Pmla Policy

Pmla Policy

You might also like

- Ruben Pater - CAPS LOCK-Valiz (2021)Document556 pagesRuben Pater - CAPS LOCK-Valiz (2021)Paulina Escobar AguirreNo ratings yet

- Yes Msme Sole Proprietor DeclarationDocument2 pagesYes Msme Sole Proprietor DeclarationSuraj SinghNo ratings yet

- SaaS Metrics Dashboard TemplateDocument12 pagesSaaS Metrics Dashboard TemplateMartin NelNo ratings yet

- Manual For A Toy Library PDFDocument21 pagesManual For A Toy Library PDFrabbitfootnintendo100% (1)

- ATM & Card Statistics For March 2018 POS AtmsDocument6 pagesATM & Card Statistics For March 2018 POS AtmsMathews KunnekkadanNo ratings yet

- ENTREPRENEURSHIP BY SPIRIT: How to Become a Dynamic and Fantastic EntrepreneurFrom EverandENTREPRENEURSHIP BY SPIRIT: How to Become a Dynamic and Fantastic EntrepreneurNo ratings yet

- AML and KYCDocument2 pagesAML and KYCRahulNo ratings yet

- Licensing HandbookDocument88 pagesLicensing HandbookajoiNo ratings yet

- Anti-Money Launder - AML-CFT Guide BI 260218 With LetterDocument3 pagesAnti-Money Launder - AML-CFT Guide BI 260218 With LetterLc KohNo ratings yet

- Microfinance 3.0Document207 pagesMicrofinance 3.0shannenNo ratings yet

- PMLA PolicyDocument36 pagesPMLA PolicySatwant singhNo ratings yet

- Kyc Aml Policy Revised DT 24.06.21 Updated Upto 10.05.2021Document98 pagesKyc Aml Policy Revised DT 24.06.21 Updated Upto 10.05.2021Priya dharshanNo ratings yet

- Facts About GamblingDocument2 pagesFacts About GamblingJohn Partridge100% (1)

- W1&2 Features of Public Listed Company and Multinational CompanyDocument9 pagesW1&2 Features of Public Listed Company and Multinational CompanyLunaNo ratings yet

- RiskManagementExaminationManaul 08 AntiMoneyLaunderingDocument15 pagesRiskManagementExaminationManaul 08 AntiMoneyLaunderinglphouneNo ratings yet

- Cash Card Terms and Conditions PDFDocument4 pagesCash Card Terms and Conditions PDFJoann BasirgoNo ratings yet

- Equifax - Canadian Income PredictorDocument2 pagesEquifax - Canadian Income PredictorANDREW SAMPSONNo ratings yet

- MarketPeak Academy Business Model-Feb 2022Document49 pagesMarketPeak Academy Business Model-Feb 2022Upendra YadavNo ratings yet

- Money Laundering Regulation and Risk Based Decision-MakingDocument6 pagesMoney Laundering Regulation and Risk Based Decision-MakingAmeer ShafiqNo ratings yet

- LOAN AGREEMENT ("Loan Agreement") : IsclaimerDocument12 pagesLOAN AGREEMENT ("Loan Agreement") : IsclaimerSurendhar SurendharNo ratings yet

- Apollo TyresDocument330 pagesApollo TyresReTHINK INDIANo ratings yet

- Bid Response DocumentDocument27 pagesBid Response DocumentAPEX ENGINEERING CONSULTANCYNo ratings yet

- RHB Product TC Personal FinancingDocument17 pagesRHB Product TC Personal FinancingDon LotNo ratings yet

- Strategic Analysis Brief - Money Laundering Through Real Estate 2015 - AUSTRACDocument6 pagesStrategic Analysis Brief - Money Laundering Through Real Estate 2015 - AUSTRACFilip FIlipsNo ratings yet

- SOP For Merchants On Self Onboarding To UCO Bank Merchant PlatformDocument6 pagesSOP For Merchants On Self Onboarding To UCO Bank Merchant Platformaashu kashyapNo ratings yet

- Bajaj Allianz General Insurance Company LimitedDocument11 pagesBajaj Allianz General Insurance Company LimitedArvind Jadhav100% (1)

- Standard Form of Rental AgreementDocument5 pagesStandard Form of Rental AgreementJane NguyenNo ratings yet

- Caoile EFT Authorization Form - EnglishDocument2 pagesCaoile EFT Authorization Form - EnglishSaki DacaraNo ratings yet

