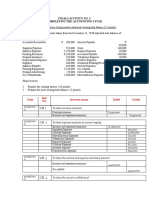

ACC111 Week-8-9 ULOb

ACC111 Week-8-9 ULOb

You might also like

- An Introduction To Scholarship Building AcademicDocument3 pagesAn Introduction To Scholarship Building AcademicNina Rosalee21% (29)

- Solution Manual For Theory and Design For Mechanical Measurements 6th Edition Richard S Figliola Donald e BeasleyDocument20 pagesSolution Manual For Theory and Design For Mechanical Measurements 6th Edition Richard S Figliola Donald e BeasleyLoriWilliamsonoqabx98% (46)

- Accounting For Managers (Assignment One (E-Finance) ) Question OneDocument7 pagesAccounting For Managers (Assignment One (E-Finance) ) Question OnehananNo ratings yet

- A Holistic Approach in Understanding The SelfDocument7 pagesA Holistic Approach in Understanding The Selflhyn JasarenoNo ratings yet

- Assignment 4 - Financial Accounting - February 11Document4 pagesAssignment 4 - Financial Accounting - February 11Ednalyn PascualNo ratings yet

- Nerissa Mae L. Santos Activity On Completing The Accounting Cycle 1Document3 pagesNerissa Mae L. Santos Activity On Completing The Accounting Cycle 1Mica Mae Correa100% (1)

- Module 4 - Problem 5Document1 pageModule 4 - Problem 5Lycksele RodulfaNo ratings yet

- Well Security When Openfile Operator: This Data Is Sourced From Peps and Updated MonthlyDocument245 pagesWell Security When Openfile Operator: This Data Is Sourced From Peps and Updated Monthlyrahul2904No ratings yet

- ACC111 Week-8-9 ULOa 2Document14 pagesACC111 Week-8-9 ULOa 2lhyn JasarenoNo ratings yet

- Finals Activity No .2 Completing THE Accounting Cycle: Palad, Nica C. Mr. Alfred BautistaDocument6 pagesFinals Activity No .2 Completing THE Accounting Cycle: Palad, Nica C. Mr. Alfred BautistaMica Mae CorreaNo ratings yet

- Cash Receipt and Disbursement ProgramDocument1 pageCash Receipt and Disbursement ProgramNicah AcojonNo ratings yet

- TAXN 1016 FE - Long ProblemsDocument11 pagesTAXN 1016 FE - Long ProblemsCrystel Kate MananganNo ratings yet

- Exercise 5 - Completing The Accounting Cycle For Merchandising and Service BusinessDocument4 pagesExercise 5 - Completing The Accounting Cycle For Merchandising and Service BusinessShiela Rengel0% (2)

- AE21 Lesson 6: Review of The Accounting Cycle: Worksheet and Adjusting EntriesDocument6 pagesAE21 Lesson 6: Review of The Accounting Cycle: Worksheet and Adjusting EntriesGlenda LinatocNo ratings yet

- Sample Problem For Last MeetingDocument11 pagesSample Problem For Last MeetingLylanie Alcoran AnibNo ratings yet

- 04 Prelim ExaminationDocument2 pages04 Prelim ExaminationJomarie BenedictoNo ratings yet

- MOJAKOE AK1 UTS 2012 GasalDocument15 pagesMOJAKOE AK1 UTS 2012 GasalVincenttio le CloudNo ratings yet

- Course Book Chapter 10Document28 pagesCourse Book Chapter 10Amirul Hakim Nor AzmanNo ratings yet

- Problem 3 ACCA101Document3 pagesProblem 3 ACCA101Nicole FidelsonNo ratings yet

- Acc 111 - Week 1-3 UloeDocument5 pagesAcc 111 - Week 1-3 UloeJaisa Mae RosalesNo ratings yet

- Comprehensive Problem: Flashback Activity 4Document1 pageComprehensive Problem: Flashback Activity 4James SyNo ratings yet

- 04 Handout 1Document6 pages04 Handout 1Nhov CabralNo ratings yet

- FS - LandscapeDocument9 pagesFS - LandscapeMekay OcasionesNo ratings yet

- Bai Tap - IAS 12 - Tu LuanDocument14 pagesBai Tap - IAS 12 - Tu LuanTrần Nguyễn Tuệ MinhNo ratings yet

