Download as pdf or txt

You might also like

- Discussion 1 Second Sem .PDF-1Document11 pagesDiscussion 1 Second Sem .PDF-1Io Aya100% (2)

- Practical Accounting P-2Document7 pagesPractical Accounting P-2KingChryshAnneNo ratings yet

- Cash FlowDocument6 pagesCash FlowKailaNo ratings yet

- Accounting For Business CombinationsDocument19 pagesAccounting For Business Combinationsvinanovia50% (2)

- 19 Ifric-12Document9 pages19 Ifric-12DM BuenconsejoNo ratings yet

- Review Test FarDocument10 pagesReview Test FarEli PinesNo ratings yet

- MAC 102 201905 Foundations of Accounting II.Document6 pagesMAC 102 201905 Foundations of Accounting II.Angellah Batiraishe MoyoNo ratings yet

- Business Combination - SubsequentDocument2 pagesBusiness Combination - SubsequentMaan CabolesNo ratings yet

- MSC F&A AFG 09101 Supplementary Examination 2023Document9 pagesMSC F&A AFG 09101 Supplementary Examination 2023Sebastian MlingwaNo ratings yet

- Cash Flow AnalysisDocument4 pagesCash Flow AnalysisMargin Pason RanjoNo ratings yet

- Assignment 1Document7 pagesAssignment 1Dat DoanNo ratings yet

- Business Combination Accounted For Under The Equity MethodDocument4 pagesBusiness Combination Accounted For Under The Equity MethodMixx MineNo ratings yet

- Review Problems AnswersDocument4 pagesReview Problems AnswersFranchette Yvonne JulianNo ratings yet

- Comprehensive Illustration of Consolidated Financial Statements - Intercompany Sale of Inventories PDFDocument9 pagesComprehensive Illustration of Consolidated Financial Statements - Intercompany Sale of Inventories PDFamie honnagNo ratings yet

- Discussion 1 Second Sem PDFDocument11 pagesDiscussion 1 Second Sem PDFRNo ratings yet

- Quiz Chapter 17Document1 pageQuiz Chapter 17Zaira UdtohanNo ratings yet

- Chapter 46 Cash Flow ComprehensiveDocument8 pagesChapter 46 Cash Flow ComprehensiveCheesca Macabanti - 12 Euclid-Digital ModularNo ratings yet

- Accounting Assignment (100) : A. B. C. The Journal EntryDocument2 pagesAccounting Assignment (100) : A. B. C. The Journal EntryFaiaz ShahreearNo ratings yet

- Sample Questions and Solutions - Final ExamDocument4 pagesSample Questions and Solutions - Final ExamNadjah JNo ratings yet

- Bac 203 Cat 2Document3 pagesBac 203 Cat 2Brian MutuaNo ratings yet

- C 1Document10 pagesC 1biniamNo ratings yet

- Assignment 2Document7 pagesAssignment 2Dat DoanNo ratings yet

- Handout Fin Man 2302Document2 pagesHandout Fin Man 2302Ranz Nikko N PaetNo ratings yet

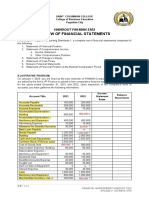

- Far01 - The Financial Statements PresentationDocument10 pagesFar01 - The Financial Statements PresentationRNo ratings yet

- Cash ExampleDocument1 pageCash ExampleFRANCIS IAN ALBARACIN IINo ratings yet

- Ias 1 - Questions..Document8 pagesIas 1 - Questions..Timothy KawumaNo ratings yet

- Project Two. Process Financial Transactions and Prepare Financial The Accounts in The Ledger ofDocument11 pagesProject Two. Process Financial Transactions and Prepare Financial The Accounts in The Ledger ofGetahunNo ratings yet

- Advac2 MidtermDocument5 pagesAdvac2 MidtermgeminailnaNo ratings yet

- FFS - NumericalsDocument5 pagesFFS - NumericalsFunny ManNo ratings yet

- Adv AssignmentDocument3 pagesAdv AssignmentBromanineNo ratings yet

- Buscom SeatworkDocument3 pagesBuscom SeatworkTintin AquinoNo ratings yet

- Ac6 ProblemsDocument21 pagesAc6 ProblemsLysss EpssssNo ratings yet

- Topic 2 - Af09101 - Financial StatementsDocument42 pagesTopic 2 - Af09101 - Financial Statementsarusha afroNo ratings yet

