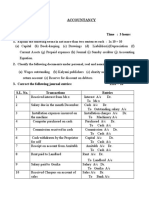

Correction of Errors

Correction of Errors

You might also like

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Fiori Apps For SAP FICO - SAP FICO Fiori Apps - SAP FICO AppsDocument65 pagesFiori Apps For SAP FICO - SAP FICO Fiori Apps - SAP FICO AppspnareshpnkNo ratings yet

- FarDocument8 pagesFarnivea gumayagay71% (7)

- Modern Trader - June 2018Document84 pagesModern Trader - June 2018amyNo ratings yet

- London Examinations GCE: Accounting (Modular Syllabus) Advanced Subsidiary/Advanced LevelDocument16 pagesLondon Examinations GCE: Accounting (Modular Syllabus) Advanced Subsidiary/Advanced Levelrahat879No ratings yet

- Accounting: Pearson Edexcel (Modular Syllabus)Document16 pagesAccounting: Pearson Edexcel (Modular Syllabus)Ammar SohailNo ratings yet

- Accounting: Pearson Edexcel (Modular Syllabus)Document16 pagesAccounting: Pearson Edexcel (Modular Syllabus)rahat879No ratings yet

- Accounting Analysis of TransactionsDocument14 pagesAccounting Analysis of TransactionscamilleNo ratings yet

- Ifa QP 1215Document12 pagesIfa QP 1215tarawallyalhaji1997No ratings yet

- Group Assignment On Fundamentals of Accounting IDocument6 pagesGroup Assignment On Fundamentals of Accounting IKaleab ShimelsNo ratings yet

- Accountancy and Auditing-2016 PDFDocument6 pagesAccountancy and Auditing-2016 PDFMian Abdullah YaseenNo ratings yet

- Accountancy I 2016 PDFDocument4 pagesAccountancy I 2016 PDFShahid RazwanNo ratings yet

- London Examinations GCE: Accounting (Modular Syllabus) Advanced Subsidiary/Advanced LevelDocument16 pagesLondon Examinations GCE: Accounting (Modular Syllabus) Advanced Subsidiary/Advanced LevelFarbeen Satira MirzaNo ratings yet

- Accountancy Auditing 2016Document7 pagesAccountancy Auditing 2016Abdul basitNo ratings yet

- December 2010 FA4QDocument6 pagesDecember 2010 FA4QkalowekamoNo ratings yet

- Book-Keeping Form Three PDFDocument4 pagesBook-Keeping Form Three PDFdesa ntosNo ratings yet

- Explain The Following Terms in Not More Than Two Sentences Each: 1x 10 10Document4 pagesExplain The Following Terms in Not More Than Two Sentences Each: 1x 10 10Anita PanigrahiNo ratings yet

- T I C A P: Foundation Examinations Spring 2008Document4 pagesT I C A P: Foundation Examinations Spring 2008adnanNo ratings yet

- Finacial Accountig1Document7 pagesFinacial Accountig1Prashanth PendyalaNo ratings yet

- L1 1introductiontofinancialaccountingDocument8 pagesL1 1introductiontofinancialaccountingLoli LalaNo ratings yet

- RTP May 16 GRP-1Document140 pagesRTP May 16 GRP-1Shakshi AgarwalNo ratings yet

- BF 120Document11 pagesBF 120Dixie Cheelo100% (1)

- ch01 PDFDocument2 pagesch01 PDFDanish BaigNo ratings yet

- Compre 3Document7 pagesCompre 3casio3627No ratings yet

- Financial AccoutningDocument7 pagesFinancial AccoutningMr Aruladithiya DevarajNo ratings yet

- Far Reviewer Comprehensive Various Problems QuestionsDocument5 pagesFar Reviewer Comprehensive Various Problems QuestionsCharles Eli AlejandroNo ratings yet

- SdsasacsacsacsacsacDocument4 pagesSdsasacsacsacsacsacIden PratamaNo ratings yet

- CFR Exam GuideDocument32 pagesCFR Exam GuideNkopane MonahengNo ratings yet

- AccountancyDocument8 pagesAccountancyAnkit KumarNo ratings yet

- Accountancy Sample PaperDocument6 pagesAccountancy Sample PaperDevansh BawejaNo ratings yet

