Download as docx, pdf, or txt

You might also like

- Chapter 5 Final Income Taxation Summary BanggawanDocument8 pagesChapter 5 Final Income Taxation Summary Banggawanyours truly,100% (3)

- CH13 Balance Sheet 12.31.26Document4 pagesCH13 Balance Sheet 12.31.26Crystal TelaNo ratings yet

- Tax ReviewerDocument62 pagesTax ReviewerFelixberto Jr. BaisNo ratings yet

- Topic 5 - Final Income TaxationDocument12 pagesTopic 5 - Final Income TaxationNicol Jay Duriguez100% (3)

- E-Book - Apples and Oranges - Finance For Non-Finance in DistrubitionDocument33 pagesE-Book - Apples and Oranges - Finance For Non-Finance in DistrubitionyusufNo ratings yet

- Final TaxDocument26 pagesFinal TaxMarie MendozaNo ratings yet

- 2019 Mid-Semester Mock Exam SolutionDocument11 pages2019 Mid-Semester Mock Exam SolutionMichael BobNo ratings yet

- CHAPTER 6 Final Income Taxation (Module)Document14 pagesCHAPTER 6 Final Income Taxation (Module)Shane Mark CabiasaNo ratings yet

- UntitledDocument127 pagesUntitledemielyn lafortezaNo ratings yet

- Final Income TaxationDocument8 pagesFinal Income TaxationJade Ivy GarciaNo ratings yet

- Final Income Taxation: Lesson 5Document28 pagesFinal Income Taxation: Lesson 5lc50% (4)

- IT Module No. 5 Final Income Taxation Module Specific Learning OutcomesDocument11 pagesIT Module No. 5 Final Income Taxation Module Specific Learning Outcomesdesiree bautistaNo ratings yet

- Passive IncomeDocument31 pagesPassive IncomeE.D.J100% (1)

- Chapter 5 - Final Income Taxation Chapter Overview and ObjectivesDocument22 pagesChapter 5 - Final Income Taxation Chapter Overview and ObjectivesCindy Felipe50% (2)

- Chapter 5 Final Income TaxationDocument26 pagesChapter 5 Final Income TaxationJason MablesNo ratings yet

- Chapter 4 v4 RevisedDocument18 pagesChapter 4 v4 RevisedThe makas AbababaNo ratings yet

- Chapter 4 v4Document18 pagesChapter 4 v4Sheilamae Sernadilla GregorioNo ratings yet

- M5 - Final Income TaxationDocument31 pagesM5 - Final Income TaxationTERRIUS Ace100% (1)

- Chapter 5Document22 pagesChapter 5crackheads philippinesNo ratings yet

- Final Income TaxationDocument86 pagesFinal Income TaxationKil ZoldyckNo ratings yet

- Tax Law Summary TopicDocument3 pagesTax Law Summary Topicjuldan ordestaNo ratings yet

- Income TaxationDocument23 pagesIncome TaxationJhermaine SantiagoNo ratings yet

- Summary of Final Income TaxDocument7 pagesSummary of Final Income TaxeysiNo ratings yet

- TAXATIONDocument48 pagesTAXATIONJeffrey VergaraNo ratings yet

- Axsdaqgasdgasdg 123123 Aeasdfw SadgDocument6 pagesAxsdaqgasdgasdg 123123 Aeasdfw SadgMark LimNo ratings yet

- Taxation CH 5Document6 pagesTaxation CH 5Kristel Nuyda LobasNo ratings yet

- Pre Termination of LongDocument5 pagesPre Termination of LongBisag AsaNo ratings yet

- Final Income TaxationDocument8 pagesFinal Income TaxationAndy TolentinoNo ratings yet

- M4 P3 Inclusion Students Copy 1Document33 pagesM4 P3 Inclusion Students Copy 1Aaron BuendiaNo ratings yet

- Income Taxation ReviewerDocument27 pagesIncome Taxation Reviewerdinglasan.dymphnaNo ratings yet

