Download as pdf or txt

You might also like

- Unit 6 Written Assignment BUS 5110Document5 pagesUnit 6 Written Assignment BUS 5110luiza100% (6)

- Ross12e Chapter03 TB AnswerkeyDocument44 pagesRoss12e Chapter03 TB AnswerkeyÂn TrầnNo ratings yet

- Managerial Accounting 5e Braun and Tietz Table of ContentsDocument26 pagesManagerial Accounting 5e Braun and Tietz Table of ContentsJill ShawNo ratings yet

- Case Study - Transaction Exposure - LufthansaDocument2 pagesCase Study - Transaction Exposure - LufthansaRaguRagupathy100% (3)

- A COMPARATIVE STUDY ON FINANCIAL PERFORMANCE OF SELECT AUTOMOBILE INDUSTRIES IN INDIA" (Four Wheelers)Document100 pagesA COMPARATIVE STUDY ON FINANCIAL PERFORMANCE OF SELECT AUTOMOBILE INDUSTRIES IN INDIA" (Four Wheelers)Prashanth PB82% (17)

- A Study On Financial Performance Analysis of Three Tyre IndustryDocument36 pagesA Study On Financial Performance Analysis of Three Tyre Industryeshu67% (3)

- CH 14Document22 pagesCH 14BensonChiuNo ratings yet

- LESSON 1 IntroductionDocument7 pagesLESSON 1 IntroductionMich ValenciaNo ratings yet

- Introduction To FinanceDocument2 pagesIntroduction To FinanceSougoto PaulNo ratings yet

- A Study On Credit Risk Management EDITING (Daniel Xavier)Document91 pagesA Study On Credit Risk Management EDITING (Daniel Xavier)uday manikantaNo ratings yet

- Prelim ModuleDocument5 pagesPrelim ModuleJenefer GwmpesawNo ratings yet

- MBA-608 (CF) DoneDocument10 pagesMBA-608 (CF) DonekushNo ratings yet

- Blcok 1 Mco 7 Unit 1 Financial ManagementDocument10 pagesBlcok 1 Mco 7 Unit 1 Financial Managementshivi2504No ratings yet

- Business Finance Xii SP New SyllabusDocument21 pagesBusiness Finance Xii SP New SyllabusSanthosh Kumar100% (1)

- Nature and Scope of FinanceDocument6 pagesNature and Scope of Financejusteliza473No ratings yet

- SHIVA Chapter 1 and 2Document29 pagesSHIVA Chapter 1 and 2a NaniNo ratings yet

- Vignesh Main Project Final-1 PDFDocument60 pagesVignesh Main Project Final-1 PDFAjith KumarNo ratings yet

- Chapter One - HandoutDocument11 pagesChapter One - HandoutLeykun mengistuNo ratings yet

- 1.1 Financial StatementsDocument15 pages1.1 Financial StatementsSandeep DhupalNo ratings yet

- Question Bank For FM Both Part - A & Part - BDocument167 pagesQuestion Bank For FM Both Part - A & Part - BnandhuNo ratings yet

- Explain The Objectives of Financial Management, Interphase Between Finance and Other FunctionsDocument12 pagesExplain The Objectives of Financial Management, Interphase Between Finance and Other FunctionsgangadharNo ratings yet

- Lesson 02Document10 pagesLesson 02Zeleine Raine Del RosarioNo ratings yet

- Fundamentals of Finance and Financial ManagementDocument4 pagesFundamentals of Finance and Financial ManagementCrisha Diane GalvezNo ratings yet

- Af 212 Financial ManagementDocument608 pagesAf 212 Financial ManagementMaster KihimbwaNo ratings yet

- Chapter 3Document26 pagesChapter 3Siddhesh TamhanekarNo ratings yet

- Chapter 1Document12 pagesChapter 1Demeke AtNo ratings yet

- 1.1 Concept of FinanceDocument10 pages1.1 Concept of Financeprasadnaidu00No ratings yet

- FM 1 MaterialDocument17 pagesFM 1 MaterialSwati SachdevaNo ratings yet

- Financial ManagementDocument51 pagesFinancial Managementarjunmba119624No ratings yet

- Prakash ShrideviDocument94 pagesPrakash ShrideviAbhishekNo ratings yet

- PDF To Document 687Document29 pagesPDF To Document 687karthikmerwade4No ratings yet

- Week 2Document8 pagesWeek 2Shanley Vanna EscalonaNo ratings yet

- Module 1 FM NotesDocument18 pagesModule 1 FM NotesDachu DarshanNo ratings yet

- A Study On Financial Strength and Weakness of Sree Ranga Foods (Rainbow Masala)Document83 pagesA Study On Financial Strength and Weakness of Sree Ranga Foods (Rainbow Masala)Naresh KumarNo ratings yet