- November 2022: Reg. No.Document7 pagesNovember 2022: Reg. No.kaurkarun7No ratings yet

- 4120504Document3 pages4120504m_gadhvi6840No ratings yet

- CHAPTER 3 Bai TapDocument19 pagesCHAPTER 3 Bai TapPhuong Anh HoangNo ratings yet

- January 31: Birendra Mahato Adjusting Entries and WorksheetDocument17 pagesJanuary 31: Birendra Mahato Adjusting Entries and WorksheetAjit UpretyNo ratings yet

- Companyfinal Accounts Including A Manufacturing AccountDocument8 pagesCompanyfinal Accounts Including A Manufacturing AccountMahmozNo ratings yet

- Chapter 6-Trial Balance and Rectification of Errors Previous QuestionsDocument12 pagesChapter 6-Trial Balance and Rectification of Errors Previous Questionscrescenthss vanimalNo ratings yet

- MA - W2019 (4519201) (GTURanker - Com)Document3 pagesMA - W2019 (4519201) (GTURanker - Com)Sourav SinhaNo ratings yet

- Past Papers For Single Entry and Incomplete RecordsDocument2 pagesPast Papers For Single Entry and Incomplete RecordsMahreena IlyasNo ratings yet

- 25 Question PaperDocument4 pages25 Question PaperPacific Tiger0% (1)

- Unit IDocument10 pagesUnit IkuselvNo ratings yet

- Assignment POSTING TO THE LEDGERDocument7 pagesAssignment POSTING TO THE LEDGERJie SapornaNo ratings yet

- ECO-2 ENG CompressedDocument4 pagesECO-2 ENG CompressedAmit AdhikariNo ratings yet

- Internal Question Bank MA 2022Document7 pagesInternal Question Bank MA 2022singhalsanchit321No ratings yet

- CE Principles of Accounts 2001 PaperDocument8 pagesCE Principles of Accounts 2001 PaperdicktkloNo ratings yet

- Final - Unit - 10 - Financial Accounting - TrangDocument5 pagesFinal - Unit - 10 - Financial Accounting - TrangKevin PhạmNo ratings yet

- © The Institute of Chartered Accountants of India: (6 X 2 12 Marks) (4 Marks)Document19 pages© The Institute of Chartered Accountants of India: (6 X 2 12 Marks) (4 Marks)Prayag TrivediNo ratings yet

- 2016-12 ICMAB FL 001 PAC Year Question December 2016Document3 pages2016-12 ICMAB FL 001 PAC Year Question December 2016Mohammad ShahidNo ratings yet

- Adjusting EntriesDocument5 pagesAdjusting EntriesM Hassan BrohiNo ratings yet

- Unadjusted Trial Balance ProblemsDocument7 pagesUnadjusted Trial Balance ProblemssheenacgacitaNo ratings yet

- Mock 1Document16 pagesMock 1kimsadiaminNo ratings yet

- AFM Q-BankDocument42 pagesAFM Q-Banks BNo ratings yet

- Section A Answer BOTH Questions in This Section. 1 Aaron and Bitan Are in Partnership, Sharing Profits and Losses EquallyDocument15 pagesSection A Answer BOTH Questions in This Section. 1 Aaron and Bitan Are in Partnership, Sharing Profits and Losses EquallySethmika DiasNo ratings yet

- WAC11 2016 May AS QPDocument15 pagesWAC11 2016 May AS QPAfrida AnanNo ratings yet

- Financial Statement Class 11Document3 pagesFinancial Statement Class 11KUNAL SHARMANo ratings yet

- Extra Exercises ErrorsDocument6 pagesExtra Exercises ErrorsMohd Rafi Jasman100% (1)

- Test 5Document4 pagesTest 5suzalaggarwalllNo ratings yet

- Costing and AccountancyDocument3 pagesCosting and AccountancyDeepakNo ratings yet

- MTP - Intermediate - Syllabus 2016 - June2020 - Set1: Paper 5-Financial AccountingDocument7 pagesMTP - Intermediate - Syllabus 2016 - June2020 - Set1: Paper 5-Financial Accountingvikash guptaNo ratings yet

