Download as docx, pdf, or txt

You might also like

- Essentials of Internal MedicineDocument832 pagesEssentials of Internal MedicineEmanuelMC100% (77)

- Sac Training Guide 2019 Final PDFDocument49 pagesSac Training Guide 2019 Final PDFArmando Santos100% (1)

- Capital Struture Analysis Oman CompaniesDocument9 pagesCapital Struture Analysis Oman CompaniesSalman SajidNo ratings yet

- ThanatiaDocument670 pagesThanatiaJoão ClaudioNo ratings yet

- Fca B SiddharthDocument12 pagesFca B SiddharthSiddharth SangtaniNo ratings yet

- Prasad 4thsemDocument19 pagesPrasad 4thsemPrasad YaligarNo ratings yet

- 21MBA13 Accounting For Managers: Topic: Financial Analysis of Indian OilDocument29 pages21MBA13 Accounting For Managers: Topic: Financial Analysis of Indian OilNikshith HegdeNo ratings yet

- Janata Bank Id.79 & 69Document13 pagesJanata Bank Id.79 & 69mulham.bba.20210202079No ratings yet

- Assignment 2Document12 pagesAssignment 2Nimra SiddiqueNo ratings yet

- The Influence of CSR & Corporate Governance OnDocument16 pagesThe Influence of CSR & Corporate Governance OnTRIPPY入KR1No ratings yet

- SailashreeChakraborty 13600921093 FM401Document12 pagesSailashreeChakraborty 13600921093 FM401Sailashree ChakrabortyNo ratings yet

- Tata Motors AnalysisDocument9 pagesTata Motors AnalysisrastehertaNo ratings yet

- Finance TermpaperDocument12 pagesFinance Termpaper21.Tamzid TapuNo ratings yet

- Solvency Position: 1. Debt-Equity RatioDocument5 pagesSolvency Position: 1. Debt-Equity RatioShilpiNo ratings yet

- Ey Aarsrapport 2021 22 35Document1 pageEy Aarsrapport 2021 22 35Ronald RunruilNo ratings yet

- FIN701 Finance and Accounting: Action Learning Project Group-14Document13 pagesFIN701 Finance and Accounting: Action Learning Project Group-14sunny bhardwajNo ratings yet

- Ratio Analysis of Arvind LTD.: Ratios Mar 21 Mar 20 Mar 19 Mar 18 Mar 17Document10 pagesRatio Analysis of Arvind LTD.: Ratios Mar 21 Mar 20 Mar 19 Mar 18 Mar 17simranNo ratings yet

- IPDC FinanceDocument14 pagesIPDC FinanceAshraful Islam AbirNo ratings yet

- Operating Cycle: To CashDocument8 pagesOperating Cycle: To CashNoor Islam FahadNo ratings yet

- Army IbaDocument34 pagesArmy IbaZayed Islam SabitNo ratings yet

- Acme Financial ReportDocument11 pagesAcme Financial ReportGhost MailerNo ratings yet

- AccountingDocument15 pagesAccountingVishwas tomarNo ratings yet

- 5.12 CALCULATING AND INTERPRETING RISK RATIOS. Refer To The Financial Statement Data For Hasbro in Problem 4.23Document14 pages5.12 CALCULATING AND INTERPRETING RISK RATIOS. Refer To The Financial Statement Data For Hasbro in Problem 4.23Lê Thiên Giang 2KT-19No ratings yet

- Project ValuesDocument30 pagesProject ValueshariharanpNo ratings yet

- Liquidity RatiosDocument5 pagesLiquidity Ratioskashish AgarwalNo ratings yet

- Current RatioDocument1 pageCurrent RatioAsir Awsaf AliNo ratings yet

- IBF Term ReportDocument12 pagesIBF Term Reportabdulhadees48No ratings yet

- 161-11-5041 Report 1Document18 pages161-11-5041 Report 1Amir ShohelNo ratings yet

- Anandam CompanyDocument8 pagesAnandam CompanyNarinderNo ratings yet

- Financial Ratios FRA UpdatedDocument10 pagesFinancial Ratios FRA Updated367Rahul Kumar SinghNo ratings yet

- Name: Hira Saqib Rehman Submitted To: Sir Nasir Rasool Section:03 Date: 11 December 2023 Subject: Financial Statement AnalysisDocument18 pagesName: Hira Saqib Rehman Submitted To: Sir Nasir Rasool Section:03 Date: 11 December 2023 Subject: Financial Statement Analysishira saqibNo ratings yet

