Download as docx, pdf, or txt

You might also like

- Non-VAT Goods Chart of AccountsDocument13 pagesNon-VAT Goods Chart of AccountsJenny BernardinoNo ratings yet

- Begin Reinforcement Activity 1Document39 pagesBegin Reinforcement Activity 1Kendall Art25% (4)

- Happy Tours and Travel Agency Chart of Accounts To Balance SheetDocument11 pagesHappy Tours and Travel Agency Chart of Accounts To Balance SheetChristine Tiprado100% (3)

- Financial Statement AnalysisDocument26 pagesFinancial Statement AnalysisJade Gomez100% (2)

- Detoya Accounting CycleDocument17 pagesDetoya Accounting CycleElma Joyce Bondoc100% (5)

- Edgar Detoya Transactions ExerciseDocument23 pagesEdgar Detoya Transactions ExerciseRica Joy BejaNo ratings yet

- Assignment 4 - Financial Accounting - February 11Document4 pagesAssignment 4 - Financial Accounting - February 11Ednalyn PascualNo ratings yet

- 05 Nov 2020 - (Free) ..Cnf6v0dxaxe - Fatwa3ylew0ohqd - Bgd1ah1xdmcaegf3dxzrcafzaxnydaqiaxmbdxb2aq0dcav2cxmDocument4 pages05 Nov 2020 - (Free) ..Cnf6v0dxaxe - Fatwa3ylew0ohqd - Bgd1ah1xdmcaegf3dxzrcafzaxnydaqiaxmbdxb2aq0dcav2cxmmark AssanteNo ratings yet

- Edgar Detoya Tax Consultant (Acca101)Document56 pagesEdgar Detoya Tax Consultant (Acca101)Hannah Pearl Flores VillarNo ratings yet

- Abuegmidterm Activity 1 Edgar DetoyaDocument21 pagesAbuegmidterm Activity 1 Edgar DetoyaAnonn78% (9)

- Raftelis Report On Siemen's ContractDocument58 pagesRaftelis Report On Siemen's Contractthe kingfishNo ratings yet

- Accounting Activities - MerchandisingDocument6 pagesAccounting Activities - MerchandisingJoyNo ratings yet

- Solutions To Journal Entry Problem 2Document4 pagesSolutions To Journal Entry Problem 2Kristine BacaniNo ratings yet

- 10.29 Acctg Cycle FIRST PRELIM Answer Key BlankDocument31 pages10.29 Acctg Cycle FIRST PRELIM Answer Key BlankRhadzmae OmalNo ratings yet

- Acctg Cycle Excel Format - Answer Key Liz Cee Cleaning Service - 10.12.2021 BlankDocument33 pagesAcctg Cycle Excel Format - Answer Key Liz Cee Cleaning Service - 10.12.2021 BlankRhadzmae Omal100% (1)

- GISKA AURA GRAFINSI - 20211119164355 - ACCT6349002 - LB10 - MID - ConfDocument15 pagesGISKA AURA GRAFINSI - 20211119164355 - ACCT6349002 - LB10 - MID - Confgiska grafinsiNo ratings yet

- Edgar DetoyaDocument16 pagesEdgar DetoyaAngelica EltagonNo ratings yet

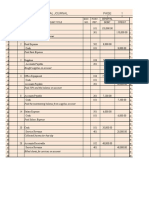

- General Journal: Page No. - 1 Description PR Date 2021 Debit CreditDocument2 pagesGeneral Journal: Page No. - 1 Description PR Date 2021 Debit CreditmeepxxxNo ratings yet

- Practice SetDocument6 pagesPractice SetShealtiel Kyze CahiligNo ratings yet

- Journal Adjusting Dan Statement Income Akuntansi Eryca Nusrat Eugenya Ramli 1231712016Document26 pagesJournal Adjusting Dan Statement Income Akuntansi Eryca Nusrat Eugenya Ramli 1231712016Eryca EugenyaNo ratings yet

- DIKO SUSUKUAN-mergedDocument11 pagesDIKO SUSUKUAN-mergedchoigyu031301No ratings yet

- Activity 3 - TolentinoDocument7 pagesActivity 3 - TolentinoDJazel TolentinoNo ratings yet

- Activity 3 - TolentinoDocument7 pagesActivity 3 - TolentinoDJazel Tolentino100% (1)

- Activity 3 - TolentinoDocument7 pagesActivity 3 - TolentinoDJazel TolentinoNo ratings yet

