Download as pdf or txt

You might also like

- Performance Evaluation Parameters For Projects and Non-ProfitsDocument58 pagesPerformance Evaluation Parameters For Projects and Non-ProfitsAnjali Angel Thakur93% (14)

- CashPro Global Payments STP Guide - Mexico V6.1 June 2021Document39 pagesCashPro Global Payments STP Guide - Mexico V6.1 June 2021Peter SimplonNo ratings yet

- Project Execution and ControlDocument0 pagesProject Execution and ControlMahnooranjumNo ratings yet

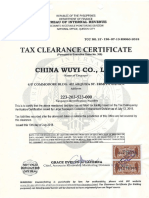

- Tax ClearanceDocument1 pageTax ClearanceliuNo ratings yet

- Lecture 4Document70 pagesLecture 4Tadesse MegersaNo ratings yet

- Shadab Ali Gadahi - F16Pg37 - Group-Ii Submit To: Engr. Abdul Qadir ShaikhDocument8 pagesShadab Ali Gadahi - F16Pg37 - Group-Ii Submit To: Engr. Abdul Qadir ShaikhMahtab SajnaniNo ratings yet

- Chapter 4 Project Monitoring and ImplementationDocument55 pagesChapter 4 Project Monitoring and Implementationmddev87No ratings yet

- Presentation 7Document9 pagesPresentation 7Amrit SapkotaNo ratings yet

- PM 6Document33 pagesPM 6Ahmed SaeedNo ratings yet

- Project Management (Project Control Concept)Document31 pagesProject Management (Project Control Concept)joseph100% (1)

- Unit 4Document36 pagesUnit 4153-B RAKSHITHANo ratings yet

- Project Monitoring and Control Process 10 Key ActivitiesDocument57 pagesProject Monitoring and Control Process 10 Key ActivitiesM ShahidNo ratings yet

- Unit Five: Managing Project Change and A Model For Project ControlDocument21 pagesUnit Five: Managing Project Change and A Model For Project ControlDiriba MokononNo ratings yet

- 3rd Reporter PROJECT EVALUATION AND CONTROLDocument14 pages3rd Reporter PROJECT EVALUATION AND CONTROLDaisy Madera ArguellesNo ratings yet

- PMP Notes From Andy CroweDocument21 pagesPMP Notes From Andy CroweRobincrusoe100% (4)

- Project ControlDocument13 pagesProject ControlsibtikhokharNo ratings yet

- Project Execution Monitoring and Control (Mouse)Document13 pagesProject Execution Monitoring and Control (Mouse)Cassandri LabuschagneNo ratings yet

- Project Monitoring and ControlDocument10 pagesProject Monitoring and ControlDangi DilleeRamNo ratings yet

- Wa0007.Document11 pagesWa0007.butolashreya35No ratings yet

- SPM Unit-4 Part-1Document54 pagesSPM Unit-4 Part-1abhioptimus00No ratings yet

- Project Monitoring and Control 5.2Document30 pagesProject Monitoring and Control 5.2Dangi DilleeRamNo ratings yet

- Project Management FinalDocument7 pagesProject Management FinalAbrar AlharmiNo ratings yet

- Project Management C17Document2 pagesProject Management C17CristianaGonçalvesNo ratings yet

- Project Management Case StudyDocument40 pagesProject Management Case Studyvasudev_ny100% (5)

- BSBPMG512 FabioFranco Q3Document1 pageBSBPMG512 FabioFranco Q3EjNo ratings yet

- SPM Unit4Document48 pagesSPM Unit4Kostubh MaheshwariNo ratings yet

- Project Monitoring and Control Expediting PDFDocument5 pagesProject Monitoring and Control Expediting PDFRebecca MariamNo ratings yet

- PM Unit 5Document27 pagesPM Unit 5Hardik KhandharNo ratings yet

- Project Implementation and ManagementDocument19 pagesProject Implementation and Managementjoy dungonNo ratings yet