- Tài Chính Công TyDocument14 pagesTài Chính Công Typttd154No ratings yet

- Introduction To Financial Management: GROUP PROJECT: Ratio Analysis ofDocument34 pagesIntroduction To Financial Management: GROUP PROJECT: Ratio Analysis ofJahida Akter LovnaNo ratings yet

- Ba 2.2 OfssDocument33 pagesBa 2.2 OfssakashNo ratings yet

- Ratio Analysis: Profitability RatiosDocument5 pagesRatio Analysis: Profitability RatiosATANU ROYCHOUDHURYNo ratings yet

- Tata Motors ReportDocument5 pagesTata Motors ReportrastehertaNo ratings yet

- 16 - Manju - Infosys Technolgy Ltd.Document15 pages16 - Manju - Infosys Technolgy Ltd.rajat_singlaNo ratings yet

- Kongkaikai 10 Writing Materials#Document7 pagesKongkaikai 10 Writing Materials#abiramieNo ratings yet

- Boat FinicialDocument4 pagesBoat Finicialchirag raoNo ratings yet

- My Home-1Document14 pagesMy Home-1sampad DasNo ratings yet

- Tata Motors ReportDocument5 pagesTata Motors ReportrastehertaNo ratings yet

- Grow Well 1Document12 pagesGrow Well 1ShivamKumar DubeyNo ratings yet

- Finanlcial Statements AnalysisDocument25 pagesFinanlcial Statements AnalysisAhsaan NadeemNo ratings yet

- 135 Kunal Sem2 A Afs FinratioDocument2 pages135 Kunal Sem2 A Afs FinratioSakshi ShahNo ratings yet

- 3 CompaniesreportfinanceDocument45 pages3 CompaniesreportfinanceMarisha RizalNo ratings yet

- Page 1 of 2 Assessment of Working Capital Requirements Name: M/S S K Auto PartsDocument2 pagesPage 1 of 2 Assessment of Working Capital Requirements Name: M/S S K Auto PartsAnsari JiNo ratings yet

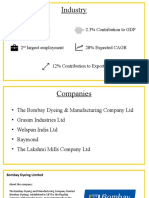

- Industry: Textile Industry 2.3% Contribution To GDPDocument16 pagesIndustry: Textile Industry 2.3% Contribution To GDPNishita VoraNo ratings yet

- Premier CementDocument13 pagesPremier CementspookywolfzNo ratings yet

- Acid Test ROA InterpretationsDocument2 pagesAcid Test ROA InterpretationsMary Mia CenizaNo ratings yet

- Internsip Presentation On Financial Performance Analysis of NCC Bank Limited A Study On Madhunaghat BranchDocument19 pagesInternsip Presentation On Financial Performance Analysis of NCC Bank Limited A Study On Madhunaghat BranchShafayet JamilNo ratings yet

- Financial and Stock MarketDocument12 pagesFinancial and Stock MarketYogyata MishraNo ratings yet

- Gas PetronasDocument33 pagesGas PetronasNour FaizahNo ratings yet

- Solvency Ratios: Name Unit 2014 2015 Maithan Alloys Anjaney Alloys Maithan AlloysDocument3 pagesSolvency Ratios: Name Unit 2014 2015 Maithan Alloys Anjaney Alloys Maithan AlloysANSHULI DMNo ratings yet

- Individual Assignment - Ratio AnalysisDocument9 pagesIndividual Assignment - Ratio Analysisyash rathodNo ratings yet

- Current RatioDocument10 pagesCurrent RatioAnugya GuptaNo ratings yet

- Financial Statement Analysis of Microsoft: Rania Elhossary Abu Dhabi University, EmailDocument19 pagesFinancial Statement Analysis of Microsoft: Rania Elhossary Abu Dhabi University, EmailvaibhavNo ratings yet

- Project FinanceDocument18 pagesProject FinanceSajid AliNo ratings yet

- Corporate Finance Corporate Finance: 2020-22 - By: Purvi Jain JSW Steel Ltd. JSW Steel LTDDocument11 pagesCorporate Finance Corporate Finance: 2020-22 - By: Purvi Jain JSW Steel Ltd. JSW Steel LTDpurvi jainNo ratings yet