- Terms of Use MTVDocument9 pagesTerms of Use MTVjohnNo ratings yet

- Payment Application Form: Applicant'S ParticularsDocument2 pagesPayment Application Form: Applicant'S ParticularsVijay PuramNo ratings yet

- Capital Markets Partner Guide 09Document56 pagesCapital Markets Partner Guide 09Kumar PriyeshNo ratings yet

- WK Report OTC148 ZVCC1 Credit Card Authorization ReportDocument19 pagesWK Report OTC148 ZVCC1 Credit Card Authorization ReportChaitanya ParamkusamNo ratings yet

- Application DocumentsDocument65 pagesApplication DocumentsNone None NoneNo ratings yet

- HR Generic Payroll Mergers and Acquisitions Checklist Rev 09 08Document11 pagesHR Generic Payroll Mergers and Acquisitions Checklist Rev 09 08claokerNo ratings yet

- PLDT Tarlac 1Document4 pagesPLDT Tarlac 1ann camposNo ratings yet

- Me LINKSDocument5 pagesMe LINKSShaheen ShaikNo ratings yet

- Grant Thornton Kenya FastfactsDocument2 pagesGrant Thornton Kenya FastfactsJay PatelNo ratings yet

- Satrix ETF Form 2 Additional Investments (Lump Sums Only) Aug 2013 - Listing DocumentsDocument5 pagesSatrix ETF Form 2 Additional Investments (Lump Sums Only) Aug 2013 - Listing Documents0796105632No ratings yet

- My Bank StatementDocument3 pagesMy Bank StatementhanhNo ratings yet

- Have LlsDocument428 pagesHave LlsGagandeep SinghNo ratings yet

- Loan Agreement: Parties PartyDocument5 pagesLoan Agreement: Parties PartyNurseklistaNo ratings yet

- Visa Core RulesDocument915 pagesVisa Core RulesJoachim Jørgensen100% (1)

- PDFsam BankDocument1 pagePDFsam BanksMileNo ratings yet

- Know Your Client and Anti-Money Laundering Questionnaire: Bank of Taiwan South Africa BranchDocument8 pagesKnow Your Client and Anti-Money Laundering Questionnaire: Bank of Taiwan South Africa BranchJagadeesh H JaganNo ratings yet

- AML CDD CFT Policy PDFDocument34 pagesAML CDD CFT Policy PDFOwais AhmedNo ratings yet

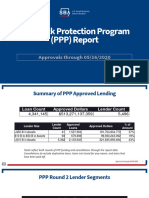

- PPP ReportDocument7 pagesPPP ReportBrittany EtheridgeNo ratings yet

- AML Template 5983002Document58 pagesAML Template 5983002Strategy GameNo ratings yet

- Bank Annual ReportDocument386 pagesBank Annual ReportumeshNo ratings yet

- Crb84a5dddid2474989 BorrowerDocument13 pagesCrb84a5dddid2474989 BorrowerKaran SharmaNo ratings yet

- Application No.:: SEBI / IRDA Registration NO.Document24 pagesApplication No.:: SEBI / IRDA Registration NO.Mohd MizanNo ratings yet

- Companies Act - Formation of Company & PromotionDocument28 pagesCompanies Act - Formation of Company & PromotionRISHI CHANDAKNo ratings yet

- PDFDocument2 pagesPDFVinod kumar yadavNo ratings yet

- HSBC Bank ReportDocument16 pagesHSBC Bank ReportAhsan ButtNo ratings yet

- Annual Report 2076-2077Document196 pagesAnnual Report 2076-2077Mandeep BashisthaNo ratings yet

- A Project Report On A Comparitive Analysis of Different Product and Marketing Strategies of Kotak Mahindra Bank W.R.T Other BanksDocument112 pagesA Project Report On A Comparitive Analysis of Different Product and Marketing Strategies of Kotak Mahindra Bank W.R.T Other BanksNishaAroraNo ratings yet

- PD Digital Currency v.14 14.12.17Document51 pagesPD Digital Currency v.14 14.12.17Li ZhenNo ratings yet

- Courier Service Agr2Document5 pagesCourier Service Agr2Roy PersonalNo ratings yet

- Truist Ach FormDocument1 pageTruist Ach FormhugstinsNo ratings yet

- CA - ITPAM - Quick Start GuideDocument21 pagesCA - ITPAM - Quick Start GuideDaniel LazaratosNo ratings yet

- More - Info - Purchase - House - D5 - 11062014Document7 pagesMore - Info - Purchase - House - D5 - 11062014sambasivammeNo ratings yet