- Proj Implementation - ControllingDocument72 pagesProj Implementation - ControllingBhawesh SthaNo ratings yet

- Software Project Management Processes and Life Cycle: Lecture Notes 4Document34 pagesSoftware Project Management Processes and Life Cycle: Lecture Notes 4Ali OmarNo ratings yet

- Module 4 - Planning For ImplementationDocument14 pagesModule 4 - Planning For ImplementationAnthonyNo ratings yet

- Project ControlDocument23 pagesProject ControlSanduni jayarathneNo ratings yet

- Project Control and EvaluationDocument14 pagesProject Control and Evaluationcy lifeNo ratings yet

- Project Management Presentation Software EngineeringDocument17 pagesProject Management Presentation Software EngineeringShaheer100% (2)

- Chap05 - Project Monitoring and ControlDocument22 pagesChap05 - Project Monitoring and ControlS Varun SubramanyamNo ratings yet

- Monitoring and Control1Document13 pagesMonitoring and Control1Raja Usama GoharNo ratings yet

- Monitoring & Controlling Processing GroupDocument8 pagesMonitoring & Controlling Processing GroupBryan NorwayneNo ratings yet

- UNIT - 4 Project ImplementationDocument9 pagesUNIT - 4 Project ImplementationYatendra SinghNo ratings yet

- Ch.4: The Project Control: - Monitoring A Project - Measuring Project Performance - CommunicatingDocument12 pagesCh.4: The Project Control: - Monitoring A Project - Measuring Project Performance - CommunicatingArslan SaleemNo ratings yet

- CH - 4 Project Implementation and ControllingDocument70 pagesCH - 4 Project Implementation and ControllingRoshan DahalNo ratings yet

- 02 Project ManagementDocument8 pages02 Project Managementcanasena072No ratings yet

- Monitoring and EvaluationDocument18 pagesMonitoring and EvaluationKipyegon ErickNo ratings yet

- Manajemen Proyek Sistem Informasi (Mpsi) Knowledge Areas - Integration ManagementDocument5 pagesManajemen Proyek Sistem Informasi (Mpsi) Knowledge Areas - Integration ManagementAnisah RangkutiNo ratings yet

- 2 Monitoring and Controlling The Project Including Performance MetricsDocument53 pages2 Monitoring and Controlling The Project Including Performance Metrics20105167No ratings yet

- Lec 12Document7 pagesLec 12Ghassan TariqNo ratings yet

- Chapter Five: Project Implementation, Termination and EvaluationDocument41 pagesChapter Five: Project Implementation, Termination and EvaluationOumer ShaffiNo ratings yet

- Session 19 - MCS - Management Control Systems in Projects - Dec 2020Document13 pagesSession 19 - MCS - Management Control Systems in Projects - Dec 2020kirsurkulkarniNo ratings yet

- FFFFFFFFFDocument22 pagesFFFFFFFFFShahab SadqpurNo ratings yet

- Project Management Leadership EntrepreneurshipDocument15 pagesProject Management Leadership EntrepreneurshipJane GarciaNo ratings yet

- Unit IV FinalDocument43 pagesUnit IV FinalMahima 2001No ratings yet

- J-Control Elements: BackgroundDocument9 pagesJ-Control Elements: BackgroundMohamed H. JiffryNo ratings yet

- Chapter ThreeDocument30 pagesChapter ThreeAlfiya DemozeNo ratings yet

- Performance Evaluation Parameters For Projects and Non ProfitsDocument58 pagesPerformance Evaluation Parameters For Projects and Non ProfitsadhikaNo ratings yet

- Q-4 What Are The Various Steps in Project Monitoring andDocument3 pagesQ-4 What Are The Various Steps in Project Monitoring andbhavin1234567No ratings yet

- 11 Unnamed 21 03 2024Document15 pages11 Unnamed 21 03 2024Anitej SoodNo ratings yet

