Download as docx, pdf, or txt

You might also like

- IFRS Simplified: A fast and easy-to-understand overview of the new International Financial Reporting StandardsFrom EverandIFRS Simplified: A fast and easy-to-understand overview of the new International Financial Reporting StandardsRating: 4 out of 5 stars4/5 (11)

- How To Adjusted BalanceDocument4 pagesHow To Adjusted BalanceAnya Daniella80% (5)

- Ais Problem 2.2Document21 pagesAis Problem 2.2Md Rifat Motaleb100% (1)

- 21day Studyplan For LLQP ExamDocument9 pages21day Studyplan For LLQP ExamMatthew ChambersNo ratings yet

- The Accounting Policies Regarding The Fixed Assets Between The Omfp 1802/2014 and The Ias-IfrsDocument6 pagesThe Accounting Policies Regarding The Fixed Assets Between The Omfp 1802/2014 and The Ias-IfrsRoxana MarilenaNo ratings yet

- International Financial Reporting Standards A PreDocument10 pagesInternational Financial Reporting Standards A Preadmid aisyahNo ratings yet

- European Accounting Harmonisation: Consequences of IFRS Adoption On Trade in Goods and Foreign Direct InvestmentsDocument31 pagesEuropean Accounting Harmonisation: Consequences of IFRS Adoption On Trade in Goods and Foreign Direct Investmentsakash mahmudNo ratings yet

- Comparability and Reliability of Financial Information in The Sector of Czech SMES (Ten Years of IFRS As A Part of Czech Accounting Context)Document14 pagesComparability and Reliability of Financial Information in The Sector of Czech SMES (Ten Years of IFRS As A Part of Czech Accounting Context)Minh PhuongNo ratings yet

- Article1380541325 - Mihai Et AlDocument6 pagesArticle1380541325 - Mihai Et Alstudentul1986No ratings yet

- An Analysis of The Convergence Level of Tangible Assets (Ppe) According To Romanian National Accounting Regulation and Ifrs For SmesDocument26 pagesAn Analysis of The Convergence Level of Tangible Assets (Ppe) According To Romanian National Accounting Regulation and Ifrs For SmesRoxana MarilenaNo ratings yet

- Shsconf Glob20 02039Document9 pagesShsconf Glob20 02039GaborViriNo ratings yet

- Need For Harmonisation As A Reason For International Differences in Financial ReportingDocument4 pagesNeed For Harmonisation As A Reason For International Differences in Financial ReportingSasha KingNo ratings yet

- Multinational InfluenceDocument14 pagesMultinational InfluenceVitalie MihailovNo ratings yet

- The Evolution of The Limitation of The Application of The Accounts Function by Romanian CompaniesDocument10 pagesThe Evolution of The Limitation of The Application of The Accounts Function by Romanian CompaniesLucia Morosan-DanilaNo ratings yet

- Ne Gash 2012Document20 pagesNe Gash 2012Fenny MarietzaNo ratings yet

- Workin Working Paper Series Paper SeriesDocument28 pagesWorkin Working Paper Series Paper Seriessandeep_singh90No ratings yet

- OECONOMICA The IASB and FASB Convergence PDFDocument23 pagesOECONOMICA The IASB and FASB Convergence PDFmansoor mahmoodNo ratings yet

- Accounting Rules in MacedoniaDocument1 pageAccounting Rules in MacedoniaZiko_66No ratings yet

- Stephen Das A 4022183 Research Proposal-IfRSDocument25 pagesStephen Das A 4022183 Research Proposal-IfRSStephen Das100% (1)

- (FINAL) Int Accounting - The Application of IFRS in Practice (BW) - 1Document14 pages(FINAL) Int Accounting - The Application of IFRS in Practice (BW) - 1Pascu ElenaNo ratings yet

- 1 Adoption - of - IFRS - Spain PDFDocument31 pages1 Adoption - of - IFRS - Spain PDFJULIO CESAR MILLAN SOLARTENo ratings yet

- Accounting Dissertations - IfRSDocument30 pagesAccounting Dissertations - IfRSgappu002No ratings yet

- The Effects of Ifrs On Net Income and Equity Evidence From Romanian Listed CompaniesDocument4 pagesThe Effects of Ifrs On Net Income and Equity Evidence From Romanian Listed CompaniesRantiNo ratings yet

- IFRS Pentru IMMDocument3 pagesIFRS Pentru IMMIonut MiteleaNo ratings yet

- Ipsas AseDocument24 pagesIpsas Aseanne_marryNo ratings yet

- Kiranjot Kaur 2Document27 pagesKiranjot Kaur 2Rupali MalhotraNo ratings yet

- Analysis of The Accounting Systems From Romania and Moldova: AbstractDocument6 pagesAnalysis of The Accounting Systems From Romania and Moldova: AbstractLucia Morosan-DanilaNo ratings yet

