Download as pdf or txt

You might also like

- HW 3 Ratio Analysis WalmartDocument10 pagesHW 3 Ratio Analysis Walmartcorbin_amsel50% (2)

- The European Monetary System, The Maastricht Treaty, Birth of The Euro and Its FutureDocument41 pagesThe European Monetary System, The Maastricht Treaty, Birth of The Euro and Its FutureSharon NunesNo ratings yet

- Optimum Currency Areas and The European Experience: Slides Prepared by Thomas BishopDocument51 pagesOptimum Currency Areas and The European Experience: Slides Prepared by Thomas BishopTariqul IslamNo ratings yet

- Chapter 20Document57 pagesChapter 20Hoang Trung NguyenNo ratings yet

- Httpslearn Eu Central 1 Prod Fleet01 Xythos - Content.blackboardcdn - Com610a68551efab32185376x Blackboard S3 Bucket Learn EuDocument48 pagesHttpslearn Eu Central 1 Prod Fleet01 Xythos - Content.blackboardcdn - Com610a68551efab32185376x Blackboard S3 Bucket Learn EuValerie RogatskinaNo ratings yet

- Lesson 2 HistoryDocument13 pagesLesson 2 Historyrorita.canaleuniparthenope.itNo ratings yet

- European Monetary PolicyDocument21 pagesEuropean Monetary PolicySlashXNo ratings yet

- Euro Euro: System SystemDocument57 pagesEuro Euro: System SystemKripansh GroverNo ratings yet

- Current Issues in European Integration LUBS 3570: Lecture 2: History, Institutions and The Current CrisisDocument24 pagesCurrent Issues in European Integration LUBS 3570: Lecture 2: History, Institutions and The Current Crisiscoolguy1993No ratings yet

- The Road To The Euro: One Currency For One EuropeDocument24 pagesThe Road To The Euro: One Currency For One Europexanoca13No ratings yet

- Ems, Emu and EuroDocument16 pagesEms, Emu and EuroKapil DhingraNo ratings yet

- European Monetary SystemDocument3 pagesEuropean Monetary SystemDavid Andrés Robalino ChicaNo ratings yet

- EU euro індивідуальнаDocument2 pagesEU euro індивідуальнаНаталія ХоменкоNo ratings yet

- SailashreeChakraborty 13600921093 FM405Document10 pagesSailashreeChakraborty 13600921093 FM405Sailashree ChakrabortyNo ratings yet

- EU Politics and EconomicsDocument4 pagesEU Politics and Economicscondesemma7No ratings yet

- How The European Monetary Union Was Created? What Are The Main Stages and Evolution of The Process?Document34 pagesHow The European Monetary Union Was Created? What Are The Main Stages and Evolution of The Process?vidya kamnurkarNo ratings yet

- And Monetary Union: in The European CommunityDocument38 pagesAnd Monetary Union: in The European Communityedo-peiraias.blogspot.comNo ratings yet

- Final MusamDocument118 pagesFinal MusamMuzna AhmedNo ratings yet

- European Monetary System (EMS) An Arrangement Initiated in 1979 Where Members of The European Economic Community Agreed To Link Their CurrenciesDocument5 pagesEuropean Monetary System (EMS) An Arrangement Initiated in 1979 Where Members of The European Economic Community Agreed To Link Their Currenciessameerkhan855No ratings yet

- Notes Chapter 9Document11 pagesNotes Chapter 9Amaia MartinicorenaNo ratings yet

- Eurozone Group 4Document36 pagesEurozone Group 4NhiHoangNo ratings yet

- Adv N Disadv of RTBDocument2 pagesAdv N Disadv of RTBsweetuuNo ratings yet

- European Intergration LectureDocument5 pagesEuropean Intergration LecturePeggy van der meerNo ratings yet

- European Monetary SystemDocument16 pagesEuropean Monetary SystemNaliniNo ratings yet

- OverviewoftheEurozoneCrisis PPTDocument31 pagesOverviewoftheEurozoneCrisis PPTCaleb ReisNo ratings yet

- Euro CurrencyDocument53 pagesEuro CurrencyShruti Kalantri0% (1)

- European Moneytary System - LapDocument13 pagesEuropean Moneytary System - LapThanh phong HồNo ratings yet

- 7 Europoean Union Studies TE 2020Document57 pages7 Europoean Union Studies TE 2020Gamer HDNo ratings yet

