Download as pdf or txt

You might also like

- Udhemy CourcesDocument1 pageUdhemy CourcesRam Sri100% (1)

- Paycheck 20211203 002360 Maurisha 202112231136Document1 pagePaycheck 20211203 002360 Maurisha 202112231136saraNo ratings yet

- Societe Generale Global Solution Centre Pvt. LTD.: Net Pay: Rs. 61991.00 Sixty One Thousand Nine Hundred Ninety OneDocument2 pagesSociete Generale Global Solution Centre Pvt. LTD.: Net Pay: Rs. 61991.00 Sixty One Thousand Nine Hundred Ninety OnePramod Kumar100% (1)

- Pay SlipDocument1 pagePay SlipnauvalNo ratings yet

- Phil Tax System and Income Taxation FQ1-FQ2Document12 pagesPhil Tax System and Income Taxation FQ1-FQ2Sherina ManlisesNo ratings yet

- TXPOL 2019 Dec ADocument8 pagesTXPOL 2019 Dec AKAH MENG KAMNo ratings yet

- F6RUS AnsDocument9 pagesF6RUS AnsСветлана КозловаNo ratings yet

- S20 TX ROM Sample AnswersDocument8 pagesS20 TX ROM Sample AnswersKAH MENG KAMNo ratings yet

- TX-CYP Dec 21 AnswersDocument8 pagesTX-CYP Dec 21 AnswersKAM JIA LINGNo ratings yet

- F6rom - 2010 - Dec - A ACCADocument10 pagesF6rom - 2010 - Dec - A ACCAgeorgetacaprarescuNo ratings yet

- TXZAF 2019 Dec ADocument8 pagesTXZAF 2019 Dec AKAH MENG KAMNo ratings yet

- TXSGP 2018 SepDec ADocument8 pagesTXSGP 2018 SepDec AKAH MENG KAMNo ratings yet

- Txbwa 2019 Dec ADocument9 pagesTxbwa 2019 Dec Agajendra.naiduNo ratings yet

- Atxuk Sample Marjun 2019 ADocument10 pagesAtxuk Sample Marjun 2019 AAdam KhanNo ratings yet

- S20 TX ZWE Sample AnswersDocument9 pagesS20 TX ZWE Sample AnswersKAH MENG KAMNo ratings yet

- Txmwi 2018 Dec ADocument7 pagesTxmwi 2018 Dec AangaNo ratings yet

- 2-3mwi 2006 Dec ADocument13 pages2-3mwi 2006 Dec AangaNo ratings yet

- TXUK 2019 MarJun ADocument11 pagesTXUK 2019 MarJun AmdNo ratings yet

- F6 AnsDocument9 pagesF6 AnsRaza AliNo ratings yet

- S20 TX MWI Sample AnswersDocument8 pagesS20 TX MWI Sample AnswersangaNo ratings yet

- Txmys 2022 Dec ADocument10 pagesTxmys 2022 Dec Amuhammadafifi126No ratings yet

- S20 TX ZAF Sample AnswersDocument8 pagesS20 TX ZAF Sample AnswersKAH MENG KAMNo ratings yet

- F6zwe 2015 Dec ADocument8 pagesF6zwe 2015 Dec APhebieon MukwenhaNo ratings yet

- f6vnm 2016 Dec ADocument6 pagesf6vnm 2016 Dec AHuyền NguyễnNo ratings yet

- Txbwa 2022 Dec ADocument9 pagesTxbwa 2022 Dec AArundhati SinghNo ratings yet

- ABC and XYZ - QuestionDocument2 pagesABC and XYZ - QuestionMohammad El HajjNo ratings yet

- F6mwi 2007 Dec QDocument8 pagesF6mwi 2007 Dec Qanga100% (1)

- Business Taxation: (Malawi)Document10 pagesBusiness Taxation: (Malawi)angaNo ratings yet

- 2016 Jun Ans-5-6Document2 pages2016 Jun Ans-5-6何健珩No ratings yet

- December 2010 TC10BADocument12 pagesDecember 2010 TC10BAkalowekamoNo ratings yet