- Exercises On Implementation of DCF ApproachDocument10 pagesExercises On Implementation of DCF ApproachVincenzoPizzulliNo ratings yet

- Activity - Preparation of Financial StatementsDocument4 pagesActivity - Preparation of Financial StatementsJoy ValenciaNo ratings yet

- Corporate Taxes Part 1 (VAT, EWT and Income Tax) CaseDocument4 pagesCorporate Taxes Part 1 (VAT, EWT and Income Tax) CaseMikaela L. RoqueNo ratings yet

- Midterms Problem SolvingDocument3 pagesMidterms Problem SolvingTRINA ARUTANo ratings yet

- Midterm Examination For AC11N: ProblemDocument1 pageMidterm Examination For AC11N: ProblemLeica JaymeNo ratings yet

- Tagala Aec 217 Week 4 ActivityDocument2 pagesTagala Aec 217 Week 4 ActivityDrewGuanzonGoboyTagalaNo ratings yet

- Group Assignment On Fundamentals of Accounting IDocument6 pagesGroup Assignment On Fundamentals of Accounting IKaleab ShimelsNo ratings yet

- Jawaban No 3 A Dan BDocument6 pagesJawaban No 3 A Dan BAndi Rahmat HidayatNo ratings yet

- Acct1101 Final Examination SEMESTER 2, 2020Document13 pagesAcct1101 Final Examination SEMESTER 2, 2020Yahya ZafarNo ratings yet

- Barangay Buenasuerte Notes To Financial StatementsDocument5 pagesBarangay Buenasuerte Notes To Financial StatementsRose Macoy CastilloNo ratings yet

- Elimination RoundDocument11 pagesElimination RoundDeeNo ratings yet

- Complete Cycle Servicing Graded ActivityDocument2 pagesComplete Cycle Servicing Graded ActivityErfel Al KitmaNo ratings yet

- Adjusting EntriesDocument5 pagesAdjusting EntriesM Hassan BrohiNo ratings yet

- Chapter 14Document6 pagesChapter 14Mychie Lynne MayugaNo ratings yet

- ACCA101 Leah May SantiagoDocument9 pagesACCA101 Leah May SantiagoNicole FidelsonNo ratings yet

- 06 Task Performance 1 ARGDocument4 pages06 Task Performance 1 ARGshiplusNo ratings yet

- Toaz - Info Prelim Midterm PRDocument98 pagesToaz - Info Prelim Midterm PRClandestine SoulNo ratings yet

- Practical Case Financial BudgetDocument17 pagesPractical Case Financial BudgetScribdTranslationsNo ratings yet

- QuizDocument2 pagesQuizaprilbetito02No ratings yet

- Junior Philippine Institute of AccountantsDocument10 pagesJunior Philippine Institute of AccountantsJuan paoloNo ratings yet

- Adjusting EntryDocument13 pagesAdjusting Entrymichaella maglinteNo ratings yet

- Fabm2 Learning-Activity-2Document5 pagesFabm2 Learning-Activity-2Cha Eun WooNo ratings yet

- WorksheetDocument10 pagesWorksheetScribdTranslationsNo ratings yet

- BINI General Merchandise Answer Key 2Document19 pagesBINI General Merchandise Answer Key 2workwithericajaneNo ratings yet

- INCOTAXDocument4 pagesINCOTAXnicole bancoroNo ratings yet

- Cap II Group I RTP Dec2023Document84 pagesCap II Group I RTP Dec2023pratyushmudbhari340No ratings yet

- Activity 01 PDFDocument5 pagesActivity 01 PDFJennifer AdvientoNo ratings yet

- No.2 FA Assignment 3 Amato FIXDocument3 pagesNo.2 FA Assignment 3 Amato FIXKevin DeswandaNo ratings yet

- AnsweredASS16 AccountingDocument6 pagesAnsweredASS16 Accountingvomawew647No ratings yet

- 3 Exam Part IDocument6 pages3 Exam Part IRJ DAVE DURUHANo ratings yet

- Quiz 2 Cashflows Final PDFDocument4 pagesQuiz 2 Cashflows Final PDFChito MirandaNo ratings yet

- Financial Statements PreparationDocument6 pagesFinancial Statements Preparationana lopezNo ratings yet