- Financial StatementsDocument7 pagesFinancial StatementsJoel BlairNo ratings yet

- 22715-Article Text-89374-1-10-20200727Document12 pages22715-Article Text-89374-1-10-20200727Juan Paolo VentosaNo ratings yet

- Ifrs AssignmentDocument13 pagesIfrs Assignmentarijit nathNo ratings yet

- 10.1007@978 3 319 28225 127Document12 pages10.1007@978 3 319 28225 127Denisa GrădinaruNo ratings yet

- Master Thesis PP88092Document70 pagesMaster Thesis PP88092Aeson Dela CruzNo ratings yet

- Ebook Introduction To IFRSDocument21 pagesEbook Introduction To IFRSNadarajanNo ratings yet

- Accounting and AuditingDocument3 pagesAccounting and AuditingMarc AurelioNo ratings yet

- The Need For Financial Statements To Disclose TrueDocument9 pagesThe Need For Financial Statements To Disclose TruesutriNo ratings yet

- IFRS Adoption in Roman Information Nia: The Effects Upon Financial and Its RelevanceDocument6 pagesIFRS Adoption in Roman Information Nia: The Effects Upon Financial and Its RelevanceAura MihaelaNo ratings yet

- MPRA Paper 18279Document32 pagesMPRA Paper 18279christine_andreiNo ratings yet

- Script Topic 1 Fall 2020 IFRSDocument20 pagesScript Topic 1 Fall 2020 IFRSyingqiao.panNo ratings yet

- Audit Reports On Financial Statements Prepared According To IASB Standards: Empirical Evidence From The European UnionDocument27 pagesAudit Reports On Financial Statements Prepared According To IASB Standards: Empirical Evidence From The European UnionSpytersNo ratings yet

- Accounting Standards - Will The World Be Talking The Same Language - Published in CA Journal Feb 2005Document6 pagesAccounting Standards - Will The World Be Talking The Same Language - Published in CA Journal Feb 2005shrikantsubsNo ratings yet

- The Impact of The IAS/IFRS Adoption On The Predictive Quality of Discretionary Accruals: A Comparison Between The French and The British ContextDocument24 pagesThe Impact of The IAS/IFRS Adoption On The Predictive Quality of Discretionary Accruals: A Comparison Between The French and The British ContextAhmadi AliNo ratings yet

- Jurnal IFRSDocument17 pagesJurnal IFRSAdhi PramuditaNo ratings yet

- Auditing Implications of IFRS Transition: Audit 03/04Document18 pagesAuditing Implications of IFRS Transition: Audit 03/04RedaBendimeradNo ratings yet

- Implications of IFRS Adoption On BalanceDocument10 pagesImplications of IFRS Adoption On BalancelogeshthekingNo ratings yet

- E - Content On IFRSDocument20 pagesE - Content On IFRSPranit Satyavan NaikNo ratings yet

- Ejaj Disser (1) (1) HYPODocument36 pagesEjaj Disser (1) (1) HYPOEjajNo ratings yet

- IFRS-Opportunities & Challenges For IndiaDocument5 pagesIFRS-Opportunities & Challenges For IndiaTincy KurianNo ratings yet

- WW5050 Progettoricerca Cordazzo WebDocument1 pageWW5050 Progettoricerca Cordazzo WebGhislaine Umuhoza GakubaNo ratings yet

- The Effect of International Financial Reporting Standards (IFRS) Adoption On The Performance of Firms in NigeriaDocument33 pagesThe Effect of International Financial Reporting Standards (IFRS) Adoption On The Performance of Firms in NigeriaAicha Ben TaherNo ratings yet

- Harmonization and Convergence of StandardsDocument2 pagesHarmonization and Convergence of StandardsSuzette EstiponaNo ratings yet

- SummaryDocument6 pagesSummaryPrinces LaribaNo ratings yet

- Introduction To IFRSDocument13 pagesIntroduction To IFRSgovindsekharNo ratings yet

- Definisi Dan Sejarah IfrsDocument20 pagesDefinisi Dan Sejarah IfrsGinda Rafiel Sitorus PaneNo ratings yet

- 1 s2.0 S1877042813052130 MainDocument7 pages1 s2.0 S1877042813052130 MainSahar FekihNo ratings yet

- Objective: Session 01 - International Financial Reporting StandardsDocument18 pagesObjective: Session 01 - International Financial Reporting StandardsVladlenaAlekseenkoNo ratings yet

- Adam ZakariaDocument28 pagesAdam ZakariaRajipah OsmanNo ratings yet

- AS Dita - IfRS As A Guide To Overcome Challenges in International AccountingDocument9 pagesAS Dita - IfRS As A Guide To Overcome Challenges in International AccountingYor AdeNo ratings yet

