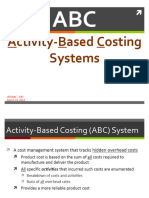

4 Activity Based Costing

4 Activity Based Costing

You might also like

- TAX - Final Pre-Board With Answer Key Batch Exodus - EncryptedDocument16 pagesTAX - Final Pre-Board With Answer Key Batch Exodus - EncryptedSophia Perez100% (1)

- C TB1200 90 Sample QuestionsDocument5 pagesC TB1200 90 Sample QuestionsSébastien MichelNo ratings yet

- Thomas & Ely (1996) - "Making Differences Matter: A New Paradigm For Managing Diversity," Harvard Business ReviewDocument2 pagesThomas & Ely (1996) - "Making Differences Matter: A New Paradigm For Managing Diversity," Harvard Business ReviewEdison Bitencourt de Almeida100% (1)

- Garrison Lecture Chapter 7Document64 pagesGarrison Lecture Chapter 7Enelyn Rose GigtintaNo ratings yet

- CH 6 Activity Based CostingDocument15 pagesCH 6 Activity Based CostingAmit SawantNo ratings yet

- Hilton Chapter 5 Adobe Connect Activity-Based Costing and ManagementDocument11 pagesHilton Chapter 5 Adobe Connect Activity-Based Costing and ManagementyosepjoltNo ratings yet

- Learning ObjectivesDocument3 pagesLearning ObjectivesAngel Margarette BelenNo ratings yet

- Including: Chapter 8 (Appendix)Document48 pagesIncluding: Chapter 8 (Appendix)Tiến DũngNo ratings yet

- Chapter 5 Activity Based Costing & Activity Based ManagementDocument5 pagesChapter 5 Activity Based Costing & Activity Based ManagementOyuNo ratings yet

- Unit 2Document8 pagesUnit 2Shikara DumayagNo ratings yet

- Week 6 Lecture SlidesDocument51 pagesWeek 6 Lecture Slidessaba bastiNo ratings yet

- Activity-Based Costing: Mcgraw-Hill/IrwinDocument70 pagesActivity-Based Costing: Mcgraw-Hill/IrwinHadayNo ratings yet

- Management Advisory Services Adb/Jju/Bdt MAS.2814 - Activity-Based Costing System MAY 2020Document2 pagesManagement Advisory Services Adb/Jju/Bdt MAS.2814 - Activity-Based Costing System MAY 2020Donny TrumpNo ratings yet

- Week Four: Costing SystemsDocument4 pagesWeek Four: Costing SystemsNizam JewelNo ratings yet

- Smac Cheatsheet 2Document2 pagesSmac Cheatsheet 2Dries VanvoorenNo ratings yet

- Activity Based CostingDocument31 pagesActivity Based Costingwww.nickpicsplusNo ratings yet

- Group 4 - Cost AccountingDocument26 pagesGroup 4 - Cost Accounting20 Đặng Kiều Hoài PhươngNo ratings yet

- Lanen - Fundamentals of Cost Accounting - 6e - Chapter 9 - NotesDocument3 pagesLanen - Fundamentals of Cost Accounting - 6e - Chapter 9 - NotesRorNo ratings yet

- Activity Based CostingDocument12 pagesActivity Based CostingMuhammad Imran AwanNo ratings yet

- Review Chapter 1-2-4-18Document55 pagesReview Chapter 1-2-4-18hoangmyduyennguyen2004No ratings yet

- BA 116 / 1 Semester, AY 2013-2014 Activity-Based Costing (ABC) Systems: Handout #7Document2 pagesBA 116 / 1 Semester, AY 2013-2014 Activity-Based Costing (ABC) Systems: Handout #7Becky GonzagaNo ratings yet

- Activity-Based Costing and Management: Mcgraw-Hill/IrwinDocument41 pagesActivity-Based Costing and Management: Mcgraw-Hill/IrwinTruyện ĐọcNo ratings yet

- Chapter Three PDFDocument33 pagesChapter Three PDFSum AïyahNo ratings yet

- ACC2706 / ACC2002 Management Accounting Semester II, AY 2020/21Document51 pagesACC2706 / ACC2002 Management Accounting Semester II, AY 2020/21avNo ratings yet

- MS 3413 Activity-Based Costing SystemDocument5 pagesMS 3413 Activity-Based Costing SystemMonica GarciaNo ratings yet

- w5 ABC ShortDocument26 pagesw5 ABC ShortEugene TeoNo ratings yet

- Activity Based Costing - UNAMDocument32 pagesActivity Based Costing - UNAMWilhelmina KandjekeNo ratings yet