- NAME: Uson, Juhlia Reeiana S. DATE: April 20, 2021 GRADE AND SECTION: 9 - Holy Trinity ScoreDocument3 pagesNAME: Uson, Juhlia Reeiana S. DATE: April 20, 2021 GRADE AND SECTION: 9 - Holy Trinity ScoreJuhlia UsonNo ratings yet

- Journal EntryDocument2 pagesJournal EntryBea Dela PeniaNo ratings yet

- Fabm 21Document6 pagesFabm 21kristelNo ratings yet

- 07 Activity 1Document2 pages07 Activity 1Althea NovidaNo ratings yet

- Group 3-Adjusting Journal EntryDocument27 pagesGroup 3-Adjusting Journal EntryDanny LeonenNo ratings yet

- 06 BTLE 30043 Santos Repair Shop Complete Cycle StudentDocument29 pages06 BTLE 30043 Santos Repair Shop Complete Cycle StudentnicoleshiNo ratings yet

- Businesses in PoblacionDocument29 pagesBusinesses in PoblacionnicoleshiNo ratings yet

- Exercises I - Answer KeyDocument5 pagesExercises I - Answer KeyJowjie TV100% (1)

- Giska Aura Grafinsi - 20211119134302 - Acct6349002 - LB10 - MidDocument13 pagesGiska Aura Grafinsi - 20211119134302 - Acct6349002 - LB10 - Midgiska grafinsiNo ratings yet

- Interactive Question 4: Acquisition of A Subsidiary: Non-Current AssetsDocument4 pagesInteractive Question 4: Acquisition of A Subsidiary: Non-Current AssetsRiad FaisalNo ratings yet

- Case 4 Matapang's Repair BusinessDocument13 pagesCase 4 Matapang's Repair BusinessCobie VillenaNo ratings yet

- SEATWORK6Document6 pagesSEATWORK6dumpanonymouslyNo ratings yet

- Acctg Cycle Assign Answer KeyDocument32 pagesAcctg Cycle Assign Answer KeyAdrian Jay BeloyNo ratings yet

- Far1 Chapter 2Document63 pagesFar1 Chapter 2Erik NavarroNo ratings yet

- Perilla Geriqjoedn 1Document20 pagesPerilla Geriqjoedn 1Geriq Joeden PerillaNo ratings yet

- Question 2 of 2 - Homework - Chapter 11Document5 pagesQuestion 2 of 2 - Homework - Chapter 11Thiha MyoNo ratings yet

- Elsa Fox, Tax Consultant General Journal For The Month Ended in December 2019Document7 pagesElsa Fox, Tax Consultant General Journal For The Month Ended in December 2019Jasmine Cate JumillaNo ratings yet

- Exercise 17 SolutionDocument1 pageExercise 17 SolutionhontoskokoNo ratings yet

- ACC 01 - Recording of Transactions For Service - Journal EntriesDocument3 pagesACC 01 - Recording of Transactions For Service - Journal EntriesAlbert BugasNo ratings yet

- Buenaventuraej Bsa1bmidterm Activity 1 Edgar DetoyaDocument21 pagesBuenaventuraej Bsa1bmidterm Activity 1 Edgar DetoyaAnonnNo ratings yet

- ACTIVITY 1 ExampleDocument32 pagesACTIVITY 1 Exampleaivan john CañadillaNo ratings yet

- Wi-Tribe Pakistan Limited: Pay SlipDocument1 pageWi-Tribe Pakistan Limited: Pay Slipusman majeedNo ratings yet

- Rivera and Santos PartnershipDocument31 pagesRivera and Santos PartnershipDaneca GallardoNo ratings yet

- Lesson34 2Document10 pagesLesson34 2Sami UllahNo ratings yet

- Santos Financial StatementDocument14 pagesSantos Financial StatementJulianne Marie TolosaNo ratings yet

- Chapter 7Document9 pagesChapter 7Hezekiah Babor LopeNo ratings yet

- Assignment ACT201 SMR1Document15 pagesAssignment ACT201 SMR1Md.sabir 1831620030No ratings yet

- Ledger Posting With OE GL UTB SamplesDocument46 pagesLedger Posting With OE GL UTB SamplesZamantha OliverosNo ratings yet

- I. True or False: Pre TestDocument18 pagesI. True or False: Pre TestErina SmithNo ratings yet

- 15.3 Chapter 21 Excel HomeworkDocument6 pages15.3 Chapter 21 Excel HomeworkJuliana CaroNo ratings yet

- ACCT 100 Quiz 2 Due Date: October 11 Starting at 8:05pm Time Allowed: 1 HourDocument11 pagesACCT 100 Quiz 2 Due Date: October 11 Starting at 8:05pm Time Allowed: 1 HourAhmed SamadNo ratings yet

