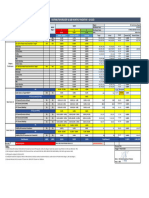

Final Mock Calculations

Final Mock Calculations

You might also like

- Wells Fargo Bank StatementDocument4 pagesWells Fargo Bank Statementalan benedetta50% (2)

- TD Business Premier Checking: Account SummaryDocument3 pagesTD Business Premier Checking: Account SummaryJohn Bean75% (4)

- Activity 1 Periodic - ARS MerchandisingDocument2 pagesActivity 1 Periodic - ARS MerchandisingElisa Landingin100% (2)

- Chapter 2 ExercisesDocument8 pagesChapter 2 ExercisesChoco PieNo ratings yet

- Simple Kriging DemoDocument6 pagesSimple Kriging Demokosaraju suhasNo ratings yet

- Sensitivity Analysis: Capital CostDocument4 pagesSensitivity Analysis: Capital CostZaini AhNo ratings yet

- Econ231W MWD ExampleDocument7 pagesEcon231W MWD ExampleMangapul Parmonangan DamanikNo ratings yet

- Chapter 3 ProblemsDocument7 pagesChapter 3 ProblemsShaila MarceloNo ratings yet

- Portfolio Diversification: Different Sectors UK - Japan - USA By: Alaa Hamwi, Shubhesh Goel, Vismita BanthiaDocument6 pagesPortfolio Diversification: Different Sectors UK - Japan - USA By: Alaa Hamwi, Shubhesh Goel, Vismita BanthiaShubhesh GoelNo ratings yet

- Wa0004.Document1 pageWa0004.prathamesh.kadam888No ratings yet

- Risk Hedging: Investment Analysis and Portfolio ManagementDocument16 pagesRisk Hedging: Investment Analysis and Portfolio ManagementPhuong Anh NguyenNo ratings yet

- Ho-Lee Binomial TreesDocument9 pagesHo-Lee Binomial TreesirsadNo ratings yet

- Jn91ao4yltxa4dcoqvqv7w17bivz6b 1Document2 pagesJn91ao4yltxa4dcoqvqv7w17bivz6b 1Vinay AgarwalNo ratings yet

- STAtis FixsDocument4 pagesSTAtis FixsYusron Nur HadiNo ratings yet

- Mulia Berkah - OctDocument1 pageMulia Berkah - OctNovita DpsNo ratings yet

- ReportDocument4 pagesReportLâm Bá ĐạtNo ratings yet

- Variance Covariance Matrix Mean Mins Mean Constan RetrunDocument5 pagesVariance Covariance Matrix Mean Mins Mean Constan RetrunQasim InayatNo ratings yet

- Calculos para Reporte 2 Material FragilDocument5 pagesCalculos para Reporte 2 Material FragilMORALES WILSON JAHIR VON QUEDNOWNo ratings yet

- Statistics Report: Output Filename: Statistik - Sap Sep 28, 2019Document3 pagesStatistics Report: Output Filename: Statistik - Sap Sep 28, 2019Khalid IkhsanuddinNo ratings yet

- Classwork w6 - David Pirih - d11210508Document24 pagesClasswork w6 - David Pirih - d11210508David Roderick PirihNo ratings yet

- AE9-Act.6-Measure of DispersionDocument4 pagesAE9-Act.6-Measure of Dispersionangelita aldayNo ratings yet

- Quality Engineering Report IIIDocument3 pagesQuality Engineering Report IIIKurtNo ratings yet

- Balanced - Dataset - Comparison: P-ValueDocument21 pagesBalanced - Dataset - Comparison: P-ValueChinniah DevarNo ratings yet

- CAPMDocument5 pagesCAPMRosalina Luisa Mayhuay AlvaroNo ratings yet

- Revisi ValidDocument12 pagesRevisi ValidirfanNo ratings yet

- Lampiran ReturnDocument12 pagesLampiran ReturnGus Suma Arta SevenmanNo ratings yet

- Calculos Petro BS Abril 2021Document2,371 pagesCalculos Petro BS Abril 2021fidel ZambranoNo ratings yet