- Session - 5&6: Activity-Based Costing: PGP 2022-24 Prof. M. Shameem JawedDocument26 pagesSession - 5&6: Activity-Based Costing: PGP 2022-24 Prof. M. Shameem JawedAnkitShettyNo ratings yet

- Activity-Based CostingDocument49 pagesActivity-Based CostingJene LmNo ratings yet

- Knowing The Root Causes of Activity Costs Is The Key To Improvement of Cost Efficiency and InnovationDocument1 pageKnowing The Root Causes of Activity Costs Is The Key To Improvement of Cost Efficiency and InnovationJelay QuilatanNo ratings yet

- Brewer 8e PPT Ch04 TDocument36 pagesBrewer 8e PPT Ch04 TJuan Camilo IdarragaNo ratings yet

- Activity-Based Costing: Better Costing For Better DecisionsDocument25 pagesActivity-Based Costing: Better Costing For Better DecisionsArun KCNo ratings yet

- ABC CostingDocument35 pagesABC CostingShivangi JhawarNo ratings yet

- Costing Textbook CADocument294 pagesCosting Textbook CAAryan RajNo ratings yet

- Activity Based CostingDocument30 pagesActivity Based CostingGwenn VillamorNo ratings yet

- Activity Based CostingDocument36 pagesActivity Based CostingRashmeet Arora100% (1)

- Lesson ABCDocument15 pagesLesson ABCCj GarciaNo ratings yet

- ABC Costing PDFDocument33 pagesABC Costing PDFDrpranav SaraswatNo ratings yet

- Systems Design: Activity-Based Costing and Management: MANAGEMENT ACCOUNTING-Solutions ManualDocument15 pagesSystems Design: Activity-Based Costing and Management: MANAGEMENT ACCOUNTING-Solutions ManualBianca LizardoNo ratings yet

- Chapter Five: Activity-Based Costing (ABC) and Activity-Based Management (ABM)Document38 pagesChapter Five: Activity-Based Costing (ABC) and Activity-Based Management (ABM)Rangga PurnaNo ratings yet

- Activity-Based CostingDocument59 pagesActivity-Based CostinghanaNo ratings yet

- Activity-Based Costing: Better Costing For Better DecisionsDocument22 pagesActivity-Based Costing: Better Costing For Better DecisionsHasleen KaurNo ratings yet

- Activity Based CostingDocument4 pagesActivity Based CostingMaria Via Cristian MauricioNo ratings yet

- Chapter 5 Activity Based Costing - DO-unlockedDocument49 pagesChapter 5 Activity Based Costing - DO-unlockedtirupati phutelaNo ratings yet

- 10632m Lecture 6 - Full Costing I (Full Version)Document53 pages10632m Lecture 6 - Full Costing I (Full Version)kammiefan215No ratings yet

- Module Week 2b Acctg16Document18 pagesModule Week 2b Acctg16Andrea Florence Guy VidalNo ratings yet

- Activity-Based Costing: Questions For Writing and DiscussionDocument42 pagesActivity-Based Costing: Questions For Writing and DiscussionMaria Sarah SantosNo ratings yet

- Lecture 2Document22 pagesLecture 2An Nguyen Thai HongNo ratings yet

- ABC SystemsDocument15 pagesABC SystemsChristian TanNo ratings yet

- Cost Concepts HandoutDocument5 pagesCost Concepts HandoutNovilyn LeonardoNo ratings yet

- Cost Management Systems and Activity-Based Costing: Learning ObjectivesDocument15 pagesCost Management Systems and Activity-Based Costing: Learning ObjectivesIsaac Samy IsaacNo ratings yet

- Unit 9 Activity Based CostingDocument32 pagesUnit 9 Activity Based CostingjayitadebangiNo ratings yet

- Activity Based CostingDocument30 pagesActivity Based Costinghardik1302No ratings yet

- ABC CostingDocument39 pagesABC Costingtyagiaanya101No ratings yet

- Activity Based CostingDocument17 pagesActivity Based Costingvinati100% (2)

- Topic 2: Managing Costs - Activity-Based Costing ("ABC") : ACCT2522 Management Accounting For Decision AnalysisDocument58 pagesTopic 2: Managing Costs - Activity-Based Costing ("ABC") : ACCT2522 Management Accounting For Decision AnalysisFreda DengNo ratings yet

