Download as docx, pdf, or txt

You might also like

- FIN 325-3-2 Final Project Milestone Two Vertical and Horizontal Analysis Saeed Algarni Facebook IDocument9 pagesFIN 325-3-2 Final Project Milestone Two Vertical and Horizontal Analysis Saeed Algarni Facebook IAlison JcNo ratings yet

- CA Real Estate Exam Prep - Transfer of PropertyDocument5 pagesCA Real Estate Exam Prep - Transfer of PropertyThu-An Nguyen Thanh100% (1)

- Ezz Steel Financial AnalysisDocument31 pagesEzz Steel Financial Analysismohamed ashorNo ratings yet

- 01 - FS AnalysisDocument17 pages01 - FS AnalysisRyzel Borja0% (1)

- A. Trend Percentages: RequiredDocument5 pagesA. Trend Percentages: RequiredAngel NuevoNo ratings yet

- FABM 2 Module 5 FS AnalysisDocument9 pagesFABM 2 Module 5 FS AnalysisJOHN PAUL LAGAO100% (4)

- Vertical and Horizontal Analysis ActivityDocument3 pagesVertical and Horizontal Analysis ActivityKenneth FulguerinasNo ratings yet

- Mayes 8e CH03 Problem SetDocument8 pagesMayes 8e CH03 Problem SetBunga Mega WangiNo ratings yet

- Inv 688817583 200279620 202011200114 PDFDocument1 pageInv 688817583 200279620 202011200114 PDFriyasathsafranNo ratings yet

- Lecture4 - Principles of Finance - Financial Analysis - GARIVERADocument31 pagesLecture4 - Principles of Finance - Financial Analysis - GARIVERArenzen jay medenillaNo ratings yet

- Analysis and Interpretation - BalladaDocument4 pagesAnalysis and Interpretation - BalladaClaire Evann Villena EboraNo ratings yet

- Ratio and Trend Analysis (FC)Document26 pagesRatio and Trend Analysis (FC)Cindelyn LibodlibodNo ratings yet

- (Financial Analysis) MANALO, Frances M. LM2-1Document3 pages(Financial Analysis) MANALO, Frances M. LM2-11900118No ratings yet

- Analysis and Interpretation of Financial Statements: What's NewDocument16 pagesAnalysis and Interpretation of Financial Statements: What's NewJanna Gunio50% (2)

- Trend AnalysisDocument1 pageTrend Analysisapi-385117572No ratings yet

- VCMMMM Final RequirementDocument8 pagesVCMMMM Final RequirementMaxine Lois PagaraganNo ratings yet

- Topic 12 - Analysis 2022Document15 pagesTopic 12 - Analysis 2022Danyael millevoNo ratings yet

- FA AnalysisDocument22 pagesFA Analysisharendra choudharyNo ratings yet

- Final Req VCMDocument8 pagesFinal Req VCMMaxine Lois PagaraganNo ratings yet

- Analysis of FS PDF Vertical and HorizontalDocument9 pagesAnalysis of FS PDF Vertical and HorizontalJmaseNo ratings yet

- Analysis and Interpretation of Financial StatementsDocument9 pagesAnalysis and Interpretation of Financial StatementsMckayla Charmian CasumbalNo ratings yet

- Group 9 10Document14 pagesGroup 9 10Jocel CaoNo ratings yet

- 12-Abm-B Busfin PT2Document2 pages12-Abm-B Busfin PT2Dax CruzNo ratings yet

- Finman FinalsDocument4 pagesFinman FinalsDianarose RioNo ratings yet

- MAS 3 SamplesDocument10 pagesMAS 3 SamplesRujean Salar AltejarNo ratings yet

- FS AnalysisDocument5 pagesFS AnalysisLopezNo ratings yet

- Chapter 3 - Financial Statement AnalysisDocument7 pagesChapter 3 - Financial Statement AnalysisLorraine Millama PurayNo ratings yet

- Final Output: Direction: Problem Solving. Presented Below Is The Comparative Financial Statements of TanDocument2 pagesFinal Output: Direction: Problem Solving. Presented Below Is The Comparative Financial Statements of TanCatty Kiara RamirezNo ratings yet

- Quiz BusFinHVRJULIANA VILLANUEVA ABM201-1Document10 pagesQuiz BusFinHVRJULIANA VILLANUEVA ABM201-1Juliana Angela VillanuevaNo ratings yet

- LOPEZ, ELLA MARIE - QUIZ 2 FinAnaRepDocument4 pagesLOPEZ, ELLA MARIE - QUIZ 2 FinAnaRepElla Marie LopezNo ratings yet

- Lopez, Ella Marie - Quiz 2 FinanarepDocument4 pagesLopez, Ella Marie - Quiz 2 FinanarepElla Marie Lopez0% (1)