- M SL SR Rotation V Moment RotationDocument4 pagesM SL SR Rotation V Moment RotationRavi SalimathNo ratings yet

- Statistics Report: Output Filename: Histogram Dec 11, 2018Document3 pagesStatistics Report: Output Filename: Histogram Dec 11, 2018ansarNo ratings yet

- Statistics Report: Output Filename: Fe Dec 13, 2018Document3 pagesStatistics Report: Output Filename: Fe Dec 13, 2018nurafniNo ratings yet

- LinPro PrintingDocument9 pagesLinPro PrintingtresspasseeNo ratings yet

- Mutual Fund AnalysisDocument21 pagesMutual Fund AnalysisRaman Kumar SinghNo ratings yet

- Answer of q1Document9 pagesAnswer of q1Afaq AhmedNo ratings yet

- Kurva Kalibrasi Larutan Standar C-Organik: 1. Penentuan LinieritasDocument4 pagesKurva Kalibrasi Larutan Standar C-Organik: 1. Penentuan Linieritasaprilia kurnia putriNo ratings yet

- Cu EstaDocument2 pagesCu EstaNando YarangaNo ratings yet

- Esfuerzo Vs Deformacion: Carga (lb) -P Elongaciòn (in) ΔL Esfuerzo (psi) σ Deformacion (in/in) εDocument3 pagesEsfuerzo Vs Deformacion: Carga (lb) -P Elongaciòn (in) ΔL Esfuerzo (psi) σ Deformacion (in/in) εAtilio Suàrez BardellineNo ratings yet

- Graph of Refractive Index Against Composition of EthanolDocument11 pagesGraph of Refractive Index Against Composition of EthanolchaitanyaNo ratings yet

- Soal 32Document2 pagesSoal 32HalimahNo ratings yet

- Let DESCRIBE Me For Futher Explaination in Detail (Near Future)Document30 pagesLet DESCRIBE Me For Futher Explaination in Detail (Near Future)AntenasmNo ratings yet

- Trabalho Metrologia - Aula 03Document10 pagesTrabalho Metrologia - Aula 03felipefeltreNo ratings yet

- Stock Expected Return DailyDocument35 pagesStock Expected Return DailyJustin NguyenNo ratings yet

- CapmDocument2 pagesCapmmaxdegroot321No ratings yet

- Pengolahan DataDocument12 pagesPengolahan Dataari antoNo ratings yet

- Annual Rate 13% Quarterly Rate 0.0325Document4 pagesAnnual Rate 13% Quarterly Rate 0.0325Maithri Vidana KariyakaranageNo ratings yet

- Probit Analysis: Mortallitas N Versus Konsentrasi: Response InformationDocument3 pagesProbit Analysis: Mortallitas N Versus Konsentrasi: Response InformationeristapfNo ratings yet

- Op2 Ejercicio y GraficoDocument6 pagesOp2 Ejercicio y GraficoAracely SerrudoNo ratings yet

- Each Element Is Devided by Column SumDocument3 pagesEach Element Is Devided by Column SumClutch And FlywheelNo ratings yet

- Each Element Is Devided by Column SumDocument3 pagesEach Element Is Devided by Column SumClutch And FlywheelNo ratings yet

- LAB RAÚL - DIODO .XLSBDocument4 pagesLAB RAÚL - DIODO .XLSBAriel AlbaezNo ratings yet

- Farha ProjectDocument18 pagesFarha ProjectBhavya PabbisettyNo ratings yet

- Rate of Reaction Chem IADocument3 pagesRate of Reaction Chem IAJessica SieNo ratings yet

- STATistics HomeworkDocument11 pagesSTATistics HomeworkGega XachidENo ratings yet

- Grafico Gaudin Schauman: Tamaño de ParticulaDocument7 pagesGrafico Gaudin Schauman: Tamaño de Particulaflorencio ramos montanoNo ratings yet

- PPP Investment StrategyDocument7 pagesPPP Investment StrategyAllur Sai Vijay KumarNo ratings yet

- Florensia Kristaveren 102316028 / CE1 Tugas Nanomaterial (Gambar 11)Document8 pagesFlorensia Kristaveren 102316028 / CE1 Tugas Nanomaterial (Gambar 11)Florensia KristaverenNo ratings yet