- ACTIVITY BASED COSTINGDocument58 pagesACTIVITY BASED COSTINGvangoorihome2No ratings yet

- Machine Setup: Activity-Based CostingDocument40 pagesMachine Setup: Activity-Based CostingJayson TasarraNo ratings yet

- Activity Based Costing (ABC)Document43 pagesActivity Based Costing (ABC)Snn News TubeNo ratings yet

- Overhead Costing and Activity Based Costing (W)Document11 pagesOverhead Costing and Activity Based Costing (W)Muhammad NaeemNo ratings yet

- Cost Management SystemDocument12 pagesCost Management SystemdianaNo ratings yet

- Solution Manual of Chapter 7 Managerial Accounting 15th Edition Ray H Garrison Eric W Noreen and Peter C BrewerDocument55 pagesSolution Manual of Chapter 7 Managerial Accounting 15th Edition Ray H Garrison Eric W Noreen and Peter C BrewerSEHA ÖZTÜRK100% (1)

- 15 Rizals 2nd Sojourn in Paris and The Universal Exposition of 1889Document12 pages15 Rizals 2nd Sojourn in Paris and The Universal Exposition of 1889Febbie Novem LavariasNo ratings yet

- 5 Medical Studies at USTDocument6 pages5 Medical Studies at USTFebbie Novem LavariasNo ratings yet

- 6 in Sunny SpainDocument15 pages6 in Sunny SpainFebbie Novem LavariasNo ratings yet

- 9 Rizals Grand Tour of Europe With Viola (1887)Document11 pages9 Rizals Grand Tour of Europe With Viola (1887)Febbie Novem LavariasNo ratings yet

- 20 Ophthalmic Surgeon in Hong Kong (1891-1892)Document10 pages20 Ophthalmic Surgeon in Hong Kong (1891-1892)Febbie Novem LavariasNo ratings yet

- Ra 1425Document4 pagesRa 1425Febbie Novem LavariasNo ratings yet

- 19 El Fili Published in GhentDocument9 pages19 El Fili Published in GhentFebbie Novem LavariasNo ratings yet

- 21 2nd Homecoming and The Liga FilipinaDocument6 pages21 2nd Homecoming and The Liga FilipinaFebbie Novem LavariasNo ratings yet

- 22 Exile in Dapitan 1892-1896Document13 pages22 Exile in Dapitan 1892-1896Febbie Novem LavariasNo ratings yet

- 17 Misfortunes in Madrid (1890-1891)Document7 pages17 Misfortunes in Madrid (1890-1891)Febbie Novem LavariasNo ratings yet

- 12 Romantic Interlude in JapanDocument8 pages12 Romantic Interlude in JapanFebbie Novem LavariasNo ratings yet

- 14 Rizal in LondonDocument11 pages14 Rizal in LondonFebbie Novem LavariasNo ratings yet

- 16 in Belgian Brussels (1890)Document9 pages16 in Belgian Brussels (1890)Febbie Novem LavariasNo ratings yet

- 1 Managerial Accounting and The Business EnvironmentDocument7 pages1 Managerial Accounting and The Business EnvironmentFebbie Novem LavariasNo ratings yet

- 13 Rizals Visit To The USADocument6 pages13 Rizals Visit To The USAFebbie Novem LavariasNo ratings yet

- Rizal and His Time PrologueDocument4 pagesRizal and His Time PrologueFebbie Novem LavariasNo ratings yet

- 2 Cost Volume Profit RelationshipsDocument34 pages2 Cost Volume Profit RelationshipsFebbie Novem LavariasNo ratings yet

- 4 Scholastic Triumphs at Ateneo de ManilaDocument10 pages4 Scholastic Triumphs at Ateneo de ManilaFebbie Novem LavariasNo ratings yet

- 11 in Hong Kong and MacaoDocument6 pages11 in Hong Kong and MacaoFebbie Novem LavariasNo ratings yet

- 7 Paris To BerlinDocument8 pages7 Paris To BerlinFebbie Novem LavariasNo ratings yet

- 8 Noli Me Tangere Published in BerlinDocument8 pages8 Noli Me Tangere Published in BerlinFebbie Novem LavariasNo ratings yet

- 10 First Homecoming 1887-1888Document12 pages10 First Homecoming 1887-1888Febbie Novem LavariasNo ratings yet

- 7 Standard Costs and VariancesDocument25 pages7 Standard Costs and VariancesFebbie Novem LavariasNo ratings yet

- 8 Performance Measurement in Decentralized OrganizationsDocument3 pages8 Performance Measurement in Decentralized OrganizationsFebbie Novem LavariasNo ratings yet