- Ias 07Document72 pagesIas 07Hannan Fatima EllahiNo ratings yet

- 2019-06 ICMAB FL 001 PAC Year Question JUNE 2019Document3 pages2019-06 ICMAB FL 001 PAC Year Question JUNE 2019Mohammad ShahidNo ratings yet

- 2020-12 ICMAB FL 001 PAC Year Question December 2020Document3 pages2020-12 ICMAB FL 001 PAC Year Question December 2020Mohammad ShahidNo ratings yet

- Accounting Process of A Services BusinessDocument9 pagesAccounting Process of A Services BusinessFiverr RallNo ratings yet

- ExamDocument5 pagesExamRudsan TurquezaNo ratings yet

- Enter Your Data: The Business Plan Will Appear in The Next SheetDocument13 pagesEnter Your Data: The Business Plan Will Appear in The Next SheetPrakash DuttaNo ratings yet

- 92 08 DeductionsDocument18 pages92 08 DeductionsNikkoNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- UGE1 - Author's PurposeDocument4 pagesUGE1 - Author's Purposelhyn JasarenoNo ratings yet

- CBM 112 Final Exam ReviewDocument3 pagesCBM 112 Final Exam Reviewlhyn JasarenoNo ratings yet

- GE 2 TopicsDocument32 pagesGE 2 Topicslhyn JasarenoNo ratings yet

- BLENDED LEARNING EFFECTIVENESSbigoDocument1 pageBLENDED LEARNING EFFECTIVENESSbigolhyn JasarenoNo ratings yet

- SPEECHDocument2 pagesSPEECHlhyn JasarenoNo ratings yet

- Document StyleDocument11 pagesDocument Stylelhyn JasarenoNo ratings yet

- ACC111 Week-8-9 ULOa 2Document14 pagesACC111 Week-8-9 ULOa 2lhyn JasarenoNo ratings yet

- Research PaperDocument13 pagesResearch Paperlhyn JasarenoNo ratings yet

- Pre TestDocument10 pagesPre Testlhyn JasarenoNo ratings yet

- Reveiwer 1Document1 pageReveiwer 1lhyn JasarenoNo ratings yet

- Acc111 - Q and ADocument5 pagesAcc111 - Q and Alhyn JasarenoNo ratings yet

- Department of Accounting Education ACC 111 - Course SyllabusDocument10 pagesDepartment of Accounting Education ACC 111 - Course Syllabuslhyn JasarenoNo ratings yet

- Purposive Communication Reviewer 2Document4 pagesPurposive Communication Reviewer 2lhyn JasarenoNo ratings yet

- Ponce Final Paper - Luis Ramirez-With-Cover-Page-V2Document27 pagesPonce Final Paper - Luis Ramirez-With-Cover-Page-V2Roswitha Klassen0% (1)

- Organizational Behavior: Robbins & JudgeDocument18 pagesOrganizational Behavior: Robbins & JudgeYandex PrithuNo ratings yet

- DR .Sharma Ji-05Document1 pageDR .Sharma Ji-05arunNo ratings yet

- (VigChr Supp 115) Lenka Karfíková - Grace and The Will According To Augustine 2012 PDFDocument443 pages(VigChr Supp 115) Lenka Karfíková - Grace and The Will According To Augustine 2012 PDFNovi Testamenti FiliusNo ratings yet

- Write A Short Note On Object Oriented MethodologyDocument5 pagesWrite A Short Note On Object Oriented Methodologycokog41585No ratings yet

- Climatic-Chambers DS FDMDocument3 pagesClimatic-Chambers DS FDMconkhimocNo ratings yet

- PR2 Qtr1 Module 2Document50 pagesPR2 Qtr1 Module 2mememew suppasitNo ratings yet

- Plumb Conc.Document28 pagesPlumb Conc.Muhammad AwaisNo ratings yet

- CAESAR II® How To Solve Friction ForceDocument2 pagesCAESAR II® How To Solve Friction Forcefurqan100% (1)

- STULZ WIB 67C 0811 en PDFDocument49 pagesSTULZ WIB 67C 0811 en PDFJaime MendozaNo ratings yet

- Reding Gapped TextDocument18 pagesReding Gapped TextChi Nguyen0% (2)