- European Debt Crisis FinalDocument45 pagesEuropean Debt Crisis FinalJagadish NavaleNo ratings yet

- European Monetary IntegrationDocument32 pagesEuropean Monetary IntegrationFlower Power100% (1)

- The ECB and The Single Monetary PolicyDocument12 pagesThe ECB and The Single Monetary PolicyRoy Garin100% (1)

- Eurozone AssignmentDocument7 pagesEurozone AssignmentMuhammad Taha AmerjeeNo ratings yet

- What Is The 'European Monetary System - EMS'Document5 pagesWhat Is The 'European Monetary System - EMS'Swathi JampalaNo ratings yet

- Regional IntegrationDocument40 pagesRegional IntegrationJagannath DasNo ratings yet

- European Union: Presentation Prepared For: International BusinessDocument69 pagesEuropean Union: Presentation Prepared For: International BusinessSrinivas ReddyNo ratings yet

- European Monetary SystemDocument2 pagesEuropean Monetary SystemMelissa Muñoz100% (1)

- Lecture Notes 0Document6 pagesLecture Notes 0Sonia DeolNo ratings yet

- Regional Economic IntegrationDocument50 pagesRegional Economic IntegrationIskandar Zulkarnain KamalluddinNo ratings yet

- Bài đọc 8 Từ bài đọc sau, hãy rút ra những cột mốc chính hình thành liên minh tiền tệ Châu Âu. Cấp độ hội nhập sâu (centralization - tập trung hóa) được thể hiện ở những chi tiết nào?Document15 pagesBài đọc 8 Từ bài đọc sau, hãy rút ra những cột mốc chính hình thành liên minh tiền tệ Châu Âu. Cấp độ hội nhập sâu (centralization - tập trung hóa) được thể hiện ở những chi tiết nào?Khánh NhưNo ratings yet

- Towards A Single Currency: A Brief History of EMUDocument6 pagesTowards A Single Currency: A Brief History of EMUSimona OanaNo ratings yet

- Prepared By: Akanksha Jain Ambika Gupta Prateek Gupta Syed MustansirDocument20 pagesPrepared By: Akanksha Jain Ambika Gupta Prateek Gupta Syed MustansirakankshajnNo ratings yet

- Advantages and Disadvantages of Introducing The Euro: Ireneusz PszczółkaDocument8 pagesAdvantages and Disadvantages of Introducing The Euro: Ireneusz PszczółkaafmorozNo ratings yet

- 7 EMU-Wang AoDocument22 pages7 EMU-Wang AoWang AoNo ratings yet

- Inter Finance Banking Report FinalDocument13 pagesInter Finance Banking Report FinalEvan NoorNo ratings yet

- Introduction of Euro As Common CurrencyDocument53 pagesIntroduction of Euro As Common Currencysuhaspatel84No ratings yet

- European Monetary SystemDocument22 pagesEuropean Monetary SystemasifanisNo ratings yet

- Essay 2 - PrintedDocument5 pagesEssay 2 - PrintedPham_Minh_Quye_2150No ratings yet

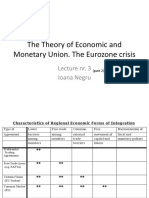

- The Theory of Economic and Monetary Union. The Eurozone CrisisDocument40 pagesThe Theory of Economic and Monetary Union. The Eurozone CrisisSalamander1212No ratings yet

- Escb en WebenDocument36 pagesEscb en WebenAnca NeamțuNo ratings yet

- Eurozone Crisis FinalDocument38 pagesEurozone Crisis FinalCharu PundirNo ratings yet

- Prepared By: Akanksha Jain Ambika Gupta Prateek GuptaDocument19 pagesPrepared By: Akanksha Jain Ambika Gupta Prateek GuptaakankshajnNo ratings yet

- The Single European Currency: Key IssuesDocument20 pagesThe Single European Currency: Key Issuespravo20No ratings yet

- Euro ZoneDocument14 pagesEuro ZoneNidhi GargNo ratings yet

- UNIT I Int Banking and FinanceDocument29 pagesUNIT I Int Banking and FinancesejalNo ratings yet

- Brexit V2Document45 pagesBrexit V2Aya SaadNo ratings yet

- ECB European Central BankDocument12 pagesECB European Central BankHiral SoniNo ratings yet

- The European Union (EU)Document9 pagesThe European Union (EU)aravindpoliticsNo ratings yet

- RTB'S Across The GlobeDocument12 pagesRTB'S Across The GlobevanathimuruganNo ratings yet

