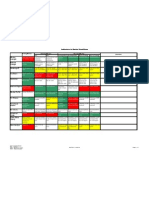

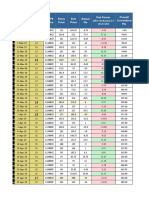

Black-Scholes Options Pricing Calculator: Effect of A Change in The Stock Price

Black-Scholes Options Pricing Calculator: Effect of A Change in The Stock Price

You might also like

- Courtney Smith - How To Make A Living Trading Foreign ExchangeDocument35 pagesCourtney Smith - How To Make A Living Trading Foreign Exchangeduyphung1234100% (1)

- Group 1 American Greetings ReportDocument13 pagesGroup 1 American Greetings Reportshershah hassan100% (1)

- A Rhino Update (Aug '23)Document27 pagesA Rhino Update (Aug '23)manhphuho88No ratings yet

- Option Buying Setup: by - Jitendra JainDocument17 pagesOption Buying Setup: by - Jitendra JainmonucoolNo ratings yet

- Option Premium CalculatorDocument6 pagesOption Premium CalculatorAbhinavVermaNo ratings yet

- BANKNIFTY Options Open Interest AnalysisDocument20 pagesBANKNIFTY Options Open Interest AnalysisindianroadromeoNo ratings yet

- Open High Low Close H-O O-L Min ValueDocument5 pagesOpen High Low Close H-O O-L Min ValueJeniffer RayenNo ratings yet

- Max Pain AnalysisDocument3 pagesMax Pain Analysisanindya pal100% (1)

- Options Open Interest AnalysisDocument19 pagesOptions Open Interest AnalysisManish SharmaNo ratings yet

- CPR Formula ExcelsheetDocument2 pagesCPR Formula ExcelsheetHarshit KarnaniNo ratings yet

- Gann - Enthios CalculatorDocument13 pagesGann - Enthios CalculatorRaghavendra KNo ratings yet

- Rahul Mohindar Osc (RMO)Document2 pagesRahul Mohindar Osc (RMO)Marcelo Plaza0% (1)

- FM4, Exercises 17, Black-ScholesDocument54 pagesFM4, Exercises 17, Black-Scholeswenhao zhouNo ratings yet

- Hedging Breakeven CalculatorDocument11 pagesHedging Breakeven CalculatorjitendrasutarNo ratings yet

- Effect of Return and Volatility Calculation On Option Pricing: Using BankniftyDocument8 pagesEffect of Return and Volatility Calculation On Option Pricing: Using BankniftyKolekarMakrandMahadeoNo ratings yet

- Buy Level Buy LevelDocument9 pagesBuy Level Buy LevelJeniffer RayenNo ratings yet

- Call OI Strike Put OI Call Value Put Value Total StrikeDocument19 pagesCall OI Strike Put OI Call Value Put Value Total StrikejitendrasutarNo ratings yet

- Indicators Manual 2012Document117 pagesIndicators Manual 2012upkumaraNo ratings yet

- Intraday CALLS: For Long Call (Intraday) 2,000 125Document12 pagesIntraday CALLS: For Long Call (Intraday) 2,000 125DNYANESH MASKENo ratings yet

- Option Greeks 5 Tools To Measure RiskDocument23 pagesOption Greeks 5 Tools To Measure RiskdaksheduhubNo ratings yet

- Trader's Destination Intraday Calculators: Edit The Cells in Black Only, Dont Edit Any Other CellsDocument2 pagesTrader's Destination Intraday Calculators: Edit The Cells in Black Only, Dont Edit Any Other CellsKubera TradeNo ratings yet

- 0.1.JustNifty TA 1 (By Ilango)Document849 pages0.1.JustNifty TA 1 (By Ilango)Jeniffer RayenNo ratings yet

- Crudeoil 6pm StrategyDocument2 pagesCrudeoil 6pm StrategymohanNo ratings yet

- Nifty SignalDocument14 pagesNifty SignalmahendraboradeNo ratings yet

- Supertrend (7,3) BUY Signal Generated, Technical Analysis ScannerDocument2 pagesSupertrend (7,3) BUY Signal Generated, Technical Analysis ScannerSuryakant PatilNo ratings yet