- Dàn Ý Quá Trình PMDocument19 pagesDàn Ý Quá Trình PMHuycs 1111No ratings yet

- Project Life CycleDocument22 pagesProject Life CycleDev GamerNo ratings yet

- 13 Project Evaluation and ControlDocument5 pages13 Project Evaluation and ControlDaisy Madera ArguellesNo ratings yet

- CH 2 - Part 2Document61 pagesCH 2 - Part 2solomon takeleNo ratings yet

- 308 Class5Document71 pages308 Class5Bokul HossainNo ratings yet

- Exchange Rate MovementsDocument4 pagesExchange Rate MovementsBokul HossainNo ratings yet

- 308 Class3Document23 pages308 Class3Bokul HossainNo ratings yet

- 308 Class4Document55 pages308 Class4Bokul HossainNo ratings yet

- 13 Project Quality ManagementDocument54 pages13 Project Quality ManagementBokul HossainNo ratings yet

- 308 Class1Document21 pages308 Class1Bokul HossainNo ratings yet

- 308 Class6Document28 pages308 Class6Bokul HossainNo ratings yet

- 06 Project SchedulingDocument75 pages06 Project SchedulingBokul HossainNo ratings yet

- 12 Project Cost ManagementDocument54 pages12 Project Cost ManagementBokul HossainNo ratings yet

- 08 Project CrashingDocument16 pages08 Project CrashingBokul HossainNo ratings yet

- 11 EvaDocument31 pages11 EvaBokul HossainNo ratings yet

- Lec6 V1Document35 pagesLec6 V1Bokul HossainNo ratings yet

- Lec2&3 XDocument47 pagesLec2&3 XBokul HossainNo ratings yet

- 07 Project PERTDocument37 pages07 Project PERTBokul HossainNo ratings yet

- Ciadmin,+Journal+Manager,+2354 9421 1 CEDocument10 pagesCiadmin,+Journal+Manager,+2354 9421 1 CEBokul HossainNo ratings yet

- LEC5Document20 pagesLEC5Bokul HossainNo ratings yet

- QuestionnaireDocument3 pagesQuestionnaireBokul HossainNo ratings yet

- LEC4Document21 pagesLEC4Bokul HossainNo ratings yet

- LEC1 XDocument19 pagesLEC1 XBokul HossainNo ratings yet

- 505 AllDocument509 pages505 AllBokul HossainNo ratings yet

- BATBC Stock Analysis ReportDocument86 pagesBATBC Stock Analysis ReportBokul Hossain0% (1)

- AYAN2Document3 pagesAYAN2Mr. SufiNo ratings yet

- Stats 242: Algorithmic Trading and Quantitative Strategies Summer 2011Document9 pagesStats 242: Algorithmic Trading and Quantitative Strategies Summer 2011Veeken ChaglassianNo ratings yet

- E1.17 Exponential Growth - Decay 2AB Topic Booklet 1,2Document7 pagesE1.17 Exponential Growth - Decay 2AB Topic Booklet 1,2Jimei TanNo ratings yet

- OISD-129 GAP AnalysisDocument1 pageOISD-129 GAP AnalysisNayan AhmedNo ratings yet

- 146-Article Text-959-2-10-20230221Document12 pages146-Article Text-959-2-10-20230221unangsutisna195No ratings yet

- DR - 011123 - Project Fujimaki - EDKDocument2 pagesDR - 011123 - Project Fujimaki - EDKMuhammad RozaqNo ratings yet

- Penawaran Dalam Bahasa InggrisDocument1 pagePenawaran Dalam Bahasa InggrisSyarifudin50% (4)

- Drawings For Rack 20 X VM 2-2140Document2 pagesDrawings For Rack 20 X VM 2-2140Nguyễn Anh DanhNo ratings yet

