Download as xls, pdf, or txt

You might also like

- Grade 9 Financial Literacy Workbook Term 4Document16 pagesGrade 9 Financial Literacy Workbook Term 4thokoanebokang00No ratings yet

- Sun Brewing Case ExhibitsDocument26 pagesSun Brewing Case ExhibitsShshankNo ratings yet

- "Case Analysis-Cafés Monte Blanco: Building A Profit Plan": Managerial AccountingDocument8 pages"Case Analysis-Cafés Monte Blanco: Building A Profit Plan": Managerial Accountingvipul tutejaNo ratings yet

- BFIN 300 SP 19 Final Guideline AnswersDocument9 pagesBFIN 300 SP 19 Final Guideline AnswersZafran AqilNo ratings yet

- Analisis Laporan Keuangan SubramanyamDocument40 pagesAnalisis Laporan Keuangan Subramanyamirfanlaka2No ratings yet

- Tata MotorsDocument24 pagesTata MotorsApurvAdarshNo ratings yet

- Course: Hospitality Financial Management 2 Course Code: HFM 211 Topic: Financial Statements Lecturer: DR O. MhlangaDocument2 pagesCourse: Hospitality Financial Management 2 Course Code: HFM 211 Topic: Financial Statements Lecturer: DR O. MhlangaThando NkosiNo ratings yet

- Income Statement ExerciseDocument6 pagesIncome Statement Exercisenatasha dikolaNo ratings yet

- Basic Accounting Equation and Vat TutorialsDocument3 pagesBasic Accounting Equation and Vat TutorialsThembelihle SitholeNo ratings yet

- Master Fiancial Statements SP Act 1Document13 pagesMaster Fiancial Statements SP Act 1Kathryn ParadisosNo ratings yet

- Financial Statements For Sole Partnership - KatDocument12 pagesFinancial Statements For Sole Partnership - KatKathryn ParadisosNo ratings yet

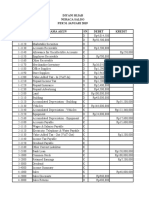

- ZSD Training Hub Balance SheetDocument1 pageZSD Training Hub Balance SheetTiisetsoNo ratings yet

- Property24 Detailed Rate Card 2024Document2 pagesProperty24 Detailed Rate Card 2024Njabulo S. NgwenyaNo ratings yet

- Amalgamation - Example 1 To 4Document4 pagesAmalgamation - Example 1 To 4Zhong HanNo ratings yet

- VAT Test One 2021 Question PaperDocument3 pagesVAT Test One 2021 Question PapermballyenhlendabaNo ratings yet

- Chapter 10 - Debtors and CreditorsDocument20 pagesChapter 10 - Debtors and CreditorsMkhonto XuluNo ratings yet

- AGUSTINA PUTRI MANISHA-Toko Panasonic-29Document32 pagesAGUSTINA PUTRI MANISHA-Toko Panasonic-29Agustina Putrii MNo ratings yet

- Closing Entries 2022Document17 pagesClosing Entries 2022Tuyakula ShipadiNo ratings yet

- N5 Financial Accounting June 2018Document18 pagesN5 Financial Accounting June 2018Anil HarichandreNo ratings yet

- July Cost ForecastDocument2 pagesJuly Cost ForecastKingstone basikoloNo ratings yet

- P7 Ahmad Sugiarto AdhariDocument5 pagesP7 Ahmad Sugiarto Adhariahmad shinigamiNo ratings yet

- Balance SheetDocument4 pagesBalance SheetkhozqluckyNo ratings yet

- Sale Agreement Annexure BudgetsDocument1 pageSale Agreement Annexure Budgetssivz7730No ratings yet

- EMS G9 Act 8 Class ExampleDocument2 pagesEMS G9 Act 8 Class Examplemphephuhope3No ratings yet

- 2018 MONTLY BUDGET (R 19800) Expenses April MAY June July AUGDocument2 pages2018 MONTLY BUDGET (R 19800) Expenses April MAY June July AUGViweNo ratings yet

- Financial Accounting 2 Assign 2Document7 pagesFinancial Accounting 2 Assign 2ronellNo ratings yet

- Tutorial 5 - Cash FlowsDocument3 pagesTutorial 5 - Cash Flows85pd6t77wnNo ratings yet

- Smart LaundryDocument21 pagesSmart Laundryfriskila dewiNo ratings yet

- Accounting Cycle WorksheetDocument11 pagesAccounting Cycle Worksheettarikuabdisa0No ratings yet

- FS$12134061$BCLACC$466850$3491Document9 pagesFS$12134061$BCLACC$466850$3491CalistaNo ratings yet

