Download as pdf or txt

You might also like

- MCI Communications CorporationDocument6 pagesMCI Communications Corporationnipun9143No ratings yet

- Problem 5Document3 pagesProblem 5AyhuNo ratings yet

- Investment in Associate-HandoutDocument9 pagesInvestment in Associate-HandoutPhoeza Espinosa VillanuevaNo ratings yet

- Chapter Two Relevant Information and Decision Making: 5.1 The Role of Accounting in Special DecisionsDocument11 pagesChapter Two Relevant Information and Decision Making: 5.1 The Role of Accounting in Special DecisionsshimelisNo ratings yet

- The Application of Budgets and Budgetary Control On The Performance of Small and Medium-Sized Enterprises (Smes)Document18 pagesThe Application of Budgets and Budgetary Control On The Performance of Small and Medium-Sized Enterprises (Smes)P.S.VP JahnaviNo ratings yet

- Managerial Economics Center of Gravity: TH TH THDocument1 pageManagerial Economics Center of Gravity: TH TH THReginald ValenciaNo ratings yet

- Financial Management 1 5Document27 pagesFinancial Management 1 5imrickymaeberdinNo ratings yet

- Offer LetterDocument7 pagesOffer LetterBobby GenitaNo ratings yet

- Share Based-Appreciation Rights PDFDocument11 pagesShare Based-Appreciation Rights PDFLee andrew MurilloNo ratings yet

- Predetermined Overhead RatesDocument16 pagesPredetermined Overhead RatesjangjangNo ratings yet

- Chapter 1 FullDocument73 pagesChapter 1 FullAnjali Angel ThakurNo ratings yet

- Chapter 3Document19 pagesChapter 3Tofik SalmanNo ratings yet

- PFRS 17Document2 pagesPFRS 17Annie JuliaNo ratings yet

- 118.2 - Illustrative Example - Hedge Accounting: FV HedgeDocument2 pages118.2 - Illustrative Example - Hedge Accounting: FV HedgeStephen GarciaNo ratings yet

- Reviewer On Ch. 6 7 8 AISDocument18 pagesReviewer On Ch. 6 7 8 AISYan FranciaNo ratings yet

- Answer: 2018 Employee Benefit ExpenseDocument1 pageAnswer: 2018 Employee Benefit Expensehae1234100% (1)

- 1 ACCT 2A&B P. FormationDocument7 pages1 ACCT 2A&B P. FormationHillary Grace VeronaNo ratings yet

- Chapter 5 - Audit PlanningDocument13 pagesChapter 5 - Audit PlanningAlellie Khay JordanNo ratings yet

- Management Accounting Concepts and TechniquesDocument277 pagesManagement Accounting Concepts and TechniquesCalvince OumaNo ratings yet

- Company Profile Rustan Marketing Corporation HistoryDocument7 pagesCompany Profile Rustan Marketing Corporation HistoryAngieline Bautista ManzanalNo ratings yet

- PrintFundamentals of Outsourcing Module 2Document10 pagesPrintFundamentals of Outsourcing Module 2Cali Shandy H.No ratings yet

- Chapter Five Inventory Management - Chapter 4Document10 pagesChapter Five Inventory Management - Chapter 4eferemNo ratings yet

- Sec Code of Corporate Governance AnswerDocument3 pagesSec Code of Corporate Governance AnswerHechel DatinguinooNo ratings yet

- Multiple ChoiceDocument1 pageMultiple ChoiceGinie Lyn RosalNo ratings yet

- Segment Reporting Decentralized Operations and Responsibility Accounting SystemDocument34 pagesSegment Reporting Decentralized Operations and Responsibility Accounting SystemalliahnahNo ratings yet

- Business PolicyDocument7 pagesBusiness PolicySuzette EstiponaNo ratings yet

- N. Cruz-Course Material For Strategic Cost ManagementDocument134 pagesN. Cruz-Course Material For Strategic Cost ManagementEmmanuel VillafuerteNo ratings yet

- Where Financial Reporting Still Falls ShortDocument8 pagesWhere Financial Reporting Still Falls ShortRavikanth ReddyNo ratings yet

- MA Chapter 8Document2 pagesMA Chapter 8Sionet AlangilanNo ratings yet

- IcebreakerDocument5 pagesIcebreakerRyan MagalangNo ratings yet

- Practice Problems With Answers - Process Costing Average MethodDocument3 pagesPractice Problems With Answers - Process Costing Average MethodAndrea ValdezNo ratings yet