- ShShort Straddle StrategyDocument6 pagesShShort Straddle StrategyDeepak RanaNo ratings yet

- Revision Live SessionsDocument19 pagesRevision Live SessionsYash GangwalNo ratings yet

- Student Trading Guide - IntroductionDocument39 pagesStudent Trading Guide - IntroductionB.R SinghNo ratings yet

- Call OI Strike Put OI Call Value Put Value Total StrikeDocument4 pagesCall OI Strike Put OI Call Value Put Value Total Striked_narnoliaNo ratings yet

- Nifty Intraday Levels TableDocument8 pagesNifty Intraday Levels TableManoj PalNo ratings yet

- Open Interest BasicsDocument20 pagesOpen Interest Basicskaran MNo ratings yet

- Trading Journal BRODocument21 pagesTrading Journal BROjobertNo ratings yet

- Wave CalculatorDocument2 pagesWave CalculatorArun VinodNo ratings yet

- NIFTY Options Open Interest AnalysisDocument26 pagesNIFTY Options Open Interest AnalysisindianroadromeoNo ratings yet

- Live Trading Session With Rishikesh SirDocument6 pagesLive Trading Session With Rishikesh SirYash GangwalNo ratings yet

- Bajaj AutoDocument4 pagesBajaj AutoSathyamurthy RamanujamNo ratings yet

- Elliot Wave Calaculator ForexDocument3 pagesElliot Wave Calaculator ForexAlvin CardonaNo ratings yet

- Option ExampleDocument7 pagesOption ExampleKaren LiuNo ratings yet

- Previous Day'S Price: Projection For TodayDocument5 pagesPrevious Day'S Price: Projection For TodaycratnanamNo ratings yet

- Shruti Jain Smart Task 02Document7 pagesShruti Jain Smart Task 02shruti jainNo ratings yet

- Implied Volatility and Profit vs. Loss: 1-888-OPTIONSDocument35 pagesImplied Volatility and Profit vs. Loss: 1-888-OPTIONSkaruthi_1979No ratings yet

- Indicator Vs Market ConditionsDocument1 pageIndicator Vs Market ConditionsbrijeshagraNo ratings yet

- Folio Dashboard: PolarisDocument28 pagesFolio Dashboard: PolarisJeniffer RayenNo ratings yet

- Nifty Intraday OptionsDocument63 pagesNifty Intraday OptionsmuthureNo ratings yet

- Option Chain-20-01-2022Document10 pagesOption Chain-20-01-2022vpritNo ratings yet

- Shiv Trend FinderDocument15 pagesShiv Trend FinderstelsoftNo ratings yet

- Level For Long Level For ShortDocument2 pagesLevel For Long Level For ShortPulkit AgarwalNo ratings yet

- Technical Analysis EnglishDocument30 pagesTechnical Analysis EnglishRAJESH KUMARNo ratings yet

- Options Open Interest AnalysisDocument19 pagesOptions Open Interest AnalysisMan ZealNo ratings yet

- Final Webinar TWKJ July2020 PDFDocument58 pagesFinal Webinar TWKJ July2020 PDFRohit PurandareNo ratings yet

- Sanjeevani Forex Education RewDocument34 pagesSanjeevani Forex Education RewfaiyazaslamNo ratings yet

- 9 Option Strategies CH 11Document35 pages9 Option Strategies CH 11RLG631No ratings yet

- Technical Indicator ExplanationDocument4 pagesTechnical Indicator ExplanationfranraizerNo ratings yet

- Technical Analysis GuideDocument38 pagesTechnical Analysis Guidealay2986100% (1)

- Financial Option Trading Data AnalysisDocument25 pagesFinancial Option Trading Data AnalysisPranav SinghNo ratings yet

- Option PDFDocument4 pagesOption PDFjallwynaldrinNo ratings yet

- The Only HEIKIN ASHI Day Trading StrategyDocument3 pagesThe Only HEIKIN ASHI Day Trading StrategySurya Ningrat0% (1)