- Anti Money Laundering Policy 2016-17Document30 pagesAnti Money Laundering Policy 2016-17nagallanraoNo ratings yet

- Standard Guidelines On Anti-Money LaundringDocument28 pagesStandard Guidelines On Anti-Money Laundringplanet_ocho7472100% (1)

- PDFFile5b28c97d06d877 47667992Document158 pagesPDFFile5b28c97d06d877 47667992nidhi UnnikrishnanNo ratings yet

- Shreyas DM ProfileDocument1 pageShreyas DM ProfilepranavNo ratings yet

- Digaf Mfi ProfileDocument18 pagesDigaf Mfi ProfileEtsegenet MelkamuNo ratings yet

- Introduction To RiskDocument16 pagesIntroduction To RiskMd Daud HossianNo ratings yet

- Trojan Nickel Mine Contract Engines 2019Document13 pagesTrojan Nickel Mine Contract Engines 2019Hebert SozinyuNo ratings yet

- Taxation LawDocument7 pagesTaxation LawAliNo ratings yet

- ch18 Derivatives and Risk ManagementDocument32 pagesch18 Derivatives and Risk ManagementGonzalo Jr. RualesNo ratings yet

- List of Countries and Capitals With Currency and LanguageDocument36 pagesList of Countries and Capitals With Currency and LanguageGaby López MoguelNo ratings yet

- Critical Analysis of Retail Banking of Indusind Bank: A ProjectDocument9 pagesCritical Analysis of Retail Banking of Indusind Bank: A ProjectPRASANNA GURAVNo ratings yet

- Reading Practice 6Document2 pagesReading Practice 6Doaa AhmedNo ratings yet

- Assignment 1Document8 pagesAssignment 1Nguyễn QuỳnhNo ratings yet

- JIS School FeesDocument4 pagesJIS School FeesAgnesNo ratings yet

- International Tuition Fees: Macquarie Business SchoolDocument7 pagesInternational Tuition Fees: Macquarie Business Schoolarjon ahmedNo ratings yet

- Resume - Huzaifa Khan (P)Document1 pageResume - Huzaifa Khan (P)Huzaifa KhanNo ratings yet

- Cost Accounting Revision QuestionsDocument3 pagesCost Accounting Revision QuestionsMutambu MwetaNo ratings yet

- Valenzuela Vs CA, December 22, 1998Document2 pagesValenzuela Vs CA, December 22, 1998Kim Arniño100% (1)

- Supervisory Policy Manual: TM-E-1 Risk Management of E-BankingDocument37 pagesSupervisory Policy Manual: TM-E-1 Risk Management of E-Bankinglky.hkhcsNo ratings yet

- Understanding Lump SumDocument2 pagesUnderstanding Lump SumYhamNo ratings yet

- Market Research On Cause of Client DropoutDocument25 pagesMarket Research On Cause of Client Dropouthailu letaNo ratings yet

- The FTS Orange Book (NGO & Related Contacts in Durban)Document21 pagesThe FTS Orange Book (NGO & Related Contacts in Durban)Feeding_the_SelfNo ratings yet

- Ecb - Mepletter201119 Urtasun E834423206.en PDFDocument3 pagesEcb - Mepletter201119 Urtasun E834423206.en PDFgrobbebolNo ratings yet

- Aris Nicholas-Resume-No Contact-Cybersecurity-Network Services-April 2023Document4 pagesAris Nicholas-Resume-No Contact-Cybersecurity-Network Services-April 2023api-654754384No ratings yet

- Potential Negative Effects in A Cashless Society 17pg.Document17 pagesPotential Negative Effects in A Cashless Society 17pg.mannysteveNo ratings yet

- Unit 8: Accounting For Spoilage, Reworked Units and Scrap ContentDocument26 pagesUnit 8: Accounting For Spoilage, Reworked Units and Scrap Contentዝምታ ተሻለ0% (1)

- Cqi ToolsDocument4 pagesCqi ToolsChilufya MulopaNo ratings yet

- To All Pharmacy Institutions Approved U/s 12 of The Pharmacy ActDocument9 pagesTo All Pharmacy Institutions Approved U/s 12 of The Pharmacy ActYorest CapsulesNo ratings yet

- Bowes ExploringInnovationinHousing 2018CFRDocument97 pagesBowes ExploringInnovationinHousing 2018CFRCecil SolomonNo ratings yet