- Individual Assignment.123Document5 pagesIndividual Assignment.123Tsegaye BubamoNo ratings yet

- Time Allowed: 3 Hours Max Marks: 100: Colleges 1st SimulationDocument3 pagesTime Allowed: 3 Hours Max Marks: 100: Colleges 1st SimulationKashifNo ratings yet

- FDN J22 - TS 2 - P1 Account - QueDocument5 pagesFDN J22 - TS 2 - P1 Account - QueShantanu JadhavNo ratings yet

- Bookkeeping: June 2019Document5 pagesBookkeeping: June 2019Kay100% (1)

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Unit 1 MechDocument6 pagesUnit 1 Mechsubodya alahakoonNo ratings yet

- UntitledDocument7 pagesUntitledsubodya alahakoonNo ratings yet

- Sina y I: N 1g L Range YzDocument3 pagesSina y I: N 1g L Range Yzsubodya alahakoonNo ratings yet

- ChemistryDocument3 pagesChemistrysubodya alahakoonNo ratings yet

- 4SI0 01 Que 20150515Document16 pages4SI0 01 Que 20150515subodya alahakoonNo ratings yet

- 4SI0 01 MSC 20150812Document11 pages4SI0 01 MSC 20150812subodya alahakoonNo ratings yet

- Market Failure 2020Document25 pagesMarket Failure 2020subodya alahakoonNo ratings yet

- 4MA1 1FR Rms 20180822Document19 pages4MA1 1FR Rms 20180822subodya alahakoonNo ratings yet

- 4SI0 01 Rms 20180822Document13 pages4SI0 01 Rms 20180822subodya alahakoonNo ratings yet

- Physics: Pearson Edexcel International Advanced LevelDocument20 pagesPhysics: Pearson Edexcel International Advanced Levelsubodya alahakoonNo ratings yet

- Mark Scheme (Results) : Summer 2018Document19 pagesMark Scheme (Results) : Summer 2018subodya alahakoonNo ratings yet

- Government Intervention Latest'Document12 pagesGovernment Intervention Latest'subodya alahakoonNo ratings yet

- Resolving Past Paper Questions Jan 2002 To Jan 2009Document15 pagesResolving Past Paper Questions Jan 2002 To Jan 2009subodya alahakoonNo ratings yet

- FI-SD Integration - I - SAP BlogsDocument23 pagesFI-SD Integration - I - SAP BlogsArun Varshney (MULAYAM)No ratings yet

- AP: Entering DR and CR Memos: Payables Oracle R12 Payables Supplier Balance 2 CommentsDocument3 pagesAP: Entering DR and CR Memos: Payables Oracle R12 Payables Supplier Balance 2 CommentsSaq IbNo ratings yet

- 004 Topic 4 (Set A) QDocument16 pages004 Topic 4 (Set A) Qcixiang0620No ratings yet

- Finacle-10-Menu Options PDFDocument96 pagesFinacle-10-Menu Options PDFakshay2orionNo ratings yet

- Teresita Buenaflor ShoesDocument13 pagesTeresita Buenaflor ShoesThe Phoebie JhemNo ratings yet

- ACCT505 Week 2 Quiz 1 Job Order and Process Costing SystemsDocument8 pagesACCT505 Week 2 Quiz 1 Job Order and Process Costing SystemsNatasha DeclanNo ratings yet

- Merchandising Financial StatementsDocument7 pagesMerchandising Financial Statementskochanay oya-oy100% (1)

- Proposed Chart of Accounts-8Document62 pagesProposed Chart of Accounts-8Zimbo Kigo100% (1)

- Chapter 2 The Accounting ProcessDocument12 pagesChapter 2 The Accounting ProcessFrakeZNo ratings yet

- f8 Pilot Paper IntDocument20 pagesf8 Pilot Paper IntXin LiNo ratings yet

- Intermediate Accounting Stice 19th Edition Solutions ManualDocument8 pagesIntermediate Accounting Stice 19th Edition Solutions ManualLisa Beighley100% (34)

- Accounting For Trading Business Chapter 5Document40 pagesAccounting For Trading Business Chapter 5MUHAMMAD AMMAD ARSHAD100% (1)