- Hardy CrossDocument2 pagesHardy CrossHugo ESCALANTENo ratings yet

- 0.029 F (X) 0.2133695052x - 0.1360856179 R 0.9952345266: Voltaje (V)Document4 pages0.029 F (X) 0.2133695052x - 0.1360856179 R 0.9952345266: Voltaje (V)Angie Mendoza VargasNo ratings yet

- Location Report 2018Document2 pagesLocation Report 2018Pierre D. LittleNo ratings yet

- GrafikDocument10 pagesGrafikaldino wijayaNo ratings yet

- Portfolio Performance PresentationDocument9 pagesPortfolio Performance Presentationharshwardhan.singh202No ratings yet

- Corporate Risk EstimatesDocument21 pagesCorporate Risk EstimatesRahul sardanaNo ratings yet

- InventoryDocument8 pagesInventorySandeep SatapathyNo ratings yet

- Monserrat2D Activity6 AE9Document5 pagesMonserrat2D Activity6 AE9Jerome MonserratNo ratings yet

- Without 351Document3 pagesWithout 351fadsNo ratings yet

- FINA 411 - W21 - F - C02 - Fin Mkts at Clss Fin InstDocument32 pagesFINA 411 - W21 - F - C02 - Fin Mkts at Clss Fin InstfadsNo ratings yet

- Fina 411 - w21 - F - c03 - How Sec Are TRDDocument24 pagesFina 411 - w21 - F - c03 - How Sec Are TRDfadsNo ratings yet

- Fina 411 - w21 - F - c01 - Invest EnvDocument27 pagesFina 411 - w21 - F - c01 - Invest EnvfadsNo ratings yet

- Fina 411 - w21 - F - c05 - Cap All Risk AtsDocument22 pagesFina 411 - w21 - F - c05 - Cap All Risk AtsfadsNo ratings yet

- Fina 411 - w21 - F - c04 - Ret Risk Hist RecDocument26 pagesFina 411 - w21 - F - c04 - Ret Risk Hist RecfadsNo ratings yet

- Business Finance: Quarter I (Week 5)Document12 pagesBusiness Finance: Quarter I (Week 5)clarisse ginez83% (6)

- Term Descriptions: Glossary of TermsDocument2 pagesTerm Descriptions: Glossary of TermsabdellaNo ratings yet

- Auditing: Text Book: Principles of Auditing by Khawaja Amjad SaeedDocument39 pagesAuditing: Text Book: Principles of Auditing by Khawaja Amjad SaeedShahoo Baloch100% (1)

- The Digital Fifth Fintech News 2nd June 2023Document25 pagesThe Digital Fifth Fintech News 2nd June 2023Vivek BandebucheNo ratings yet

- RA1 AccountsPDFDocument2 pagesRA1 AccountsPDFAnshita KohliNo ratings yet

- Functions of Financial SystemDocument2 pagesFunctions of Financial Systemrahulravi4u83% (53)

- Calculo Del COK v2Document16 pagesCalculo Del COK v2Liz AguilarNo ratings yet

- Rickards The Global Elites' Secret Plan For The Next Financial CrisisDocument4 pagesRickards The Global Elites' Secret Plan For The Next Financial CrisisOCHETE AMNo ratings yet

- Business Studies InsuranceDocument7 pagesBusiness Studies InsuranceAdish JainNo ratings yet

- Cpa Exam Digital BookletDocument20 pagesCpa Exam Digital BookletMaruf Hasan NirzhorNo ratings yet

- Dandot 2008 AnnualDocument39 pagesDandot 2008 AnnualMuhammad haseebNo ratings yet

- Liberty Medical Group Balance Sheet - Two-Year Comparison: AssetsDocument10 pagesLiberty Medical Group Balance Sheet - Two-Year Comparison: AssetsthrowawayyyNo ratings yet

- Ca3 Acc306 PankajDocument13 pagesCa3 Acc306 PankajPankaj MahantaNo ratings yet

- Personal Finance AppendixDocument27 pagesPersonal Finance AppendixBara DanielNo ratings yet