- TXZWE 2018 Dec ADocument9 pagesTXZWE 2018 Dec AKAH MENG KAMNo ratings yet

- MJ17 - Hybrids - P6UK - AMENDED AnswersDocument12 pagesMJ17 - Hybrids - P6UK - AMENDED AnswersHassan jalilNo ratings yet

- SolMan Empleo Robles Intangible AssetDocument18 pagesSolMan Empleo Robles Intangible AssetJohanna Raissa CapadaNo ratings yet

- Chapter 21 - QB - Q1 - SolutionDocument4 pagesChapter 21 - QB - Q1 - SolutionRichard SibekoNo ratings yet

- 2019 Dec Ans-5-6Document2 pages2019 Dec Ans-5-6何健珩No ratings yet

- 2015 Jun Ans-8Document1 page2015 Jun Ans-8何健珩No ratings yet

- F6ZWE 2015 Jun ADocument8 pagesF6ZWE 2015 Jun APhebieon MukwenhaNo ratings yet

- F6ZWEDocument8 pagesF6ZWEkevior2No ratings yet

- F6MWI 2015 Jun ADocument7 pagesF6MWI 2015 Jun AangaNo ratings yet

- TXROM 2019 Dec ADocument9 pagesTXROM 2019 Dec AKAH MENG KAMNo ratings yet

- Less: Municipal Taxes Paid by Mr. Raj: © The Institute of Chartered Accountants of IndiaDocument11 pagesLess: Municipal Taxes Paid by Mr. Raj: © The Institute of Chartered Accountants of IndiaKetan DedhaNo ratings yet

- F6mys 2015 Dec ADocument8 pagesF6mys 2015 Dec ABryan EngNo ratings yet

- 2017 Dec Ans-6Document1 page2017 Dec Ans-6何健珩No ratings yet

- Taxation (Malawi) : Monday 1 December 2008Document10 pagesTaxation (Malawi) : Monday 1 December 2008angaNo ratings yet

- Sumana Podder: Taxation Assignment - 1Document3 pagesSumana Podder: Taxation Assignment - 1akash deyNo ratings yet

- Tutorial Ias 33Document5 pagesTutorial Ias 33tinashekuzangaNo ratings yet

- S20 TX BWA Sample AnswersDocument10 pagesS20 TX BWA Sample AnswersKAM JIA LINGNo ratings yet

- ACC 401-2023 GA 2-EvenDocument3 pagesACC 401-2023 GA 2-EvenOhene Asare PogastyNo ratings yet

- AnswersDocument7 pagesAnswersMlambo ConnieNo ratings yet

- 2016 Dec Ans-6Document1 page2016 Dec Ans-6何健珩No ratings yet

- 2018 Dec Ans-6-7Document2 pages2018 Dec Ans-6-7何健珩No ratings yet

- 73264bos59105 Inter P1aDocument12 pages73264bos59105 Inter P1aRaish QURESHINo ratings yet

- S20 TX SGP Sample AnswersDocument7 pagesS20 TX SGP Sample AnswersKAH MENG KAMNo ratings yet

- 2-3mwi 2006 Jun ADocument12 pages2-3mwi 2006 Jun AangaNo ratings yet

- R2.TAXM - .L Solution CMA June 2021 Exam.Document8 pagesR2.TAXM - .L Solution CMA June 2021 Exam.Pavel DhakaNo ratings yet

- Vat Questions: GARFIELD (Mar/Jun 16)Document3 pagesVat Questions: GARFIELD (Mar/Jun 16)Rabi HashimNo ratings yet

- 2019 Jun Ans-8Document1 page2019 Jun Ans-8何健珩No ratings yet

- CAF 1 Autumn 2023Document7 pagesCAF 1 Autumn 2023Asim MahmoodNo ratings yet

- Accounting 22 - Final Exam - 2023Document9 pagesAccounting 22 - Final Exam - 2023LaurenNo ratings yet