- Share Chart Option StrategiesDocument24 pagesShare Chart Option StrategiespdservicesNo ratings yet

- MCX Strategy (By Bhavesh Bhavsar)Document1 pageMCX Strategy (By Bhavesh Bhavsar)honeyvijayNo ratings yet

- SAP Dictionary HRDocument714 pagesSAP Dictionary HRFilippos StamatiadisNo ratings yet

- CCPSDocument2 pagesCCPSelitevaluation2022No ratings yet

- Reserve Bank of India - Notifications DEAF PDFDocument1 pageReserve Bank of India - Notifications DEAF PDF9901754662No ratings yet

- The Wealthy Barber 1Document11 pagesThe Wealthy Barber 1api-526752866No ratings yet

- Income Tax: Dr. Sandeep Kumar Department of Commerce, St. Xavier's College, RanchiDocument23 pagesIncome Tax: Dr. Sandeep Kumar Department of Commerce, St. Xavier's College, Ranchinirman chawlaNo ratings yet

- Institute of Bankers of Sri Lanka: D 07 - Investment BankingDocument17 pagesInstitute of Bankers of Sri Lanka: D 07 - Investment BankingSuvindu DulhanNo ratings yet

- Complaint Against Zions BankDocument56 pagesComplaint Against Zions BankThe Salt Lake TribuneNo ratings yet

- Green River Rodmakers ETP3000 S07Document10 pagesGreen River Rodmakers ETP3000 S07Vlad George PopescuNo ratings yet

- Far410 Dec 2019Document8 pagesFar410 Dec 2019NurulHuda Auni Binti Ab RahmanNo ratings yet

- Chapter 10 Decentralization: Responsibility Accounting, Performance Evaluation, and Transfer PricingDocument70 pagesChapter 10 Decentralization: Responsibility Accounting, Performance Evaluation, and Transfer PricingEninta SebayangNo ratings yet

- ReceiptsDocument9 pagesReceiptsinfoNo ratings yet

- Collateral Allocation MechanismsDocument3 pagesCollateral Allocation MechanismsaNo ratings yet

- Actuarial MathematicsDocument32 pagesActuarial MathematicsAhsan HabibNo ratings yet

- Working CapitalDocument9 pagesWorking CapitalLakshya AgrawalNo ratings yet

- Analysis Kisumu-County 2023 FinalDocument20 pagesAnalysis Kisumu-County 2023 FinaluongozifreshNo ratings yet

- B Com Hons Sem 2 EditedDocument22 pagesB Com Hons Sem 2 EditedShikha GoyalNo ratings yet

- Midterm Assignment 6: Frando, Maria Teresa S. OL33E63Document3 pagesMidterm Assignment 6: Frando, Maria Teresa S. OL33E63Maria Teresa Frando CahandingNo ratings yet

- Draft AtapDocument9 pagesDraft AtapMuhd ArifNo ratings yet

- Project Report On: Submitted byDocument47 pagesProject Report On: Submitted byManoj ParabNo ratings yet

- Aber Report 2020 - en - 4Document92 pagesAber Report 2020 - en - 4ForkLogNo ratings yet

- Capital BudgetingDocument12 pagesCapital BudgetingKhadar50% (4)

- Fundamentals of Computer Problem Solving: Assignment 3Document7 pagesFundamentals of Computer Problem Solving: Assignment 3Nor Syahirah Mohd NorNo ratings yet

- Definition of Capital AllowancesDocument9 pagesDefinition of Capital AllowancesAdesolaNo ratings yet

- Foreign Capital and Economic Growth of IndiaDocument23 pagesForeign Capital and Economic Growth of IndiaMitesh ShahNo ratings yet

- India - MS Economics Aug 2022Document11 pagesIndia - MS Economics Aug 2022Salim MiyaNo ratings yet

- BOP Category Guide PDFDocument29 pagesBOP Category Guide PDFsimbamikeNo ratings yet

- A Project Report HDFC BANKDocument48 pagesA Project Report HDFC BANKVikas SinghNo ratings yet