- Cfas ActivitiesDocument10 pagesCfas ActivitiesAntonNo ratings yet

- Chapter 1 11 IA3Document10 pagesChapter 1 11 IA3ZicoNo ratings yet

- Accounting Fundamentals PracticeDocument9 pagesAccounting Fundamentals PracticealitohdezsalNo ratings yet

- SFP and SCF - Practice QuestionsDocument3 pagesSFP and SCF - Practice QuestionsFazelah YakubNo ratings yet

- Template - MIDTERM EXAM INTERMEDIATE 1Document7 pagesTemplate - MIDTERM EXAM INTERMEDIATE 1Rani RahayuNo ratings yet

- FINANCIAL RATIOS: (Compute For Year 2020 Only, Answers Must Be Rounded Off in Two Decimal Places) (5 Points)Document2 pagesFINANCIAL RATIOS: (Compute For Year 2020 Only, Answers Must Be Rounded Off in Two Decimal Places) (5 Points)ISABELA QUITCONo ratings yet

- Bus Com Handout 1 Bus CombinationDocument9 pagesBus Com Handout 1 Bus CombinationChristine RepuldaNo ratings yet

- Partnership Formation Problem No. 1Document8 pagesPartnership Formation Problem No. 1tide podsNo ratings yet

- Financial Accounting Q&aDocument4 pagesFinancial Accounting Q&aGlen JavellanaNo ratings yet

- AFAR001 PartnershipDocument11 pagesAFAR001 PartnershipLen Charisse Sioco100% (1)

- Ak 01Document5 pagesAk 01djawapinNo ratings yet

- Assignment 3Document7 pagesAssignment 3Dat DoanNo ratings yet

- Accounting Fundamentals Practice-ASH - IVADocument12 pagesAccounting Fundamentals Practice-ASH - IVAalitohdezsalNo ratings yet

- Acc8fsconso Sdoa2019Document5 pagesAcc8fsconso Sdoa2019Sharmaine Clemencio0No ratings yet

- Training Program: Subject:: Final ProjectDocument7 pagesTraining Program: Subject:: Final ProjectSuraj ApexNo ratings yet

- 5.2. Unit 5 AAB AP A2 Report SunDocument5 pages5.2. Unit 5 AAB AP A2 Report SunHằng Nguyễn ThuNo ratings yet

- Corporate LiquidationDocument3 pagesCorporate LiquidationAbbey Emmanuelle ValenzuelaNo ratings yet

- 2018-06 ICMAB FL 001 PAC Year Question JUNE 2018Document4 pages2018-06 ICMAB FL 001 PAC Year Question JUNE 2018Mohammad ShahidNo ratings yet

- Quiz 2 Cashflows Final PDFDocument4 pagesQuiz 2 Cashflows Final PDFChito MirandaNo ratings yet

- Net Asset AcquisitionDocument2 pagesNet Asset AcquisitionRafael BarbinNo ratings yet

- Net Asset AcquisitionDocument2 pagesNet Asset AcquisitionRafael BarbinNo ratings yet

- Home Office, Branch Accounting & Business CombinationDocument5 pagesHome Office, Branch Accounting & Business CombinationPaupauNo ratings yet

- Act 202 - Financial Accounting QDocument3 pagesAct 202 - Financial Accounting QShebgatul MursalinNo ratings yet

- Prelim Exam Business CombinationDocument3 pagesPrelim Exam Business CombinationHyakkimura GamingNo ratings yet

- Financial Reporting Tutorial QSN Solutions 2021 JC JaftoDocument31 pagesFinancial Reporting Tutorial QSN Solutions 2021 JC JaftoInnocent GwangwaraNo ratings yet

- 17769cash Flow Practice QuestionsDocument8 pages17769cash Flow Practice QuestionsirmaNo ratings yet