- Financial Forecasting SCI PDFDocument29 pagesFinancial Forecasting SCI PDFMa. Lou Erika BALITENo ratings yet

- CHAPTER 5 - Portfolio TheoryDocument58 pagesCHAPTER 5 - Portfolio TheoryKabutu ChuungaNo ratings yet

- Analysis of Investments in Associates of An SME1Document3 pagesAnalysis of Investments in Associates of An SME1Jan ryanNo ratings yet

- Chapter-Six Accounting For General, Special Revenue and Capital Project FundsDocument31 pagesChapter-Six Accounting For General, Special Revenue and Capital Project FundsMany Girma100% (1)

- FINMNN1 Chapter 4 Short Term Financial PlanningDocument16 pagesFINMNN1 Chapter 4 Short Term Financial Planningkissmoon732No ratings yet

- JOB Order CostingDocument4 pagesJOB Order CostingWag NasabiNo ratings yet

- Financial Management - Chapter 1 NotesDocument2 pagesFinancial Management - Chapter 1 Notessjshubham2No ratings yet

- 301 - SM Unit I. NotesDocument32 pages301 - SM Unit I. NotesShubham ArgadeNo ratings yet

- WaccDocument7 pagesWacccb_mahendraNo ratings yet

- Chapter 35 - Operating Segments Segment ReportingDocument4 pagesChapter 35 - Operating Segments Segment ReportingJoyce Anne GarduqueNo ratings yet

- Intermediate Accounting 2Document2 pagesIntermediate Accounting 2stephbatac241No ratings yet

- Pas 28Document6 pagesPas 28AnneNo ratings yet

- VanDerbeck14e SM Ch03Document32 pagesVanDerbeck14e SM Ch03Mahnoor MaalikNo ratings yet

- Chapter 2: Introducing Money EssayDocument1 pageChapter 2: Introducing Money EssayhsjhsNo ratings yet

- IAS 23 Borrowing CostDocument6 pagesIAS 23 Borrowing CostButt ArhamNo ratings yet

- A-Standards of Ethical Conduct For Management AccountantsDocument4 pagesA-Standards of Ethical Conduct For Management AccountantsChhun Mony RathNo ratings yet

- 1 The Basis of Strategy: StructureDocument17 pages1 The Basis of Strategy: StructureAlliah Gianne JacelaNo ratings yet

- 603 P&CM Unit 1 Performance ManagementDocument15 pages603 P&CM Unit 1 Performance ManagementFaiyaz panchbhayaNo ratings yet

- Easy Way To Remember CurrenciesDocument5 pagesEasy Way To Remember Currenciesjyottsna100% (2)

- Planning An Audit of Financial Statements8888888Document11 pagesPlanning An Audit of Financial Statements8888888sajedulNo ratings yet

- Conversion CycleDocument2 pagesConversion Cyclejoanbltzr0% (1)

- PRELEC1 Final ExamDocument4 pagesPRELEC1 Final ExamAramina Cabigting BocNo ratings yet

- MANSCI Final Exam QuestionnaireDocument10 pagesMANSCI Final Exam QuestionnaireChristine NionesNo ratings yet

- IAS 19 - Employee Benefits Supplementary NotesDocument19 pagesIAS 19 - Employee Benefits Supplementary NotesPASTORYNo ratings yet

- The Time Value of Money (True or False)Document4 pagesThe Time Value of Money (True or False)Mary DenizeNo ratings yet

- Invoice/Accounts Receivable Flow ChartDocument1 pageInvoice/Accounts Receivable Flow ChartAndy_plajuNo ratings yet

- 221 PrintDocument23 pages221 PrintChara etangNo ratings yet

- Share Based Compensation - Share Appreciation RightDocument15 pagesShare Based Compensation - Share Appreciation RightVivien Naig100% (1)

- ADV I CH 2 Edited 2022Document28 pagesADV I CH 2 Edited 2022HkNo ratings yet

- #2 Share Based Compensation PDFDocument5 pages#2 Share Based Compensation PDFjanus lopezNo ratings yet

- Chapter Two: Accounting For Share-Based CompensationDocument31 pagesChapter Two: Accounting For Share-Based CompensationtalilaNo ratings yet

- Activity Design MaramagDocument3 pagesActivity Design MaramagPhoeza Espinosa VillanuevaNo ratings yet

- Cna PS Depot 10262023Document6 pagesCna PS Depot 10262023Phoeza Espinosa VillanuevaNo ratings yet