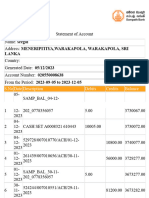

- Lanka: S.No Date Description Debits Credits BalanceDocument34 pagesLanka: S.No Date Description Debits Credits BalanceLasith IsuruNo ratings yet

- AIFs in GIFT IFSC Booklet October 2020Document12 pagesAIFs in GIFT IFSC Booklet October 2020Karthick JayNo ratings yet

- Mod Sub Inspector Challan FormDocument1 pageMod Sub Inspector Challan FormMuhammad Rɘʜʌŋ BakhshNo ratings yet

- Solution Manual For Auditing and Assurance Services 7Th Edition Louwers Blay Sinason Strawser Thibodeau 1259573281 9781259573286 Full Chapter PDFDocument36 pagesSolution Manual For Auditing and Assurance Services 7Th Edition Louwers Blay Sinason Strawser Thibodeau 1259573281 9781259573286 Full Chapter PDFlarry.mccoy970100% (19)

- CGAP Appraisal Report For The Selection of MFIs Along The SNNP Region of Ethiopia.Document31 pagesCGAP Appraisal Report For The Selection of MFIs Along The SNNP Region of Ethiopia.Diana Nabukenya KattoNo ratings yet

- The Future of Payments 2023Document64 pagesThe Future of Payments 2023Karim Jindani100% (1)

- UNIT II The Accounting Process Service and TradingDocument22 pagesUNIT II The Accounting Process Service and TradingAlezandra SantelicesNo ratings yet

- Technocrat Consultancy-Naya Rastriya-Niyatra JVDocument9 pagesTechnocrat Consultancy-Naya Rastriya-Niyatra JVBright Tone Music InstituteNo ratings yet

- History of Bear and Bull MarketsDocument1 pageHistory of Bear and Bull MarketscuntNo ratings yet

- Fire & Security Policy - ScheduleDocument3 pagesFire & Security Policy - Schedulekhalidalamoudy100% (1)

- Penanshin Shipping (Phils.) Inc.: Debit NoteDocument1 pagePenanshin Shipping (Phils.) Inc.: Debit NoteEnriquez Martinez May AnnNo ratings yet

Download as xlsx, pdf, or txt

You might also like

- Wells Fargo Bank StatementDocument4 pagesWells Fargo Bank Statementalan benedetta50% (2)

- TD Business Premier Checking: Account SummaryDocument3 pagesTD Business Premier Checking: Account SummaryJohn Bean75% (4)

- Activity 1 Periodic - ARS MerchandisingDocument2 pagesActivity 1 Periodic - ARS MerchandisingElisa Landingin100% (2)

- Chapter 2 ExercisesDocument8 pagesChapter 2 ExercisesChoco PieNo ratings yet

- Simple Kriging DemoDocument6 pagesSimple Kriging Demokosaraju suhasNo ratings yet

- Sensitivity Analysis: Capital CostDocument4 pagesSensitivity Analysis: Capital CostZaini AhNo ratings yet

- Econ231W MWD ExampleDocument7 pagesEcon231W MWD ExampleMangapul Parmonangan DamanikNo ratings yet

- Chapter 3 ProblemsDocument7 pagesChapter 3 ProblemsShaila MarceloNo ratings yet

- Portfolio Diversification: Different Sectors UK - Japan - USA By: Alaa Hamwi, Shubhesh Goel, Vismita BanthiaDocument6 pagesPortfolio Diversification: Different Sectors UK - Japan - USA By: Alaa Hamwi, Shubhesh Goel, Vismita BanthiaShubhesh GoelNo ratings yet

- Wa0004.Document1 pageWa0004.prathamesh.kadam888No ratings yet

- Risk Hedging: Investment Analysis and Portfolio ManagementDocument16 pagesRisk Hedging: Investment Analysis and Portfolio ManagementPhuong Anh NguyenNo ratings yet

- Ho-Lee Binomial TreesDocument9 pagesHo-Lee Binomial TreesirsadNo ratings yet

- Jn91ao4yltxa4dcoqvqv7w17bivz6b 1Document2 pagesJn91ao4yltxa4dcoqvqv7w17bivz6b 1Vinay AgarwalNo ratings yet