- Basf RatiosDocument2 pagesBasf Ratiosprajaktashirke49No ratings yet

- Group Information: Dien Quang Lamp Joint Stock Company Công ty Cổ phần Bóng đèn Điện Quang (DQC)Document8 pagesGroup Information: Dien Quang Lamp Joint Stock Company Công ty Cổ phần Bóng đèn Điện Quang (DQC)BonBonNo ratings yet

- Fin 201 WordDocument17 pagesFin 201 Wordsayara.akhter08No ratings yet

- Asb - 212 10 140Document12 pagesAsb - 212 10 140smartasss100% (1)

- Supra AccessoryDocument7 pagesSupra AccessoryaeroglideNo ratings yet

- Crude Oil (Conversions)Document3 pagesCrude Oil (Conversions)Carolo DemoNo ratings yet

- Book Review For: One Up On Wall StreetDocument22 pagesBook Review For: One Up On Wall StreetSenthil KumarNo ratings yet

- The Duality of Human Nature in Oscar Wilde's The Importance of Being EarnestDocument28 pagesThe Duality of Human Nature in Oscar Wilde's The Importance of Being EarnestSowmya ShreeNo ratings yet

- Bishop 1997Document25 pagesBishop 1997Celina AgostinhoNo ratings yet

- DT81 Data Logger DatasheetDocument2 pagesDT81 Data Logger DatasheetDuška JarčevićNo ratings yet

- TGDocument180 pagesTGavikram1984No ratings yet

- Mock Trial Task CardsDocument8 pagesMock Trial Task CardsVitaliy Fedchenko0% (1)

- David RohlDocument3 pagesDavid RohlPhil CaudleNo ratings yet

- Characteristics of g3 - An Alternative To SF6Document5 pagesCharacteristics of g3 - An Alternative To SF6Abdul MoizNo ratings yet

- Acm 4 - B4-A1Document4 pagesAcm 4 - B4-A1Heru HaryantoNo ratings yet

- A&H Carrefour LayoutDocument1 pageA&H Carrefour LayoutAshraf EhabNo ratings yet

- IGST CH Status As On 01.01.2018Document443 pagesIGST CH Status As On 01.01.2018SK Business groupNo ratings yet

- DK Pocket Genius - HorsesDocument158 pagesDK Pocket Genius - HorsesAnamaria RaduNo ratings yet

- Fxrate 06 06 2023Document2 pagesFxrate 06 06 2023ShohanNo ratings yet

- Dictionary of Mission Theology, History, Perspectives Müller, KarlDocument552 pagesDictionary of Mission Theology, History, Perspectives Müller, KarlRev. Johana VangchhiaNo ratings yet

- Kroenke, K. Et Al (2002) The PHQ-15 - Validity of A New Measure For Evaluating The Severity of Somatic SymptomsDocument9 pagesKroenke, K. Et Al (2002) The PHQ-15 - Validity of A New Measure For Evaluating The Severity of Somatic SymptomsKristopher MacKenzie BrignardelloNo ratings yet

- ATS3445 Tutorial 1 2023Document16 pagesATS3445 Tutorial 1 2023april ngNo ratings yet

- Bombardier CRJ 00-Environmental Control SystemDocument42 pagesBombardier CRJ 00-Environmental Control SystemVincent GuignotNo ratings yet

- Top 40 C Programming Interview Questions and AnswersDocument8 pagesTop 40 C Programming Interview Questions and Answersasanga_indrajithNo ratings yet

- 4J10 CHUNG KA CHUN 4J10 - Untitled DocumentDocument1 page4J10 CHUNG KA CHUN 4J10 - Untitled Document4J10 CHUNG KA CHUN 4J10No ratings yet

- Chapter 24 Practice QuestionsDocument7 pagesChapter 24 Practice QuestionsArlene F. Montalbo100% (1)

- The Sabbath As FreedomDocument14 pagesThe Sabbath As Freedomapi-232715913No ratings yet

- Structral DatasheetDocument254 pagesStructral DatasheetdeepakNo ratings yet

- Glory To God Light From Light With LyricsDocument13 pagesGlory To God Light From Light With LyricsRodolfo DeriquitoNo ratings yet

- Mini Capstone Final Project Implementation and AssessmentDocument8 pagesMini Capstone Final Project Implementation and AssessmentSodium ChlorideNo ratings yet