Download as docx, pdf, or txt

You might also like

- Wal-Mart Statement of Earnings and Deductions.: 702 S.W. 8th St.,Bentonville, Arkansas 72716Document1 pageWal-Mart Statement of Earnings and Deductions.: 702 S.W. 8th St.,Bentonville, Arkansas 72716osce1349No ratings yet

- (Chapter 1) Sol Man Intermediate Accounting 2 by Zeus MillanDocument8 pages(Chapter 1) Sol Man Intermediate Accounting 2 by Zeus MillanJonathan Villazon Rosales67% (3)

- Admissionado - 50 MBA Essays That WorkedDocument86 pagesAdmissionado - 50 MBA Essays That Workedbossvigor100% (3)

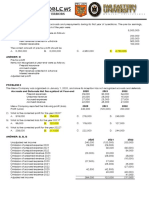

- Chapter 2-Statement of Financial Position: Problem 2-1 (AICPA Adapted)Document27 pagesChapter 2-Statement of Financial Position: Problem 2-1 (AICPA Adapted)Asi Cas Jav100% (1)

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Digital Printing and Desktop Publishing Project ReportDocument61 pagesDigital Printing and Desktop Publishing Project ReportGanesh Babu60% (10)

- FIN 320 Project Two Financial FormulasDocument19 pagesFIN 320 Project Two Financial FormulasLyca MaeNo ratings yet

- Mergent Online As Reported - Tesla IncDocument2 pagesMergent Online As Reported - Tesla IncLyca MaeNo ratings yet

- Sol. Man. - Chapter 1 Current LiabilitiesDocument10 pagesSol. Man. - Chapter 1 Current LiabilitiesChristine Mae Fernandez Mata100% (4)

- Intermediate Accounting 2 Millan 221013 124345Document233 pagesIntermediate Accounting 2 Millan 221013 124345Krazy Butterfly100% (1)

- INTERMEDIATE ACCOUNTING 2 VALIX (Solution Manual)Document210 pagesINTERMEDIATE ACCOUNTING 2 VALIX (Solution Manual)Shairine Aquino100% (2)

- CH 8 LiabilitiesDocument10 pagesCH 8 LiabilitiesKrizia Oliva100% (1)

- Partnership Agency TrustDocument58 pagesPartnership Agency TrustThea Baltazar100% (6)

- UCC IRS Form For Discharge of Estate Tax Liens f4422Document3 pagesUCC IRS Form For Discharge of Estate Tax Liens f4422Anonymous 23VuLx100% (26)

- FIRST PB FAR Solutions PDFDocument6 pagesFIRST PB FAR Solutions PDFStephanie Joy NogollosNo ratings yet

- Cpa Review School of The Philippines Mani LaDocument6 pagesCpa Review School of The Philippines Mani LaSophia PerezNo ratings yet

- FAR Problem Quiz 1 SolDocument3 pagesFAR Problem Quiz 1 SolEdnalyn CruzNo ratings yet

- FAR Final Preboard SolutionsDocument6 pagesFAR Final Preboard SolutionsVillanueva, Mariella De VeraNo ratings yet

- Module 1 - Seatwork Answer KeyDocument3 pagesModule 1 - Seatwork Answer KeyKATHRYN CLAUDETTE RESENTENo ratings yet

- BAFACR16 01 Problem IllustrationsDocument2 pagesBAFACR16 01 Problem Illustrationsmisssunshine112No ratings yet

- Accounting For Special Transactions and Business CombinationsDocument3 pagesAccounting For Special Transactions and Business CombinationsJustine Reine CornicoNo ratings yet

- Batch 95 FAR First Preboard SolutionDocument7 pagesBatch 95 FAR First Preboard Solutionssslll2No ratings yet

- Batch 93 FAR First Preboard February 2023 - SolutionDocument5 pagesBatch 93 FAR First Preboard February 2023 - SolutionlorenzNo ratings yet

- 95 AFAR Final Preboard SolutionsDocument10 pages95 AFAR Final Preboard Solutions20100723No ratings yet

- Solutions Test BankDocument26 pagesSolutions Test Bankshanaya valezaNo ratings yet

- AFA IIP.L III SolutionJune 2016Document4 pagesAFA IIP.L III SolutionJune 2016HossainNo ratings yet