- 12 Accountancy Lyp 2017 Delhi Set1 PDFDocument39 pages12 Accountancy Lyp 2017 Delhi Set1 PDFAshish GangwalNo ratings yet

- KM23315567 StatementDocument9 pagesKM23315567 StatementPrashant RajNo ratings yet

- AFAR FinalMockBoard BDocument11 pagesAFAR FinalMockBoard BCattleyaNo ratings yet

- Adjusting Journal EntriesDocument11 pagesAdjusting Journal EntriesKatrina RomasantaNo ratings yet

- Ppe Depreciation and DepletionDocument21 pagesPpe Depreciation and DepletionEarl Lalaine EscolNo ratings yet

- Accounts 1 SampleDocument31 pagesAccounts 1 SampleShingirayi MazingaizoNo ratings yet

- Quiz # 2 NewsDocument20 pagesQuiz # 2 NewsSaram NadeemNo ratings yet

- The Journal: Frank Wood's Business Accounting 1, 12Document25 pagesThe Journal: Frank Wood's Business Accounting 1, 12Kofi AsaaseNo ratings yet

- BHN Ajar Samone Equipment Repair Inc - TBafte Adj - FIn StatementsDocument32 pagesBHN Ajar Samone Equipment Repair Inc - TBafte Adj - FIn StatementsKevin FernandaNo ratings yet

- Accountancy Previous QuestionsDocument4 pagesAccountancy Previous QuestionsmurthyNo ratings yet

- Turkey x0092 S Kriz-2Document11 pagesTurkey x0092 S Kriz-2Muhammad AounNo ratings yet

- Homework 2Document3 pagesHomework 2Charlie RNo ratings yet

- Write Off Policy FINALDocument5 pagesWrite Off Policy FINALHoward UntalanNo ratings yet

- Chap 4 The Recording ProcessDocument58 pagesChap 4 The Recording ProcesstamimNo ratings yet

- Cornerstones of Financial Accounting 4th Edition Rich Solutions ManualDocument25 pagesCornerstones of Financial Accounting 4th Edition Rich Solutions ManualShawnHessbody100% (60)

Download as docx, pdf, or txt

You might also like

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Fiori Apps For SAP FICO - SAP FICO Fiori Apps - SAP FICO AppsDocument65 pagesFiori Apps For SAP FICO - SAP FICO Fiori Apps - SAP FICO AppspnareshpnkNo ratings yet

- FarDocument8 pagesFarnivea gumayagay71% (7)

- Modern Trader - June 2018Document84 pagesModern Trader - June 2018amyNo ratings yet

- London Examinations GCE: Accounting (Modular Syllabus) Advanced Subsidiary/Advanced LevelDocument16 pagesLondon Examinations GCE: Accounting (Modular Syllabus) Advanced Subsidiary/Advanced Levelrahat879No ratings yet

- Accounting: Pearson Edexcel (Modular Syllabus)Document16 pagesAccounting: Pearson Edexcel (Modular Syllabus)Ammar SohailNo ratings yet

- Accounting: Pearson Edexcel (Modular Syllabus)Document16 pagesAccounting: Pearson Edexcel (Modular Syllabus)rahat879No ratings yet

- Accounting Analysis of TransactionsDocument14 pagesAccounting Analysis of TransactionscamilleNo ratings yet

- Ifa QP 1215Document12 pagesIfa QP 1215tarawallyalhaji1997No ratings yet

- Group Assignment On Fundamentals of Accounting IDocument6 pagesGroup Assignment On Fundamentals of Accounting IKaleab ShimelsNo ratings yet

- Accountancy and Auditing-2016 PDFDocument6 pagesAccountancy and Auditing-2016 PDFMian Abdullah YaseenNo ratings yet

- Accountancy I 2016 PDFDocument4 pagesAccountancy I 2016 PDFShahid RazwanNo ratings yet

- London Examinations GCE: Accounting (Modular Syllabus) Advanced Subsidiary/Advanced LevelDocument16 pagesLondon Examinations GCE: Accounting (Modular Syllabus) Advanced Subsidiary/Advanced LevelFarbeen Satira MirzaNo ratings yet