- MNL H8DCL (I) (6) (F)Document79 pagesMNL H8DCL (I) (6) (F)ericfgregoryNo ratings yet

- Vancouver Marathon by SlidesgoDocument37 pagesVancouver Marathon by SlidesgoAriya AnamNo ratings yet

- Aquafine DW Series ManualDocument19 pagesAquafine DW Series Manualjorman GuzmanNo ratings yet

- Ahb Example Amba System: Technical Reference ManualDocument222 pagesAhb Example Amba System: Technical Reference ManualJinsNo ratings yet

- MPI GTU Study Material E-Notes Introduction-To-Microprocessor 13052022114954AMDocument4 pagesMPI GTU Study Material E-Notes Introduction-To-Microprocessor 13052022114954AMKartik RamchandaniNo ratings yet

- Source TransformationDocument5 pagesSource Transformationraovinayakm2No ratings yet

- Poem Leisure - f3Document5 pagesPoem Leisure - f3fazdly0706No ratings yet

- Chapter One The Problem and Its Setting 1.1 Background of The StudyDocument10 pagesChapter One The Problem and Its Setting 1.1 Background of The StudyJholo BuctonNo ratings yet

- Assignment 2Document2 pagesAssignment 2Nzan NkapNo ratings yet

- Week 2: Introduction To LiteratureDocument45 pagesWeek 2: Introduction To LiteratureEirlys NhiNo ratings yet

- Jacob BohmeDocument12 pagesJacob BohmeTimothy Edwards100% (1)

- MG Motor Success Story - Case Study - FN PDFDocument4 pagesMG Motor Success Story - Case Study - FN PDFsevakendra palyaNo ratings yet

- SWE2007 - Fundamentals of Operating SystemsDocument6 pagesSWE2007 - Fundamentals of Operating SystemsmaneeshmogallpuNo ratings yet

- CP E80.50 EPSWindowsClient UserGuide enDocument36 pagesCP E80.50 EPSWindowsClient UserGuide enmbaezasotoNo ratings yet

- Timeline of Indian History - Wikipedia, The Free EncyclopediaDocument24 pagesTimeline of Indian History - Wikipedia, The Free EncyclopediaPrabhu Charan TejaNo ratings yet

- Statement of IntentDocument4 pagesStatement of IntentteanNo ratings yet

Download as pdf or txt

You might also like

- An Introduction To Scholarship Building AcademicDocument3 pagesAn Introduction To Scholarship Building AcademicNina Rosalee21% (29)

- Solution Manual For Theory and Design For Mechanical Measurements 6th Edition Richard S Figliola Donald e BeasleyDocument20 pagesSolution Manual For Theory and Design For Mechanical Measurements 6th Edition Richard S Figliola Donald e BeasleyLoriWilliamsonoqabx98% (46)

- Accounting For Managers (Assignment One (E-Finance) ) Question OneDocument7 pagesAccounting For Managers (Assignment One (E-Finance) ) Question OnehananNo ratings yet

- A Holistic Approach in Understanding The SelfDocument7 pagesA Holistic Approach in Understanding The Selflhyn JasarenoNo ratings yet

- Assignment 4 - Financial Accounting - February 11Document4 pagesAssignment 4 - Financial Accounting - February 11Ednalyn PascualNo ratings yet

- Nerissa Mae L. Santos Activity On Completing The Accounting Cycle 1Document3 pagesNerissa Mae L. Santos Activity On Completing The Accounting Cycle 1Mica Mae Correa100% (1)

- Module 4 - Problem 5Document1 pageModule 4 - Problem 5Lycksele RodulfaNo ratings yet

- Well Security When Openfile Operator: This Data Is Sourced From Peps and Updated MonthlyDocument245 pagesWell Security When Openfile Operator: This Data Is Sourced From Peps and Updated Monthlyrahul2904No ratings yet

- ACC111 Week-8-9 ULOa 2Document14 pagesACC111 Week-8-9 ULOa 2lhyn JasarenoNo ratings yet

- Finals Activity No .2 Completing THE Accounting Cycle: Palad, Nica C. Mr. Alfred BautistaDocument6 pagesFinals Activity No .2 Completing THE Accounting Cycle: Palad, Nica C. Mr. Alfred BautistaMica Mae CorreaNo ratings yet