- 1041 COC-PolicyOrientationEO138 PDFDocument1 page1041 COC-PolicyOrientationEO138 PDFPhoeza Espinosa VillanuevaNo ratings yet

- Certificate of Turn OverDocument3 pagesCertificate of Turn OverPhoeza Espinosa VillanuevaNo ratings yet

- MOA For TABLET 2023Document2 pagesMOA For TABLET 2023Phoeza Espinosa VillanuevaNo ratings yet

- CS Form No. 6, Revised 2020 (More Than 60 Days)Document1 pageCS Form No. 6, Revised 2020 (More Than 60 Days)Phoeza Espinosa VillanuevaNo ratings yet

- No Administrative Case - CertDocument1 pageNo Administrative Case - CertPhoeza Espinosa VillanuevaNo ratings yet

- Comelec CertDocument3 pagesComelec CertPhoeza Espinosa VillanuevaNo ratings yet

- Ali Sec17a 2020Document376 pagesAli Sec17a 2020Phoeza Espinosa VillanuevaNo ratings yet

- Purchase OrderDocument4 pagesPurchase OrderPhoeza Espinosa VillanuevaNo ratings yet

- DO - s2020 - 004-Mobile Load1Document2 pagesDO - s2020 - 004-Mobile Load1Phoeza Espinosa VillanuevaNo ratings yet

- Organization & Org StructureDocument16 pagesOrganization & Org StructurePhoeza Espinosa VillanuevaNo ratings yet

- AFAR Non Profit Organizations - QuestionsDocument24 pagesAFAR Non Profit Organizations - QuestionsPhoeza Espinosa VillanuevaNo ratings yet

- Pa 217 - Sani, NF - Whathow - Design Effective InterventionsDocument16 pagesPa 217 - Sani, NF - Whathow - Design Effective InterventionsPhoeza Espinosa VillanuevaNo ratings yet

- 2020 ChecklistDocument17 pages2020 ChecklistPhoeza Espinosa Villanueva100% (1)

- Excel - Professional Services Inc.: Management Firm of Professional Review and Training Center (PRTC)Document7 pagesExcel - Professional Services Inc.: Management Firm of Professional Review and Training Center (PRTC)Phoeza Espinosa VillanuevaNo ratings yet

- FAR.2847 Operating-Segments PDFDocument4 pagesFAR.2847 Operating-Segments PDFPhoeza Espinosa VillanuevaNo ratings yet

- Design of Individual PositionsDocument12 pagesDesign of Individual PositionsPhoeza Espinosa VillanuevaNo ratings yet

- Contingency Factors: Phoeza Espinosa-Villanueva PA 217 ReporterDocument13 pagesContingency Factors: Phoeza Espinosa-Villanueva PA 217 ReporterPhoeza Espinosa VillanuevaNo ratings yet

- New Format of FormsDocument21 pagesNew Format of FormsPhoeza Espinosa VillanuevaNo ratings yet

- Annex B - Omnibus Sworn StatementDocument3 pagesAnnex B - Omnibus Sworn StatementPhoeza Espinosa VillanuevaNo ratings yet

- IS Auditing Quizzer 2020 Version PDFDocument13 pagesIS Auditing Quizzer 2020 Version PDFPhoeza Espinosa VillanuevaNo ratings yet

- Kolambugan District: Public Schools Division SuperintendentDocument1 pageKolambugan District: Public Schools Division SuperintendentPhoeza Espinosa VillanuevaNo ratings yet

- Management Advisory Services Adb/Jju/Bdt MAS.2814 DIY - Activity-Based Costing System MAY 2020Document3 pagesManagement Advisory Services Adb/Jju/Bdt MAS.2814 DIY - Activity-Based Costing System MAY 2020Phoeza Espinosa VillanuevaNo ratings yet

- 2809 Process Costing PDFDocument80 pages2809 Process Costing PDFPhoeza Espinosa VillanuevaNo ratings yet

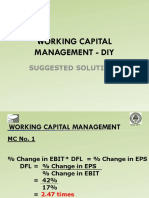

- Working Capital Management - Diy: Suggested SolutionsDocument25 pagesWorking Capital Management - Diy: Suggested SolutionsPhoeza Espinosa VillanuevaNo ratings yet

- RFBT Answer Key Drill - 2020 RDocument4 pagesRFBT Answer Key Drill - 2020 RPhoeza Espinosa VillanuevaNo ratings yet

- Quantitative Techniques in Management - Diy: Suggested SolutionsDocument32 pagesQuantitative Techniques in Management - Diy: Suggested SolutionsPhoeza Espinosa VillanuevaNo ratings yet