- Uy Balance SheetDocument8 pagesUy Balance SheetMary Louise CamposanoNo ratings yet

- Weddings R US Accounting CycleDocument9 pagesWeddings R US Accounting CycleRaisa LidasanNo ratings yet

- Repetitio Activity IIIDocument35 pagesRepetitio Activity IIIJesa TanNo ratings yet

- Projected One-Year Cash Flow Lip Redux Cash Flow Statement As of October 2020 Account Titles Debit Credit Source of FundsDocument1 pageProjected One-Year Cash Flow Lip Redux Cash Flow Statement As of October 2020 Account Titles Debit Credit Source of Fundsmjmj.lorenzo0805No ratings yet

- Grade 11 Provincial Examination Accounting P1 (English) 2020 Exemplars Question PaperDocument15 pagesGrade 11 Provincial Examination Accounting P1 (English) 2020 Exemplars Question PaperNITANo ratings yet

- Bernabe Accounting-FirmDocument33 pagesBernabe Accounting-FirmElla Ramos100% (1)

- General Journal ExcelDocument10 pagesGeneral Journal ExcelJoy Mikaela GozonNo ratings yet

- Using Economic Indicators to Improve Investment AnalysisFrom EverandUsing Economic Indicators to Improve Investment AnalysisRating: 3.5 out of 5 stars3.5/5 (1)

- Finan.2 Module-2 Assignment Lesson-2Document2 pagesFinan.2 Module-2 Assignment Lesson-2Anjelika ViescaNo ratings yet

- Of Tea and HighDocument212 pagesOf Tea and HighAnjelika ViescaNo ratings yet

- Making Your Ch.1Document22 pagesMaking Your Ch.1Anjelika ViescaNo ratings yet

- Acctg 9 Chap 3 TermsDocument9 pagesAcctg 9 Chap 3 TermsAnjelika ViescaNo ratings yet

- CHAPTER5Document8 pagesCHAPTER5Anjelika ViescaNo ratings yet

- BanksDocument5 pagesBanksAnjelika ViescaNo ratings yet

- MemoDocument1 pageMemoAnjelika ViescaNo ratings yet

- Acctg 19Document11 pagesAcctg 19Anjelika ViescaNo ratings yet

- The PDIC Is The Statutory Receiver and Liquidator of Closed BanksDocument2 pagesThe PDIC Is The Statutory Receiver and Liquidator of Closed BanksAnjelika ViescaNo ratings yet

- Application LetterDocument3 pagesApplication LetterAnjelika ViescaNo ratings yet

- Audited Financials 2022Document159 pagesAudited Financials 2022Anjelika ViescaNo ratings yet

- FS 2021Document73 pagesFS 2021Anjelika ViescaNo ratings yet

- Sun Pharma Phillipines Inc.Document42 pagesSun Pharma Phillipines Inc.Anjelika ViescaNo ratings yet

- PAGE - 14 - QuestionsDocument34 pagesPAGE - 14 - QuestionsAnjelika ViescaNo ratings yet

- APC 305 Week 5 DisbursementsDocument13 pagesAPC 305 Week 5 DisbursementsAnjelika ViescaNo ratings yet

- Financial MGT Module 2Document26 pagesFinancial MGT Module 2Anjelika ViescaNo ratings yet

- COST ACCTNG - Chapters 5-6 ActivitiesDocument30 pagesCOST ACCTNG - Chapters 5-6 ActivitiesAnjelika ViescaNo ratings yet

- Financial MGT New Module 4Document17 pagesFinancial MGT New Module 4Anjelika ViescaNo ratings yet

- Financial MGT Module 1Document24 pagesFinancial MGT Module 1Anjelika ViescaNo ratings yet

- Why Is Accounting Often Referred To As The Language of BusinessDocument15 pagesWhy Is Accounting Often Referred To As The Language of BusinessAnjelika ViescaNo ratings yet

- Acctgchap 2Document15 pagesAcctgchap 2Anjelika ViescaNo ratings yet

- Chapter 3Document14 pagesChapter 3Anjelika ViescaNo ratings yet

- Chapter 6 Gender and SocietyDocument20 pagesChapter 6 Gender and SocietyAnjelika ViescaNo ratings yet

- True or False, PG 190Document11 pagesTrue or False, PG 190Anjelika ViescaNo ratings yet

- Gec 2Document8 pagesGec 2Anjelika ViescaNo ratings yet

- Anjelika B. Viesca Bsa 1-ADocument11 pagesAnjelika B. Viesca Bsa 1-AAnjelika ViescaNo ratings yet