- The Hong Kong Polytechnic University Hong Kong Community CollegeDocument6 pagesThe Hong Kong Polytechnic University Hong Kong Community CollegeFung Yat Kit KeithNo ratings yet

- CPAR B94 FAR Final PB Exam - Answers - SolutionsDocument8 pagesCPAR B94 FAR Final PB Exam - Answers - SolutionsJazehl ValdezNo ratings yet

- CPAR B94 TAX Final PB Exam - Answers - SolutionsDocument12 pagesCPAR B94 TAX Final PB Exam - Answers - SolutionsSilver LilyNo ratings yet

- Ia Forcadela Part IIIDocument5 pagesIa Forcadela Part IIIMary Joanne forcadelaNo ratings yet

- Solution: - A) Gross Profit Net Sales-Cost of Sales 3,000,000-2,000,000Document4 pagesSolution: - A) Gross Profit Net Sales-Cost of Sales 3,000,000-2,000,000Eyasu DestaNo ratings yet

- Basic Accounting Midterm ExamDocument11 pagesBasic Accounting Midterm ExamC J A SNo ratings yet

- Cash Basis To Accrual AccountingDocument8 pagesCash Basis To Accrual Accountingcortezzz100% (2)

- IA Chapter-4-7Document11 pagesIA Chapter-4-7Christine Joyce EnriquezNo ratings yet

- CH 2 Answers PDFDocument5 pagesCH 2 Answers PDFLian Blakely CousinNo ratings yet

- FAR First Preboard Batch 89 SolutionDocument6 pagesFAR First Preboard Batch 89 SolutionZiee00No ratings yet

- Activities On Module 1 - Partnership AccountingDocument4 pagesActivities On Module 1 - Partnership AccountingANDI TE'A MARI SIMBALANo ratings yet

- Liabilities 31.3.20X1 Rs 31.3.20X2 Rs Assets: Course: Fac Quiz:5 Section B DATE: 02/09/2019Document3 pagesLiabilities 31.3.20X1 Rs 31.3.20X2 Rs Assets: Course: Fac Quiz:5 Section B DATE: 02/09/2019Amit GodaraNo ratings yet

- Auditing Problems: Ap - 01: Correction of ErrorsDocument15 pagesAuditing Problems: Ap - 01: Correction of ErrorsPrinces100% (2)

- FPQ1 - Answer KeyDocument6 pagesFPQ1 - Answer KeyJi YuNo ratings yet

- Answers - Chapter 1 - Current LiabilitiesDocument5 pagesAnswers - Chapter 1 - Current LiabilitiesLhica EsterasNo ratings yet

- Sol. Man. - Chapter 4 - Accounts Receivable - Ia Part 1aDocument19 pagesSol. Man. - Chapter 4 - Accounts Receivable - Ia Part 1aMiguel AmihanNo ratings yet

- Sol. Man. - Chapter 6 - Teacher's Manual - Ia Part 1aDocument7 pagesSol. Man. - Chapter 6 - Teacher's Manual - Ia Part 1aYamateNo ratings yet

- Chapter 1 Current LiabilitiesDocument7 pagesChapter 1 Current LiabilitiesThalia Rhine AberteNo ratings yet

- Teacher's Manual - Financial Acctg 2Document233 pagesTeacher's Manual - Financial Acctg 2Adrian Mallari71% (21)

- Chapter 4 Receivables and Related RevenuesDocument12 pagesChapter 4 Receivables and Related Revenuesjohn condesNo ratings yet

- Solution Manual-Module 1: Acc 311 - Acctg For Special Transactions and Business CombinationsDocument11 pagesSolution Manual-Module 1: Acc 311 - Acctg For Special Transactions and Business CombinationsJoy SantosNo ratings yet

- Review of The Accounting Process Problems 2-1. (Tiger Company)Document5 pagesReview of The Accounting Process Problems 2-1. (Tiger Company)Pauline Kisha CastroNo ratings yet

- Sol. Man. - Chapter 12 - Partnership OperationsDocument11 pagesSol. Man. - Chapter 12 - Partnership OperationspehikNo ratings yet