- Module 05 Final Income TaxationDocument19 pagesModule 05 Final Income TaxationSly BlueNo ratings yet

- Passive Income Subject To Final TaxDocument1 pagePassive Income Subject To Final TaxdailydoseoflawNo ratings yet

- Summary of You Tube VideoDocument2 pagesSummary of You Tube VideoErylle Jeen VivasNo ratings yet

- Chapter 5 TaxDocument9 pagesChapter 5 Taxxavia9531No ratings yet

- Tax For Rental Income in The PhilippinesDocument3 pagesTax For Rental Income in The PhilippinesRESIE GALANGNo ratings yet

- Final Income TaxationDocument4 pagesFinal Income TaxationJean Diane Jovelo100% (1)

- Gross IncomeDocument32 pagesGross IncomeMariaCarlaMañagoNo ratings yet

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Document33 pagesReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB CloydNo ratings yet

- Items of Gross Income: Mutually Exclusive CoverageDocument23 pagesItems of Gross Income: Mutually Exclusive CoverageW-304-Bautista,PreciousNo ratings yet

- Income Tax Part IIIDocument6 pagesIncome Tax Part IIImary jhoyNo ratings yet

- Revenue Regs 10-98Document4 pagesRevenue Regs 10-98John Michael VidaNo ratings yet

- Chapter 5 - Final Income Taxation PDFDocument39 pagesChapter 5 - Final Income Taxation PDFgeraldine biasong100% (1)

- Taxation of Passive Income: PublicDocument23 pagesTaxation of Passive Income: PublicSeokjin KimNo ratings yet

- Income Tax Table - NIRCDocument6 pagesIncome Tax Table - NIRCgoateneo1bigfightNo ratings yet

- EXERCISESDocument25 pagesEXERCISESGandaNo ratings yet

- Foreign Tax CreditDocument2 pagesForeign Tax CreditSophiaFrancescaEspinosaNo ratings yet

- Chapter 5 - Final Income TaxationDocument13 pagesChapter 5 - Final Income TaxationBisag AsaNo ratings yet

- Week 4 Course Material For Income TaxationDocument12 pagesWeek 4 Course Material For Income TaxationAshly MateoNo ratings yet

- tAX LESSON B .Document10 pagestAX LESSON B .intramuramazingNo ratings yet

- Income Taxation Finals Quiz 2Document7 pagesIncome Taxation Finals Quiz 2Jericho DupayaNo ratings yet

- Classification of Individual Taxpayers:: Income Tax RatesDocument21 pagesClassification of Individual Taxpayers:: Income Tax RatesAngelica E. RefuerzoNo ratings yet

- 3 Income Tax ConceptsDocument37 pages3 Income Tax ConceptsRommel Espinocilla Jr.No ratings yet

- Income Tax 1. Definition, Nature, and General Principles A. Criteria in Imposing Philippine Income TaxDocument36 pagesIncome Tax 1. Definition, Nature, and General Principles A. Criteria in Imposing Philippine Income TaxPascua PeejayNo ratings yet

- Quiz 1Document8 pagesQuiz 1Kurt dela TorreNo ratings yet

- Chapter 2.1 - Income Subject To Final TaxDocument30 pagesChapter 2.1 - Income Subject To Final Taxjudel ArielNo ratings yet

- 02 Corporate Income TaxDocument10 pages02 Corporate Income TaxbajujuNo ratings yet

- Taxation of CorporationsDocument26 pagesTaxation of CorporationsjolinaNo ratings yet

- CHAPTER 13 - SummarizeDocument13 pagesCHAPTER 13 - SummarizejsgiganteNo ratings yet

- TAXNDocument22 pagesTAXNMonica MonicaNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesFrom EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNo ratings yet

- 02 Conceptual Framework - RevisedDocument13 pages02 Conceptual Framework - RevisedPanda CocoNo ratings yet

- Far 1abDocument242 pagesFar 1abPanda CocoNo ratings yet

- Tax 06 Capital Gains Taxation Part 4Document7 pagesTax 06 Capital Gains Taxation Part 4Panda CocoNo ratings yet