- Cash Receipt and Disbursement ProgramDocument1 pageCash Receipt and Disbursement ProgramNicah AcojonNo ratings yet

- TAXN 1016 FE - Long ProblemsDocument11 pagesTAXN 1016 FE - Long ProblemsCrystel Kate MananganNo ratings yet

- Exercise 5 - Completing The Accounting Cycle For Merchandising and Service BusinessDocument4 pagesExercise 5 - Completing The Accounting Cycle For Merchandising and Service BusinessShiela Rengel0% (2)

- AE21 Lesson 6: Review of The Accounting Cycle: Worksheet and Adjusting EntriesDocument6 pagesAE21 Lesson 6: Review of The Accounting Cycle: Worksheet and Adjusting EntriesGlenda LinatocNo ratings yet

- Sample Problem For Last MeetingDocument11 pagesSample Problem For Last MeetingLylanie Alcoran AnibNo ratings yet

- 04 Prelim ExaminationDocument2 pages04 Prelim ExaminationJomarie BenedictoNo ratings yet

- MOJAKOE AK1 UTS 2012 GasalDocument15 pagesMOJAKOE AK1 UTS 2012 GasalVincenttio le CloudNo ratings yet

- Course Book Chapter 10Document28 pagesCourse Book Chapter 10Amirul Hakim Nor AzmanNo ratings yet

- Problem 3 ACCA101Document3 pagesProblem 3 ACCA101Nicole FidelsonNo ratings yet

- Acc 111 - Week 1-3 UloeDocument5 pagesAcc 111 - Week 1-3 UloeJaisa Mae RosalesNo ratings yet

- Comprehensive Problem: Flashback Activity 4Document1 pageComprehensive Problem: Flashback Activity 4James SyNo ratings yet

- 04 Handout 1Document6 pages04 Handout 1Nhov CabralNo ratings yet

- FS - LandscapeDocument9 pagesFS - LandscapeMekay OcasionesNo ratings yet

- Bai Tap - IAS 12 - Tu LuanDocument14 pagesBai Tap - IAS 12 - Tu LuanTrần Nguyễn Tuệ MinhNo ratings yet

- Exercises On Implementation of DCF ApproachDocument10 pagesExercises On Implementation of DCF ApproachVincenzoPizzulliNo ratings yet

- Activity - Preparation of Financial StatementsDocument4 pagesActivity - Preparation of Financial StatementsJoy ValenciaNo ratings yet

- Corporate Taxes Part 1 (VAT, EWT and Income Tax) CaseDocument4 pagesCorporate Taxes Part 1 (VAT, EWT and Income Tax) CaseMikaela L. RoqueNo ratings yet

- Midterms Problem SolvingDocument3 pagesMidterms Problem SolvingTRINA ARUTANo ratings yet

- Midterm Examination For AC11N: ProblemDocument1 pageMidterm Examination For AC11N: ProblemLeica JaymeNo ratings yet

- Tagala Aec 217 Week 4 ActivityDocument2 pagesTagala Aec 217 Week 4 ActivityDrewGuanzonGoboyTagalaNo ratings yet

- Group Assignment On Fundamentals of Accounting IDocument6 pagesGroup Assignment On Fundamentals of Accounting IKaleab ShimelsNo ratings yet

- Jawaban No 3 A Dan BDocument6 pagesJawaban No 3 A Dan BAndi Rahmat HidayatNo ratings yet

- Acct1101 Final Examination SEMESTER 2, 2020Document13 pagesAcct1101 Final Examination SEMESTER 2, 2020Yahya ZafarNo ratings yet

- Barangay Buenasuerte Notes To Financial StatementsDocument5 pagesBarangay Buenasuerte Notes To Financial StatementsRose Macoy CastilloNo ratings yet

- Elimination RoundDocument11 pagesElimination RoundDeeNo ratings yet

- Complete Cycle Servicing Graded ActivityDocument2 pagesComplete Cycle Servicing Graded ActivityErfel Al KitmaNo ratings yet

- Adjusting EntriesDocument5 pagesAdjusting EntriesM Hassan BrohiNo ratings yet

- Chapter 14Document6 pagesChapter 14Mychie Lynne MayugaNo ratings yet

- ACCA101 Leah May SantiagoDocument9 pagesACCA101 Leah May SantiagoNicole FidelsonNo ratings yet