- New Era University: College of AccountancyDocument4 pagesNew Era University: College of AccountancyPeta AkountNo ratings yet

- W7 Module 6 COMPARATIVE FINANCIAL STATEMENT ANALYSISDocument8 pagesW7 Module 6 COMPARATIVE FINANCIAL STATEMENT ANALYSISDanica VetuzNo ratings yet

- W2020 ACC100 Financial Statement AnalysisDocument5 pagesW2020 ACC100 Financial Statement AnalysisMahmoud ZizoNo ratings yet

- DLP Fs Analysis Concepts and FormatDocument14 pagesDLP Fs Analysis Concepts and FormatDia Did L. RadNo ratings yet

- Analysis and Interpretation of Financial StatementsDocument24 pagesAnalysis and Interpretation of Financial StatementsMariel NatullaNo ratings yet

- Financial Statement Analysis-2Document12 pagesFinancial Statement Analysis-2Glaidel Rodenas PeñaNo ratings yet

- Week 6 AssignmentDocument3 pagesWeek 6 AssignmentLovepreet malhiNo ratings yet

- Abm 2 (Week 2)Document4 pagesAbm 2 (Week 2)testing padasNo ratings yet

- Common-Size Financial StatementsDocument16 pagesCommon-Size Financial StatementsApril IsidroNo ratings yet

- Fabm 2 - Module 6Document8 pagesFabm 2 - Module 6Kelvin SaplaNo ratings yet

- Chapter 3 Working CapitalDocument39 pagesChapter 3 Working Capitalericka casiNo ratings yet

- FINANCIAL ANALYSIS Practice 3Document15 pagesFINANCIAL ANALYSIS Practice 3Hallasgo, Elymar SorianoNo ratings yet

- Horizontal and Vertical AnalysisDocument5 pagesHorizontal and Vertical AnalysisAshley Rouge Capati QuirozNo ratings yet

- Financial Statement AnalysisDocument6 pagesFinancial Statement AnalysisEmmanuel PenullarNo ratings yet

- Module 5Document10 pagesModule 5Rainielle Sy DulatreNo ratings yet

- Unit TestDocument3 pagesUnit TestKetty De GuzmanNo ratings yet

- CH03 ProblemDocument3 pagesCH03 Problemtrangtran01010No ratings yet

- MS03-11-Financial Statement AnalysisDocument13 pagesMS03-11-Financial Statement AnalysisAngel Leah CuambotNo ratings yet

- Long Test BFDocument2 pagesLong Test BFApril De HittaNo ratings yet

- FABMDocument5 pagesFABMAshley Rouge Capati QuirozNo ratings yet

- FinMan (Common-Size Analysis)Document4 pagesFinMan (Common-Size Analysis)Lorren Graze RamiroNo ratings yet

- Basic Finance I.Z.Y.X Comparative Income StatementDocument3 pagesBasic Finance I.Z.Y.X Comparative Income StatementKazia PerinoNo ratings yet

- Balance Sheet Horizontal Analysis Assets 2019 2020 2020 Current AssetsDocument8 pagesBalance Sheet Horizontal Analysis Assets 2019 2020 2020 Current AssetsCINDY MAE DUMAPIASNo ratings yet

- Analysis AppleDocument18 pagesAnalysis AppleAdhira VenkatNo ratings yet

- Local Media2551384955216348707Document4 pagesLocal Media2551384955216348707alinashane obleaNo ratings yet

- Topic 4-5 Financial Planning Tools and ConceptsDocument22 pagesTopic 4-5 Financial Planning Tools and ConceptsAngelica GerondaNo ratings yet

- Rules On Capital Assets Transactions Corporation IndividualDocument2 pagesRules On Capital Assets Transactions Corporation Individualzeref dragneelNo ratings yet

- Executive Summary: Philippines Construction CompanyDocument7 pagesExecutive Summary: Philippines Construction CompanyVon Ulysses CastilloNo ratings yet

- Fundamentals of Accountancy,: Learner's PacketDocument11 pagesFundamentals of Accountancy,: Learner's PacketMarc PagcaliwaganNo ratings yet

- Topic 4-5 Financial Planning Tools and ConceptsDocument22 pagesTopic 4-5 Financial Planning Tools and ConceptsAngelica GerondaNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- Basic Finance Exercice 2Document3 pagesBasic Finance Exercice 2Kazia PerinoNo ratings yet

- Basic Finance - Unit Lesson CLO Major Task 1Document6 pagesBasic Finance - Unit Lesson CLO Major Task 1Kazia PerinoNo ratings yet

- Basic Finance I.Z.Y.X Comparative Income StatementDocument3 pagesBasic Finance I.Z.Y.X Comparative Income StatementKazia PerinoNo ratings yet