- Teacher's Manual - Chapter 22 Current LiabilitiesDocument8 pagesTeacher's Manual - Chapter 22 Current LiabilitiesErwin Dave M. DahaoNo ratings yet

- Ia2 Ka & SolDocument31 pagesIa2 Ka & SolCarlah Jeane BasinaNo ratings yet

- Sol. Man. - Chapter 6 - Receivables Addtl Concept - Ia Part 1aDocument7 pagesSol. Man. - Chapter 6 - Receivables Addtl Concept - Ia Part 1aJenny Joy Alcantara0% (1)

- Notes To AccountsDocument2 pagesNotes To Accountsnahangar113No ratings yet

- Quiz 2 - Income Tax Concepts and ComplianceDocument3 pagesQuiz 2 - Income Tax Concepts and Compliancelc100% (1)

- Fundamentals of Corporate Finance 6th Edition Christensen Solutions ManualDocument6 pagesFundamentals of Corporate Finance 6th Edition Christensen Solutions ManualJamesOrtegapfcs100% (65)

- Quiz 1.01 Financial Statements To Interim ReportingDocument22 pagesQuiz 1.01 Financial Statements To Interim ReportingJohn Lexter MacalberNo ratings yet

- Schedule 3Document8 pagesSchedule 3Hilary GaureaNo ratings yet

- Intac QuizDocument4 pagesIntac QuizPamela Joy AlvarezNo ratings yet

- Ratio Analysis ActivityDocument3 pagesRatio Analysis ActivityKarlla ManalastasNo ratings yet

- Accounting For Special Transaction - MAYO1Document15 pagesAccounting For Special Transaction - MAYO1Geraldine MayoNo ratings yet

- Aud315 - Quizzes Solution PaperDocument6 pagesAud315 - Quizzes Solution PaperLorraineMartinNo ratings yet

- Activity 4-IntAcc1Document2 pagesActivity 4-IntAcc10322-1975No ratings yet

- PROBLEM 1. (Current and Non-Current Liabilities) : To Record The Purchase of Knives As PremiumsDocument2 pagesPROBLEM 1. (Current and Non-Current Liabilities) : To Record The Purchase of Knives As PremiumsDanica RamosNo ratings yet

- Chapter 10 - Cash To Accrual Basis of AccountingDocument3 pagesChapter 10 - Cash To Accrual Basis of AccountingJEFFERSON CUTENo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Attachment 2Document14 pagesAttachment 2Lyca MaeNo ratings yet

- Answer 3Document21 pagesAnswer 3Lyca MaeNo ratings yet

- MerchandisingDocument11 pagesMerchandisingLyca MaeNo ratings yet

- Mergent Online Officers - Tesla IncDocument1 pageMergent Online Officers - Tesla IncLyca MaeNo ratings yet

- FIN 320 Project Two Business Options ListDocument1 pageFIN 320 Project Two Business Options ListLyca MaeNo ratings yet

- Strategic Business Analysis TopicsDocument3 pagesStrategic Business Analysis TopicsLyca MaeNo ratings yet

- Marasigan WorksheetDocument15 pagesMarasigan WorksheetLyca MaeNo ratings yet

- Audit of Liabilities (Diagnostic Exam)Document4 pagesAudit of Liabilities (Diagnostic Exam)Lyca MaeNo ratings yet

- Worksheet AssignmentDocument2 pagesWorksheet AssignmentLyca MaeNo ratings yet

- Undergraduate Discussion Rubric - BUS-307-R4751 Business Law II 23EW4Document3 pagesUndergraduate Discussion Rubric - BUS-307-R4751 Business Law II 23EW4Lyca MaeNo ratings yet

- Worksheet MerchandisingDocument3 pagesWorksheet MerchandisingLyca MaeNo ratings yet

- 2-1 Discussion LiabilityDocument2 pages2-1 Discussion LiabilityLyca MaeNo ratings yet

- Quiz 2 PrE3Document13 pagesQuiz 2 PrE3Lyca MaeNo ratings yet

- Audit Procedures For LiabilitiesDocument2 pagesAudit Procedures For LiabilitiesLyca MaeNo ratings yet

- PrE3 Final ExamDocument16 pagesPrE3 Final ExamLyca MaeNo ratings yet

- Audit of Liabilities Q&ADocument3 pagesAudit of Liabilities Q&ALyca MaeNo ratings yet