- STAtis FixsDocument4 pagesSTAtis FixsYusron Nur HadiNo ratings yet

- Mulia Berkah - OctDocument1 pageMulia Berkah - OctNovita DpsNo ratings yet

- ReportDocument4 pagesReportLâm Bá ĐạtNo ratings yet

- Variance Covariance Matrix Mean Mins Mean Constan RetrunDocument5 pagesVariance Covariance Matrix Mean Mins Mean Constan RetrunQasim InayatNo ratings yet

- Calculos para Reporte 2 Material FragilDocument5 pagesCalculos para Reporte 2 Material FragilMORALES WILSON JAHIR VON QUEDNOWNo ratings yet

- Statistics Report: Output Filename: Statistik - Sap Sep 28, 2019Document3 pagesStatistics Report: Output Filename: Statistik - Sap Sep 28, 2019Khalid IkhsanuddinNo ratings yet

- Classwork w6 - David Pirih - d11210508Document24 pagesClasswork w6 - David Pirih - d11210508David Roderick PirihNo ratings yet

- AE9-Act.6-Measure of DispersionDocument4 pagesAE9-Act.6-Measure of Dispersionangelita aldayNo ratings yet

- Quality Engineering Report IIIDocument3 pagesQuality Engineering Report IIIKurtNo ratings yet

- Balanced - Dataset - Comparison: P-ValueDocument21 pagesBalanced - Dataset - Comparison: P-ValueChinniah DevarNo ratings yet

- CAPMDocument5 pagesCAPMRosalina Luisa Mayhuay AlvaroNo ratings yet

- Revisi ValidDocument12 pagesRevisi ValidirfanNo ratings yet

- Lampiran ReturnDocument12 pagesLampiran ReturnGus Suma Arta SevenmanNo ratings yet

- Calculos Petro BS Abril 2021Document2,371 pagesCalculos Petro BS Abril 2021fidel ZambranoNo ratings yet

- M SL SR Rotation V Moment RotationDocument4 pagesM SL SR Rotation V Moment RotationRavi SalimathNo ratings yet

- Statistics Report: Output Filename: Histogram Dec 11, 2018Document3 pagesStatistics Report: Output Filename: Histogram Dec 11, 2018ansarNo ratings yet

- Statistics Report: Output Filename: Fe Dec 13, 2018Document3 pagesStatistics Report: Output Filename: Fe Dec 13, 2018nurafniNo ratings yet

- LinPro PrintingDocument9 pagesLinPro PrintingtresspasseeNo ratings yet

- Mutual Fund AnalysisDocument21 pagesMutual Fund AnalysisRaman Kumar SinghNo ratings yet

- Answer of q1Document9 pagesAnswer of q1Afaq AhmedNo ratings yet

- Kurva Kalibrasi Larutan Standar C-Organik: 1. Penentuan LinieritasDocument4 pagesKurva Kalibrasi Larutan Standar C-Organik: 1. Penentuan Linieritasaprilia kurnia putriNo ratings yet

- Cu EstaDocument2 pagesCu EstaNando YarangaNo ratings yet

- Esfuerzo Vs Deformacion: Carga (lb) -P Elongaciòn (in) ΔL Esfuerzo (psi) σ Deformacion (in/in) εDocument3 pagesEsfuerzo Vs Deformacion: Carga (lb) -P Elongaciòn (in) ΔL Esfuerzo (psi) σ Deformacion (in/in) εAtilio Suàrez BardellineNo ratings yet

- Graph of Refractive Index Against Composition of EthanolDocument11 pagesGraph of Refractive Index Against Composition of EthanolchaitanyaNo ratings yet

- Soal 32Document2 pagesSoal 32HalimahNo ratings yet

- Let DESCRIBE Me For Futher Explaination in Detail (Near Future)Document30 pagesLet DESCRIBE Me For Futher Explaination in Detail (Near Future)AntenasmNo ratings yet

- Trabalho Metrologia - Aula 03Document10 pagesTrabalho Metrologia - Aula 03felipefeltreNo ratings yet

