Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5825)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 30-Dec-2020-Memorandum To Sebi and Justice BN AgrawalDocument17 pages30-Dec-2020-Memorandum To Sebi and Justice BN AgrawalMoneylife FoundationNo ratings yet

- Chapter 10 - Solution ManualDocument27 pagesChapter 10 - Solution Manualjuan100% (1)

- Financial Management PROBLEMS FROM UNIT - 2Document14 pagesFinancial Management PROBLEMS FROM UNIT - 2jeganrajrajNo ratings yet

- Summer Internship Project Working Capital Finance From BankDocument33 pagesSummer Internship Project Working Capital Finance From Bankpranjali shindeNo ratings yet

- NJCU - Workshop Presentation - FinalDocument19 pagesNJCU - Workshop Presentation - Finalgreergirl2No ratings yet

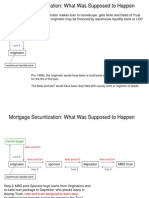

- Mortgage Securitization: What Was Supposed To HappenDocument5 pagesMortgage Securitization: What Was Supposed To Happengreergirl2No ratings yet

- NJTPC AG - Press7.25Document1 pageNJTPC AG - Press7.25greergirl2No ratings yet

- PR MortgageFraudDocument1 pagePR MortgageFraudgreergirl2No ratings yet

- NJTPC HR3808.PRDocument2 pagesNJTPC HR3808.PRgreergirl2No ratings yet

- PT Asuransi Simas Jiwa (Asj) : Press Release Kredit Rating IndonesiaDocument2 pagesPT Asuransi Simas Jiwa (Asj) : Press Release Kredit Rating IndonesiaTri Nanda Christo MarthinusNo ratings yet

- Determinants of Takaful Investment in The Northwest Region of Nigeria: A Pilot StudyDocument13 pagesDeterminants of Takaful Investment in The Northwest Region of Nigeria: A Pilot StudyAbdullahi ManirNo ratings yet

- 12 2019 AIF March 11 FINALDocument72 pages12 2019 AIF March 11 FINALSugar RayNo ratings yet

- Evaluation and Selection of Strategies Revision NotesDocument5 pagesEvaluation and Selection of Strategies Revision NotesDave Dearing100% (1)

- Jawaban Siklus Manual Ukk 2022Document7 pagesJawaban Siklus Manual Ukk 2022irma nurmayantiNo ratings yet

- Full Download Macroeconomics Policy and Practice 2nd Edition Mishkin Solutions Manual PDF Full ChapterDocument36 pagesFull Download Macroeconomics Policy and Practice 2nd Edition Mishkin Solutions Manual PDF Full Chapterythrowemisavize.blfs2100% (19)

- IAMGOLD Reports Second Quarter 2020 Results 060802020Document16 pagesIAMGOLD Reports Second Quarter 2020 Results 060802020Suriname MirrorNo ratings yet

- Debt Relief For Nicaragua: Breaking Out of The Poverty TrapDocument34 pagesDebt Relief For Nicaragua: Breaking Out of The Poverty TrapOxfamNo ratings yet

- The Future of EverythingDocument216 pagesThe Future of EverythingKanchai Keeratikamon100% (1)

- Joneja Bright Steels: The Cash Discount DecisionDocument13 pagesJoneja Bright Steels: The Cash Discount DecisionDiv_nNo ratings yet

- (Worked) (Worked) : Total 5,333.61 Total 7,427.38Document13 pages(Worked) (Worked) : Total 5,333.61 Total 7,427.38Nicole N. BeldinezaNo ratings yet

- Share Mary Ann V Domincel Chapter 5Document2 pagesShare Mary Ann V Domincel Chapter 5MA ValdezNo ratings yet

- Beverly High Hero Project Draws Nearly 400 Participants - Beverly Hills Weekly, Issue #664Document1 pageBeverly High Hero Project Draws Nearly 400 Participants - Beverly Hills Weekly, Issue #664BeverlyHillsWeeklyNo ratings yet

- 2 Semester AY 2018 - 2019 ofDocument3 pages2 Semester AY 2018 - 2019 ofVirgil Kit Augustin AbanillaNo ratings yet

- 10 Funding Options To Raise Startup Capital For BusinessDocument32 pages10 Funding Options To Raise Startup Capital For BusinessAnjani Kumar SinhaNo ratings yet

- Dpb2033 Business MathematicsDocument2 pagesDpb2033 Business MathematicsMuhdHilmanNo ratings yet

- IJIBM Vol9No4 Nov2017Document310 pagesIJIBM Vol9No4 Nov2017فوزان علیNo ratings yet

- Agriculture Advance at A Glance by RTC ChennaiDocument317 pagesAgriculture Advance at A Glance by RTC ChennaiMehul ChakrabartyNo ratings yet

- What Is A Bank Identification Number (BIN), and HDocument1 pageWhat Is A Bank Identification Number (BIN), and HYogeshwaran.sNo ratings yet

- Tax QuizDocument2 pagesTax QuizMJ ArazasNo ratings yet

- AA Product Design: Temenos Education CentreDocument52 pagesAA Product Design: Temenos Education CentreRaghavendra RaoNo ratings yet

- CFAS - Final Exam ADocument11 pagesCFAS - Final Exam AKristine Esplana ToraldeNo ratings yet

- The Last Chronicles of Planet Earth July 11 2010 Edition by Frank Dimora 3Document291 pagesThe Last Chronicles of Planet Earth July 11 2010 Edition by Frank Dimora 3ticklemeNo ratings yet

- Interest RateDocument32 pagesInterest RateMayur N Malviya85% (13)

- Ironridge Hits Back at SEC Action - Growth Capital Investor - 07/21/2015Document2 pagesIronridge Hits Back at SEC Action - Growth Capital Investor - 07/21/2015Ironridge Global PartnersNo ratings yet