Download as pdf or txt

You might also like

- Millionaire Expat: How To Build Wealth Living OverseasFrom EverandMillionaire Expat: How To Build Wealth Living OverseasRating: 3 out of 5 stars3/5 (10)

- Case 1Document130 pagesCase 1Mert KaygusuzNo ratings yet

- Capital Budgeting Idea For Netflix Inc.Document26 pagesCapital Budgeting Idea For Netflix Inc.PraNo ratings yet

- Q4 2010 GlenviewDocument22 pagesQ4 2010 GlenviewaviNo ratings yet

- Orbis Equity Annual Reports 2011Document32 pagesOrbis Equity Annual Reports 2011noranycNo ratings yet

- Raport Fitch StatiDocument2 pagesRaport Fitch StatiRadu BurdujanNo ratings yet

- Andrews AnalysisDocument11 pagesAndrews Analysisapi-334753705No ratings yet

- Currency Report Card - USD Recovery: Three Month Forecast ReturnsDocument26 pagesCurrency Report Card - USD Recovery: Three Month Forecast Returnsderailedcapitalism.comNo ratings yet

- Foriegn Exchange Exposure & Risk ManagementDocument100 pagesForiegn Exchange Exposure & Risk Managementsathvik.g.m.s.sai100% (1)

- BIS - Triennial Central Bank Survey Interest Rate (2022)Document21 pagesBIS - Triennial Central Bank Survey Interest Rate (2022)Bautista GriffiniNo ratings yet

- rpfx22 FXDocument23 pagesrpfx22 FXVincent LyNo ratings yet

- AA Fixed IncomeDocument22 pagesAA Fixed Incomenbfbr536No ratings yet

- Triennial Central Bank Survey: Foreign Exchange Turnover in April 2016Document23 pagesTriennial Central Bank Survey: Foreign Exchange Turnover in April 2016merveNo ratings yet

- AA EquityDocument21 pagesAA EquityPedro CastroNo ratings yet

- Shikhar Sharma Theswedishinvestor Iag1-HmmDocument5 pagesShikhar Sharma Theswedishinvestor Iag1-HmmresourcesficNo ratings yet

- International Banking and Financial Markets DevelopmentDocument174 pagesInternational Banking and Financial Markets Developmentthe1uploaderNo ratings yet

- Eun 10e International Financial Management PPT CH05 AccessibleDocument43 pagesEun 10e International Financial Management PPT CH05 AccessibleMaciel García FuentesNo ratings yet

- Document 3-3Document55 pagesDocument 3-3Loyi TimbaNo ratings yet

- Exchange Rate ManagementDocument100 pagesExchange Rate ManagementNitish MunshiNo ratings yet

- First Q Uarter R Eport 2010Document16 pagesFirst Q Uarter R Eport 2010richardck20No ratings yet

- Methodology SP Equity Futures and Currency Futures IndicesDocument12 pagesMethodology SP Equity Futures and Currency Futures Indicesarjunmadan1No ratings yet

- Dollar Cost Averaging vs. Lump Sum Investing: Benjamin FelixDocument17 pagesDollar Cost Averaging vs. Lump Sum Investing: Benjamin FelixCláudioNo ratings yet

- Document 3-2Document56 pagesDocument 3-2Loyi TimbaNo ratings yet

- Sticky Wicket of Indian Companies - Foreign Currency Convertible BondsDocument17 pagesSticky Wicket of Indian Companies - Foreign Currency Convertible BondsVishakha Geeta ChetanNo ratings yet

- Assignment 1Document16 pagesAssignment 1Wajeeha SiddiquiNo ratings yet

- Patterns in International Banking: Key Take-Aways and ImplicationsDocument14 pagesPatterns in International Banking: Key Take-Aways and ImplicationsDenis DenisNo ratings yet

- Best Investement-High Res-Trust MFDocument224 pagesBest Investement-High Res-Trust MFDDM NABARD GIRIDIHNo ratings yet

- Assignment On Carry Trading & Value TradingDocument12 pagesAssignment On Carry Trading & Value TradingMasuma Binte SakhawatNo ratings yet

- Asia Securities Industry and Financial Markets Association: Factors That Assist The Development of Liquidity 2009Document18 pagesAsia Securities Industry and Financial Markets Association: Factors That Assist The Development of Liquidity 2009Asian Development BankNo ratings yet

- FOREX ManagementDocument24 pagesFOREX ManagementSaksham MathurNo ratings yet

- Model QuestionDocument4 pagesModel QuestionJahidul IslamNo ratings yet

- Foreign Currency ConversionDocument39 pagesForeign Currency ConversionRutuja KulkarniNo ratings yet

- Fullerton SGD Heritage Income: June 2020Document3 pagesFullerton SGD Heritage Income: June 2020InaRizkyNo ratings yet