- Accountancy Auditing 2016Document7 pagesAccountancy Auditing 2016Abdul basitNo ratings yet

- December 2010 FA4QDocument6 pagesDecember 2010 FA4QkalowekamoNo ratings yet

- Book-Keeping Form Three PDFDocument4 pagesBook-Keeping Form Three PDFdesa ntosNo ratings yet

- Explain The Following Terms in Not More Than Two Sentences Each: 1x 10 10Document4 pagesExplain The Following Terms in Not More Than Two Sentences Each: 1x 10 10Anita PanigrahiNo ratings yet

- T I C A P: Foundation Examinations Spring 2008Document4 pagesT I C A P: Foundation Examinations Spring 2008adnanNo ratings yet

- Finacial Accountig1Document7 pagesFinacial Accountig1Prashanth PendyalaNo ratings yet

- L1 1introductiontofinancialaccountingDocument8 pagesL1 1introductiontofinancialaccountingLoli LalaNo ratings yet

- RTP May 16 GRP-1Document140 pagesRTP May 16 GRP-1Shakshi AgarwalNo ratings yet

- BF 120Document11 pagesBF 120Dixie Cheelo100% (1)

- ch01 PDFDocument2 pagesch01 PDFDanish BaigNo ratings yet

- Compre 3Document7 pagesCompre 3casio3627No ratings yet

- Financial AccoutningDocument7 pagesFinancial AccoutningMr Aruladithiya DevarajNo ratings yet

- Far Reviewer Comprehensive Various Problems QuestionsDocument5 pagesFar Reviewer Comprehensive Various Problems QuestionsCharles Eli AlejandroNo ratings yet

- SdsasacsacsacsacsacDocument4 pagesSdsasacsacsacsacsacIden PratamaNo ratings yet

- CFR Exam GuideDocument32 pagesCFR Exam GuideNkopane MonahengNo ratings yet

- AccountancyDocument8 pagesAccountancyAnkit KumarNo ratings yet

- Accountancy Sample PaperDocument6 pagesAccountancy Sample PaperDevansh BawejaNo ratings yet

- November 2022: Reg. No.Document7 pagesNovember 2022: Reg. No.kaurkarun7No ratings yet

- 4120504Document3 pages4120504m_gadhvi6840No ratings yet

- CHAPTER 3 Bai TapDocument19 pagesCHAPTER 3 Bai TapPhuong Anh HoangNo ratings yet

- January 31: Birendra Mahato Adjusting Entries and WorksheetDocument17 pagesJanuary 31: Birendra Mahato Adjusting Entries and WorksheetAjit UpretyNo ratings yet

- Companyfinal Accounts Including A Manufacturing AccountDocument8 pagesCompanyfinal Accounts Including A Manufacturing AccountMahmozNo ratings yet

- Chapter 6-Trial Balance and Rectification of Errors Previous QuestionsDocument12 pagesChapter 6-Trial Balance and Rectification of Errors Previous Questionscrescenthss vanimalNo ratings yet

- MA - W2019 (4519201) (GTURanker - Com)Document3 pagesMA - W2019 (4519201) (GTURanker - Com)Sourav SinhaNo ratings yet

- Past Papers For Single Entry and Incomplete RecordsDocument2 pagesPast Papers For Single Entry and Incomplete RecordsMahreena IlyasNo ratings yet

- 25 Question PaperDocument4 pages25 Question PaperPacific Tiger0% (1)

- Unit IDocument10 pagesUnit IkuselvNo ratings yet

- Assignment POSTING TO THE LEDGERDocument7 pagesAssignment POSTING TO THE LEDGERJie SapornaNo ratings yet

- ECO-2 ENG CompressedDocument4 pagesECO-2 ENG CompressedAmit AdhikariNo ratings yet

- Internal Question Bank MA 2022Document7 pagesInternal Question Bank MA 2022singhalsanchit321No ratings yet

- CE Principles of Accounts 2001 PaperDocument8 pagesCE Principles of Accounts 2001 PaperdicktkloNo ratings yet

- Final - Unit - 10 - Financial Accounting - TrangDocument5 pagesFinal - Unit - 10 - Financial Accounting - TrangKevin PhạmNo ratings yet