- Accounting For Factory OverheadDocument10 pagesAccounting For Factory OverheadAnjelika ViescaNo ratings yet

- COST ACCTNG - Chapters 7 9 ActivitiesDocument27 pagesCOST ACCTNG - Chapters 7 9 ActivitiesAnjelika ViescaNo ratings yet

- Ch05 - Basics of AnalysisDocument37 pagesCh05 - Basics of AnalysisSamar MessaoudNo ratings yet

- D4 Audit Working PaperDocument5 pagesD4 Audit Working PaperSyazliana KasimNo ratings yet

- Expenses Reimbursement Form: Details of Advance ReceivedDocument2 pagesExpenses Reimbursement Form: Details of Advance ReceivedmisbahNo ratings yet

- Solution Manual For Microeconomics 15th Canadian Edition Campbell R Mcconnell Stanley L Brue Sean Masaki Flynn Tom BarbieroDocument34 pagesSolution Manual For Microeconomics 15th Canadian Edition Campbell R Mcconnell Stanley L Brue Sean Masaki Flynn Tom Barbierowisardspoliate.ybjnr100% (51)

- Consolidated Balance Sheet of Mahindra and Mahindra - in Rs. Cr.Document10 pagesConsolidated Balance Sheet of Mahindra and Mahindra - in Rs. Cr.bhagathnagarNo ratings yet

- Chapter 6 - Joint ArrangementsDocument16 pagesChapter 6 - Joint ArrangementsChloe Oberlin0% (2)

- Hotel Expense AccountingDocument7 pagesHotel Expense AccountingPj Sorn100% (1)

- Participant's Note - Meaning and Scope of Supply and Time and Valuation of SupplyDocument20 pagesParticipant's Note - Meaning and Scope of Supply and Time and Valuation of SupplyaskNo ratings yet

- Rockwell Land CorporationDocument15 pagesRockwell Land CorporationaravillarinoNo ratings yet

- Foreign Exchange General Motors SupplDocument9 pagesForeign Exchange General Motors SupplTheresa BrownNo ratings yet

- Dog Grooming Business Plan ExampleDocument35 pagesDog Grooming Business Plan ExampleJoseph QuillNo ratings yet

- Balance Sheet AnalysisDocument25 pagesBalance Sheet Analysissinger0% (1)

- MR Lokesh Goddati Employee ID: 00146914 Unit: SBU1Document5 pagesMR Lokesh Goddati Employee ID: 00146914 Unit: SBU1satyakrishna electricalsNo ratings yet

- Gbolahan Project (EFFECT OF BUDGETING ON THE FINANCIAL PERFORMANCEDocument37 pagesGbolahan Project (EFFECT OF BUDGETING ON THE FINANCIAL PERFORMANCECrown DavidNo ratings yet

- 13 IAS 20 and IAS 23Document13 pages13 IAS 20 and IAS 23Zatsumono YamamotoNo ratings yet

- Passing Package AccDocument93 pagesPassing Package AccOM VNo ratings yet

- Kerala Account CodeDocument20 pagesKerala Account CodePradeep KumarNo ratings yet

- Minor Operating Department Medha Singh (127) Muskan AgarwalaDocument3 pagesMinor Operating Department Medha Singh (127) Muskan AgarwalaMedha SinghNo ratings yet

- BAM031 P3 Q2 CorporationsDocument26 pagesBAM031 P3 Q2 CorporationsMary Lyn DatuinNo ratings yet

- Final AccountsDocument40 pagesFinal AccountsCA Deepak Ehn100% (1)

- Assignment 2 Part B DocumentDocument13 pagesAssignment 2 Part B DocumentKojiro FuumaNo ratings yet

- Acc 101Document24 pagesAcc 101Shyam RathiNo ratings yet

- Laws Relating To Finance and Support Services of TESDA, CHED, Dep-EdDocument51 pagesLaws Relating To Finance and Support Services of TESDA, CHED, Dep-EdEron Roi Centina-gacutan100% (1)

- BSNL Financial Statement AnalysisDocument62 pagesBSNL Financial Statement AnalysisAnonymous kHs8LninS67% (3)

- Audit Manual For CoopsDocument35 pagesAudit Manual For CoopsowieNo ratings yet

- Report of Condition Total AssetsDocument8 pagesReport of Condition Total AssetsJohn Joshua S. GeronaNo ratings yet

- MOD2 Statement of Cash FlowsDocument2 pagesMOD2 Statement of Cash FlowsGemma DenolanNo ratings yet