- Accounting For Special TransactionDocument15 pagesAccounting For Special TransactionRichelle Mea B. PeñaNo ratings yet

- IFRS Reporting Specialist Case StudyDocument11 pagesIFRS Reporting Specialist Case StudyglmncubeNo ratings yet

- Group Activity 2 Answer KeyDocument4 pagesGroup Activity 2 Answer Keykrisha milloNo ratings yet

- Jobb Internet AdvertisingDocument2 pagesJobb Internet Advertisingrethaxaba82No ratings yet

- Acc Budgeting - Revsion 2023 NovDocument12 pagesAcc Budgeting - Revsion 2023 Novtshegomore2005No ratings yet

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- TXPOL 2019 Dec QDocument14 pagesTXPOL 2019 Dec QKAH MENG KAMNo ratings yet

- TXROM 2019 Jun QDocument17 pagesTXROM 2019 Jun QKAH MENG KAMNo ratings yet

- TXPOL 2019 Dec ADocument8 pagesTXPOL 2019 Dec AKAH MENG KAMNo ratings yet

- TXROM 2018 Dec QDocument16 pagesTXROM 2018 Dec QKAH MENG KAMNo ratings yet

- S20 TX ROM Sample AnswersDocument8 pagesS20 TX ROM Sample AnswersKAH MENG KAMNo ratings yet

- TXROM 2019 Dec QDocument17 pagesTXROM 2019 Dec QKAH MENG KAMNo ratings yet

- TXSGP 2018 SepDec ADocument8 pagesTXSGP 2018 SepDec AKAH MENG KAMNo ratings yet

- TXROM 2019 Dec ADocument9 pagesTXROM 2019 Dec AKAH MENG KAMNo ratings yet

- Txrus 2019 Dec QDocument15 pagesTxrus 2019 Dec QKAH MENG KAMNo ratings yet

- S20 TX RUS Sample AnswersDocument8 pagesS20 TX RUS Sample AnswersKAH MENG KAMNo ratings yet

- S20 TX SGP Sample AnswersDocument7 pagesS20 TX SGP Sample AnswersKAH MENG KAMNo ratings yet

- AA SD21 QsDocument23 pagesAA SD21 QsKAH MENG KAMNo ratings yet

- TXZWE 2018 Dec QDocument15 pagesTXZWE 2018 Dec QKAH MENG KAMNo ratings yet

- TXZAF 2018 Dec QDocument16 pagesTXZAF 2018 Dec QKAH MENG KAMNo ratings yet

- TXZAF 2019 Dec QDocument17 pagesTXZAF 2019 Dec QKAH MENG KAMNo ratings yet

- TX (SGP) Sept 20 Sample CBE QuestionsDocument28 pagesTX (SGP) Sept 20 Sample CBE QuestionsKAH MENG KAMNo ratings yet

- S20 TX ZAF Sample AnswersDocument8 pagesS20 TX ZAF Sample AnswersKAH MENG KAMNo ratings yet

- Taxation VNM - ACCA F6Document8 pagesTaxation VNM - ACCA F6Nguyễn Hải TrânNo ratings yet

- TXZAF 2019 Dec ADocument8 pagesTXZAF 2019 Dec AKAH MENG KAMNo ratings yet

- TXZWE 2018 Dec ADocument9 pagesTXZWE 2018 Dec AKAH MENG KAMNo ratings yet

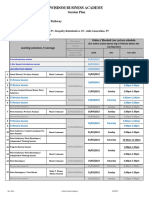

- SCS-Pathway Session Plans 2022Document2 pagesSCS-Pathway Session Plans 2022KAH MENG KAMNo ratings yet

- SCS FamiliarisationDocument26 pagesSCS FamiliarisationKAH MENG KAMNo ratings yet

- S20 TX ZWE Sample AnswersDocument9 pagesS20 TX ZWE Sample AnswersKAH MENG KAMNo ratings yet

- SCS May 22 Game PlannerDocument31 pagesSCS May 22 Game PlannerKAH MENG KAMNo ratings yet