- © The Institute of Chartered Accountants of India: (6 X 2 12 Marks) (4 Marks)Document19 pages© The Institute of Chartered Accountants of India: (6 X 2 12 Marks) (4 Marks)Prayag TrivediNo ratings yet

- 2016-12 ICMAB FL 001 PAC Year Question December 2016Document3 pages2016-12 ICMAB FL 001 PAC Year Question December 2016Mohammad ShahidNo ratings yet

- Adjusting EntriesDocument5 pagesAdjusting EntriesM Hassan BrohiNo ratings yet

- Unadjusted Trial Balance ProblemsDocument7 pagesUnadjusted Trial Balance ProblemssheenacgacitaNo ratings yet

- Mock 1Document16 pagesMock 1kimsadiaminNo ratings yet

- AFM Q-BankDocument42 pagesAFM Q-Banks BNo ratings yet

- Section A Answer BOTH Questions in This Section. 1 Aaron and Bitan Are in Partnership, Sharing Profits and Losses EquallyDocument15 pagesSection A Answer BOTH Questions in This Section. 1 Aaron and Bitan Are in Partnership, Sharing Profits and Losses EquallySethmika DiasNo ratings yet

- WAC11 2016 May AS QPDocument15 pagesWAC11 2016 May AS QPAfrida AnanNo ratings yet

- Financial Statement Class 11Document3 pagesFinancial Statement Class 11KUNAL SHARMANo ratings yet

- Extra Exercises ErrorsDocument6 pagesExtra Exercises ErrorsMohd Rafi Jasman100% (1)

- Test 5Document4 pagesTest 5suzalaggarwalllNo ratings yet

- Costing and AccountancyDocument3 pagesCosting and AccountancyDeepakNo ratings yet

- MTP - Intermediate - Syllabus 2016 - June2020 - Set1: Paper 5-Financial AccountingDocument7 pagesMTP - Intermediate - Syllabus 2016 - June2020 - Set1: Paper 5-Financial Accountingvikash guptaNo ratings yet

- Individual Assignment.123Document5 pagesIndividual Assignment.123Tsegaye BubamoNo ratings yet

- Time Allowed: 3 Hours Max Marks: 100: Colleges 1st SimulationDocument3 pagesTime Allowed: 3 Hours Max Marks: 100: Colleges 1st SimulationKashifNo ratings yet

- FDN J22 - TS 2 - P1 Account - QueDocument5 pagesFDN J22 - TS 2 - P1 Account - QueShantanu JadhavNo ratings yet

- Bookkeeping: June 2019Document5 pagesBookkeeping: June 2019Kay100% (1)

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Unit 1 MechDocument6 pagesUnit 1 Mechsubodya alahakoonNo ratings yet

- UntitledDocument7 pagesUntitledsubodya alahakoonNo ratings yet

- Sina y I: N 1g L Range YzDocument3 pagesSina y I: N 1g L Range Yzsubodya alahakoonNo ratings yet

- ChemistryDocument3 pagesChemistrysubodya alahakoonNo ratings yet

- 4SI0 01 Que 20150515Document16 pages4SI0 01 Que 20150515subodya alahakoonNo ratings yet

- 4SI0 01 MSC 20150812Document11 pages4SI0 01 MSC 20150812subodya alahakoonNo ratings yet

- Market Failure 2020Document25 pagesMarket Failure 2020subodya alahakoonNo ratings yet

- 4MA1 1FR Rms 20180822Document19 pages4MA1 1FR Rms 20180822subodya alahakoonNo ratings yet

- 4SI0 01 Rms 20180822Document13 pages4SI0 01 Rms 20180822subodya alahakoonNo ratings yet

- Physics: Pearson Edexcel International Advanced LevelDocument20 pagesPhysics: Pearson Edexcel International Advanced Levelsubodya alahakoonNo ratings yet

- Mark Scheme (Results) : Summer 2018Document19 pagesMark Scheme (Results) : Summer 2018subodya alahakoonNo ratings yet

- Government Intervention Latest'Document12 pagesGovernment Intervention Latest'subodya alahakoonNo ratings yet