- 5 Profit PlanningDocument17 pages5 Profit PlanningFebbie Novem LavariasNo ratings yet

- 3 Early Education in Calamba and BinanDocument5 pages3 Early Education in Calamba and BinanFebbie Novem LavariasNo ratings yet

- 3 Variable Costing A Tool For ManagementDocument14 pages3 Variable Costing A Tool For ManagementFebbie Novem LavariasNo ratings yet

- 1 Advent of The National HeroDocument6 pages1 Advent of The National HeroFebbie Novem LavariasNo ratings yet

- 6 Flexible Budgets and Performance AnalysisDocument11 pages6 Flexible Budgets and Performance AnalysisFebbie Novem LavariasNo ratings yet

- A Public Relations ApproachDocument33 pagesA Public Relations Approachmona_13mera7931100% (2)

- Mos QuestionsDocument3 pagesMos QuestionsDurgesh AgnihotriNo ratings yet

- Statemant HSBCDocument1 pageStatemant HSBCVera DedkovskaNo ratings yet

- Barber & Odean - The Internet and The InvestorDocument14 pagesBarber & Odean - The Internet and The Investoronat85No ratings yet

- Basic FormulasDocument1 pageBasic FormulasDhanaperumal VarulaNo ratings yet

- Pricing Analytics: Creating Linear & Power Demand CurvesDocument48 pagesPricing Analytics: Creating Linear & Power Demand CurvesAbhijeetNo ratings yet

- Syllabus CPM DiplomaDocument6 pagesSyllabus CPM DiplomaGirman ranaNo ratings yet

- Impact of Using ICT - Agrani Bank BangladeshDocument37 pagesImpact of Using ICT - Agrani Bank BangladeshshafiulalamchowdhuryNo ratings yet

- Akansha Topani - No ShortcutsDocument3 pagesAkansha Topani - No Shortcutsakansha topaniNo ratings yet

- 1st Module AssessmentfmDocument6 pages1st Module AssessmentfmMansi GuptaNo ratings yet

- Quiz No 22 - TendersDocument5 pagesQuiz No 22 - TenderskanagarajodishaNo ratings yet

- The Success of The "Vive 100"Document2 pagesThe Success of The "Vive 100"JuanPabloJaramilloNo ratings yet

- Paper On VarDocument157 pagesPaper On VarHemendra GuptaNo ratings yet

- KSRMDocument2 pagesKSRMkahamedNo ratings yet

- Marketing Plan - SiantechDocument47 pagesMarketing Plan - SiantechAhmed NasrNo ratings yet

- Maceda Law Realty Installment Buyer Protection Act: Own House CondominiumDocument4 pagesMaceda Law Realty Installment Buyer Protection Act: Own House CondominiumsherwinNo ratings yet

- Macroeconomics EC2065 CHAPTER 6 - MONEY AND MONETARY POLICYDocument54 pagesMacroeconomics EC2065 CHAPTER 6 - MONEY AND MONETARY POLICYkaylaNo ratings yet

- Introduction To Human Resource ManagementDocument5 pagesIntroduction To Human Resource ManagementJe SacdalNo ratings yet

- Foreign Exchange Market: Presentation OnDocument19 pagesForeign Exchange Market: Presentation OnKavya lakshmikanthNo ratings yet

- Maceda Vs Energy Regulatory BoardDocument15 pagesMaceda Vs Energy Regulatory BoardJan Igor GalinatoNo ratings yet

- COMPAÑIA GENERAL DE TABACOS DE FILIPINAS Vs ManilaDocument2 pagesCOMPAÑIA GENERAL DE TABACOS DE FILIPINAS Vs ManilaLau NunezNo ratings yet

- ONGC - Stock Update 240921Document14 pagesONGC - Stock Update 240921Mohit MauryaNo ratings yet

- Bank AuditDocument16 pagesBank AuditThunderHeadNo ratings yet

- Resume 5Document3 pagesResume 5Zahid HussainNo ratings yet

- Unit 4. 21st Century Literacies C. Savings and Banking D. Avoiding Financial Scams I.Introduction / RationaleDocument10 pagesUnit 4. 21st Century Literacies C. Savings and Banking D. Avoiding Financial Scams I.Introduction / RationaleLance AustriaNo ratings yet

- Ax Blog 2Document293 pagesAx Blog 2pjanssen2306No ratings yet

- 304 Ope Som-Mcq-2019Document7 pages304 Ope Som-Mcq-2019Prafull P KulkarniNo ratings yet