- Stock Expected Return DailyDocument35 pagesStock Expected Return DailyJustin NguyenNo ratings yet

- CapmDocument2 pagesCapmmaxdegroot321No ratings yet

- Pengolahan DataDocument12 pagesPengolahan Dataari antoNo ratings yet

- Annual Rate 13% Quarterly Rate 0.0325Document4 pagesAnnual Rate 13% Quarterly Rate 0.0325Maithri Vidana KariyakaranageNo ratings yet

- Probit Analysis: Mortallitas N Versus Konsentrasi: Response InformationDocument3 pagesProbit Analysis: Mortallitas N Versus Konsentrasi: Response InformationeristapfNo ratings yet

- Op2 Ejercicio y GraficoDocument6 pagesOp2 Ejercicio y GraficoAracely SerrudoNo ratings yet

- Each Element Is Devided by Column SumDocument3 pagesEach Element Is Devided by Column SumClutch And FlywheelNo ratings yet

- Each Element Is Devided by Column SumDocument3 pagesEach Element Is Devided by Column SumClutch And FlywheelNo ratings yet

- LAB RAÚL - DIODO .XLSBDocument4 pagesLAB RAÚL - DIODO .XLSBAriel AlbaezNo ratings yet

- Farha ProjectDocument18 pagesFarha ProjectBhavya PabbisettyNo ratings yet

- Rate of Reaction Chem IADocument3 pagesRate of Reaction Chem IAJessica SieNo ratings yet

- STATistics HomeworkDocument11 pagesSTATistics HomeworkGega XachidENo ratings yet

- Grafico Gaudin Schauman: Tamaño de ParticulaDocument7 pagesGrafico Gaudin Schauman: Tamaño de Particulaflorencio ramos montanoNo ratings yet

- PPP Investment StrategyDocument7 pagesPPP Investment StrategyAllur Sai Vijay KumarNo ratings yet

- Florensia Kristaveren 102316028 / CE1 Tugas Nanomaterial (Gambar 11)Document8 pagesFlorensia Kristaveren 102316028 / CE1 Tugas Nanomaterial (Gambar 11)Florensia KristaverenNo ratings yet

- Hardy CrossDocument2 pagesHardy CrossHugo ESCALANTENo ratings yet

- 0.029 F (X) 0.2133695052x - 0.1360856179 R 0.9952345266: Voltaje (V)Document4 pages0.029 F (X) 0.2133695052x - 0.1360856179 R 0.9952345266: Voltaje (V)Angie Mendoza VargasNo ratings yet

- Location Report 2018Document2 pagesLocation Report 2018Pierre D. LittleNo ratings yet

- GrafikDocument10 pagesGrafikaldino wijayaNo ratings yet

- Portfolio Performance PresentationDocument9 pagesPortfolio Performance Presentationharshwardhan.singh202No ratings yet

- Corporate Risk EstimatesDocument21 pagesCorporate Risk EstimatesRahul sardanaNo ratings yet

- InventoryDocument8 pagesInventorySandeep SatapathyNo ratings yet

- Monserrat2D Activity6 AE9Document5 pagesMonserrat2D Activity6 AE9Jerome MonserratNo ratings yet

- Without 351Document3 pagesWithout 351fadsNo ratings yet

- FINA 411 - W21 - F - C02 - Fin Mkts at Clss Fin InstDocument32 pagesFINA 411 - W21 - F - C02 - Fin Mkts at Clss Fin InstfadsNo ratings yet

- Fina 411 - w21 - F - c03 - How Sec Are TRDDocument24 pagesFina 411 - w21 - F - c03 - How Sec Are TRDfadsNo ratings yet

- Fina 411 - w21 - F - c01 - Invest EnvDocument27 pagesFina 411 - w21 - F - c01 - Invest EnvfadsNo ratings yet

- Fina 411 - w21 - F - c05 - Cap All Risk AtsDocument22 pagesFina 411 - w21 - F - c05 - Cap All Risk AtsfadsNo ratings yet

- Fina 411 - w21 - F - c04 - Ret Risk Hist RecDocument26 pagesFina 411 - w21 - F - c04 - Ret Risk Hist RecfadsNo ratings yet