- Journal Entries For The Month of November: Solutions To Handout # 1: in Class Problem # 1Document8 pagesJournal Entries For The Month of November: Solutions To Handout # 1: in Class Problem # 1simran punjabiNo ratings yet

- Accounting Grade 9 November ExamDocument7 pagesAccounting Grade 9 November Examabongwek0No ratings yet

- Assignment July 2022Document6 pagesAssignment July 2022Dusabamahoro JoniveNo ratings yet

- Quiz AkunDocument5 pagesQuiz Akunrhmaaynfz rvyNo ratings yet

- Cash Flow CNC Router - Rev7 - 24jul2017Document167 pagesCash Flow CNC Router - Rev7 - 24jul2017Bayu NugrahaNo ratings yet

- Roon Richera GirsangDocument2 pagesRoon Richera Girsangkidus.gaming52No ratings yet

- Assignment 4 Acc1 D20059486-D GxabaDocument12 pagesAssignment 4 Acc1 D20059486-D GxabaGugulethu XabaNo ratings yet

- Lira Consulting, Sa Adjusting Entry May 31, 2017: TotalDocument10 pagesLira Consulting, Sa Adjusting Entry May 31, 2017: TotalAngellamndaNo ratings yet

- Fabm Sample Exercises With Answer KeyDocument7 pagesFabm Sample Exercises With Answer KeySg Dimz100% (1)

- WS 2 Financial Report Dhafi XI BarcelonaDocument5 pagesWS 2 Financial Report Dhafi XI BarcelonaWedi PratamaNo ratings yet

- Akuntansi Keuangan LanjutanDocument28 pagesAkuntansi Keuangan LanjutanYulitaNo ratings yet

- FAC1502-2014 Exam Paper SolutionsDocument1 pageFAC1502-2014 Exam Paper SolutionsnjabuzamaNo ratings yet

- Practice For FinalsDocument3 pagesPractice For FinalsStefanie EstilloreNo ratings yet

- Admission of Partner Extra QuestionDocument2 pagesAdmission of Partner Extra Questionaneupane465No ratings yet

- Bahas SoalDocument5 pagesBahas SoalAlifahmuhtiNo ratings yet

- 4 - Dissolution IllustrationDocument14 pages4 - Dissolution IllustrationAlrac GarciaNo ratings yet

- PartnershipDocument28 pagesPartnershipVasu JainNo ratings yet

- Rm. MusicDocument17 pagesRm. MusicMutia AlhasanahNo ratings yet

- Projected Income StatementDocument2 pagesProjected Income StatementChristine VillaNo ratings yet

- Adjustments To Final AccountsDocument20 pagesAdjustments To Final AccountsSalamaNo ratings yet

- Ak - Keuangan Salon CantikDocument13 pagesAk - Keuangan Salon CantikNajwa SyaharaniNo ratings yet

- Partnership - I: Change in Profit Sharing RatioDocument33 pagesPartnership - I: Change in Profit Sharing RatioUjjwal BeriwalNo ratings yet

- Ngongo Lundikazi 201813006 Tut3Document6 pagesNgongo Lundikazi 201813006 Tut3lundingongoNo ratings yet

- Lembar Kerja Komputer Ukk Tina Nur Aisyah Xii Ak 1 25Document30 pagesLembar Kerja Komputer Ukk Tina Nur Aisyah Xii Ak 1 25RizalJalilPujaKesumaNo ratings yet

- Test - AccountingDocument7 pagesTest - AccountingSoumyadip DasNo ratings yet

- Assignment AnswerDocument2 pagesAssignment AnswerMims ChiiiNo ratings yet

- FSeT - Recommended HW CH7Document31 pagesFSeT - Recommended HW CH7tabi10592No ratings yet

- Tutorial Unit 2 Relevant Costing SolutionsDocument3 pagesTutorial Unit 2 Relevant Costing SolutionsNdivho MavhethaNo ratings yet

- Latihan Ukk Brilian Anastasya PutriDocument36 pagesLatihan Ukk Brilian Anastasya PutriApoloos Ryan100% (1)

- Kunci Jawaban Quiz AI UTS TA Ganjil 1920Document7 pagesKunci Jawaban Quiz AI UTS TA Ganjil 1920David PhangNo ratings yet

- Accounting Worksheet Problem 4Document19 pagesAccounting Worksheet Problem 4RELLON, James, M.100% (1)

- ACR4.3 Cindy QaaniaDocument4 pagesACR4.3 Cindy QaaniaIndrian Sibi todingNo ratings yet

- Lembar Jawaban Siklus DagangDocument56 pagesLembar Jawaban Siklus DagangSuci Agriani IdrusNo ratings yet

- Chapter 09 - InventoryDocument29 pagesChapter 09 - InventoryMkhonto XuluNo ratings yet

