- 03 291 - Jugovic SchiozziDocument14 pages03 291 - Jugovic SchiozziNećeš SadaNo ratings yet

- Neutrona Wand AssemblyDocument17 pagesNeutrona Wand AssemblyJd DibrellNo ratings yet

- Qatar Strategic Transport Model (QSTM) - Oct 2013Document63 pagesQatar Strategic Transport Model (QSTM) - Oct 2013Ahmed FaroukNo ratings yet

- Jurnal 1Document18 pagesJurnal 1Elisabeth SinagaNo ratings yet

- South Africa 2000 enDocument213 pagesSouth Africa 2000 enYonnyNo ratings yet

- A Socio-Ecological Study of Population, Migration, Urbanization, and Socio-Climate Variation in Andhra Pradesh and Telangana, IndiaDocument33 pagesA Socio-Ecological Study of Population, Migration, Urbanization, and Socio-Climate Variation in Andhra Pradesh and Telangana, IndiaKousik D. MalakarNo ratings yet

- News ItemDocument8 pagesNews ItemAnonymous SLYi8ORABNo ratings yet

- WP - FooDocument3 pagesWP - FooMichael T. SalerNo ratings yet

- Hardware City Journal - Vol. 3 No. 7 - April 13, 2012Document16 pagesHardware City Journal - Vol. 3 No. 7 - April 13, 2012hardwarecityjournalNo ratings yet

- TTBR 23 December 2023 LDocument22 pagesTTBR 23 December 2023 L96priyanshNo ratings yet

- 9531IIEDDocument50 pages9531IIEDAlex MuroNo ratings yet

- 2019 - JSLHR 19 00014Document17 pages2019 - JSLHR 19 00014Paul RodrigoNo ratings yet

- Scope of Land Management and Its Chance To Implement Urban DevelopmentDocument18 pagesScope of Land Management and Its Chance To Implement Urban DevelopmentJai VigneshNo ratings yet

- Sor - WRD Gob - 01 - 10 - 12Document383 pagesSor - WRD Gob - 01 - 10 - 12Abhishek sNo ratings yet

- Topical S 2017Document86 pagesTopical S 2017Nguyễn HoàngNo ratings yet

- What Is Data Justice The Case For Connecting DigitDocument14 pagesWhat Is Data Justice The Case For Connecting DigitSuraj PrakashNo ratings yet

- CTP 08-01 BPDocument1 pageCTP 08-01 BPDaily GanomuktiNo ratings yet

- Soc297 Quiz 5Document5 pagesSoc297 Quiz 5Cute AkoNo ratings yet

- Shift From Open Distance Learning To Open Distance E-LearningDocument14 pagesShift From Open Distance Learning To Open Distance E-LearningSanNo ratings yet

- A Chatbot Using LSTM-based Multi-Layer Embedding For Elderly CareDocument5 pagesA Chatbot Using LSTM-based Multi-Layer Embedding For Elderly CareBoni ChalaNo ratings yet

- Threshing MachineDocument15 pagesThreshing MachineAbel SamuelNo ratings yet

- Save The Sound Tweed EA Comments To FAADocument13 pagesSave The Sound Tweed EA Comments To FAAEllyn SantiagoNo ratings yet

- March 2022 TissnetprepDocument42 pagesMarch 2022 TissnetprepVishal Maurya100% (1)

- NetSDK Programming Manual (Intelligent Traffic)Document63 pagesNetSDK Programming Manual (Intelligent Traffic)Ivan RangelNo ratings yet

- WWW Learninsta Com Extra Questions For Class 10 Social Science Geography ChapterDocument24 pagesWWW Learninsta Com Extra Questions For Class 10 Social Science Geography ChapterMala DeviNo ratings yet

- Challan AxisDocument3 pagesChallan AxisSumit Darak50% (2)

- AZ-104T00-A - Microsoft Azure Administrator - 3Document2 pagesAZ-104T00-A - Microsoft Azure Administrator - 3jesus jimenezNo ratings yet

- MST Group Brochure 2022 2 Page Spread Website FriendlyDocument15 pagesMST Group Brochure 2022 2 Page Spread Website FriendlyAlim KhalimbetovNo ratings yet