- Integrated Logistics SupportDocument9 pagesIntegrated Logistics SupportCasa Permai Guest HouseNo ratings yet

Download as pdf or txt

You might also like

- Ruben Pater - CAPS LOCK-Valiz (2021)Document556 pagesRuben Pater - CAPS LOCK-Valiz (2021)Paulina Escobar AguirreNo ratings yet

- Yes Msme Sole Proprietor DeclarationDocument2 pagesYes Msme Sole Proprietor DeclarationSuraj SinghNo ratings yet

- SaaS Metrics Dashboard TemplateDocument12 pagesSaaS Metrics Dashboard TemplateMartin NelNo ratings yet

- Manual For A Toy Library PDFDocument21 pagesManual For A Toy Library PDFrabbitfootnintendo100% (1)

- ATM & Card Statistics For March 2018 POS AtmsDocument6 pagesATM & Card Statistics For March 2018 POS AtmsMathews KunnekkadanNo ratings yet

- ENTREPRENEURSHIP BY SPIRIT: How to Become a Dynamic and Fantastic EntrepreneurFrom EverandENTREPRENEURSHIP BY SPIRIT: How to Become a Dynamic and Fantastic EntrepreneurNo ratings yet

- AML and KYCDocument2 pagesAML and KYCRahulNo ratings yet

- Licensing HandbookDocument88 pagesLicensing HandbookajoiNo ratings yet

- Anti-Money Launder - AML-CFT Guide BI 260218 With LetterDocument3 pagesAnti-Money Launder - AML-CFT Guide BI 260218 With LetterLc KohNo ratings yet

- Microfinance 3.0Document207 pagesMicrofinance 3.0shannenNo ratings yet

- PMLA PolicyDocument36 pagesPMLA PolicySatwant singhNo ratings yet

- Kyc Aml Policy Revised DT 24.06.21 Updated Upto 10.05.2021Document98 pagesKyc Aml Policy Revised DT 24.06.21 Updated Upto 10.05.2021Priya dharshanNo ratings yet

- Facts About GamblingDocument2 pagesFacts About GamblingJohn Partridge100% (1)

- W1&2 Features of Public Listed Company and Multinational CompanyDocument9 pagesW1&2 Features of Public Listed Company and Multinational CompanyLunaNo ratings yet

- RiskManagementExaminationManaul 08 AntiMoneyLaunderingDocument15 pagesRiskManagementExaminationManaul 08 AntiMoneyLaunderinglphouneNo ratings yet

- Cash Card Terms and Conditions PDFDocument4 pagesCash Card Terms and Conditions PDFJoann BasirgoNo ratings yet

- Equifax - Canadian Income PredictorDocument2 pagesEquifax - Canadian Income PredictorANDREW SAMPSONNo ratings yet

- MarketPeak Academy Business Model-Feb 2022Document49 pagesMarketPeak Academy Business Model-Feb 2022Upendra YadavNo ratings yet

- Money Laundering Regulation and Risk Based Decision-MakingDocument6 pagesMoney Laundering Regulation and Risk Based Decision-MakingAmeer ShafiqNo ratings yet

- LOAN AGREEMENT ("Loan Agreement") : IsclaimerDocument12 pagesLOAN AGREEMENT ("Loan Agreement") : IsclaimerSurendhar SurendharNo ratings yet

- Apollo TyresDocument330 pagesApollo TyresReTHINK INDIANo ratings yet

- Bid Response DocumentDocument27 pagesBid Response DocumentAPEX ENGINEERING CONSULTANCYNo ratings yet

- RHB Product TC Personal FinancingDocument17 pagesRHB Product TC Personal FinancingDon LotNo ratings yet

- Strategic Analysis Brief - Money Laundering Through Real Estate 2015 - AUSTRACDocument6 pagesStrategic Analysis Brief - Money Laundering Through Real Estate 2015 - AUSTRACFilip FIlipsNo ratings yet

- SOP For Merchants On Self Onboarding To UCO Bank Merchant PlatformDocument6 pagesSOP For Merchants On Self Onboarding To UCO Bank Merchant Platformaashu kashyapNo ratings yet

- Bajaj Allianz General Insurance Company LimitedDocument11 pagesBajaj Allianz General Insurance Company LimitedArvind Jadhav100% (1)

- Standard Form of Rental AgreementDocument5 pagesStandard Form of Rental AgreementJane NguyenNo ratings yet

- Caoile EFT Authorization Form - EnglishDocument2 pagesCaoile EFT Authorization Form - EnglishSaki DacaraNo ratings yet