- Final Taxes RatesDocument2 pagesFinal Taxes RatesPanda CocoNo ratings yet

- Fee ChallanDocument1 pageFee ChallanM abubakar AbubakarNo ratings yet

- P1 QuizzerDocument26 pagesP1 QuizzerLorena Joy AggabaoNo ratings yet

- TheEconomist 2023 04 08Document338 pagesTheEconomist 2023 04 08xuanzhou willNo ratings yet

- Fsa AnswersDocument22 pagesFsa AnswersManan GuptaNo ratings yet

- The NUS MBA Brochure WebDocument20 pagesThe NUS MBA Brochure WebPrateek BaranwalNo ratings yet

- Bizmanualz CFO Policies and Procedures Series SampleDocument15 pagesBizmanualz CFO Policies and Procedures Series SampleSam Sep A SixtyoneNo ratings yet

- Beerbal & Co Profile PDFDocument14 pagesBeerbal & Co Profile PDFIrshad murtazaNo ratings yet

- Development Macroeconomics (Princeton University Press)Document452 pagesDevelopment Macroeconomics (Princeton University Press)sanjana972No ratings yet

- Family Constitution and Family by LawsDocument12 pagesFamily Constitution and Family by LawsMike Kuria MuchokiNo ratings yet

- Management of Liquidity and Liquid Assets in SmallDocument20 pagesManagement of Liquidity and Liquid Assets in SmallBachisse Mohamed AmineNo ratings yet

- Valuation FormDocument2 pagesValuation Formrushikes80No ratings yet

- Module 1 & 2 Accounting For Special TransactionsDocument19 pagesModule 1 & 2 Accounting For Special TransactionsLian MaragayNo ratings yet

- Quotations-82 - Strip Seal Expansion Joint 900meters - ChennaiDocument2 pagesQuotations-82 - Strip Seal Expansion Joint 900meters - ChennaismithNo ratings yet

- Actividad Eje 4 Negocios Internacionales FinalDocument22 pagesActividad Eje 4 Negocios Internacionales FinalahilarionNo ratings yet

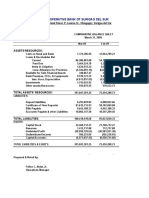

- Cooperative Bank of Surigao Del SurDocument4 pagesCooperative Bank of Surigao Del SurAnonymous iScW9lNo ratings yet

- Report Sime DarbyDocument6 pagesReport Sime DarbyNor Azura0% (1)

- Paper - 8A: Financial Management and Economics For Finance Part A: Financial Management Questions Ratio AnalysisDocument33 pagesPaper - 8A: Financial Management and Economics For Finance Part A: Financial Management Questions Ratio Analysisrohith shivakumarNo ratings yet

- Fundamentals of Islamic FinanceDocument65 pagesFundamentals of Islamic FinanceZafar IqbalNo ratings yet

- Group Assignment - Group 2Document48 pagesGroup Assignment - Group 2Đình MinhNo ratings yet

- Practice Quiz 02 ACTG240 Q2202021Document9 pagesPractice Quiz 02 ACTG240 Q2202021Minh DeanNo ratings yet

- MBA 631rift Valley OutlineDocument4 pagesMBA 631rift Valley OutlineTatekia DanielNo ratings yet

- Standardisation and AdaptationDocument39 pagesStandardisation and AdaptationHalyna NguyenNo ratings yet

- EmptyDocument2 pagesEmptyPranav ChaudhariNo ratings yet

- RCC Road New EmpanelDocument22 pagesRCC Road New Empanelketan dhameliyaNo ratings yet

- Sec 4 BooklistDocument4 pagesSec 4 BooklistcephavNo ratings yet

- Chua v. Metrobank, G.R. No. 182311, August 19, 2009Document15 pagesChua v. Metrobank, G.R. No. 182311, August 19, 2009Alan Vincent FontanosaNo ratings yet

- Swiggy Order 46542631331Document2 pagesSwiggy Order 46542631331Ajinkya PanchbudheNo ratings yet