- Op 150141 Elektrotehničar Za Razvoj Veb I Mobilnih AplikacijaDocument312 pagesOp 150141 Elektrotehničar Za Razvoj Veb I Mobilnih AplikacijazvonebulNo ratings yet

- Advt. No. 01-2023Document5 pagesAdvt. No. 01-2023Simulacra TechnologiesNo ratings yet

- Geant4 ExampleDocument8 pagesGeant4 ExampleAtiqNo ratings yet

- Kit SDS Cover Sheet: Product Name Part Number Additional Product InformationDocument53 pagesKit SDS Cover Sheet: Product Name Part Number Additional Product InformationAhmedJumanNo ratings yet

- M2an 1977 11 1 93 0Document16 pagesM2an 1977 11 1 93 0Zina SawafNo ratings yet

- 10 1136@bmj m1326 PDFDocument2 pages10 1136@bmj m1326 PDFemmanuel prahNo ratings yet

- Amway GAR - BrochureDocument4 pagesAmway GAR - BrochureDiepP -Skincare CoachNo ratings yet

- Corporate Social Responsibility Practices Assessment Towards Responsible Entrepreneurship For Tabuk City's Micro Small and Medium EnterprisesDocument52 pagesCorporate Social Responsibility Practices Assessment Towards Responsible Entrepreneurship For Tabuk City's Micro Small and Medium EnterprisesIJELS Research JournalNo ratings yet

- Exemplu CVDocument2 pagesExemplu CVAdrian CapatinaNo ratings yet

- Mapping Cultural Events in Aripo Member States 2019 26.05.20Document58 pagesMapping Cultural Events in Aripo Member States 2019 26.05.20Events KultureNo ratings yet

- MAML THC Statement 8-22Document3 pagesMAML THC Statement 8-22FluenceMediaNo ratings yet

- ET Prime - HDFC Bank HDFC Merger - The HDFC LTD and HDFC Bank Merger - What Does It Mean For Investors - The Economic TimesDocument8 pagesET Prime - HDFC Bank HDFC Merger - The HDFC LTD and HDFC Bank Merger - What Does It Mean For Investors - The Economic TimesAryaman RawatNo ratings yet

- Europrobe Service ManualDocument17 pagesEuroprobe Service ManualJulio VellameNo ratings yet

- Powet Plant Control and Instrumentation: Lecture NotesDocument57 pagesPowet Plant Control and Instrumentation: Lecture Notessvvsnraju100% (1)

- Open PositionsDocument9 pagesOpen PositionsAtheen GuptaNo ratings yet

- Corporate Recovery and Tax Incentives For EnterprisesDocument5 pagesCorporate Recovery and Tax Incentives For EnterprisesIvy BoseNo ratings yet

- ACN 4135: Taxation: Income From Capital GainDocument10 pagesACN 4135: Taxation: Income From Capital GainHasibur Rahman100% (1)

- Lagdamin MP5Document4 pagesLagdamin MP5josh lagdaminNo ratings yet

- Direct Taxes and International TaxationDocument19 pagesDirect Taxes and International TaxationKumar SAPNo ratings yet

- Medicine WellnessDocument1 pageMedicine WellnessAyushiSrivastavaNo ratings yet

- Indian Income Tax Return Acknowledgement 2021-22: Assessment YearDocument1 pageIndian Income Tax Return Acknowledgement 2021-22: Assessment YearSaurya KumarNo ratings yet

- Restructuring Egypt's Railways - Augst 05 PDFDocument28 pagesRestructuring Egypt's Railways - Augst 05 PDFMahmoud Abo-hashemNo ratings yet

- Spesifikasi Kaedah Pengiraan Berkomputer PCB 2023Document48 pagesSpesifikasi Kaedah Pengiraan Berkomputer PCB 2023Annie LimNo ratings yet

- Ap 1070768102020Document1 pageAp 1070768102020Galaiah BellamkondaNo ratings yet

- P3771 Payslip Dec2019 PDFDocument1 pageP3771 Payslip Dec2019 PDFStalin Naveen KumarNo ratings yet

- E229EMBNT78989Document2 pagesE229EMBNT78989mansoor 31 shaikhNo ratings yet

- International Tax AvoidanceDocument27 pagesInternational Tax Avoidanceflordeliz12No ratings yet