- Terms of Use MTVDocument9 pagesTerms of Use MTVjohnNo ratings yet

- Payment Application Form: Applicant'S ParticularsDocument2 pagesPayment Application Form: Applicant'S ParticularsVijay PuramNo ratings yet

- Capital Markets Partner Guide 09Document56 pagesCapital Markets Partner Guide 09Kumar PriyeshNo ratings yet

- WK Report OTC148 ZVCC1 Credit Card Authorization ReportDocument19 pagesWK Report OTC148 ZVCC1 Credit Card Authorization ReportChaitanya ParamkusamNo ratings yet

- Application DocumentsDocument65 pagesApplication DocumentsNone None NoneNo ratings yet

- HR Generic Payroll Mergers and Acquisitions Checklist Rev 09 08Document11 pagesHR Generic Payroll Mergers and Acquisitions Checklist Rev 09 08claokerNo ratings yet

- PLDT Tarlac 1Document4 pagesPLDT Tarlac 1ann camposNo ratings yet

- Me LINKSDocument5 pagesMe LINKSShaheen ShaikNo ratings yet

- Grant Thornton Kenya FastfactsDocument2 pagesGrant Thornton Kenya FastfactsJay PatelNo ratings yet

- Satrix ETF Form 2 Additional Investments (Lump Sums Only) Aug 2013 - Listing DocumentsDocument5 pagesSatrix ETF Form 2 Additional Investments (Lump Sums Only) Aug 2013 - Listing Documents0796105632No ratings yet

- My Bank StatementDocument3 pagesMy Bank StatementhanhNo ratings yet

- Have LlsDocument428 pagesHave LlsGagandeep SinghNo ratings yet

- Loan Agreement: Parties PartyDocument5 pagesLoan Agreement: Parties PartyNurseklistaNo ratings yet

- Visa Core RulesDocument915 pagesVisa Core RulesJoachim Jørgensen100% (1)

- PDFsam BankDocument1 pagePDFsam BanksMileNo ratings yet

- Know Your Client and Anti-Money Laundering Questionnaire: Bank of Taiwan South Africa BranchDocument8 pagesKnow Your Client and Anti-Money Laundering Questionnaire: Bank of Taiwan South Africa BranchJagadeesh H JaganNo ratings yet

- AML CDD CFT Policy PDFDocument34 pagesAML CDD CFT Policy PDFOwais AhmedNo ratings yet

- PPP ReportDocument7 pagesPPP ReportBrittany EtheridgeNo ratings yet

- AML Template 5983002Document58 pagesAML Template 5983002Strategy GameNo ratings yet

- Bank Annual ReportDocument386 pagesBank Annual ReportumeshNo ratings yet

- Crb84a5dddid2474989 BorrowerDocument13 pagesCrb84a5dddid2474989 BorrowerKaran SharmaNo ratings yet

- Application No.:: SEBI / IRDA Registration NO.Document24 pagesApplication No.:: SEBI / IRDA Registration NO.Mohd MizanNo ratings yet

- Companies Act - Formation of Company & PromotionDocument28 pagesCompanies Act - Formation of Company & PromotionRISHI CHANDAKNo ratings yet

- PDFDocument2 pagesPDFVinod kumar yadavNo ratings yet

- HSBC Bank ReportDocument16 pagesHSBC Bank ReportAhsan ButtNo ratings yet

- Annual Report 2076-2077Document196 pagesAnnual Report 2076-2077Mandeep BashisthaNo ratings yet

- A Project Report On A Comparitive Analysis of Different Product and Marketing Strategies of Kotak Mahindra Bank W.R.T Other BanksDocument112 pagesA Project Report On A Comparitive Analysis of Different Product and Marketing Strategies of Kotak Mahindra Bank W.R.T Other BanksNishaAroraNo ratings yet

- PD Digital Currency v.14 14.12.17Document51 pagesPD Digital Currency v.14 14.12.17Li ZhenNo ratings yet

- Courier Service Agr2Document5 pagesCourier Service Agr2Roy PersonalNo ratings yet

- Truist Ach FormDocument1 pageTruist Ach FormhugstinsNo ratings yet

- CA - ITPAM - Quick Start GuideDocument21 pagesCA - ITPAM - Quick Start GuideDaniel LazaratosNo ratings yet

- More - Info - Purchase - House - D5 - 11062014Document7 pagesMore - Info - Purchase - House - D5 - 11062014sambasivammeNo ratings yet