- Effects of Implementing A Fixed Exchange Rate System in India-Edit 1Document9 pagesEffects of Implementing A Fixed Exchange Rate System in India-Edit 1Sibi PariNo ratings yet

- Dollarbull ETF Handbook (Dec 2022)Document24 pagesDollarbull ETF Handbook (Dec 2022)Jai HiralalNo ratings yet

- Questionnaire "A Study On Investment Behaviour of Academician With Special Reference To Surat City"Document7 pagesQuestionnaire "A Study On Investment Behaviour of Academician With Special Reference To Surat City"Bhakti MehtaNo ratings yet

- Dailyfx Guide en 2021 q4 AudDocument7 pagesDailyfx Guide en 2021 q4 AudVeljko KerčevićNo ratings yet

- Cma Final - Book 2 - Forex and DerivativesDocument156 pagesCma Final - Book 2 - Forex and DerivativesadhishsirNo ratings yet

- Cma Final - Book 2 - Forex and Derivatives - RevisedDocument163 pagesCma Final - Book 2 - Forex and Derivatives - RevisedadhishsirNo ratings yet

- Document 3Document58 pagesDocument 3Loyi TimbaNo ratings yet

- Fundamental & Technical Analysis of Forex MarketDocument82 pagesFundamental & Technical Analysis of Forex Marketlokeshpatel100% (2)

- FundfactsDocument3 pagesFundfactsNavaneethakrishnan KannanNo ratings yet

- New Investment Avenues in India: Wealth InsightDocument50 pagesNew Investment Avenues in India: Wealth InsightSayed WahabNo ratings yet

- Forex Pages 42 90Document49 pagesForex Pages 42 90RITZ BROWN100% (1)

- Capital Market Assumptions For Major Asset Classes: Executive SummaryDocument20 pagesCapital Market Assumptions For Major Asset Classes: Executive SummaryjitenparekhNo ratings yet

- Equity / Growth Fund Debt/ Income FundDocument6 pagesEquity / Growth Fund Debt/ Income FundChiunnu JanuNo ratings yet

- WP 2308Document36 pagesWP 2308erjohngonzNo ratings yet

- AA Expected Returns MethodologyDocument18 pagesAA Expected Returns MethodologyPedro CastroNo ratings yet

- sr667 PDFDocument20 pagessr667 PDFbhavesh74No ratings yet

- Think FundsIndia November 2014Document8 pagesThink FundsIndia November 2014marketingNo ratings yet

- HDFC Mutual FundDocument93 pagesHDFC Mutual FundKomal MansukhaniNo ratings yet

- Balance of Payment 20 PDFDocument79 pagesBalance of Payment 20 PDFRiyaNo ratings yet

- SREFP Brochure BookletDocument20 pagesSREFP Brochure BookletKaran GuptaNo ratings yet

- The Missing Perspective - SWF Part 2Document4 pagesThe Missing Perspective - SWF Part 2dio dioNo ratings yet

- Q3 2021 Market Outlook Report E BookDocument39 pagesQ3 2021 Market Outlook Report E BookMiliana SophiosNo ratings yet

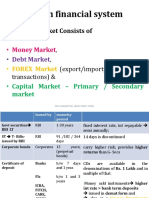

- Indian Financial System: Financial Market Consists ofDocument67 pagesIndian Financial System: Financial Market Consists ofTHILAGALAKSHMI M DNo ratings yet

- Market Commentary 1.28.2013Document3 pagesMarket Commentary 1.28.2013CLORIS4No ratings yet

- Chapter - 8 Foreign Exchange Forwards and Futures: Example 8.1Document40 pagesChapter - 8 Foreign Exchange Forwards and Futures: Example 8.1debojyotiNo ratings yet

- December 2020: Quarterly Commentary ReportDocument8 pagesDecember 2020: Quarterly Commentary ReportYog MehtaNo ratings yet

- Ongleaf Artners Unds: Emi-Nnual EportDocument48 pagesOngleaf Artners Unds: Emi-Nnual Eporteric695No ratings yet

- Common Sense Retirement Planning: Home, Savings and InvestmentFrom EverandCommon Sense Retirement Planning: Home, Savings and InvestmentNo ratings yet

- AndebolDocument14 pagesAndebolPedro CastroNo ratings yet

- Relative Clauses Worksheet and CorrectionDocument2 pagesRelative Clauses Worksheet and CorrectionPedro CastroNo ratings yet

- Revisions Worksheet and CorrectionDocument5 pagesRevisions Worksheet and CorrectionPedro CastroNo ratings yet

- Useful Expressions - EnquiryDocument2 pagesUseful Expressions - EnquiryPedro CastroNo ratings yet

- Predicting Equity Returns With InflationDocument13 pagesPredicting Equity Returns With InflationPedro CastroNo ratings yet