- IAS 12 Solutions PDFDocument74 pagesIAS 12 Solutions PDFrafid aliNo ratings yet

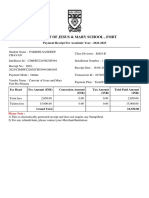

- Convent of Jesus & Mary School, Fort: Payment Receipt For Academic Year - 2022-2023Document2 pagesConvent of Jesus & Mary School, Fort: Payment Receipt For Academic Year - 2022-2023KDNo ratings yet

- Tax SolutionDocument9 pagesTax SolutionGhulam Mohyudin KharalNo ratings yet

- Vergara, Gian Bianca F. BSAT-4A Recitation: Compensation IncomeDocument3 pagesVergara, Gian Bianca F. BSAT-4A Recitation: Compensation Incomelena cpa100% (2)

- Moody's Credit Outlook - November 18 2013Document54 pagesMoody's Credit Outlook - November 18 2013Nick Reisman100% (1)

- Chapter 13 Principles of DeductionDocument5 pagesChapter 13 Principles of DeductionJason Mables100% (1)

- Emudhra Limited: One Year - Unlimited SigningDocument1 pageEmudhra Limited: One Year - Unlimited SigningNivash KrishnanNo ratings yet

- Fort Bonifacio Development Corporation vs. Commissioner of Internal RevenueDocument1 pageFort Bonifacio Development Corporation vs. Commissioner of Internal RevenueDeus DulayNo ratings yet

- Part H 2 - CIR vs. Procter GambleDocument2 pagesPart H 2 - CIR vs. Procter GambleCyruz TuppalNo ratings yet

- Talking Economics Digest Innovation Special IssueDocument25 pagesTalking Economics Digest Innovation Special IssueIPS Sri LankaNo ratings yet

- Traces: Details of SalaryDocument4 pagesTraces: Details of SalaryMadu JaguNo ratings yet

- UntitledDocument7 pagesUntitledBlake WeberNo ratings yet

- Taxation - 6 SemesterDocument28 pagesTaxation - 6 SemesterKhalid123No ratings yet

- Income Tax Department: Computerized Payment Receipt (CPR - It)Document4 pagesIncome Tax Department: Computerized Payment Receipt (CPR - It)M Naveed SultanNo ratings yet

- BCM 304Document5 pagesBCM 304SHIVAM SANTOSHNo ratings yet

- MyPayroll User Guide For Investment Declaration For FY 2020-21Document18 pagesMyPayroll User Guide For Investment Declaration For FY 2020-21bhaavaNo ratings yet

- Computation of Total Income Income From House Property (Chapter IV C) - 149209Document5 pagesComputation of Total Income Income From House Property (Chapter IV C) - 149209MVLNo ratings yet

Download as pdf or txt

You might also like

- Notice of Assessment - Year Ended 30 June 2020: Ms Elaine S Ross 64 Corrofin ST Ferny Grove QLD 4055Document2 pagesNotice of Assessment - Year Ended 30 June 2020: Ms Elaine S Ross 64 Corrofin ST Ferny Grove QLD 4055Vaccine ScamNo ratings yet

- Chapter 1 Introduction - Shajaratulmuttaqin 829469Document32 pagesChapter 1 Introduction - Shajaratulmuttaqin 829469Scha AzizanNo ratings yet

- Nagarro Pool Campus Drive 2023 BatchDocument1 pageNagarro Pool Campus Drive 2023 BatchKuldeep BilloreNo ratings yet

- First Announcement COE - 70 - MedanDocument23 pagesFirst Announcement COE - 70 - MedanHeru HermantrieNo ratings yet

- Io LS-F111P 20170718 PDFDocument7 pagesIo LS-F111P 20170718 PDFJess RojasNo ratings yet

- FPPC Complaint Re: Marin Resource Conservation DistrictDocument27 pagesFPPC Complaint Re: Marin Resource Conservation DistrictWill HoustonNo ratings yet

- Terrorism (Prevention and Prohibition) Act 2022Document89 pagesTerrorism (Prevention and Prohibition) Act 2022jideNo ratings yet