- Draft Requirements For Tax Declaration TranferDocument4 pagesDraft Requirements For Tax Declaration TranfercarmanvernonNo ratings yet

Download as xls, pdf, or txt

You might also like

- Courtney Smith - How To Make A Living Trading Foreign ExchangeDocument35 pagesCourtney Smith - How To Make A Living Trading Foreign Exchangeduyphung1234100% (1)

- Group 1 American Greetings ReportDocument13 pagesGroup 1 American Greetings Reportshershah hassan100% (1)

- A Rhino Update (Aug '23)Document27 pagesA Rhino Update (Aug '23)manhphuho88No ratings yet

- Option Buying Setup: by - Jitendra JainDocument17 pagesOption Buying Setup: by - Jitendra JainmonucoolNo ratings yet

- Option Premium CalculatorDocument6 pagesOption Premium CalculatorAbhinavVermaNo ratings yet

- BANKNIFTY Options Open Interest AnalysisDocument20 pagesBANKNIFTY Options Open Interest AnalysisindianroadromeoNo ratings yet

- Open High Low Close H-O O-L Min ValueDocument5 pagesOpen High Low Close H-O O-L Min ValueJeniffer RayenNo ratings yet

- Max Pain AnalysisDocument3 pagesMax Pain Analysisanindya pal100% (1)

- Options Open Interest AnalysisDocument19 pagesOptions Open Interest AnalysisManish SharmaNo ratings yet

- CPR Formula ExcelsheetDocument2 pagesCPR Formula ExcelsheetHarshit KarnaniNo ratings yet

- Gann - Enthios CalculatorDocument13 pagesGann - Enthios CalculatorRaghavendra KNo ratings yet

- Rahul Mohindar Osc (RMO)Document2 pagesRahul Mohindar Osc (RMO)Marcelo Plaza0% (1)

- FM4, Exercises 17, Black-ScholesDocument54 pagesFM4, Exercises 17, Black-Scholeswenhao zhouNo ratings yet

- Hedging Breakeven CalculatorDocument11 pagesHedging Breakeven CalculatorjitendrasutarNo ratings yet

- Effect of Return and Volatility Calculation On Option Pricing: Using BankniftyDocument8 pagesEffect of Return and Volatility Calculation On Option Pricing: Using BankniftyKolekarMakrandMahadeoNo ratings yet

- Buy Level Buy LevelDocument9 pagesBuy Level Buy LevelJeniffer RayenNo ratings yet

- Call OI Strike Put OI Call Value Put Value Total StrikeDocument19 pagesCall OI Strike Put OI Call Value Put Value Total StrikejitendrasutarNo ratings yet

- Indicators Manual 2012Document117 pagesIndicators Manual 2012upkumaraNo ratings yet

- Intraday CALLS: For Long Call (Intraday) 2,000 125Document12 pagesIntraday CALLS: For Long Call (Intraday) 2,000 125DNYANESH MASKENo ratings yet

- Option Greeks 5 Tools To Measure RiskDocument23 pagesOption Greeks 5 Tools To Measure RiskdaksheduhubNo ratings yet

- Trader's Destination Intraday Calculators: Edit The Cells in Black Only, Dont Edit Any Other CellsDocument2 pagesTrader's Destination Intraday Calculators: Edit The Cells in Black Only, Dont Edit Any Other CellsKubera TradeNo ratings yet

- 0.1.JustNifty TA 1 (By Ilango)Document849 pages0.1.JustNifty TA 1 (By Ilango)Jeniffer RayenNo ratings yet

- Crudeoil 6pm StrategyDocument2 pagesCrudeoil 6pm StrategymohanNo ratings yet

- Nifty SignalDocument14 pagesNifty SignalmahendraboradeNo ratings yet

- Supertrend (7,3) BUY Signal Generated, Technical Analysis ScannerDocument2 pagesSupertrend (7,3) BUY Signal Generated, Technical Analysis ScannerSuryakant PatilNo ratings yet