- Business Finance: Quarter I (Week 5)Document12 pagesBusiness Finance: Quarter I (Week 5)clarisse ginez83% (6)

- Term Descriptions: Glossary of TermsDocument2 pagesTerm Descriptions: Glossary of TermsabdellaNo ratings yet

- Auditing: Text Book: Principles of Auditing by Khawaja Amjad SaeedDocument39 pagesAuditing: Text Book: Principles of Auditing by Khawaja Amjad SaeedShahoo Baloch100% (1)

- The Digital Fifth Fintech News 2nd June 2023Document25 pagesThe Digital Fifth Fintech News 2nd June 2023Vivek BandebucheNo ratings yet

- RA1 AccountsPDFDocument2 pagesRA1 AccountsPDFAnshita KohliNo ratings yet

- Functions of Financial SystemDocument2 pagesFunctions of Financial Systemrahulravi4u83% (53)

- Calculo Del COK v2Document16 pagesCalculo Del COK v2Liz AguilarNo ratings yet

- Rickards The Global Elites' Secret Plan For The Next Financial CrisisDocument4 pagesRickards The Global Elites' Secret Plan For The Next Financial CrisisOCHETE AMNo ratings yet

- Business Studies InsuranceDocument7 pagesBusiness Studies InsuranceAdish JainNo ratings yet

- Cpa Exam Digital BookletDocument20 pagesCpa Exam Digital BookletMaruf Hasan NirzhorNo ratings yet

- Dandot 2008 AnnualDocument39 pagesDandot 2008 AnnualMuhammad haseebNo ratings yet

- Liberty Medical Group Balance Sheet - Two-Year Comparison: AssetsDocument10 pagesLiberty Medical Group Balance Sheet - Two-Year Comparison: AssetsthrowawayyyNo ratings yet

- Ca3 Acc306 PankajDocument13 pagesCa3 Acc306 PankajPankaj MahantaNo ratings yet

- Personal Finance AppendixDocument27 pagesPersonal Finance AppendixBara DanielNo ratings yet

- Lanka: S.No Date Description Debits Credits BalanceDocument34 pagesLanka: S.No Date Description Debits Credits BalanceLasith IsuruNo ratings yet

- AIFs in GIFT IFSC Booklet October 2020Document12 pagesAIFs in GIFT IFSC Booklet October 2020Karthick JayNo ratings yet

- Mod Sub Inspector Challan FormDocument1 pageMod Sub Inspector Challan FormMuhammad Rɘʜʌŋ BakhshNo ratings yet

- Solution Manual For Auditing and Assurance Services 7Th Edition Louwers Blay Sinason Strawser Thibodeau 1259573281 9781259573286 Full Chapter PDFDocument36 pagesSolution Manual For Auditing and Assurance Services 7Th Edition Louwers Blay Sinason Strawser Thibodeau 1259573281 9781259573286 Full Chapter PDFlarry.mccoy970100% (19)

- CGAP Appraisal Report For The Selection of MFIs Along The SNNP Region of Ethiopia.Document31 pagesCGAP Appraisal Report For The Selection of MFIs Along The SNNP Region of Ethiopia.Diana Nabukenya KattoNo ratings yet

- The Future of Payments 2023Document64 pagesThe Future of Payments 2023Karim Jindani100% (1)

- UNIT II The Accounting Process Service and TradingDocument22 pagesUNIT II The Accounting Process Service and TradingAlezandra SantelicesNo ratings yet

- Technocrat Consultancy-Naya Rastriya-Niyatra JVDocument9 pagesTechnocrat Consultancy-Naya Rastriya-Niyatra JVBright Tone Music InstituteNo ratings yet

- History of Bear and Bull MarketsDocument1 pageHistory of Bear and Bull MarketscuntNo ratings yet

- Fire & Security Policy - ScheduleDocument3 pagesFire & Security Policy - Schedulekhalidalamoudy100% (1)

- Penanshin Shipping (Phils.) Inc.: Debit NoteDocument1 pagePenanshin Shipping (Phils.) Inc.: Debit NoteEnriquez Martinez May AnnNo ratings yet