- Gamasutra - Jason Bakker's Blog - A GDD Template For The Indie DeveloperDocument5 pagesGamasutra - Jason Bakker's Blog - A GDD Template For The Indie DeveloperDaniel HuertaNo ratings yet

- GRI2009 EBrochureDocument27 pagesGRI2009 EBrochurenjaloualiNo ratings yet

- Taxation Law ProjectDocument26 pagesTaxation Law Projectshekhar singhNo ratings yet

- 1 s2.0 S0969698923000097 MainDocument12 pages1 s2.0 S0969698923000097 MainabidanayatNo ratings yet

- Chapter 10 (Crafting The Positioning & Differentiation)Document21 pagesChapter 10 (Crafting The Positioning & Differentiation)Magued MamdouhNo ratings yet

- Bajaj Allianz General Insurance 2021Document168 pagesBajaj Allianz General Insurance 2021Mohammad Ahtesham AvezNo ratings yet

- Summoning Osean FederationDocument128 pagesSummoning Osean FederationRadja RadjaNo ratings yet

- PMP - 2Document53 pagesPMP - 2Zain Ul Abidin RanaNo ratings yet

- GRE Vocabulary04Document36 pagesGRE Vocabulary04refdoc512No ratings yet

- Coleman Report 151.6DPDocument73 pagesColeman Report 151.6DPZviad MiminoshviliNo ratings yet

- PorterDocument2 pagesPorterJasonHrvyNo ratings yet

- 03 291 - Jugovic SchiozziDocument14 pages03 291 - Jugovic SchiozziNećeš SadaNo ratings yet

- Neutrona Wand AssemblyDocument17 pagesNeutrona Wand AssemblyJd DibrellNo ratings yet

- Qatar Strategic Transport Model (QSTM) - Oct 2013Document63 pagesQatar Strategic Transport Model (QSTM) - Oct 2013Ahmed FaroukNo ratings yet

- Jurnal 1Document18 pagesJurnal 1Elisabeth SinagaNo ratings yet

- South Africa 2000 enDocument213 pagesSouth Africa 2000 enYonnyNo ratings yet

- A Socio-Ecological Study of Population, Migration, Urbanization, and Socio-Climate Variation in Andhra Pradesh and Telangana, IndiaDocument33 pagesA Socio-Ecological Study of Population, Migration, Urbanization, and Socio-Climate Variation in Andhra Pradesh and Telangana, IndiaKousik D. MalakarNo ratings yet

- News ItemDocument8 pagesNews ItemAnonymous SLYi8ORABNo ratings yet

- WP - FooDocument3 pagesWP - FooMichael T. SalerNo ratings yet

- Hardware City Journal - Vol. 3 No. 7 - April 13, 2012Document16 pagesHardware City Journal - Vol. 3 No. 7 - April 13, 2012hardwarecityjournalNo ratings yet

- TTBR 23 December 2023 LDocument22 pagesTTBR 23 December 2023 L96priyanshNo ratings yet

- 9531IIEDDocument50 pages9531IIEDAlex MuroNo ratings yet

- 2019 - JSLHR 19 00014Document17 pages2019 - JSLHR 19 00014Paul RodrigoNo ratings yet

- Scope of Land Management and Its Chance To Implement Urban DevelopmentDocument18 pagesScope of Land Management and Its Chance To Implement Urban DevelopmentJai VigneshNo ratings yet

- Sor - WRD Gob - 01 - 10 - 12Document383 pagesSor - WRD Gob - 01 - 10 - 12Abhishek sNo ratings yet

- Topical S 2017Document86 pagesTopical S 2017Nguyễn HoàngNo ratings yet

- What Is Data Justice The Case For Connecting DigitDocument14 pagesWhat Is Data Justice The Case For Connecting DigitSuraj PrakashNo ratings yet

- CTP 08-01 BPDocument1 pageCTP 08-01 BPDaily GanomuktiNo ratings yet

- Soc297 Quiz 5Document5 pagesSoc297 Quiz 5Cute AkoNo ratings yet

- Shift From Open Distance Learning To Open Distance E-LearningDocument14 pagesShift From Open Distance Learning To Open Distance E-LearningSanNo ratings yet