- Strategic Exam Blueprints 2022 2023 Version3Document56 pagesStrategic Exam Blueprints 2022 2023 Version3KAH MENG KAMNo ratings yet

- Itr2 719710260121120$Document1 pageItr2 719710260121120$vvn HarishNo ratings yet

- Worksheets - B - 4.2.1 Wages Deductions Benefits Timekeeping FormsDocument6 pagesWorksheets - B - 4.2.1 Wages Deductions Benefits Timekeeping FormsArnelson DerechoNo ratings yet

- SS International Traders-FiamaDocument1 pageSS International Traders-FiamaratiexpressNo ratings yet

- TAX-801 (Sources of Income)Document2 pagesTAX-801 (Sources of Income)MABI ESPENIDONo ratings yet

- TAX3761 - FASSET Class 1Document4 pagesTAX3761 - FASSET Class 1Vincent Mutumwa8oo9wooNo ratings yet

- MG 3027 TAXATION - Week 3 Personal AllowancesDocument28 pagesMG 3027 TAXATION - Week 3 Personal AllowancesSyed SafdarNo ratings yet

- InvoicehdDocument1 pageInvoicehdKiran RockNo ratings yet

- Tax 670 Milestone 2Document5 pagesTax 670 Milestone 2pthavNo ratings yet

- Qi0243 - Amnpn5168p - 2022-23 - Fy 2022 - 2023Document9 pagesQi0243 - Amnpn5168p - 2022-23 - Fy 2022 - 2023Dharma kurraNo ratings yet

- Green Knight Economic Development Corporation IRS Form 990 For FY2014Document30 pagesGreen Knight Economic Development Corporation IRS Form 990 For FY2014DickNo ratings yet

- Bahasa Inggris HukumDocument9 pagesBahasa Inggris HukumlorensiusNo ratings yet

- JHGHKDocument6 pagesJHGHKamritNo ratings yet

- January February March Cash SalesDocument13 pagesJanuary February March Cash SalesMary R. R. PanesNo ratings yet

- Laba Rugi Per SekolahDocument1 pageLaba Rugi Per SekolahPascal FelimNo ratings yet

- Lowe Ruling (BIR Ruling (DA - (C-283) 705-09)Document3 pagesLowe Ruling (BIR Ruling (DA - (C-283) 705-09)Kriszan ManiponNo ratings yet

- Haryana DC Max Hypermarket India PVT Ltdmusti 42/43, Village Gudhi, Bilaspur Tauru Roadopposite Jhamuwas Stadium Delhi State:Hr Post:122015Document2 pagesHaryana DC Max Hypermarket India PVT Ltdmusti 42/43, Village Gudhi, Bilaspur Tauru Roadopposite Jhamuwas Stadium Delhi State:Hr Post:122015Aksar SharmNo ratings yet

- Joint Astronomy Centre - Birthday Stars - FinalDocument2 pagesJoint Astronomy Centre - Birthday Stars - Finalhail2pigdumNo ratings yet

- Moodlecloud 24284Document1 pageMoodlecloud 24284Giged BattungNo ratings yet

- Income Tax Theory by T.S. Reddy From Margham Publication 2022-23Document1 pageIncome Tax Theory by T.S. Reddy From Margham Publication 2022-23Riya M0% (1)

- BookingTaxInvoice HTLH5Y37V9Document2 pagesBookingTaxInvoice HTLH5Y37V9yogesh guptaNo ratings yet

- TAXATION - Filing of Returns + Tax Penalties and RemediesDocument7 pagesTAXATION - Filing of Returns + Tax Penalties and RemediesJohn Mahatma Agripa100% (1)

- AC GST Tax InvoiceDocument1 pageAC GST Tax InvoiceSanjay KumarNo ratings yet

- Itr 2023 2024Document1 pageItr 2023 2024Deepak ThangamaniNo ratings yet

- Quiz 4 Income TaxDocument5 pagesQuiz 4 Income TaxjohndanielsantosNo ratings yet