Download as pdf or txt

You might also like

- TAX - Final Pre-Board With Answer Key Batch Exodus - EncryptedDocument16 pagesTAX - Final Pre-Board With Answer Key Batch Exodus - EncryptedSophia Perez100% (1)

- C TB1200 90 Sample QuestionsDocument5 pagesC TB1200 90 Sample QuestionsSébastien MichelNo ratings yet

- Thomas & Ely (1996) - "Making Differences Matter: A New Paradigm For Managing Diversity," Harvard Business ReviewDocument2 pagesThomas & Ely (1996) - "Making Differences Matter: A New Paradigm For Managing Diversity," Harvard Business ReviewEdison Bitencourt de Almeida100% (1)

- Garrison Lecture Chapter 7Document64 pagesGarrison Lecture Chapter 7Enelyn Rose GigtintaNo ratings yet

- CH 6 Activity Based CostingDocument15 pagesCH 6 Activity Based CostingAmit SawantNo ratings yet

- Hilton Chapter 5 Adobe Connect Activity-Based Costing and ManagementDocument11 pagesHilton Chapter 5 Adobe Connect Activity-Based Costing and ManagementyosepjoltNo ratings yet

- Learning ObjectivesDocument3 pagesLearning ObjectivesAngel Margarette BelenNo ratings yet

- Including: Chapter 8 (Appendix)Document48 pagesIncluding: Chapter 8 (Appendix)Tiến DũngNo ratings yet

- Chapter 5 Activity Based Costing & Activity Based ManagementDocument5 pagesChapter 5 Activity Based Costing & Activity Based ManagementOyuNo ratings yet

- Unit 2Document8 pagesUnit 2Shikara DumayagNo ratings yet

- Week 6 Lecture SlidesDocument51 pagesWeek 6 Lecture Slidessaba bastiNo ratings yet

- Activity-Based Costing: Mcgraw-Hill/IrwinDocument70 pagesActivity-Based Costing: Mcgraw-Hill/IrwinHadayNo ratings yet

- Management Advisory Services Adb/Jju/Bdt MAS.2814 - Activity-Based Costing System MAY 2020Document2 pagesManagement Advisory Services Adb/Jju/Bdt MAS.2814 - Activity-Based Costing System MAY 2020Donny TrumpNo ratings yet

- Week Four: Costing SystemsDocument4 pagesWeek Four: Costing SystemsNizam JewelNo ratings yet

- Smac Cheatsheet 2Document2 pagesSmac Cheatsheet 2Dries VanvoorenNo ratings yet

- Activity Based CostingDocument31 pagesActivity Based Costingwww.nickpicsplusNo ratings yet

- Group 4 - Cost AccountingDocument26 pagesGroup 4 - Cost Accounting20 Đặng Kiều Hoài PhươngNo ratings yet

- Lanen - Fundamentals of Cost Accounting - 6e - Chapter 9 - NotesDocument3 pagesLanen - Fundamentals of Cost Accounting - 6e - Chapter 9 - NotesRorNo ratings yet

- Activity Based CostingDocument12 pagesActivity Based CostingMuhammad Imran AwanNo ratings yet

- Review Chapter 1-2-4-18Document55 pagesReview Chapter 1-2-4-18hoangmyduyennguyen2004No ratings yet

- BA 116 / 1 Semester, AY 2013-2014 Activity-Based Costing (ABC) Systems: Handout #7Document2 pagesBA 116 / 1 Semester, AY 2013-2014 Activity-Based Costing (ABC) Systems: Handout #7Becky GonzagaNo ratings yet

- Activity-Based Costing and Management: Mcgraw-Hill/IrwinDocument41 pagesActivity-Based Costing and Management: Mcgraw-Hill/IrwinTruyện ĐọcNo ratings yet

- Chapter Three PDFDocument33 pagesChapter Three PDFSum AïyahNo ratings yet

- ACC2706 / ACC2002 Management Accounting Semester II, AY 2020/21Document51 pagesACC2706 / ACC2002 Management Accounting Semester II, AY 2020/21avNo ratings yet

- MS 3413 Activity-Based Costing SystemDocument5 pagesMS 3413 Activity-Based Costing SystemMonica GarciaNo ratings yet

- w5 ABC ShortDocument26 pagesw5 ABC ShortEugene TeoNo ratings yet

- Activity Based Costing - UNAMDocument32 pagesActivity Based Costing - UNAMWilhelmina KandjekeNo ratings yet