- A Chatbot Using LSTM-based Multi-Layer Embedding For Elderly CareDocument5 pagesA Chatbot Using LSTM-based Multi-Layer Embedding For Elderly CareBoni ChalaNo ratings yet

- Threshing MachineDocument15 pagesThreshing MachineAbel SamuelNo ratings yet

- Save The Sound Tweed EA Comments To FAADocument13 pagesSave The Sound Tweed EA Comments To FAAEllyn SantiagoNo ratings yet

- March 2022 TissnetprepDocument42 pagesMarch 2022 TissnetprepVishal Maurya100% (1)

- NetSDK Programming Manual (Intelligent Traffic)Document63 pagesNetSDK Programming Manual (Intelligent Traffic)Ivan RangelNo ratings yet

- WWW Learninsta Com Extra Questions For Class 10 Social Science Geography ChapterDocument24 pagesWWW Learninsta Com Extra Questions For Class 10 Social Science Geography ChapterMala DeviNo ratings yet

- Challan AxisDocument3 pagesChallan AxisSumit Darak50% (2)

- AZ-104T00-A - Microsoft Azure Administrator - 3Document2 pagesAZ-104T00-A - Microsoft Azure Administrator - 3jesus jimenezNo ratings yet

- MST Group Brochure 2022 2 Page Spread Website FriendlyDocument15 pagesMST Group Brochure 2022 2 Page Spread Website FriendlyAlim KhalimbetovNo ratings yet

- Op 150141 Elektrotehničar Za Razvoj Veb I Mobilnih AplikacijaDocument312 pagesOp 150141 Elektrotehničar Za Razvoj Veb I Mobilnih AplikacijazvonebulNo ratings yet

- Advt. No. 01-2023Document5 pagesAdvt. No. 01-2023Simulacra TechnologiesNo ratings yet

- Geant4 ExampleDocument8 pagesGeant4 ExampleAtiqNo ratings yet

- Kit SDS Cover Sheet: Product Name Part Number Additional Product InformationDocument53 pagesKit SDS Cover Sheet: Product Name Part Number Additional Product InformationAhmedJumanNo ratings yet

- M2an 1977 11 1 93 0Document16 pagesM2an 1977 11 1 93 0Zina SawafNo ratings yet

- 10 1136@bmj m1326 PDFDocument2 pages10 1136@bmj m1326 PDFemmanuel prahNo ratings yet

- Amway GAR - BrochureDocument4 pagesAmway GAR - BrochureDiepP -Skincare CoachNo ratings yet

- Corporate Social Responsibility Practices Assessment Towards Responsible Entrepreneurship For Tabuk City's Micro Small and Medium EnterprisesDocument52 pagesCorporate Social Responsibility Practices Assessment Towards Responsible Entrepreneurship For Tabuk City's Micro Small and Medium EnterprisesIJELS Research JournalNo ratings yet

- Exemplu CVDocument2 pagesExemplu CVAdrian CapatinaNo ratings yet

- Mapping Cultural Events in Aripo Member States 2019 26.05.20Document58 pagesMapping Cultural Events in Aripo Member States 2019 26.05.20Events KultureNo ratings yet

- MAML THC Statement 8-22Document3 pagesMAML THC Statement 8-22FluenceMediaNo ratings yet

- ET Prime - HDFC Bank HDFC Merger - The HDFC LTD and HDFC Bank Merger - What Does It Mean For Investors - The Economic TimesDocument8 pagesET Prime - HDFC Bank HDFC Merger - The HDFC LTD and HDFC Bank Merger - What Does It Mean For Investors - The Economic TimesAryaman RawatNo ratings yet

- Europrobe Service ManualDocument17 pagesEuroprobe Service ManualJulio VellameNo ratings yet

- Powet Plant Control and Instrumentation: Lecture NotesDocument57 pagesPowet Plant Control and Instrumentation: Lecture Notessvvsnraju100% (1)

- Open PositionsDocument9 pagesOpen PositionsAtheen GuptaNo ratings yet

- Corporate Recovery and Tax Incentives For EnterprisesDocument5 pagesCorporate Recovery and Tax Incentives For EnterprisesIvy BoseNo ratings yet