- Resolving Past Paper Questions Jan 2002 To Jan 2009Document15 pagesResolving Past Paper Questions Jan 2002 To Jan 2009subodya alahakoonNo ratings yet

- FI-SD Integration - I - SAP BlogsDocument23 pagesFI-SD Integration - I - SAP BlogsArun Varshney (MULAYAM)No ratings yet

- AP: Entering DR and CR Memos: Payables Oracle R12 Payables Supplier Balance 2 CommentsDocument3 pagesAP: Entering DR and CR Memos: Payables Oracle R12 Payables Supplier Balance 2 CommentsSaq IbNo ratings yet

- 004 Topic 4 (Set A) QDocument16 pages004 Topic 4 (Set A) Qcixiang0620No ratings yet

- Finacle-10-Menu Options PDFDocument96 pagesFinacle-10-Menu Options PDFakshay2orionNo ratings yet

- Teresita Buenaflor ShoesDocument13 pagesTeresita Buenaflor ShoesThe Phoebie JhemNo ratings yet

- ACCT505 Week 2 Quiz 1 Job Order and Process Costing SystemsDocument8 pagesACCT505 Week 2 Quiz 1 Job Order and Process Costing SystemsNatasha DeclanNo ratings yet

- Merchandising Financial StatementsDocument7 pagesMerchandising Financial Statementskochanay oya-oy100% (1)

- Proposed Chart of Accounts-8Document62 pagesProposed Chart of Accounts-8Zimbo Kigo100% (1)

- Chapter 2 The Accounting ProcessDocument12 pagesChapter 2 The Accounting ProcessFrakeZNo ratings yet

- f8 Pilot Paper IntDocument20 pagesf8 Pilot Paper IntXin LiNo ratings yet

- Intermediate Accounting Stice 19th Edition Solutions ManualDocument8 pagesIntermediate Accounting Stice 19th Edition Solutions ManualLisa Beighley100% (34)

- Accounting For Trading Business Chapter 5Document40 pagesAccounting For Trading Business Chapter 5MUHAMMAD AMMAD ARSHAD100% (1)

- 12 Accountancy Lyp 2017 Delhi Set1 PDFDocument39 pages12 Accountancy Lyp 2017 Delhi Set1 PDFAshish GangwalNo ratings yet

- KM23315567 StatementDocument9 pagesKM23315567 StatementPrashant RajNo ratings yet

- AFAR FinalMockBoard BDocument11 pagesAFAR FinalMockBoard BCattleyaNo ratings yet

- Adjusting Journal EntriesDocument11 pagesAdjusting Journal EntriesKatrina RomasantaNo ratings yet

- Ppe Depreciation and DepletionDocument21 pagesPpe Depreciation and DepletionEarl Lalaine EscolNo ratings yet

- Accounts 1 SampleDocument31 pagesAccounts 1 SampleShingirayi MazingaizoNo ratings yet

- Quiz # 2 NewsDocument20 pagesQuiz # 2 NewsSaram NadeemNo ratings yet

- The Journal: Frank Wood's Business Accounting 1, 12Document25 pagesThe Journal: Frank Wood's Business Accounting 1, 12Kofi AsaaseNo ratings yet

- BHN Ajar Samone Equipment Repair Inc - TBafte Adj - FIn StatementsDocument32 pagesBHN Ajar Samone Equipment Repair Inc - TBafte Adj - FIn StatementsKevin FernandaNo ratings yet

- Accountancy Previous QuestionsDocument4 pagesAccountancy Previous QuestionsmurthyNo ratings yet

- Turkey x0092 S Kriz-2Document11 pagesTurkey x0092 S Kriz-2Muhammad AounNo ratings yet

- Homework 2Document3 pagesHomework 2Charlie RNo ratings yet

- Write Off Policy FINALDocument5 pagesWrite Off Policy FINALHoward UntalanNo ratings yet

- Chap 4 The Recording ProcessDocument58 pagesChap 4 The Recording ProcesstamimNo ratings yet

- Cornerstones of Financial Accounting 4th Edition Rich Solutions ManualDocument25 pagesCornerstones of Financial Accounting 4th Edition Rich Solutions ManualShawnHessbody100% (60)