- 06 Task Performance 1 ARGDocument4 pages06 Task Performance 1 ARGshiplusNo ratings yet

- Toaz - Info Prelim Midterm PRDocument98 pagesToaz - Info Prelim Midterm PRClandestine SoulNo ratings yet

- Practical Case Financial BudgetDocument17 pagesPractical Case Financial BudgetScribdTranslationsNo ratings yet

- QuizDocument2 pagesQuizaprilbetito02No ratings yet

- Junior Philippine Institute of AccountantsDocument10 pagesJunior Philippine Institute of AccountantsJuan paoloNo ratings yet

- Adjusting EntryDocument13 pagesAdjusting Entrymichaella maglinteNo ratings yet

- Fabm2 Learning-Activity-2Document5 pagesFabm2 Learning-Activity-2Cha Eun WooNo ratings yet

- WorksheetDocument10 pagesWorksheetScribdTranslationsNo ratings yet

- BINI General Merchandise Answer Key 2Document19 pagesBINI General Merchandise Answer Key 2workwithericajaneNo ratings yet

- INCOTAXDocument4 pagesINCOTAXnicole bancoroNo ratings yet

- Cap II Group I RTP Dec2023Document84 pagesCap II Group I RTP Dec2023pratyushmudbhari340No ratings yet

- Activity 01 PDFDocument5 pagesActivity 01 PDFJennifer AdvientoNo ratings yet

- No.2 FA Assignment 3 Amato FIXDocument3 pagesNo.2 FA Assignment 3 Amato FIXKevin DeswandaNo ratings yet

- AnsweredASS16 AccountingDocument6 pagesAnsweredASS16 Accountingvomawew647No ratings yet

- 3 Exam Part IDocument6 pages3 Exam Part IRJ DAVE DURUHANo ratings yet

- Quiz 2 Cashflows Final PDFDocument4 pagesQuiz 2 Cashflows Final PDFChito MirandaNo ratings yet

- Financial Statements PreparationDocument6 pagesFinancial Statements Preparationana lopezNo ratings yet

- Ias 07Document72 pagesIas 07Hannan Fatima EllahiNo ratings yet

- 2019-06 ICMAB FL 001 PAC Year Question JUNE 2019Document3 pages2019-06 ICMAB FL 001 PAC Year Question JUNE 2019Mohammad ShahidNo ratings yet

- 2020-12 ICMAB FL 001 PAC Year Question December 2020Document3 pages2020-12 ICMAB FL 001 PAC Year Question December 2020Mohammad ShahidNo ratings yet

- Accounting Process of A Services BusinessDocument9 pagesAccounting Process of A Services BusinessFiverr RallNo ratings yet

- ExamDocument5 pagesExamRudsan TurquezaNo ratings yet

- Enter Your Data: The Business Plan Will Appear in The Next SheetDocument13 pagesEnter Your Data: The Business Plan Will Appear in The Next SheetPrakash DuttaNo ratings yet

- 92 08 DeductionsDocument18 pages92 08 DeductionsNikkoNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- UGE1 - Author's PurposeDocument4 pagesUGE1 - Author's Purposelhyn JasarenoNo ratings yet

- CBM 112 Final Exam ReviewDocument3 pagesCBM 112 Final Exam Reviewlhyn JasarenoNo ratings yet

- GE 2 TopicsDocument32 pagesGE 2 Topicslhyn JasarenoNo ratings yet

- BLENDED LEARNING EFFECTIVENESSbigoDocument1 pageBLENDED LEARNING EFFECTIVENESSbigolhyn JasarenoNo ratings yet

- SPEECHDocument2 pagesSPEECHlhyn JasarenoNo ratings yet

- Document StyleDocument11 pagesDocument Stylelhyn JasarenoNo ratings yet

- ACC111 Week-8-9 ULOa 2Document14 pagesACC111 Week-8-9 ULOa 2lhyn JasarenoNo ratings yet

- Research PaperDocument13 pagesResearch Paperlhyn JasarenoNo ratings yet

- Pre TestDocument10 pagesPre Testlhyn JasarenoNo ratings yet

- Reveiwer 1Document1 pageReveiwer 1lhyn JasarenoNo ratings yet

- Acc111 - Q and ADocument5 pagesAcc111 - Q and Alhyn JasarenoNo ratings yet

- Department of Accounting Education ACC 111 - Course SyllabusDocument10 pagesDepartment of Accounting Education ACC 111 - Course Syllabuslhyn JasarenoNo ratings yet