- ACN 4135: Taxation: Income From Capital GainDocument10 pagesACN 4135: Taxation: Income From Capital GainHasibur Rahman100% (1)

- Lagdamin MP5Document4 pagesLagdamin MP5josh lagdaminNo ratings yet

- Direct Taxes and International TaxationDocument19 pagesDirect Taxes and International TaxationKumar SAPNo ratings yet

- Medicine WellnessDocument1 pageMedicine WellnessAyushiSrivastavaNo ratings yet

- Indian Income Tax Return Acknowledgement 2021-22: Assessment YearDocument1 pageIndian Income Tax Return Acknowledgement 2021-22: Assessment YearSaurya KumarNo ratings yet

- Restructuring Egypt's Railways - Augst 05 PDFDocument28 pagesRestructuring Egypt's Railways - Augst 05 PDFMahmoud Abo-hashemNo ratings yet

- Spesifikasi Kaedah Pengiraan Berkomputer PCB 2023Document48 pagesSpesifikasi Kaedah Pengiraan Berkomputer PCB 2023Annie LimNo ratings yet

- Ap 1070768102020Document1 pageAp 1070768102020Galaiah BellamkondaNo ratings yet

- P3771 Payslip Dec2019 PDFDocument1 pageP3771 Payslip Dec2019 PDFStalin Naveen KumarNo ratings yet

- E229EMBNT78989Document2 pagesE229EMBNT78989mansoor 31 shaikhNo ratings yet

- International Tax AvoidanceDocument27 pagesInternational Tax Avoidanceflordeliz12No ratings yet

- IAS 12 Solutions PDFDocument74 pagesIAS 12 Solutions PDFrafid aliNo ratings yet

- Convent of Jesus & Mary School, Fort: Payment Receipt For Academic Year - 2022-2023Document2 pagesConvent of Jesus & Mary School, Fort: Payment Receipt For Academic Year - 2022-2023KDNo ratings yet

- Tax SolutionDocument9 pagesTax SolutionGhulam Mohyudin KharalNo ratings yet

- Vergara, Gian Bianca F. BSAT-4A Recitation: Compensation IncomeDocument3 pagesVergara, Gian Bianca F. BSAT-4A Recitation: Compensation Incomelena cpa100% (2)

- Moody's Credit Outlook - November 18 2013Document54 pagesMoody's Credit Outlook - November 18 2013Nick Reisman100% (1)

- Chapter 13 Principles of DeductionDocument5 pagesChapter 13 Principles of DeductionJason Mables100% (1)

- Emudhra Limited: One Year - Unlimited SigningDocument1 pageEmudhra Limited: One Year - Unlimited SigningNivash KrishnanNo ratings yet

- Fort Bonifacio Development Corporation vs. Commissioner of Internal RevenueDocument1 pageFort Bonifacio Development Corporation vs. Commissioner of Internal RevenueDeus DulayNo ratings yet

- Part H 2 - CIR vs. Procter GambleDocument2 pagesPart H 2 - CIR vs. Procter GambleCyruz TuppalNo ratings yet

- Talking Economics Digest Innovation Special IssueDocument25 pagesTalking Economics Digest Innovation Special IssueIPS Sri LankaNo ratings yet

- Traces: Details of SalaryDocument4 pagesTraces: Details of SalaryMadu JaguNo ratings yet

- UntitledDocument7 pagesUntitledBlake WeberNo ratings yet

- Taxation - 6 SemesterDocument28 pagesTaxation - 6 SemesterKhalid123No ratings yet

- Income Tax Department: Computerized Payment Receipt (CPR - It)Document4 pagesIncome Tax Department: Computerized Payment Receipt (CPR - It)M Naveed SultanNo ratings yet

- BCM 304Document5 pagesBCM 304SHIVAM SANTOSHNo ratings yet

- MyPayroll User Guide For Investment Declaration For FY 2020-21Document18 pagesMyPayroll User Guide For Investment Declaration For FY 2020-21bhaavaNo ratings yet

- Computation of Total Income Income From House Property (Chapter IV C) - 149209Document5 pagesComputation of Total Income Income From House Property (Chapter IV C) - 149209MVLNo ratings yet