- Practice Test 1Document5 pagesPractice Test 1Lyca MaeNo ratings yet

- Estimating Capital RequirementDocument7 pagesEstimating Capital RequirementVishwo ShresthaNo ratings yet

- Report On Business February 2010Document14 pagesReport On Business February 2010investingthesisNo ratings yet

- Taxation of Foreign Nationals - Money ControlDocument1 pageTaxation of Foreign Nationals - Money ControlSankaram KasturiNo ratings yet

- Ibpsgraminbank 2012Document170 pagesIbpsgraminbank 2012Vishal KumarNo ratings yet

- Transfer of SharesDocument4 pagesTransfer of Shareskjvbhkxcj100% (1)

- CIR V Cebu Portland CementDocument6 pagesCIR V Cebu Portland CementAnonymous mv3Y0KgNo ratings yet

- Consolidation Subsequent To Acquisition Date: AFM491 Advanced Financial AccountingDocument46 pagesConsolidation Subsequent To Acquisition Date: AFM491 Advanced Financial AccountingIzzy BNo ratings yet

- Lesson7 - Earnings - SF PDF Cms PDFDocument2 pagesLesson7 - Earnings - SF PDF Cms PDFWkbwNo ratings yet

- Book Keeping and Accounts Model Answer Series 3 2014Document13 pagesBook Keeping and Accounts Model Answer Series 3 2014cheah_chinNo ratings yet

- Chapter 6 - Revenue Recognition IssuesDocument3 pagesChapter 6 - Revenue Recognition Issuessablu khanNo ratings yet

- Chapter 6 - Teacher's Manual - Ifa Part 1aDocument12 pagesChapter 6 - Teacher's Manual - Ifa Part 1aCharmae Agan CaroroNo ratings yet

- Liabilities and EquityDocument23 pagesLiabilities and Equityadmiral spongebobNo ratings yet

- Jurnal Umum: PT Chandra IT CunsultanDocument10 pagesJurnal Umum: PT Chandra IT CunsultanRajin NugasNo ratings yet

- Nº de Nota SAP 458543: Número Versión Respons. Status Tratamiento Status Implement. Idioma TXT - Breve ComponenteDocument4 pagesNº de Nota SAP 458543: Número Versión Respons. Status Tratamiento Status Implement. Idioma TXT - Breve ComponenteAngélica NúñezNo ratings yet

- 2014 - Quiz 3Document12 pages2014 - Quiz 3rohitmahato10No ratings yet

- Elasticity: Chapter in A NutshellDocument17 pagesElasticity: Chapter in A NutshellSeng TheamNo ratings yet

- Balbes, Bella Ronah P. Act183: Income Taxation Prelim Exam S.Y 2020-2021 True or FalseDocument9 pagesBalbes, Bella Ronah P. Act183: Income Taxation Prelim Exam S.Y 2020-2021 True or FalseBella RonahNo ratings yet

- Components of A Sound Credit Risk Management ProgramDocument8 pagesComponents of A Sound Credit Risk Management ProgramArslan AshfaqNo ratings yet

- School of Advanced Studies: Principles and Processes For Enterprise DevelopmentDocument70 pagesSchool of Advanced Studies: Principles and Processes For Enterprise DevelopmentRaymond Wagas GamboaNo ratings yet

- Coal India LimitedDocument14 pagesCoal India LimitedSarju MaviNo ratings yet

- 15 1312MH CH09 PDFDocument17 pages15 1312MH CH09 PDFAntora HoqueNo ratings yet

- Comparative Study of Financial Statement Reports of Canara Bank and Comparative BankDocument41 pagesComparative Study of Financial Statement Reports of Canara Bank and Comparative Bankparamjeet kourNo ratings yet

- AFAR - Corp LiqDocument1 pageAFAR - Corp LiqJoanna Rose Deciar0% (1)

- 2014 P T DDocument39 pages2014 P T DShehzad Haider100% (1)

- SRO GUIDE 2010-2011: Advalorem Rate / Rate of ExemptionDocument93 pagesSRO GUIDE 2010-2011: Advalorem Rate / Rate of ExemptionmnasirmehmoodNo ratings yet