- Anti Money Laundering Policy 2016-17Document30 pagesAnti Money Laundering Policy 2016-17nagallanraoNo ratings yet

- Standard Guidelines On Anti-Money LaundringDocument28 pagesStandard Guidelines On Anti-Money Laundringplanet_ocho7472100% (1)

- PDFFile5b28c97d06d877 47667992Document158 pagesPDFFile5b28c97d06d877 47667992nidhi UnnikrishnanNo ratings yet

- Shreyas DM ProfileDocument1 pageShreyas DM ProfilepranavNo ratings yet

- Digaf Mfi ProfileDocument18 pagesDigaf Mfi ProfileEtsegenet MelkamuNo ratings yet

- Introduction To RiskDocument16 pagesIntroduction To RiskMd Daud HossianNo ratings yet

- Trojan Nickel Mine Contract Engines 2019Document13 pagesTrojan Nickel Mine Contract Engines 2019Hebert SozinyuNo ratings yet

- Taxation LawDocument7 pagesTaxation LawAliNo ratings yet

- ch18 Derivatives and Risk ManagementDocument32 pagesch18 Derivatives and Risk ManagementGonzalo Jr. RualesNo ratings yet

- List of Countries and Capitals With Currency and LanguageDocument36 pagesList of Countries and Capitals With Currency and LanguageGaby López MoguelNo ratings yet

- Critical Analysis of Retail Banking of Indusind Bank: A ProjectDocument9 pagesCritical Analysis of Retail Banking of Indusind Bank: A ProjectPRASANNA GURAVNo ratings yet

- Reading Practice 6Document2 pagesReading Practice 6Doaa AhmedNo ratings yet

- Assignment 1Document8 pagesAssignment 1Nguyễn QuỳnhNo ratings yet

- JIS School FeesDocument4 pagesJIS School FeesAgnesNo ratings yet

- International Tuition Fees: Macquarie Business SchoolDocument7 pagesInternational Tuition Fees: Macquarie Business Schoolarjon ahmedNo ratings yet

- Resume - Huzaifa Khan (P)Document1 pageResume - Huzaifa Khan (P)Huzaifa KhanNo ratings yet

- Cost Accounting Revision QuestionsDocument3 pagesCost Accounting Revision QuestionsMutambu MwetaNo ratings yet

- Valenzuela Vs CA, December 22, 1998Document2 pagesValenzuela Vs CA, December 22, 1998Kim Arniño100% (1)

- Supervisory Policy Manual: TM-E-1 Risk Management of E-BankingDocument37 pagesSupervisory Policy Manual: TM-E-1 Risk Management of E-Bankinglky.hkhcsNo ratings yet

- Understanding Lump SumDocument2 pagesUnderstanding Lump SumYhamNo ratings yet

- Market Research On Cause of Client DropoutDocument25 pagesMarket Research On Cause of Client Dropouthailu letaNo ratings yet

- The FTS Orange Book (NGO & Related Contacts in Durban)Document21 pagesThe FTS Orange Book (NGO & Related Contacts in Durban)Feeding_the_SelfNo ratings yet

- Ecb - Mepletter201119 Urtasun E834423206.en PDFDocument3 pagesEcb - Mepletter201119 Urtasun E834423206.en PDFgrobbebolNo ratings yet

- Aris Nicholas-Resume-No Contact-Cybersecurity-Network Services-April 2023Document4 pagesAris Nicholas-Resume-No Contact-Cybersecurity-Network Services-April 2023api-654754384No ratings yet

- Potential Negative Effects in A Cashless Society 17pg.Document17 pagesPotential Negative Effects in A Cashless Society 17pg.mannysteveNo ratings yet

- Unit 8: Accounting For Spoilage, Reworked Units and Scrap ContentDocument26 pagesUnit 8: Accounting For Spoilage, Reworked Units and Scrap Contentዝምታ ተሻለ0% (1)

- Cqi ToolsDocument4 pagesCqi ToolsChilufya MulopaNo ratings yet

- To All Pharmacy Institutions Approved U/s 12 of The Pharmacy ActDocument9 pagesTo All Pharmacy Institutions Approved U/s 12 of The Pharmacy ActYorest CapsulesNo ratings yet

- Bowes ExploringInnovationinHousing 2018CFRDocument97 pagesBowes ExploringInnovationinHousing 2018CFRCecil SolomonNo ratings yet

- Integrated Logistics SupportDocument9 pagesIntegrated Logistics SupportCasa Permai Guest HouseNo ratings yet