- Session - 5&6: Activity-Based Costing: PGP 2022-24 Prof. M. Shameem JawedDocument26 pagesSession - 5&6: Activity-Based Costing: PGP 2022-24 Prof. M. Shameem JawedAnkitShettyNo ratings yet

- Activity-Based CostingDocument49 pagesActivity-Based CostingJene LmNo ratings yet

- Knowing The Root Causes of Activity Costs Is The Key To Improvement of Cost Efficiency and InnovationDocument1 pageKnowing The Root Causes of Activity Costs Is The Key To Improvement of Cost Efficiency and InnovationJelay QuilatanNo ratings yet

- Brewer 8e PPT Ch04 TDocument36 pagesBrewer 8e PPT Ch04 TJuan Camilo IdarragaNo ratings yet

- Activity-Based Costing: Better Costing For Better DecisionsDocument25 pagesActivity-Based Costing: Better Costing For Better DecisionsArun KCNo ratings yet

- ABC CostingDocument35 pagesABC CostingShivangi JhawarNo ratings yet

- Costing Textbook CADocument294 pagesCosting Textbook CAAryan RajNo ratings yet

- Activity Based CostingDocument30 pagesActivity Based CostingGwenn VillamorNo ratings yet

- Activity Based CostingDocument36 pagesActivity Based CostingRashmeet Arora100% (1)

- Lesson ABCDocument15 pagesLesson ABCCj GarciaNo ratings yet

- ABC Costing PDFDocument33 pagesABC Costing PDFDrpranav SaraswatNo ratings yet

- Systems Design: Activity-Based Costing and Management: MANAGEMENT ACCOUNTING-Solutions ManualDocument15 pagesSystems Design: Activity-Based Costing and Management: MANAGEMENT ACCOUNTING-Solutions ManualBianca LizardoNo ratings yet

- Chapter Five: Activity-Based Costing (ABC) and Activity-Based Management (ABM)Document38 pagesChapter Five: Activity-Based Costing (ABC) and Activity-Based Management (ABM)Rangga PurnaNo ratings yet

- Activity-Based CostingDocument59 pagesActivity-Based CostinghanaNo ratings yet

- Activity-Based Costing: Better Costing For Better DecisionsDocument22 pagesActivity-Based Costing: Better Costing For Better DecisionsHasleen KaurNo ratings yet

- Activity Based CostingDocument4 pagesActivity Based CostingMaria Via Cristian MauricioNo ratings yet

- Chapter 5 Activity Based Costing - DO-unlockedDocument49 pagesChapter 5 Activity Based Costing - DO-unlockedtirupati phutelaNo ratings yet

- 10632m Lecture 6 - Full Costing I (Full Version)Document53 pages10632m Lecture 6 - Full Costing I (Full Version)kammiefan215No ratings yet

- Module Week 2b Acctg16Document18 pagesModule Week 2b Acctg16Andrea Florence Guy VidalNo ratings yet

- Activity-Based Costing: Questions For Writing and DiscussionDocument42 pagesActivity-Based Costing: Questions For Writing and DiscussionMaria Sarah SantosNo ratings yet

- Lecture 2Document22 pagesLecture 2An Nguyen Thai HongNo ratings yet

- ABC SystemsDocument15 pagesABC SystemsChristian TanNo ratings yet

- Cost Concepts HandoutDocument5 pagesCost Concepts HandoutNovilyn LeonardoNo ratings yet

- Cost Management Systems and Activity-Based Costing: Learning ObjectivesDocument15 pagesCost Management Systems and Activity-Based Costing: Learning ObjectivesIsaac Samy IsaacNo ratings yet

- Unit 9 Activity Based CostingDocument32 pagesUnit 9 Activity Based CostingjayitadebangiNo ratings yet

- Activity Based CostingDocument30 pagesActivity Based Costinghardik1302No ratings yet

- ABC CostingDocument39 pagesABC Costingtyagiaanya101No ratings yet

- Activity Based CostingDocument17 pagesActivity Based Costingvinati100% (2)

- Topic 2: Managing Costs - Activity-Based Costing ("ABC") : ACCT2522 Management Accounting For Decision AnalysisDocument58 pagesTopic 2: Managing Costs - Activity-Based Costing ("ABC") : ACCT2522 Management Accounting For Decision AnalysisFreda DengNo ratings yet

- ACTIVITY BASED COSTINGDocument58 pagesACTIVITY BASED COSTINGvangoorihome2No ratings yet