- The 1975 Referendum on Europe - Volume 1: Reflections of the ParticipantsFrom EverandThe 1975 Referendum on Europe - Volume 1: Reflections of the ParticipantsNo ratings yet

- A Europe Made of Money: The Emergence of the European Monetary SystemFrom EverandA Europe Made of Money: The Emergence of the European Monetary SystemNo ratings yet

- 230-Executive Board Meeting of NHADocument36 pages230-Executive Board Meeting of NHAHamid Naveed100% (1)

- p9 SlutsDocument1 pagep9 Slutsyonah olupauNo ratings yet

- Proceeding - LengkapDocument13 pagesProceeding - LengkapAnis MarselaNo ratings yet

- Computation of Total Income Income From Business or Profession (Chapter IV D) 273151Document3 pagesComputation of Total Income Income From Business or Profession (Chapter IV D) 273151AVINASH TIWASKARNo ratings yet

- Counsel For AppellantDocument10 pagesCounsel For AppellantScribd Government DocsNo ratings yet

- Traders Royal Bank Vs CA - G.R. No. 93397. March 3, 1997Document11 pagesTraders Royal Bank Vs CA - G.R. No. 93397. March 3, 1997Ebbe DyNo ratings yet

- Fabm 2: Quarter 3 - Module 1 The Statement of Financial Position (Elements, Forms and Its Classifications)Document23 pagesFabm 2: Quarter 3 - Module 1 The Statement of Financial Position (Elements, Forms and Its Classifications)Maria Nikka GarciaNo ratings yet

- Bricks Bussines PlanDocument23 pagesBricks Bussines Plansirajt300No ratings yet

- Hatch IndictmentDocument29 pagesHatch IndictmentMNRNo ratings yet

- 6807-1295 - Mr. Rambabu Prasad GuptaDocument2 pages6807-1295 - Mr. Rambabu Prasad GuptaMahesh SapkotaNo ratings yet

- CH 18Document129 pagesCH 18PopoChandran100% (1)

- Problem Session-2 - 15.03.2012Document44 pagesProblem Session-2 - 15.03.2012markydee_20No ratings yet

- VALUATION by Reynaldo NogralesDocument29 pagesVALUATION by Reynaldo NogralesresiajhiNo ratings yet

- SMEDA Day Care CenterDocument21 pagesSMEDA Day Care Centerincrediblekashif7916No ratings yet

- Activity 3.1Document13 pagesActivity 3.1kel dataNo ratings yet

- Book II Evidence Transaction 2024-25Document91 pagesBook II Evidence Transaction 2024-25Business Partnership DCMD UndipNo ratings yet

- Cover Letter YashpalDocument2 pagesCover Letter YashpalAmrit Pal Singh50% (4)

- Project Course Outline WUDocument6 pagesProject Course Outline WUTamiru BeyeneNo ratings yet

- Entrepreneurship (Woman Entrepreneurs)Document32 pagesEntrepreneurship (Woman Entrepreneurs)RuchiraNo ratings yet

- MBA Questions I Year & II Year Safety ManagementDocument44 pagesMBA Questions I Year & II Year Safety Managementbabu1434100% (3)

- Jollibee CompleteDocument10 pagesJollibee CompleteAbba Dee100% (2)

- Declaration For Housing LoanDocument2 pagesDeclaration For Housing LoanjaberyemeniNo ratings yet

- How Many Parts To Make at Once: Ford W. HarrisDocument5 pagesHow Many Parts To Make at Once: Ford W. HarrisJonathan D. PortaNo ratings yet

- Application For Loan Scheme of JSMFDCDocument5 pagesApplication For Loan Scheme of JSMFDCDhanesh KumarNo ratings yet

- Public Finances Management) Act 1995 (Consolidated To No 57Document49 pagesPublic Finances Management) Act 1995 (Consolidated To No 57desmond100% (1)

- Annual Report 2009Document195 pagesAnnual Report 2009Rahema HasanNo ratings yet

- Personal Banking JamaicaDocument28 pagesPersonal Banking JamaicaDuane WilliamsNo ratings yet

- 2 - Project Evaluation and Programme ManagementDocument26 pages2 - Project Evaluation and Programme ManagementDavid MunyagaNo ratings yet

- Strategic Pricing: Coordinating The Drivers of ProfitabilityDocument26 pagesStrategic Pricing: Coordinating The Drivers of ProfitabilityBien GolecruzNo ratings yet