- Basic Finance Major OutputDocument3 pagesBasic Finance Major OutputKazia PerinoNo ratings yet

- References: Enabling ActivityDocument3 pagesReferences: Enabling ActivityKazia PerinoNo ratings yet

- Bacc 2a Activity 9 Cellphone BrandsDocument2 pagesBacc 2a Activity 9 Cellphone BrandsKazia PerinoNo ratings yet

- Accounting Primer 1Document39 pagesAccounting Primer 1Mad BullNo ratings yet

- ECON August 20, 2022531 - Lecture Notes 4A1Document7 pagesECON August 20, 2022531 - Lecture Notes 4A1Sam K. Flomo JrNo ratings yet

- MCQ-Business-Management (2 Files Merged)Document47 pagesMCQ-Business-Management (2 Files Merged)Sakthivel PoovanNo ratings yet

- Books of Prime Entry: OutcomesDocument106 pagesBooks of Prime Entry: OutcomesTeboho TshisaNo ratings yet

- The Companies Audit of Cost Accounts Regulations 2020 CompressedDocument116 pagesThe Companies Audit of Cost Accounts Regulations 2020 CompressedMuhammad WaqarNo ratings yet

- Sample Questions - MSC DelhiDocument18 pagesSample Questions - MSC DelhiPriyanath PaulNo ratings yet

- The Philippine EconomyDocument44 pagesThe Philippine EconomyMarie ManansalaNo ratings yet

- The Economist 2021 PDFDocument412 pagesThe Economist 2021 PDFHsn Gn100% (4)

- Zomato - IPODocument9 pagesZomato - IPOPrasun SharmaNo ratings yet

- Notes On The Economics of Enterprise and EntrepreneurshipDocument2 pagesNotes On The Economics of Enterprise and EntrepreneurshipManu KrishNo ratings yet

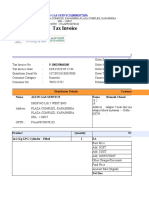

- Tax Invoice: JATIN GAS SERVICE (0000107209)Document4 pagesTax Invoice: JATIN GAS SERVICE (0000107209)RiseNo ratings yet

- 566647370.xls - R15.1 DvorakDocument9 pages566647370.xls - R15.1 DvorakleuleuNo ratings yet

- FM 1 Assignment 1Document3 pagesFM 1 Assignment 1Jelly Ann AndresNo ratings yet

- Stock Valuation - Practice QuestionsDocument6 pagesStock Valuation - Practice QuestionsKam YinNo ratings yet

- Laporan Tahunan 2019 PerusahaanDocument393 pagesLaporan Tahunan 2019 PerusahaanAnton SuryantoNo ratings yet

- Pas 1: Presentation of Financial StatementsDocument16 pagesPas 1: Presentation of Financial StatementsKryzzel Anne JonNo ratings yet

- Vul Set A Set B Set C With KeywordsDocument24 pagesVul Set A Set B Set C With KeywordsKenneth QuiranteNo ratings yet

- PINCodeDocument3 pagesPINCodeAli Shaikh0% (1)

- Group 5 QADocument12 pagesGroup 5 QADanica RaymundoNo ratings yet

- Advantage and DisadvantageDocument3 pagesAdvantage and Disadvantagemico lequinNo ratings yet

- Practical Accounting 2 by Antonio Dayag: Home Office, Branch, and AgencyDocument43 pagesPractical Accounting 2 by Antonio Dayag: Home Office, Branch, and Agencysino ako100% (2)

- Practical Financial Management 7Th Edition Lasher Test Bank Full Chapter PDFDocument67 pagesPractical Financial Management 7Th Edition Lasher Test Bank Full Chapter PDFAdrianLynchpdci100% (10)

- Ratio Rate Proportion PracticeDocument5 pagesRatio Rate Proportion PracticeMessi TaiNo ratings yet

- Australian Super BrochureDocument4 pagesAustralian Super Brochurehail capiralNo ratings yet

- 1bad5ce9ccd0849a675b4e7b06ab344a70c181080d51ebc0049dee6d00b990e8Document18 pages1bad5ce9ccd0849a675b4e7b06ab344a70c181080d51ebc0049dee6d00b990e8Yosra YacoubiNo ratings yet

- Illustrative Ind As Standalone Financial Statements: XYZ Limited Standalone Balance Sheet As at 31 March 2020Document1 pageIllustrative Ind As Standalone Financial Statements: XYZ Limited Standalone Balance Sheet As at 31 March 2020Nanda KumarNo ratings yet

- Market Cap To GDP RatioDocument8 pagesMarket Cap To GDP RatiokalpeshNo ratings yet

- Day 1 Dec 2017Document93 pagesDay 1 Dec 2017Abdul HaseebNo ratings yet