- Machine Setup: Activity-Based CostingDocument40 pagesMachine Setup: Activity-Based CostingJayson TasarraNo ratings yet

- Activity Based Costing (ABC)Document43 pagesActivity Based Costing (ABC)Snn News TubeNo ratings yet

- Overhead Costing and Activity Based Costing (W)Document11 pagesOverhead Costing and Activity Based Costing (W)Muhammad NaeemNo ratings yet

- Cost Management SystemDocument12 pagesCost Management SystemdianaNo ratings yet

- Solution Manual of Chapter 7 Managerial Accounting 15th Edition Ray H Garrison Eric W Noreen and Peter C BrewerDocument55 pagesSolution Manual of Chapter 7 Managerial Accounting 15th Edition Ray H Garrison Eric W Noreen and Peter C BrewerSEHA ÖZTÜRK100% (1)

- 15 Rizals 2nd Sojourn in Paris and The Universal Exposition of 1889Document12 pages15 Rizals 2nd Sojourn in Paris and The Universal Exposition of 1889Febbie Novem LavariasNo ratings yet

- 5 Medical Studies at USTDocument6 pages5 Medical Studies at USTFebbie Novem LavariasNo ratings yet

- 6 in Sunny SpainDocument15 pages6 in Sunny SpainFebbie Novem LavariasNo ratings yet

- 9 Rizals Grand Tour of Europe With Viola (1887)Document11 pages9 Rizals Grand Tour of Europe With Viola (1887)Febbie Novem LavariasNo ratings yet

- 20 Ophthalmic Surgeon in Hong Kong (1891-1892)Document10 pages20 Ophthalmic Surgeon in Hong Kong (1891-1892)Febbie Novem LavariasNo ratings yet

- Ra 1425Document4 pagesRa 1425Febbie Novem LavariasNo ratings yet

- 19 El Fili Published in GhentDocument9 pages19 El Fili Published in GhentFebbie Novem LavariasNo ratings yet

- 21 2nd Homecoming and The Liga FilipinaDocument6 pages21 2nd Homecoming and The Liga FilipinaFebbie Novem LavariasNo ratings yet

- 22 Exile in Dapitan 1892-1896Document13 pages22 Exile in Dapitan 1892-1896Febbie Novem LavariasNo ratings yet

- 17 Misfortunes in Madrid (1890-1891)Document7 pages17 Misfortunes in Madrid (1890-1891)Febbie Novem LavariasNo ratings yet

- 12 Romantic Interlude in JapanDocument8 pages12 Romantic Interlude in JapanFebbie Novem LavariasNo ratings yet

- 14 Rizal in LondonDocument11 pages14 Rizal in LondonFebbie Novem LavariasNo ratings yet

- 16 in Belgian Brussels (1890)Document9 pages16 in Belgian Brussels (1890)Febbie Novem LavariasNo ratings yet

- 1 Managerial Accounting and The Business EnvironmentDocument7 pages1 Managerial Accounting and The Business EnvironmentFebbie Novem LavariasNo ratings yet

- 13 Rizals Visit To The USADocument6 pages13 Rizals Visit To The USAFebbie Novem LavariasNo ratings yet

- Rizal and His Time PrologueDocument4 pagesRizal and His Time PrologueFebbie Novem LavariasNo ratings yet

- 2 Cost Volume Profit RelationshipsDocument34 pages2 Cost Volume Profit RelationshipsFebbie Novem LavariasNo ratings yet

- 4 Scholastic Triumphs at Ateneo de ManilaDocument10 pages4 Scholastic Triumphs at Ateneo de ManilaFebbie Novem LavariasNo ratings yet

- 11 in Hong Kong and MacaoDocument6 pages11 in Hong Kong and MacaoFebbie Novem LavariasNo ratings yet

- 7 Paris To BerlinDocument8 pages7 Paris To BerlinFebbie Novem LavariasNo ratings yet

- 8 Noli Me Tangere Published in BerlinDocument8 pages8 Noli Me Tangere Published in BerlinFebbie Novem LavariasNo ratings yet

- 10 First Homecoming 1887-1888Document12 pages10 First Homecoming 1887-1888Febbie Novem LavariasNo ratings yet

- 7 Standard Costs and VariancesDocument25 pages7 Standard Costs and VariancesFebbie Novem LavariasNo ratings yet

- 8 Performance Measurement in Decentralized OrganizationsDocument3 pages8 Performance Measurement in Decentralized OrganizationsFebbie Novem LavariasNo ratings yet