- FM NotesDocument61 pagesFM Noteskunal taldarNo ratings yet

- Q 1. Write Down The Objectives of Financial Management and Corporate Finance?Document7 pagesQ 1. Write Down The Objectives of Financial Management and Corporate Finance?Saad MalikNo ratings yet

- BFN 111 - Week 1Document20 pagesBFN 111 - Week 1CHIDINMA ONUORAHNo ratings yet

- Fundamentals of Financial Management (BBS II Year) Chapter: 1 (Introduction To Financial Management)Document7 pagesFundamentals of Financial Management (BBS II Year) Chapter: 1 (Introduction To Financial Management)Bibek Sh KhadgiNo ratings yet

- Financial MGMT For ABVMDocument33 pagesFinancial MGMT For ABVMjibridhamoleNo ratings yet

- Financial ManagementDocument43 pagesFinancial Managementonly_vimaljoshi100% (3)

- Business Finance Module 1Document10 pagesBusiness Finance Module 1Adoree RamosNo ratings yet

- 9.1 Management of Financial ResourcesDocument22 pages9.1 Management of Financial Resourcesanshumalviya230504No ratings yet

- Unit 1 Introduction To Financial ManagementDocument12 pagesUnit 1 Introduction To Financial ManagementPRIYA KUMARINo ratings yet

- Chapter 1 Scope and Objectives of Financial Management 2Document19 pagesChapter 1 Scope and Objectives of Financial Management 2Pandit Niraj Dilip SharmaNo ratings yet

- Managerial Finance and Accounting: Program OutcomesDocument14 pagesManagerial Finance and Accounting: Program OutcomesChicos tacosNo ratings yet

- Lecture 3 - Applying For FinanceDocument22 pagesLecture 3 - Applying For FinanceJad ZoghaibNo ratings yet

- Chapter One HandoutDocument16 pagesChapter One HandoutNati AlexNo ratings yet

- Financial Management Full NotesDocument30 pagesFinancial Management Full Notessaadsaaid0% (1)

- FinanceDocument10 pagesFinanceswati_rathourNo ratings yet

- CBET-22 102E: Rubie A. Lagare September 29, 2021Document3 pagesCBET-22 102E: Rubie A. Lagare September 29, 2021Rubie Aranas LagareNo ratings yet

- Module 3 FINP1 Financial ManagementDocument8 pagesModule 3 FINP1 Financial ManagementChristine Jane LumocsoNo ratings yet

- Financial Accounting ReportDocument11 pagesFinancial Accounting Reportthu thienNo ratings yet

- 03 BSAIS 2 Financial Management Week 5 6Document8 pages03 BSAIS 2 Financial Management Week 5 6Ace San GabrielNo ratings yet

- Thanigaimani Ph.D.1Document18 pagesThanigaimani Ph.D.1jhouvanNo ratings yet

- 1.1 What Is Financial Management?: 1.1.1 Investment DecisionDocument20 pages1.1 What Is Financial Management?: 1.1.1 Investment DecisionTasmay EnterprisesNo ratings yet

- Week 10 (Learning Materials)Document8 pagesWeek 10 (Learning Materials)CHOI HunterNo ratings yet

- Aims of Finance FunctionDocument56 pagesAims of Finance FunctionBV3S100% (1)

- A Study of Financial Performance Through RatiosDocument91 pagesA Study of Financial Performance Through RatiosPrashanth PBNo ratings yet

- Unit 1F.MDocument146 pagesUnit 1F.Mhamdi muhumed100% (4)

- Business Finance ModuleDocument37 pagesBusiness Finance Modulemiyanoharuka25No ratings yet

- FM Unit-1Document26 pagesFM Unit-1AjayNo ratings yet

- (C) Upes: Unit 1Document9 pages(C) Upes: Unit 1Ankita SharmaNo ratings yet

- Introduction To Advanced Financial ManagementDocument33 pagesIntroduction To Advanced Financial ManagementShubashPoojariNo ratings yet

- Financial Literacy for Entrepreneurs: Understanding the Numbers Behind Your BusinessFrom EverandFinancial Literacy for Entrepreneurs: Understanding the Numbers Behind Your BusinessNo ratings yet

- MGMT3076 U4v1 - 20180319Document11 pagesMGMT3076 U4v1 - 20180319Noelia Mc DonaldNo ratings yet

- ACCT3041 Unit 4 - 22082016Document15 pagesACCT3041 Unit 4 - 22082016Noelia Mc DonaldNo ratings yet

- ACCT3041 Unit 3 - 22082016Document15 pagesACCT3041 Unit 3 - 22082016Noelia Mc DonaldNo ratings yet

- ACCT3041 Unit 5 - 22082016Document11 pagesACCT3041 Unit 5 - 22082016Noelia Mc DonaldNo ratings yet

- Stock Valuation - Financial ManagementDocument10 pagesStock Valuation - Financial ManagementNoelia Mc DonaldNo ratings yet