- BiGAT IntroducaoDocument20 pagesBiGAT IntroducaoPedro CastroNo ratings yet

- The Fall of The TitansDocument11 pagesThe Fall of The TitansPedro CastroNo ratings yet

- BiGAT Padroes ClassicosDocument1 pageBiGAT Padroes ClassicosPedro CastroNo ratings yet

- AA CommoditiesDocument20 pagesAA CommoditiesPedro CastroNo ratings yet

- AA Expected Returns MethodologyDocument18 pagesAA Expected Returns MethodologyPedro CastroNo ratings yet

- AA EquityDocument21 pagesAA EquityPedro CastroNo ratings yet

- 2 Consistent Compounder StocksDocument2 pages2 Consistent Compounder StocksKunal KhandelwalNo ratings yet

- Problem Set 7 - FINS3630 (Solutions)Document4 pagesProblem Set 7 - FINS3630 (Solutions)DWdeNo ratings yet

- Constellation Software Inc. Q308: Historical Figures Restated To Comply With Revised DefinitionDocument3 pagesConstellation Software Inc. Q308: Historical Figures Restated To Comply With Revised DefinitionrNo ratings yet

- MCQ ManagementDocument47 pagesMCQ ManagementSantosh ThapaNo ratings yet

- Third Week - Dsadfor PrintingDocument14 pagesThird Week - Dsadfor Printingyukiro rineva0% (2)

- RICS On Valuation of Development LandDocument26 pagesRICS On Valuation of Development LandKartik LadNo ratings yet

- Exercises For Stock Valuation: InvestmentsDocument2 pagesExercises For Stock Valuation: InvestmentsMiguelNo ratings yet

- Role of Participants of The Stock MarketDocument16 pagesRole of Participants of The Stock MarketDanielNo ratings yet

- Nifty 4Document4 pagesNifty 4Suhas SalehittalNo ratings yet

- Capital Budgeting Decisions NotesDocument15 pagesCapital Budgeting Decisions NotesEbbyNo ratings yet

- Investment Attitude QuestionnaireDocument6 pagesInvestment Attitude QuestionnairerakeshmadNo ratings yet

- Important Questions For CBSE Class 12 Macro Economics Chapter 3 PDFDocument10 pagesImportant Questions For CBSE Class 12 Macro Economics Chapter 3 PDFAlans TechnicalNo ratings yet

- OMBF 301 C&FM AssignmentDocument1 pageOMBF 301 C&FM AssignmentSuhas PawarNo ratings yet

- Pakistan Stock ExchangeDocument11 pagesPakistan Stock Exchangeumar jilaniNo ratings yet

- Commodities MarketsDocument6 pagesCommodities MarketsMukul NarayanNo ratings yet

- East Cameron Partners The Sukuk BondDocument9 pagesEast Cameron Partners The Sukuk BondAsadNo ratings yet

- How To Download Fundamentals of Investing Pearson Series in Finance Ebook PDF Version Ebook PDF Docx Kindle Full ChapterDocument36 pagesHow To Download Fundamentals of Investing Pearson Series in Finance Ebook PDF Version Ebook PDF Docx Kindle Full Chapterannie.root658100% (33)

- 1 Securities Markets and Types of SecuritiesDocument13 pages1 Securities Markets and Types of SecuritiesMuskan SanghiNo ratings yet

- Labour-Based Works Methodology Experiences From ILO: Module 2: Planning, Design, Appraisal and ImplementationDocument46 pagesLabour-Based Works Methodology Experiences From ILO: Module 2: Planning, Design, Appraisal and ImplementationMarvin MessiNo ratings yet

- 3) Market and ClassificationDocument28 pages3) Market and ClassificationRanjit SatavNo ratings yet

- Ejercicio Nro 8 SolucionnnnnnDocument9 pagesEjercicio Nro 8 SolucionnnnnnSugar Leonardo Herrera CoaquiraNo ratings yet

- Multinational Accounting: Foreign Currency Transactions and Financial InstrumentsDocument44 pagesMultinational Accounting: Foreign Currency Transactions and Financial InstrumentsWidya PertiwiNo ratings yet

- Garcia Vs Boi GR No. 92024Document2 pagesGarcia Vs Boi GR No. 92024JayMichaelAquinoMarquezNo ratings yet

- CASH AND CASH EQUIVALENTS TheoDocument1 pageCASH AND CASH EQUIVALENTS Theovenice cambryNo ratings yet

- Chapter 9 Mini CaseDocument6 pagesChapter 9 Mini CaseStephen MagudhaNo ratings yet

- Sejal - Summer Internship Report PDFDocument49 pagesSejal - Summer Internship Report PDFsejalyadav1005No ratings yet

- Cost of Capital and Firm Performance of ESG Companies What Can We Infer From COVID-19 PandemicDocument26 pagesCost of Capital and Firm Performance of ESG Companies What Can We Infer From COVID-19 PandemicChinapratha SitikornchayarpongNo ratings yet