- 5 Profit PlanningDocument17 pages5 Profit PlanningFebbie Novem LavariasNo ratings yet

- 3 Early Education in Calamba and BinanDocument5 pages3 Early Education in Calamba and BinanFebbie Novem LavariasNo ratings yet

- 3 Variable Costing A Tool For ManagementDocument14 pages3 Variable Costing A Tool For ManagementFebbie Novem LavariasNo ratings yet

- 1 Advent of The National HeroDocument6 pages1 Advent of The National HeroFebbie Novem LavariasNo ratings yet

- 6 Flexible Budgets and Performance AnalysisDocument11 pages6 Flexible Budgets and Performance AnalysisFebbie Novem LavariasNo ratings yet

- A Public Relations ApproachDocument33 pagesA Public Relations Approachmona_13mera7931100% (2)

- Mos QuestionsDocument3 pagesMos QuestionsDurgesh AgnihotriNo ratings yet

- Statemant HSBCDocument1 pageStatemant HSBCVera DedkovskaNo ratings yet

- Barber & Odean - The Internet and The InvestorDocument14 pagesBarber & Odean - The Internet and The Investoronat85No ratings yet

- Basic FormulasDocument1 pageBasic FormulasDhanaperumal VarulaNo ratings yet

- Pricing Analytics: Creating Linear & Power Demand CurvesDocument48 pagesPricing Analytics: Creating Linear & Power Demand CurvesAbhijeetNo ratings yet

- Syllabus CPM DiplomaDocument6 pagesSyllabus CPM DiplomaGirman ranaNo ratings yet

- Impact of Using ICT - Agrani Bank BangladeshDocument37 pagesImpact of Using ICT - Agrani Bank BangladeshshafiulalamchowdhuryNo ratings yet

- Akansha Topani - No ShortcutsDocument3 pagesAkansha Topani - No Shortcutsakansha topaniNo ratings yet

- 1st Module AssessmentfmDocument6 pages1st Module AssessmentfmMansi GuptaNo ratings yet

- Quiz No 22 - TendersDocument5 pagesQuiz No 22 - TenderskanagarajodishaNo ratings yet

- The Success of The "Vive 100"Document2 pagesThe Success of The "Vive 100"JuanPabloJaramilloNo ratings yet

- Paper On VarDocument157 pagesPaper On VarHemendra GuptaNo ratings yet

- KSRMDocument2 pagesKSRMkahamedNo ratings yet

- Marketing Plan - SiantechDocument47 pagesMarketing Plan - SiantechAhmed NasrNo ratings yet

- Maceda Law Realty Installment Buyer Protection Act: Own House CondominiumDocument4 pagesMaceda Law Realty Installment Buyer Protection Act: Own House CondominiumsherwinNo ratings yet

- Macroeconomics EC2065 CHAPTER 6 - MONEY AND MONETARY POLICYDocument54 pagesMacroeconomics EC2065 CHAPTER 6 - MONEY AND MONETARY POLICYkaylaNo ratings yet

- Introduction To Human Resource ManagementDocument5 pagesIntroduction To Human Resource ManagementJe SacdalNo ratings yet

- Foreign Exchange Market: Presentation OnDocument19 pagesForeign Exchange Market: Presentation OnKavya lakshmikanthNo ratings yet

- Maceda Vs Energy Regulatory BoardDocument15 pagesMaceda Vs Energy Regulatory BoardJan Igor GalinatoNo ratings yet

- COMPAÑIA GENERAL DE TABACOS DE FILIPINAS Vs ManilaDocument2 pagesCOMPAÑIA GENERAL DE TABACOS DE FILIPINAS Vs ManilaLau NunezNo ratings yet

- ONGC - Stock Update 240921Document14 pagesONGC - Stock Update 240921Mohit MauryaNo ratings yet

- Bank AuditDocument16 pagesBank AuditThunderHeadNo ratings yet

- Resume 5Document3 pagesResume 5Zahid HussainNo ratings yet

- Unit 4. 21st Century Literacies C. Savings and Banking D. Avoiding Financial Scams I.Introduction / RationaleDocument10 pagesUnit 4. 21st Century Literacies C. Savings and Banking D. Avoiding Financial Scams I.Introduction / RationaleLance AustriaNo ratings yet

- Ax Blog 2Document293 pagesAx Blog 2pjanssen2306No ratings yet

- 304 Ope Som-Mcq-2019Document7 pages304 Ope Som-Mcq-2019Prafull P KulkarniNo ratings yet