- Purposive Communication Reviewer 2Document4 pagesPurposive Communication Reviewer 2lhyn JasarenoNo ratings yet

- Ponce Final Paper - Luis Ramirez-With-Cover-Page-V2Document27 pagesPonce Final Paper - Luis Ramirez-With-Cover-Page-V2Roswitha Klassen0% (1)

- Organizational Behavior: Robbins & JudgeDocument18 pagesOrganizational Behavior: Robbins & JudgeYandex PrithuNo ratings yet

- DR .Sharma Ji-05Document1 pageDR .Sharma Ji-05arunNo ratings yet

- (VigChr Supp 115) Lenka Karfíková - Grace and The Will According To Augustine 2012 PDFDocument443 pages(VigChr Supp 115) Lenka Karfíková - Grace and The Will According To Augustine 2012 PDFNovi Testamenti FiliusNo ratings yet

- Write A Short Note On Object Oriented MethodologyDocument5 pagesWrite A Short Note On Object Oriented Methodologycokog41585No ratings yet

- Climatic-Chambers DS FDMDocument3 pagesClimatic-Chambers DS FDMconkhimocNo ratings yet

- PR2 Qtr1 Module 2Document50 pagesPR2 Qtr1 Module 2mememew suppasitNo ratings yet

- Plumb Conc.Document28 pagesPlumb Conc.Muhammad AwaisNo ratings yet

- CAESAR II® How To Solve Friction ForceDocument2 pagesCAESAR II® How To Solve Friction Forcefurqan100% (1)

- STULZ WIB 67C 0811 en PDFDocument49 pagesSTULZ WIB 67C 0811 en PDFJaime MendozaNo ratings yet

- Reding Gapped TextDocument18 pagesReding Gapped TextChi Nguyen0% (2)

- MNL H8DCL (I) (6) (F)Document79 pagesMNL H8DCL (I) (6) (F)ericfgregoryNo ratings yet

- Vancouver Marathon by SlidesgoDocument37 pagesVancouver Marathon by SlidesgoAriya AnamNo ratings yet

- Aquafine DW Series ManualDocument19 pagesAquafine DW Series Manualjorman GuzmanNo ratings yet

- Ahb Example Amba System: Technical Reference ManualDocument222 pagesAhb Example Amba System: Technical Reference ManualJinsNo ratings yet

- MPI GTU Study Material E-Notes Introduction-To-Microprocessor 13052022114954AMDocument4 pagesMPI GTU Study Material E-Notes Introduction-To-Microprocessor 13052022114954AMKartik RamchandaniNo ratings yet

- Source TransformationDocument5 pagesSource Transformationraovinayakm2No ratings yet

- Poem Leisure - f3Document5 pagesPoem Leisure - f3fazdly0706No ratings yet

- Chapter One The Problem and Its Setting 1.1 Background of The StudyDocument10 pagesChapter One The Problem and Its Setting 1.1 Background of The StudyJholo BuctonNo ratings yet

- Assignment 2Document2 pagesAssignment 2Nzan NkapNo ratings yet

- Week 2: Introduction To LiteratureDocument45 pagesWeek 2: Introduction To LiteratureEirlys NhiNo ratings yet

- Jacob BohmeDocument12 pagesJacob BohmeTimothy Edwards100% (1)

- MG Motor Success Story - Case Study - FN PDFDocument4 pagesMG Motor Success Story - Case Study - FN PDFsevakendra palyaNo ratings yet

- SWE2007 - Fundamentals of Operating SystemsDocument6 pagesSWE2007 - Fundamentals of Operating SystemsmaneeshmogallpuNo ratings yet

- CP E80.50 EPSWindowsClient UserGuide enDocument36 pagesCP E80.50 EPSWindowsClient UserGuide enmbaezasotoNo ratings yet

- Timeline of Indian History - Wikipedia, The Free EncyclopediaDocument24 pagesTimeline of Indian History - Wikipedia, The Free EncyclopediaPrabhu Charan TejaNo ratings yet

- Statement of IntentDocument4 pagesStatement of IntentteanNo ratings yet