- 2816 Solution To Long Term Construction ContractsDocument47 pages2816 Solution To Long Term Construction ContractsPhoeza Espinosa Villanueva100% (1)

- Literature Review SalmanDocument3 pagesLiterature Review SalmanvdocxNo ratings yet

- Fin Man Dividend PolicyDocument26 pagesFin Man Dividend PolicyMarriel Fate CullanoNo ratings yet

- Concept of Capital StructureDocument22 pagesConcept of Capital StructurefatimamominNo ratings yet

- Income Statement (28.9-28.13)Document19 pagesIncome Statement (28.9-28.13)Abdul Hadi SheikhNo ratings yet

- Module 2 CVR Notes PDFDocument8 pagesModule 2 CVR Notes PDFDr. Shalini H SNo ratings yet

- 36) Audit Risks - ExamplesDocument6 pages36) Audit Risks - ExampleskasimranjhaNo ratings yet

- Business Organizations: Dennis Guardado Bmhs-3A January 5, 2021 POADocument9 pagesBusiness Organizations: Dennis Guardado Bmhs-3A January 5, 2021 POADennis GuardadoNo ratings yet

- Khadim India LTD Annual Report 2017 18 PDFDocument156 pagesKhadim India LTD Annual Report 2017 18 PDFPradeepsingh Saini0% (1)

- Accounting Is The Process of Keeping Track of A Business' FinancesDocument52 pagesAccounting Is The Process of Keeping Track of A Business' FinancesJowjie TV100% (1)

- Requirement A: Problem 4: Classroom DiscussionDocument3 pagesRequirement A: Problem 4: Classroom DiscussionZoie CorañezNo ratings yet

- FA 4 Chapter 2 - Q4Document5 pagesFA 4 Chapter 2 - Q4Vasant SriudomNo ratings yet

- Multiple Choice Questions of TYBBI Auditing (Sem 5)Document15 pagesMultiple Choice Questions of TYBBI Auditing (Sem 5)jai shree krishnaNo ratings yet

- Additional Problem Chap 3 SolutionDocument6 pagesAdditional Problem Chap 3 SolutionominNo ratings yet

- Unit 3: Indian Accounting Standard 113: Fair Value MeasurementDocument26 pagesUnit 3: Indian Accounting Standard 113: Fair Value MeasurementgauravNo ratings yet

- tb15 FINMANDocument41 pagestb15 FINMANJully GonzalesNo ratings yet

- CA Ramakrishna CVDocument2 pagesCA Ramakrishna CVCA Madhu Sudhan ReddyNo ratings yet

- CHP 13 Testbank 2Document15 pagesCHP 13 Testbank 2judyNo ratings yet

- Change in Profit-Sharing Ratio Among The Existing Partners (Reconstitution of Partnership)Document13 pagesChange in Profit-Sharing Ratio Among The Existing Partners (Reconstitution of Partnership)Yashik JindalNo ratings yet

- Multiple Choice Questions 1 BRN Corporation Has Two Divisions PDFDocument1 pageMultiple Choice Questions 1 BRN Corporation Has Two Divisions PDFLet's Talk With HassanNo ratings yet

- Ratio Analysis of HR TextilesDocument26 pagesRatio Analysis of HR TextilesOptimistic Eye100% (1)

- May 2020 - Tax Drill 2 (Individuals) - Answer KeyDocument5 pagesMay 2020 - Tax Drill 2 (Individuals) - Answer KeyROMAR A. PIGANo ratings yet

- Aber Corporation S Balance Sheet at December 31 2009 Is PresenDocument1 pageAber Corporation S Balance Sheet at December 31 2009 Is PresenM Bilal SaleemNo ratings yet

- JP摩根公司的公司估值培训资料 (英文) PDFDocument33 pagesJP摩根公司的公司估值培训资料 (英文) PDFbondbondNo ratings yet

- PROJECT (Bank Deposit)Document58 pagesPROJECT (Bank Deposit)jignas cyberNo ratings yet

- BD5 SM12Document10 pagesBD5 SM12didiajaNo ratings yet

- Samplepractice Exam 18 April 2017 Questions and AnswersDocument21 pagesSamplepractice Exam 18 April 2017 Questions and AnswersMAG MAGNo ratings yet

- DownloadDocument5 pagesDownloadabdullah bin ithninNo ratings yet

- Bharat Rasayan - Annual Report PDFDocument197 pagesBharat Rasayan - Annual Report PDFJayaprakash Gopala KamathNo ratings yet