- Chapter 05 - Journals and LedgersDocument27 pagesChapter 05 - Journals and LedgersMkhonto XuluNo ratings yet

- Chapter 06 - AdjustmentsDocument26 pagesChapter 06 - AdjustmentsMkhonto Xulu100% (1)

- Chapter 07 - Financial StatementsDocument40 pagesChapter 07 - Financial StatementsMkhonto XuluNo ratings yet

- Chapter 10 - Debtors and CreditorsDocument20 pagesChapter 10 - Debtors and CreditorsMkhonto XuluNo ratings yet

- Chapter 08 - Bank and CashDocument13 pagesChapter 08 - Bank and CashMkhonto XuluNo ratings yet

- MCQ Bcom Finance Taxation Optional Financial ManagementDocument22 pagesMCQ Bcom Finance Taxation Optional Financial ManagementShyam KumarNo ratings yet

- Fin202 - Chap 3,4,5,6Document20 pagesFin202 - Chap 3,4,5,6An Gia Khuong (K17 CT)No ratings yet

- Project Brief - Ice Cream Making Iligan Sorbetes Producers CoopDocument12 pagesProject Brief - Ice Cream Making Iligan Sorbetes Producers CoopMuneer HinayNo ratings yet

- Accountancy 2023-24 MSDocument11 pagesAccountancy 2023-24 MSirfanoushad15No ratings yet

- ABC Chapter 4 - Accounting For Business Combinations by Millan 2020 ABC Chapter 4 - Accounting For Business Combinations by Millan 2020Document8 pagesABC Chapter 4 - Accounting For Business Combinations by Millan 2020 ABC Chapter 4 - Accounting For Business Combinations by Millan 2020JessaNo ratings yet

- Tshiamo Poultry: Find UsDocument19 pagesTshiamo Poultry: Find UsQondile PhilileNo ratings yet

- FinMan Assign. No. 3 - ToyWorldDocument6 pagesFinMan Assign. No. 3 - ToyWorldKristine Nitzkie SalazarNo ratings yet

- Ak - Keuangan Salon CantikDocument13 pagesAk - Keuangan Salon CantikNajwa SyaharaniNo ratings yet

- Caleb Chipeta (g11106) and Simon Musala Kunda (Baa18056) and Lottie Jason Muwowo (Zu18115) - 1Document75 pagesCaleb Chipeta (g11106) and Simon Musala Kunda (Baa18056) and Lottie Jason Muwowo (Zu18115) - 1caleb chipetaNo ratings yet

- Airasia Comprehensive Case Analysis 2Document32 pagesAirasia Comprehensive Case Analysis 2Shaina Mae C ValenzuelaNo ratings yet

- Annual Report 2013 PDFDocument75 pagesAnnual Report 2013 PDFsururyNo ratings yet

- 1.2 Corporate Accounting PDFDocument6 pages1.2 Corporate Accounting PDFRech MJNo ratings yet

- Partnership Formation 001Document20 pagesPartnership Formation 001Ma Teresa B. Cerezo50% (2)

- Use The Following Information For The Next Seven Questions:: Activity 2.4Document2 pagesUse The Following Information For The Next Seven Questions:: Activity 2.4Tine Vasiana Duerme0% (1)

- Joint ArrrangementsDocument5 pagesJoint ArrrangementsGIGI BODONo ratings yet

- Financial Statement AnalysisDocument95 pagesFinancial Statement Analysisputri handayaniNo ratings yet

- Radico Khaitan ValuationDocument28 pagesRadico Khaitan ValuationvishakhaNo ratings yet

- Pakistan State Oil Introduction of The OrganizationDocument32 pagesPakistan State Oil Introduction of The OrganizationTAS_ALPHANo ratings yet

- PLZL Olympiada Site Visit Aug 08Document20 pagesPLZL Olympiada Site Visit Aug 08tennertyNo ratings yet

- Ch14.doc AccountingDocument45 pagesCh14.doc AccountingYAHIA ADELNo ratings yet

- Group1 RTP PDFDocument186 pagesGroup1 RTP PDFABCDEFGHNo ratings yet

- Dwnload Full Corporate Finance Asia Global 1st Edition Ross Solutions Manual PDFDocument35 pagesDwnload Full Corporate Finance Asia Global 1st Edition Ross Solutions Manual PDFmiltongoodwin2490i100% (16)

- Group Assignment Analyzing Financial Statement of VinamilkDocument24 pagesGroup Assignment Analyzing Financial Statement of VinamilkNhư ThảoNo ratings yet

- A Further Look at Financial StatementsDocument56 pagesA Further Look at Financial StatementsLê Thanh HàNo ratings yet

- Assigment Account FullDocument16 pagesAssigment Account FullFaid AmmarNo ratings yet