- The Convergence To IFRS - Reasons, Implications, Applicability, and ConcernsDocument10 pagesThe Convergence To IFRS - Reasons, Implications, Applicability, and ConcernsRajipah OsmanNo ratings yet

- Chap 003Document5 pagesChap 003phyllis123No ratings yet

- A practical guide to UCITS funds and their risk management: How to invest with securityFrom EverandA practical guide to UCITS funds and their risk management: How to invest with securityNo ratings yet

- Indian Financial SystemDocument5 pagesIndian Financial SystemHimaja GharaiNo ratings yet

- The Philippine Financial SystemDocument39 pagesThe Philippine Financial Systemathena100% (1)

- Procedure Bpu MethodDocument1 pageProcedure Bpu MethodKiki SajaNo ratings yet

- Genuime Company Required 1 Debit CreditDocument15 pagesGenuime Company Required 1 Debit CreditAnonnNo ratings yet

- Simple Financial Plan & Unit Economics - Lead Gen - Template - v3.0 by Future Flow - PUBLICDocument52 pagesSimple Financial Plan & Unit Economics - Lead Gen - Template - v3.0 by Future Flow - PUBLICRaúl GuerreroNo ratings yet

- 7 P'sDocument22 pages7 P'sSravan ErukullaNo ratings yet

- GOVERNMENT AGENCIES ACCEPTING PHILID AND EPHILID (W - Financial Institutions)Document7 pagesGOVERNMENT AGENCIES ACCEPTING PHILID AND EPHILID (W - Financial Institutions)r.penaredondoNo ratings yet

- Saving Cum Salary Account 3Document5 pagesSaving Cum Salary Account 3Ashwani KumarNo ratings yet

- Cartus Receipt GuideDocument4 pagesCartus Receipt Guideilaria zaccagniniNo ratings yet

- 2022 Quiz 2 (Solved)Document3 pages2022 Quiz 2 (Solved)Anshuman GuptaNo ratings yet

- Introduction Sutex BankDocument14 pagesIntroduction Sutex BankRonakNo ratings yet

- Accounting 141 2020Document7 pagesAccounting 141 2020alexcharles433No ratings yet

- Short Questions-Central BankDocument6 pagesShort Questions-Central BanksadNo ratings yet

- HWChapter 5Document20 pagesHWChapter 5Yawar Abbas KhanNo ratings yet

- Name: Address:: Date Account Name Currency Iban Account Number Customer IDDocument3 pagesName: Address:: Date Account Name Currency Iban Account Number Customer IDKhaled HamdyNo ratings yet

- Amla FaqsDocument4 pagesAmla FaqsMaxNo ratings yet

- Xii Mcqs CH - 15 Ratio AnalysisDocument6 pagesXii Mcqs CH - 15 Ratio AnalysisJoanna GarciaNo ratings yet

- Topic 3 - Internal Control System - Part 2-StudentDocument9 pagesTopic 3 - Internal Control System - Part 2-StudentThinh NguyenNo ratings yet

- Economics of Money Banking and Financial Markets Global 10th Edition Mishkin Test BankDocument25 pagesEconomics of Money Banking and Financial Markets Global 10th Edition Mishkin Test BankPeterHolmesfdns100% (59)

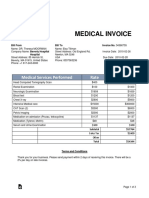

- Medical InvoiceDocument3 pagesMedical InvoiceAditya JagtapNo ratings yet

- Theory of Financial Intermediation. 1.0 History of Financail IntermediariesDocument23 pagesTheory of Financial Intermediation. 1.0 History of Financail IntermediariesAmeh AnyebeNo ratings yet

- AUDITING THEORY Jan 3 2024Document39 pagesAUDITING THEORY Jan 3 2024Jamikka DistalNo ratings yet

- Rights of MortgageeDocument3 pagesRights of Mortgageesahil200768No ratings yet

- Uday KotakDocument11 pagesUday Kotak20UBA501 HARI RAMKUMAR S MNo ratings yet

- Meressa Paper 2021Document24 pagesMeressa Paper 2021Mk FisihaNo ratings yet

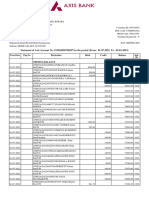

- Statement of Axis Account No:913010028728287 For The Period (From: 01-07-2022 To: 02-01-2023)Document41 pagesStatement of Axis Account No:913010028728287 For The Period (From: 01-07-2022 To: 02-01-2023)Shreshtha Suffix Financial ServicesNo ratings yet

- BankingDocument74 pagesBankingAbhishek DubeyNo ratings yet