- AFA QuizDocument15 pagesAFA QuizNoelia Mc DonaldNo ratings yet

- Financial Management - Bond ValuationDocument17 pagesFinancial Management - Bond ValuationNoelia Mc DonaldNo ratings yet

- Financial Management Time Value of MoneyDocument13 pagesFinancial Management Time Value of MoneyNoelia Mc DonaldNo ratings yet

- Advanced AccountingDocument13 pagesAdvanced AccountingNoelia Mc DonaldNo ratings yet

- Analysis - Germany - Corporate Taxation - IBFDDocument116 pagesAnalysis - Germany - Corporate Taxation - IBFDbilgintalhaNo ratings yet

- Capital Adequacy Asset Quality Management Soundness Earnings & Profitability Liquidity Sensitivity To Market RiskDocument23 pagesCapital Adequacy Asset Quality Management Soundness Earnings & Profitability Liquidity Sensitivity To Market RiskCharming AshishNo ratings yet

- A Study On How Derivative Instrument Used As An Effective Tool For Hedging, Speculation & ArbitrageDocument71 pagesA Study On How Derivative Instrument Used As An Effective Tool For Hedging, Speculation & Arbitrageujwaljaiswal100% (1)

- Joan Salgado Aud-Prob AssignmentDocument8 pagesJoan Salgado Aud-Prob AssignmentEsse ValdezNo ratings yet

- Kotler Pom18 Ch1 OmaimaDocument23 pagesKotler Pom18 Ch1 Omaimaevansalah79No ratings yet

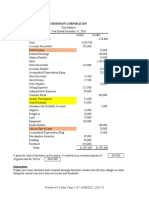

- Thompson Corporation: InstructionsDocument7 pagesThompson Corporation: InstructionsrahmawNo ratings yet

- Derringdo Question and AnswerDocument3 pagesDerringdo Question and Answerjustsee100% (2)

- Activity Chapter 3: (A) Average Annual Earnings 2,600,000Document2 pagesActivity Chapter 3: (A) Average Annual Earnings 2,600,000Randelle James FiestaNo ratings yet

- The Effect of Return On Assets (ROA) and Earning Per Share (EPS) On Stock Returns With Exchange Rates As Moderating VariablesDocument5 pagesThe Effect of Return On Assets (ROA) and Earning Per Share (EPS) On Stock Returns With Exchange Rates As Moderating VariablesInternational Journal of Business Marketing and ManagementNo ratings yet

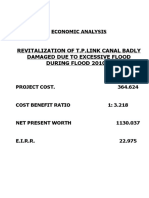

- Revitalization of T.P.Link Canal Badly Damaged Due To Excessive Flood During Flood 2010"Document4 pagesRevitalization of T.P.Link Canal Badly Damaged Due To Excessive Flood During Flood 2010"Xshf AkNo ratings yet

- Cellflix Tutorials Presents: Property, Plant and Equipment (PPE) (September 12,2020)Document74 pagesCellflix Tutorials Presents: Property, Plant and Equipment (PPE) (September 12,2020)edrianclydeNo ratings yet

- Investment TerminologyDocument20 pagesInvestment Terminologyshawon20shawonNo ratings yet

- Dabur ValuationDocument41 pagesDabur Valuationashwini patilNo ratings yet

- FINAL REPORT HDFC LifeDocument53 pagesFINAL REPORT HDFC LifeDarshan ShahNo ratings yet

- Dividend Policy NotesDocument6 pagesDividend Policy NotesSylvan Muzumbwe MakondoNo ratings yet

- Exercise 15-13 and 15-15 Samintang A031191129Document4 pagesExercise 15-13 and 15-15 Samintang A031191129SamintangNo ratings yet

- Investment Appraisal TechniquesDocument6 pagesInvestment Appraisal TechniquesERICK MLINGWANo ratings yet

- BCDocument73 pagesBCAbi Serrano Taguiam100% (2)

- FABM1 11 Quarter 4 Week 6 Las 3Document4 pagesFABM1 11 Quarter 4 Week 6 Las 3Janna PleteNo ratings yet

- Dec 2023 Financials UpdatedDocument102 pagesDec 2023 Financials Updatedpraveenramesh058No ratings yet

- ACCTG 221 Final Exam Part 1Document6 pagesACCTG 221 Final Exam Part 1Get BurnNo ratings yet

- Valuation GoodwilllDocument22 pagesValuation GoodwilllShubashPoojariNo ratings yet

- Triton Presentation 1Document28 pagesTriton Presentation 1yfatihNo ratings yet

- Project Report On The Indian Capital MarketDocument46 pagesProject Report On The Indian Capital MarketRohit JainNo ratings yet

- Foundations of Financial Management: DR Simmi AgrawalDocument33 pagesFoundations of Financial Management: DR Simmi AgrawalKapil ChoudharyNo ratings yet