- ShShort Straddle StrategyDocument6 pagesShShort Straddle StrategyDeepak RanaNo ratings yet

- Revision Live SessionsDocument19 pagesRevision Live SessionsYash GangwalNo ratings yet

- Student Trading Guide - IntroductionDocument39 pagesStudent Trading Guide - IntroductionB.R SinghNo ratings yet

- Call OI Strike Put OI Call Value Put Value Total StrikeDocument4 pagesCall OI Strike Put OI Call Value Put Value Total Striked_narnoliaNo ratings yet

- Nifty Intraday Levels TableDocument8 pagesNifty Intraday Levels TableManoj PalNo ratings yet

- Open Interest BasicsDocument20 pagesOpen Interest Basicskaran MNo ratings yet

- Trading Journal BRODocument21 pagesTrading Journal BROjobertNo ratings yet

- Wave CalculatorDocument2 pagesWave CalculatorArun VinodNo ratings yet

- NIFTY Options Open Interest AnalysisDocument26 pagesNIFTY Options Open Interest AnalysisindianroadromeoNo ratings yet

- Live Trading Session With Rishikesh SirDocument6 pagesLive Trading Session With Rishikesh SirYash GangwalNo ratings yet

- Bajaj AutoDocument4 pagesBajaj AutoSathyamurthy RamanujamNo ratings yet

- Elliot Wave Calaculator ForexDocument3 pagesElliot Wave Calaculator ForexAlvin CardonaNo ratings yet

- Option ExampleDocument7 pagesOption ExampleKaren LiuNo ratings yet

- Previous Day'S Price: Projection For TodayDocument5 pagesPrevious Day'S Price: Projection For TodaycratnanamNo ratings yet

- Shruti Jain Smart Task 02Document7 pagesShruti Jain Smart Task 02shruti jainNo ratings yet

- Implied Volatility and Profit vs. Loss: 1-888-OPTIONSDocument35 pagesImplied Volatility and Profit vs. Loss: 1-888-OPTIONSkaruthi_1979No ratings yet

- Indicator Vs Market ConditionsDocument1 pageIndicator Vs Market ConditionsbrijeshagraNo ratings yet

- Folio Dashboard: PolarisDocument28 pagesFolio Dashboard: PolarisJeniffer RayenNo ratings yet

- Nifty Intraday OptionsDocument63 pagesNifty Intraday OptionsmuthureNo ratings yet

- Option Chain-20-01-2022Document10 pagesOption Chain-20-01-2022vpritNo ratings yet

- Shiv Trend FinderDocument15 pagesShiv Trend FinderstelsoftNo ratings yet

- Level For Long Level For ShortDocument2 pagesLevel For Long Level For ShortPulkit AgarwalNo ratings yet

- Technical Analysis EnglishDocument30 pagesTechnical Analysis EnglishRAJESH KUMARNo ratings yet

- Options Open Interest AnalysisDocument19 pagesOptions Open Interest AnalysisMan ZealNo ratings yet

- Final Webinar TWKJ July2020 PDFDocument58 pagesFinal Webinar TWKJ July2020 PDFRohit PurandareNo ratings yet

- Sanjeevani Forex Education RewDocument34 pagesSanjeevani Forex Education RewfaiyazaslamNo ratings yet

- 9 Option Strategies CH 11Document35 pages9 Option Strategies CH 11RLG631No ratings yet

- Technical Indicator ExplanationDocument4 pagesTechnical Indicator ExplanationfranraizerNo ratings yet

- Technical Analysis GuideDocument38 pagesTechnical Analysis Guidealay2986100% (1)

- Financial Option Trading Data AnalysisDocument25 pagesFinancial Option Trading Data AnalysisPranav SinghNo ratings yet

- Option PDFDocument4 pagesOption PDFjallwynaldrinNo ratings yet

- The Only HEIKIN ASHI Day Trading StrategyDocument3 pagesThe Only HEIKIN ASHI Day Trading StrategySurya Ningrat0% (1)

- Share Chart Option StrategiesDocument24 pagesShare Chart Option StrategiespdservicesNo ratings yet