- INDIAN Partnership DeedDocument2 pagesINDIAN Partnership DeedCA Vaibhav Maheshwari88% (17)

- Travel Invoice Pre VisitDocument2 pagesTravel Invoice Pre VisitNAVAL BIN YOUSAFNo ratings yet

- Microeconomics 8th Edition Perloff Solutions ManualDocument24 pagesMicroeconomics 8th Edition Perloff Solutions ManualTannerPatricksgbd97% (38)

- Rational Choice Theory EssayDocument2 pagesRational Choice Theory EssayDerek BannisterNo ratings yet

- PindyckPPT-Ch.18 Full Externalities SlideDocument45 pagesPindyckPPT-Ch.18 Full Externalities SlideTashianna ColeyNo ratings yet

- Free Wifi LokacijeDocument75 pagesFree Wifi LokacijeTanja MadicNo ratings yet

- Chiesa, Paolo_ Lozza, Giovanni - [ASME ASME 1998 International Gas Turbine and Aeroengine Congress and Exhibition - Stockholm, Sweden (Tuesday 2 June 1998)] Vol (1998, American Society of Mechanical Engineers) [10.1115_98-Gt-38 - Libgen.liDocument8 pagesChiesa, Paolo_ Lozza, Giovanni - [ASME ASME 1998 International Gas Turbine and Aeroengine Congress and Exhibition - Stockholm, Sweden (Tuesday 2 June 1998)] Vol (1998, American Society of Mechanical Engineers) [10.1115_98-Gt-38 - Libgen.liDS ManojNo ratings yet

- Space Planning - Office DesignDocument63 pagesSpace Planning - Office DesignAYESHA SAEED100% (1)

- Value Chart For YES Prosperity Edge Credit CardDocument1 pageValue Chart For YES Prosperity Edge Credit CardRajeev KumarNo ratings yet

- List of Transformers & Transmission Lines of BSPTCLDocument4 pagesList of Transformers & Transmission Lines of BSPTCLChief Engineer TransOMNo ratings yet

- Perhaps You Wondered What Ben Kinmore Who Lives Off inDocument2 pagesPerhaps You Wondered What Ben Kinmore Who Lives Off intrilocksp SinghNo ratings yet

- 3D2N Semporna MabulDocument3 pages3D2N Semporna MabulFARHAH FATIHAH BINTI AZLAN -No ratings yet

- PowerPacT P-Frame Molded Case Circuit Breakers - PKA36120Document4 pagesPowerPacT P-Frame Molded Case Circuit Breakers - PKA36120techtricNo ratings yet

- GivenDocument17 pagesGivenApurvAdarshNo ratings yet

- Short Answer Key: Problem Set 1Document3 pagesShort Answer Key: Problem Set 1Sagheer Hussain DaharNo ratings yet

- Tentative MID Term Date Shate Summer 2023Document2 pagesTentative MID Term Date Shate Summer 2023Inayat UllahNo ratings yet

- Boarding Pass (COK HYD)Document20 pagesBoarding Pass (COK HYD)Nathan ManiNo ratings yet

- Fakey Trading Strategy (Inside Bar False Break Out)Document8 pagesFakey Trading Strategy (Inside Bar False Break Out)Doug Trudell100% (1)

- Super Abrasive CatalogueDocument8 pagesSuper Abrasive CatalogueBorisNo ratings yet

- Chapter 1 Introduction To Economics BMDocument42 pagesChapter 1 Introduction To Economics BMSKYRunner 777No ratings yet

![Chiesa, Paolo_ Lozza, Giovanni - [ASME ASME 1998 International Gas Turbine and Aeroengine Congress and Exhibition - Stockholm, Sweden (Tuesday 2 June 1998)] Vol (1998, American Society of Mechanical Engineers) [10.1115_98-Gt-38 - Libgen.li](https://imgv2-2-f.scribdassets.com/img/document/605752054/149x198/cebe8cc676/1667824590?v=1)