- Final Individual Assignment - 4 Nov 2022Document6 pagesFinal Individual Assignment - 4 Nov 2022Vernice CuffyNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- Slide KTQT TaDocument277 pagesSlide KTQT TaMy DgNo ratings yet

- ACC0 20053 - Intermediate Accounting 1 - 2022 Final Departmental ExamDocument41 pagesACC0 20053 - Intermediate Accounting 1 - 2022 Final Departmental ExamNathalie Faye TajaNo ratings yet

- Latest Development of IFRS (and HKFRS) : Nelson Lam Nelson Lam 林智遠 林智遠Document32 pagesLatest Development of IFRS (and HKFRS) : Nelson Lam Nelson Lam 林智遠 林智遠ChanNo ratings yet

- Audit Problem Investments Part 2Document6 pagesAudit Problem Investments Part 2Rio Cyrel CelleroNo ratings yet

- BV2018 - MFRS 4Document41 pagesBV2018 - MFRS 4Tok DalangNo ratings yet

- IFRS 4 Insurance ContractsDocument5 pagesIFRS 4 Insurance Contractstikki0219No ratings yet

- Intermediate Accounting - Property Plant and EquipmentDocument55 pagesIntermediate Accounting - Property Plant and Equipment박은하No ratings yet

- Ifrs Framework PDFDocument23 pagesIfrs Framework PDFMohammad Delowar HossainNo ratings yet

- Seminar 8 - Change in Shareholding InterestDocument37 pagesSeminar 8 - Change in Shareholding InterestCeline LowNo ratings yet

- Airbus Annual ReportDocument201 pagesAirbus Annual ReportfsdfsdfsNo ratings yet

- Revision Test Paper CAP III June 2020Document233 pagesRevision Test Paper CAP III June 2020Roshan PanditNo ratings yet

- FINAL WORK Sesi 1-3Document127 pagesFINAL WORK Sesi 1-3Fanli KayoriNo ratings yet

- Business Combination - ExercisesDocument36 pagesBusiness Combination - ExercisesJessalyn CilotNo ratings yet

- Lobrigas - Week3 Ia3Document39 pagesLobrigas - Week3 Ia3Hensel SevillaNo ratings yet

- (Ust-Jpia) Quiz 1 Intermediate Accounting 2 Solution ManualDocument6 pages(Ust-Jpia) Quiz 1 Intermediate Accounting 2 Solution ManualRENZ ALFRED ASTRERONo ratings yet

- Investments TheoryDocument8 pagesInvestments TheoryralphalonzoNo ratings yet

- Impairment of Non Current Assets - Ias 36: - Impairment Is A Reduction To The Recoverable Amount of An Asset or ADocument89 pagesImpairment of Non Current Assets - Ias 36: - Impairment Is A Reduction To The Recoverable Amount of An Asset or ATram NguyenNo ratings yet

- Synthesis - IFRSDocument37 pagesSynthesis - IFRSRoseJeanAbingosaPernito0% (1)

- Quiz Discontinued OperationDocument2 pagesQuiz Discontinued OperationRose0% (1)

- FTME Key To CorrectionDocument12 pagesFTME Key To CorrectionABMAYALADANO ,ErvinNo ratings yet

- Investment in AssociateDocument33 pagesInvestment in AssociateKimivy BusaNo ratings yet

- CARO 2020 Revised From Auditing Assurance Made Easy BookDocument13 pagesCARO 2020 Revised From Auditing Assurance Made Easy Bookpavan saiNo ratings yet

- Tutorial Mfrs140 Far27Document9 pagesTutorial Mfrs140 Far27RAUDAHNo ratings yet

- Far660 - July 2020 Set 1 SolutionDocument8 pagesFar660 - July 2020 Set 1 SolutionHanis ZahiraNo ratings yet

- Unit 3: Indian Accounting Standard 113: Fair Value MeasurementDocument26 pagesUnit 3: Indian Accounting Standard 113: Fair Value MeasurementgauravNo ratings yet

- IFRS 3 SummaryDocument4 pagesIFRS 3 SummaryAshley EstrellaNo ratings yet

- Ifrs 15Document99 pagesIfrs 15Eddie MutizwaNo ratings yet