- MCX Strategy (By Bhavesh Bhavsar)Document1 pageMCX Strategy (By Bhavesh Bhavsar)honeyvijayNo ratings yet

- SAP Dictionary HRDocument714 pagesSAP Dictionary HRFilippos StamatiadisNo ratings yet

- CCPSDocument2 pagesCCPSelitevaluation2022No ratings yet

- Reserve Bank of India - Notifications DEAF PDFDocument1 pageReserve Bank of India - Notifications DEAF PDF9901754662No ratings yet

- The Wealthy Barber 1Document11 pagesThe Wealthy Barber 1api-526752866No ratings yet

- Income Tax: Dr. Sandeep Kumar Department of Commerce, St. Xavier's College, RanchiDocument23 pagesIncome Tax: Dr. Sandeep Kumar Department of Commerce, St. Xavier's College, Ranchinirman chawlaNo ratings yet

- Institute of Bankers of Sri Lanka: D 07 - Investment BankingDocument17 pagesInstitute of Bankers of Sri Lanka: D 07 - Investment BankingSuvindu DulhanNo ratings yet

- Complaint Against Zions BankDocument56 pagesComplaint Against Zions BankThe Salt Lake TribuneNo ratings yet

- Green River Rodmakers ETP3000 S07Document10 pagesGreen River Rodmakers ETP3000 S07Vlad George PopescuNo ratings yet

- Far410 Dec 2019Document8 pagesFar410 Dec 2019NurulHuda Auni Binti Ab RahmanNo ratings yet

- Chapter 10 Decentralization: Responsibility Accounting, Performance Evaluation, and Transfer PricingDocument70 pagesChapter 10 Decentralization: Responsibility Accounting, Performance Evaluation, and Transfer PricingEninta SebayangNo ratings yet

- ReceiptsDocument9 pagesReceiptsinfoNo ratings yet

- Collateral Allocation MechanismsDocument3 pagesCollateral Allocation MechanismsaNo ratings yet

- Actuarial MathematicsDocument32 pagesActuarial MathematicsAhsan HabibNo ratings yet

- Working CapitalDocument9 pagesWorking CapitalLakshya AgrawalNo ratings yet

- Analysis Kisumu-County 2023 FinalDocument20 pagesAnalysis Kisumu-County 2023 FinaluongozifreshNo ratings yet

- B Com Hons Sem 2 EditedDocument22 pagesB Com Hons Sem 2 EditedShikha GoyalNo ratings yet

- Midterm Assignment 6: Frando, Maria Teresa S. OL33E63Document3 pagesMidterm Assignment 6: Frando, Maria Teresa S. OL33E63Maria Teresa Frando CahandingNo ratings yet

- Draft AtapDocument9 pagesDraft AtapMuhd ArifNo ratings yet

- Project Report On: Submitted byDocument47 pagesProject Report On: Submitted byManoj ParabNo ratings yet

- Aber Report 2020 - en - 4Document92 pagesAber Report 2020 - en - 4ForkLogNo ratings yet

- Capital BudgetingDocument12 pagesCapital BudgetingKhadar50% (4)

- Fundamentals of Computer Problem Solving: Assignment 3Document7 pagesFundamentals of Computer Problem Solving: Assignment 3Nor Syahirah Mohd NorNo ratings yet

- Definition of Capital AllowancesDocument9 pagesDefinition of Capital AllowancesAdesolaNo ratings yet

- Foreign Capital and Economic Growth of IndiaDocument23 pagesForeign Capital and Economic Growth of IndiaMitesh ShahNo ratings yet

- India - MS Economics Aug 2022Document11 pagesIndia - MS Economics Aug 2022Salim MiyaNo ratings yet

- BOP Category Guide PDFDocument29 pagesBOP Category Guide PDFsimbamikeNo ratings yet

- A Project Report HDFC BANKDocument48 pagesA Project Report HDFC BANKVikas SinghNo ratings yet

- Draft Requirements For Tax Declaration TranferDocument4 pagesDraft Requirements For Tax Declaration TranfercarmanvernonNo ratings yet